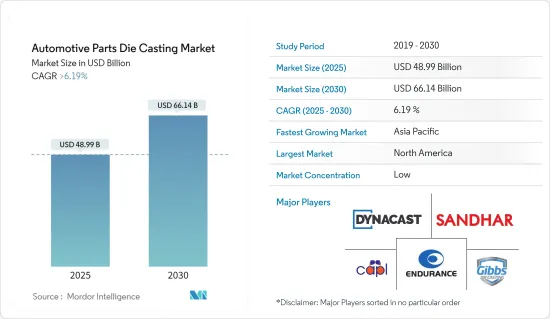

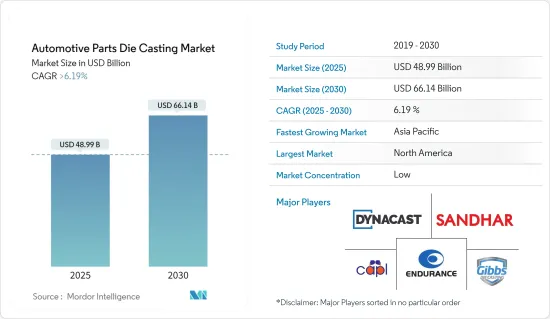

세계의 자동차 부품 다이캐스팅 시장 규모는 2025년 489억 9,000만 달러로 추정되며, 예측기간 중(2025-2030년) CAGR 6.19%를 넘고, 2030년에는 661억 4,000만 달러에 달할 것으로 예측됩니다.

자동차 부품 다이캐스팅 시장은 주로 자동차의 경량화로의 세계 변화와 전기자동차의 인기가 높아짐에 따라 큰 성장을 이루고 있습니다. 자동차 경량화의 추세는 세계 환경 규제와 지속가능성 목표에 맞추어 연비를 개선하고 이산화탄소 배출량을 줄일 필요성 때문입니다. 특히 전기자동차는 가볍고 견고한 복잡하고 고정밀 부품이 필요하며, 다이 캐스팅은 이러한 요구를 충족시키는 이상적인 프로세스입니다.

예를 들어, 자동차 배출 가스를 줄이고 연비를 개선하기 위한 CAFE 기준과 EPA 정책은 자동차 제조업체를 경량 비철금속을 사용하여 자동차 경량화를 추진하고 있습니다. EPA가 2025년까지 마일/갤런(mpg) 기준을 54.5mpg로 끌어올리려는 움직임은 다이캐스팅 업계를 지원하고 있습니다. 그 결과, 경량화 전략으로서 다이캐스팅 부품을 사용하는 것이 시장의 주요 촉진요인이 되고 있습니다.

또한 다이캐스팅 기술의 발전이 시장 확대에 크게 기여하고 있습니다. 기계 설계, 공정 제어 및 금형 기술의 혁신은 다이캐스팅 작업의 효율성과 품질을 향상시킵니다. 이러한 기술 개선은 주조 부품의 정확성과 강도를 향상시키고, 폐기물과 에너지 소비를 줄이고, 공정을 보다 친환경적이고 비용 효율적입니다. 컴퓨터 지원 엔지니어링(CAE) 및 사물 인터넷(IoT)과 같은 자동화와 디지털 기술의 통합은 다이캐스팅 프로세스를 최적화하여 리드 타임을 단축하고 생산성을 향상시킵니다.

또한 다이 캐스팅의 다양성은 복잡한 엔진 부품, 변속기 시스템 및 구조 요소를 포함한 광범위한 자동차 부품의 생산을 가능하게합니다. 고압 다이캐스팅(HPDC)은 고속 생산 능력과 높은 치수 정밀도로 복잡한 형상을 생산할 수 있는 능력을 제공하며, 저명한 기술로 등장해 왔습니다. 게다가 진공 다이캐스팅은 뛰어난 기계적 특성과 최소의 기공률로 부품을 생산하는 능력으로 자동차 부품의 품질과 내구성을 더욱 높일 수 있기 때문에 인기를 끌고 있습니다.

자동차 제조업체가 엄격한 배기가스 규제를 충족하고 EV의 배터리 항속 거리를 향상시키기 위해 차량의 경량화에 점점 힘을 가할수록 혁신적인 다이캐스팅 솔루션 수요가 급증할 것으로 예상됩니다. 이러한 이유로 자동차 산업의 진화하는 요구 사항을 충족시키기 위해 새로운 합금 개발 및 주조 기술 강화와 같은 재료 및 공정의 추가 발전이 예상됩니다.

압력 다이캐스팅은 생산 유형에 따라 가장 큰 카테고리입니다. 압력 다이캐스팅은 효율적이고 대량 생산이 가능하고 복잡하고 내구성 있는 부품을 생산할 수 있기 때문에 자동차 부품 다이캐스팅 시장을 독점하고 있습니다.

