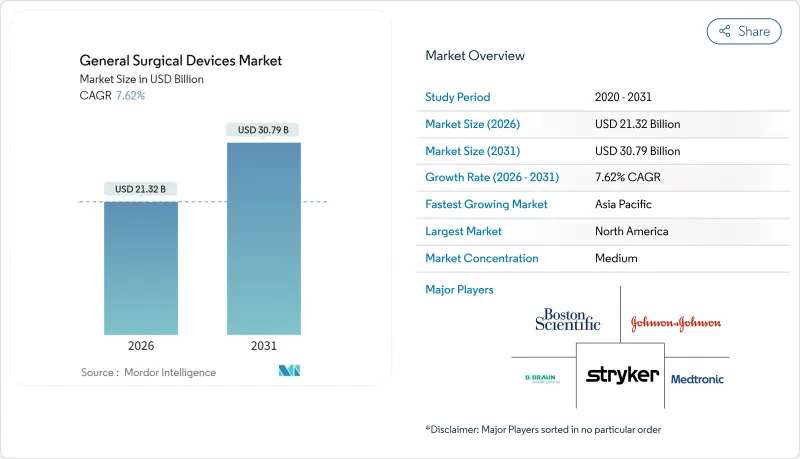

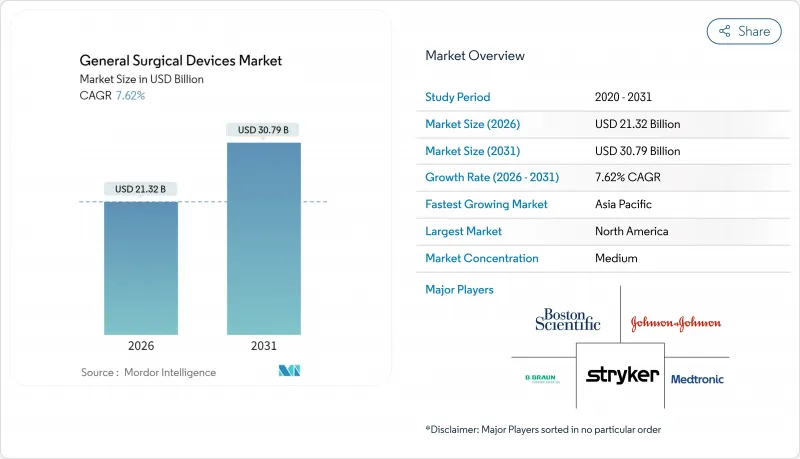

일반 외과용 기기 시장은 2025년 198억 1,000만 달러로 평가되었으며, 2026년 213억 2,000만 달러에서 2031년까지 307억 9,000만 달러에 이를 것으로 예상됩니다.

예측 기간(2026-2031년)에 있어서 CAGR은 7.62%를 나타낼 전망입니다.

이 성장의 기세는 수술 건수 증가, 저침습 기술의 급속한 보급, 회복 기간의 단축과 합병증률의 저감을 목표로 하는 지속적인 제품 혁신에 기인하고 있습니다. 북미는 선진적인 인프라와 유리한 상환제도로 일반 외과용 기기 시장을 선도하고 있는 한편 아시아태평양은 정부에 의한 병원 수용 능력의 확대와 민간 사업자에 의한 외래 진료 시설 증가에 따라 가장 급속한 성장을 보이고 있습니다. 감염 관리 규칙이 단일 사용 기구를 권장하기 때문에 일회용 소모품이 여전히 주류를 차지하고 있지만, 로봇 플랫폼의 급속한 보급은 업계가 정밀성으로 축 발을 옮기고 있음을 보여줍니다. 경쟁의 격화가 진행되고 있습니다. 대형 복합기업이 시장 점유율을 지키려고 하는 한편, 틈새 기술을 시장에 투입하는 전문성이 높은 신규 참가 기업이 대두하고 있는 상황입니다.

로봇 내비게이션 시스템, 전용 액세스 포트, 고급 영상 진단 기술의 조합으로 외과의사는 조직 손상을 줄일 수 있어 입원 기간이 2-3일 단축되어 환자의 직장 복귀까지의 기간이 반감됩니다. 정형외과 분야에서는 이러한 전환이 현저하고, 2024년에는 대상 수술의 68%로 이미 MIS가 채용되었으며, 스트라이커사의 Mako SmartRobotics 플랫폼은 수술 중 가력을 43% 삭감했습니다. 심장혈관 수술, 부인과 및 뇌 신경 수술에서도 기존 워크 플로우에 맞는 단일 포트 및 카테터 기반 솔루션이 기기 제조업체에서 추가됨에 따라 비슷한 변화가 나타납니다. 경제적 이점은 도입을 뒷받침합니다. 재입원률 감소와 병상 해방은 병원이 가치 기반 지불 목표 달성을 가능하게 하여 MIS 대응 시스템의 도입을 더욱 촉진합니다. 의료 시스템이 전통적인 수술에서 낮은 침습 수술로 전환하는 동안 이러한 요인이 결합되어 일반 외과용 기기 시장은 견조한 확장 경로를 유지할 것입니다.