가압 다이캐스팅은 주로 완벽한 표면 마무리가 있는 대량의 복잡한 부품을 제조하는 데 뛰어나므로 자동차 부품 다이 캐스팅 시장에서 매우 중요한 위치를 차지합니다. 또한 고압 다이캐스팅(HPDC)은 대형 자동차 부품 생산에 점점 더 많이 사용되고 있습니다.

Tesla와 같은 주요 자동차 회사는 자동차 프론트엔드 및 리어 엔드와 같은 중요한 부품을 단일 부품으로 제조하기 위해 HPDC를 활용합니다. HPDC의 이 응용은 자동차 제조 공정의 효율성과 지속가능성을 크게 발전시켰습니다. 예를 들어, HPDC는 70-100개의 부품을 단일 부품으로 대체할 수 있어 생산 복잡성을 극적으로 줄여 전체 효율을 향상시킵니다.

압력 다이캐스팅의 점유율이 가장 큰 반면, 진공 다이캐스팅은 제조된 부품의 품질과 강도를 향상시키는 능력에 의해 자동차 부품 다이캐스팅 시장에서 가장 빠르게 성장하는 부문으로 부상할 것으로 예상됩니다. 이 성장 궤도는 주조 공정 동안 공기의 권선을 완화시켜 구조적 무결성을 향상시킨 부품의 제조를 보장하는 이 기술의 본질적인 이점을 뒷받침합니다.

게다가 진공 다이캐스팅은 다공성을 현저하게 감소시켜 보다 고밀도로 견고한 자동차 부품을 생산합니다. 이 특성은 우수한 품질과 강도를 양보할 수 없는 중요한 자동차 부품의 제조에 점점 더 요구되고 있습니다. 게다가, 이 방법은 고품질의 내구성을 가진 부품의 제조에 뛰어나기 때문에 특히 높은 신뢰성과 성능 기준을 필요로 하는 부품의 제조에 있어서 진화하는 자동차 제조 섹터에 필수적인 기술로 자리매김하고 있습니다.

아시아태평양은 인도, 중국, 일본 등 주요 국가의 존재로 시장에서 지배적인 역할을 할 것으로 예상됩니다. 중국은 다이캐스팅 부품의 주요 생산국 중 하나이며 아시아태평양의 다이캐스팅 시장 점유율의 60% 이상을 차지하고 있습니다.

아시아태평양이 자동차 부품 다이캐스팅 시장을 선도하는 이유는 중국과 인도가 크게 기여하고 있기 때문입니다. 이것은 성장하는 자동차 산업, 높은 자동차 생산 대수, 이 지역을 거점으로 하는 대기업 자동차 제조업체에 의한 것입니다.

2022년 아시아태평양에서는 3,500만 대 이상의 자동차가 생산되었으며 중국에서만 2,700만 대의 자동차가 생산되었습니다. 중국에 이어 일본은 780만대 이상, 인도는 540만대 이상의 자동차를 생산했습니다. 게다가 2022년 동지역의 상용차 판매 대수는 전체적으로 660만대를 넘어 중국만으로 330만대 이상이 판매되었습니다.

게다가 아시아태평양은 자동차 산업의 성장에 호의적인 정부 정책에 의해 강화된 정착된 제조 인프라로부터 강점을 얻어 세계의 맥락에서 주도적 지위를 확고히 하고 있습니다. 새로운 제조 기술과 저연비 차량에 대한 주력 등의 요인이 시장을 형성하고 있습니다.

또한 중간층의 부유화가 시장 성장에 긍정적인 영향을 미치고 있습니다. 이 지역에서는 청정 에너지 차량과 환경 문제에 대한 정부 정책을 배경으로 전기자동차와 하이브리드 자동차와 같은 첨단 자동차 기술이 시장을 견인하고 있습니다. 급성장과 기술 진보를 특징으로 하는 아시아태평양의 이러한 진화하는 시장 환경은 세계 자동차 부품 다이캐스팅 업계를 더욱 견인할 것으로 예상됩니다.

다이캐스팅 세계 시장은 단편화되어 있으며, 신흥국 시장에서도 많은 지역 중소규모의 기업이 참가하고 있습니다. Nemak, Georg Fischer Automotive, Ryobi Die casting, Rheinmetall AG, Form Technologies Inc.(Dynacast), Shiloh Industries 등 인지도가 높은 주요 기업이 세계 시장 점유율의 16% 이상을 차지하고 있습니다. 이러한 주요 기업들은 더 나은 자동차 부품을 위한 생산 공정과 합금을 개발하기 위해 연구 개발에 수익을 집중하고 있습니다. 예를 들면

The Automotive Parts Die Casting Market size is estimated at USD 48.99 billion in 2025, and is expected to reach USD 66.14 billion by 2030, at a CAGR of greater than 6.19% during the forecast period (2025-2030).

The automotive parts die casting market is experiencing significant growth, primarily driven by the global shift toward lightweight vehicles and the increasing popularity of electric vehicles. This trend toward lighter vehicles arises from the need to improve fuel efficiency and reduce carbon emissions, aligning with global environmental regulations and sustainability goals. Electric vehicles, in particular, require complex, high-precision components that are both lightweight and sturdy, and die casting is an ideal process to meet these demands.