인공지능은 현재 수술 전 계획, 수술 중 지침, 수술 후 모니터링을 지원합니다. 미시간 대학과 캘리포니아 대학 샌프란시스코의 공동 개발 모델 "FastGlioma"는 잔존 뇌종양 조직을 92%의 정확도로 확인하여 놓치는 비율을 25%에서 3.8%로 줄였습니다. MySurgeryRisk와 같은 예측 엔진은 기존 평가 기법을 능가하며 합병증 발생률을 최대 30%까지 줄입니다. 이러한 툴을 도입한 병원에서는 집중치료실(ICU) 체재일수가 감소해, 보험자측도 코스트 삭감 효과를 확인. 이에 따라 AI는 시험 도입 단계에서 일상적인 조달 품목으로 이행하고 있습니다. 알고리즘이 콘솔이나 내시경에 내장되어 있는 가운데, 벤더 각사는 기계적 기능 뿐만 아니라 데이터 파이프라인에 의한 차별화를 도모하고 있어 이것도 일반 외과용 기기 시장에서의 지속적인 수요를 지지하는 새로운 진화입니다.

고급 로봇 수술 시스템과 영상 진단 제품군은 수술실당 200만 달러를 초과하는 투자를 필요로 하며, 중소득 국가에서는 표준 예산 사이클을 초과하는 회수 기간이 장벽이 됩니다. 유지 보수 계약, 소프트웨어 업데이트 및 소모품은 총 소유 비용을 밀어 올려 명백한 임상 적 이점에도 불구하고 도입을 억제합니다. 이 때문에 벤더 각사는 일반 외과용 기기 시장을 소득 계층을 넘어 이용 가능하게 유지하기 위해 비용 효율화 시스템과 종량 과금 모델이 주목을 받고 있습니다.

2025년에는 감염 관리 프로토콜이 일회용 드레이프, 트로칼 및 블레이드를 권장했기 때문에 일회용 수술용 소모품이 가장 큰 수익 점유율을 창출했습니다. 일반 외과용 기기 시장 규모의 43.78%를 차지하는 이 비율은 병원이 병원이 병원이 감염 지표를 추적할 때 표준화를 선호한다는 것을 나타냅니다. 그러나 지속가능성에 대한 노력이 저위험 사례에서의 선택적 재사용을 촉진하기 때문에 부문의 성장률은 적당한 단일 자릿수로 수렴할 것으로 예측됩니다. 이 미묘한 변화가 조달 가이드 라인을 재구성하면서도 일회용 제품의 최고 위치는 흔들리지 않습니다.

절대액으로는 소규모이지만, 로봇 지원 기구는 2031년까지 연평균 복합 성장률(CAGR) 10.62%로 다른 카테고리를 능가할 전망입니다. 고관절 재치환술, 부분 무릎 관절 치환술, 연부 조직 수술용으로 설계된 시스템이 적응증을 넓히고 습득 기간을 단축하고 있습니다. 처리 능력 향상으로 초기 투자가 상쇄되기 때문에 관리자는 로봇을 위신을 위한 구매가 아니라 생산성 향상 도구로 파악하고 있습니다. 이 추세는 일반 외과용 기기 시장의 지속적인 성장을 시사합니다.

북미는 2025년 수익의 37.45%를 차지하며 높은 수술 건수, 로봇 기술의 급속한 보급, 지원적인 상환 제도에 지지되었습니다. 미국은 밀집한 혁신 생태계의 혜택을 누리고 있지만 스테이플러 및 전기 수술 기기 시장 포화로 인해 성장은 소프트웨어 강화 시스템과 AI 모듈에 의존하는 경향이 커지고 있습니다. 캐나다에서는 가치 기반 의료로의 전환이 진행되고 병원이 기기의 성능을 엄격하게 추적하도록 촉구되고 있으며, 이러한 동향은 일반 외과용 기기 시장 전체의 조달에도 파급될 전망입니다.

유럽은 2위 규모를 유지하고 의료기기 규칙(MDR)에 근거한 엄격한 적합성 평가에도 불구하고 꾸준한 확대를 계속하고 있습니다. 독일, 영국, 프랑스가 도입을 주도하고 있으며, 특히 인공 관절 치환 로봇과 고도 화상 진단 기기 수요가 현저합니다. 남유럽·동유럽 국가에서는 시설 갱신이 진행되어 중가격대 솔루션의 새로운 판로가 창출되고 있습니다. 환율 변동이나 예산 제약은 여전히 과제이지만, 규격의 조화화에 의해 일반 외과용 기기 시장 내에서의 국경 상업화가 촉진되고 있습니다.

아시아태평양은 10.15%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 지역입니다. 중국은 현 수준의 병원에 대한 투자를 강화하는 동시에 도입 비용 절감을 목표로 하는 국내 로봇 제조업체의 육성을 진행하고 있습니다. 일본에서의 고령화는 척추·심장 디바이스 수요를 촉진하고, 인도의 민간 병원 체인은 선택적 정형외과 수술 수요 획득을 위한 수술실 용량을 확대하고 있습니다. 이 기세에 의해 이 지역이 일반 외과용 기기 시장 전체에 차지하는 비율은 상승해, 다국적 기업과 현지 참가 기업 양쪽의 경쟁 격화가 가속하고 있습니다.