For instance, CAFE standards and EPA policies to reduce automobile emissions and increase fuel efficiency are driving automobile manufacturers to reduce the weight of the automobile by using lightweight, non-ferrous metals. The move by the EPA to raise the miles per gallon (mpg) standards to 54.5 mpg by 2025 has helped the die casting industry, as the only way to get to those mileage standards is by manufacturing lightweight vehicles. Subsequently, using die cast parts as a weight-reduction strategy is a major driver for the market.

Further, advancements in die casting technology are significantly contributing to the expansion of the market. Innovations in machine design, process control, and mold technologies improve the efficiency and quality of die casting operations. These technological improvements increase the precision and strength of the cast parts and reduce waste and energy consumption, making the process more environmentally friendly and cost-effective. Integrating automation and digital technologies, such as computer-aided engineering (CAE) and the Internet of Things (IoT), optimizes the die casting process, leading to reduced lead times and increased productivity.

Moreover, the versatility of die casting allows for the production of a wide range of automotive parts, including intricate engine components, transmission systems, and structural elements. High-pressure die casting (HPDC) has emerged as a prominent technology, offering high-speed production capabilities and the ability to produce complex shapes with high dimensional accuracy. Moreover, vacuum die casting is gaining traction due to its ability to produce parts with superior mechanical properties and minimal porosity, further enhancing the quality and durability of automotive components.

As vehicle manufacturers increasingly focus on reducing vehicle weight to meet stringent emission standards and improve battery range in EVs, the demand for innovative die casting solutions is expected to surge. This is likely to lead to further advancements in materials and processes, such as the development of new alloys and enhanced casting techniques, to meet the evolving requirements of the automotive industry.

Pressure die casting is the largest category based on production type. Pressure die casting dominates the automotive parts die casting market with its efficient, high-volume, intricate, and durable components production.

Pressure die casting has been pivotal in the automotive parts die casting market, primarily due to its proficiency in fabricating high-volume, complex parts with perfect surface finish. Additionally, high-pressure die casting (HPDC) is increasingly used to produce large auto parts.

Major automotive companies like Tesla are utilizing HPDC to manufacture significant components, such as the front and rear ends of vehicles, as single parts. This application of HPDC has led to significant advancements in the efficiency and sustainability of automotive manufacturing processes. For instance, HPDC allows for replacing 70 to 100 parts with a single part, drastically reducing production complexity and improving overall efficiency.

While pressure die casting has the largest share, vacuum die casting is expected to emerge as the fastest-growing segment in the automotive parts die casting market, driven by its ability to enhance the quality and strength of manufactured components. This growth trajectory is underpinned by the technology's intrinsic advantage in mitigating air entrapment during the casting process, thereby ensuring the production of components with enhanced structural integrity.

Further, vacuum die-casting significantly reduces porosity, creating denser and more robust automotive parts. This attribute is increasingly sought in producing critical automotive components, where superior quality and strength are non-negotiable. Moreover, the method's proficiency in manufacturing high-quality, durable parts positions it as an indispensable technology in the evolving automotive manufacturing sector, particularly for components that require higher reliability and performance standards.

The Asia-Pacific region is expected to play a dominant role in the market owing to the presence of key countries like India, China, and Japan. China is one of the major producers of die casting parts, accounting for more than 60% of the regional (Asia-Pacific) die casting market share.

The Asia-Pacific region leads in the automotive parts die casting market because of significant contributions from China and India. This is due to their growing car industry, high vehicle production, and major car manufacturers based there.

In 2022, over 35 million vehicles were produced in Asia-Pacific, with China accounting for 27 million motor vehicles alone. China was followed by Japan and India, which produced over 7.8 million and 5.4 million motor vehicles, respectively. Additionally, the overall commercial vehicle sales in the region in 2022 were registered at over 6.6 million units; over 3.3 million units were sold in China alone.

Moreover, the Asia-Pacific region derives strength from a well-entrenched manufacturing infrastructure, augmented by government policies favorably inclined toward the automotive industry's growth, thereby cementing its leadership position in the global context. Factors such as new manufacturing technologies and a focus on fuel-efficient cars shape the market.

The increasing wealth of the middle class also positively impacts the market growth. The region's push for advanced car technologies like electric and hybrid vehicles, backed by government policies for clean energy vehicles and environmental concerns, drives the market. This evolving market environment in Asia-Pacific, marked by rapid growth and technological advancements, is expected to drive the global automotive parts further die casting industry.

The global market for die casting is fragmented, with many regional small-medium scale players from developing countries entering the market. Major recognized players, such as Nemak, Georg Fischer Automotive, Ryobi Die casting, Rheinmetall AG, Form Technologies Inc. (Dynacast), and Shiloh Industries, accounted for over 16% of the global market share. These key players have focused their revenues on R&D to develop better production processes and alloys for automotive parts. For instance,