The general surgical devices market was valued at USD 19.81 billion in 2025 and estimated to grow from USD 21.32 billion in 2026 to reach USD 30.79 billion by 2031, at a CAGR of 7.62% during the forecast period (2026-2031).

Momentum comes from rising surgical volumes, accelerated adoption of minimally invasive techniques, and continuous product innovation aimed at shortening recovery times and lowering complication rates. North America leads the general surgical devices market thanks to advanced infrastructure and favorable reimbursement, while Asia-Pacific is advancing fastest as governments scale hospital capacity and private operators add ambulatory sites. Disposable supplies retain dominance because infection-control rules favor single-use tools, yet rapid gains in robotic platforms illustrate the industry's pivot toward precision. Competitive intensity is increasing as large conglomerates defend their share against focused entrants bringing niche technologies to market.

Robotic navigation systems, specialized access ports, and refined imaging together help surgeons reduce tissue trauma, which in turn lowers length of stay by 2-3 days and halves the time patients need before returning to work. Orthopedics illustrates the shift as 68% of eligible procedures in 2024 already used MIS, and Stryker's Mako SmartRobotics platform cut intra-operative force by 43%. Cardiovascular, gynecology, and neurosurgery specialties show comparable trajectories as device makers add single-port or catheter-based solutions that fit existing workflows. The economic upside strengthens the case: lowering readmissions and freeing beds help hospitals meet value-based payment targets, which further stimulates procurement of MIS-compatible systems. Collectively, these factors will keep the general surgical devices market on a robust expansion path as health systems continue replacing open approaches with keyhole alternatives.

Artificial intelligence now supports pre-operative planning, intra-operative guidance, and post-operative monitoring. FastGlioma, a University of Michigan-UCSF model, identified residual brain tumor tissue with 92% accuracy and reduced miss rates from 25% to 3.8%. Predictive engines such as MySurgeryRisk outperform conventional assessments, cutting complication incidence by up to 30%. Hospitals using these tools see fewer ICU days, and payers note cost avoidance; thus, AI is moving from pilot projects into routine procurement line-items. As algorithms migrate onto consoles and endoscopes, vendors differentiate through data pipelines rather than purely mechanical features yet another evolution that underpins sustained demand in the general surgical devices market.

Advanced robotics and imaging suites require investments that can exceed USD 2 million per operating room, a hurdle for facilities in middle-income countries where paybacks stretch beyond standard budgeting cycles. Service contracts, software upgrades, and disposables compound total cost of ownership, dampening uptake despite clear clinical benefits. Consequently, value-engineered systems and pay-per-use models are gaining traction as vendors attempt to keep the general surgical devices market accessible across income tiers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Disposable surgical supplies generated the largest revenue share in 2025 as infection-control protocols favored single-use drapes, trocars, and blades. Their 43.78% command of the general surgical devices market size underscores hospital preference for standardization when tracking nosocomial infection metrics. Segment growth nevertheless converges toward mid-single-digit rates because sustainability efforts encourage selective reusability in low-risk cases, a nuance reshaping procurement guidelines without dislodging disposables from top position.

Robotic-assisted instruments, though smaller in absolute dollars, are set to outpace every other category through 2031, riding an 10.62% CAGR. Systems tailored for hip revision, partial knee, and soft-tissue work broaden indications and shorten learning curves. As throughput improvements offset capital outlays, administrators increasingly view robotics as productivity tools rather than prestige purchases. This dynamic points to sustained momentum for the general surgical devices market.

The General Surgical Devices Market Report is Segmented by Product Type (Minimally Invasive Surgery Instruments, Robotic-Assisted Surgery Instruments, Energy-Based Surgery Instruments (RF, Ultrasonic), and More), Application (Orthopaedic, Cardiology, and More), End User (Hospitals, Ambulatory Surgical Centres, and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 37.45% of 2025 revenue, buoyed by high procedure counts, rapid uptake of robotics, and supportive reimbursement. The U.S. benefits from a dense innovation ecosystem, but market saturation in staples and electrosurgery means growth increasingly stems from software-enhanced systems and AI modules. Canada's push toward value-based care encourages hospitals to track device performance closely, a trend likely to ripple into procurement across the general surgical devices market.

Europe ranks second and maintains steady expansion despite rigorous conformity assessments under the Medical Device Regulation. Germany, the United Kingdom, and France lead adoption, particularly for joint arthroplasty robots and advanced imaging. Southern and Eastern European states are upgrading facilities, creating fresh avenues for mid-priced solutions. Currency fluctuations and budget constraints remain hurdles, but harmonized standards improve cross-border commercialization inside the general surgical devices market.

Asia-Pacific represents the fastest-growing region with a 10.15% CAGR. China invests heavily in county-level hospitals while fostering domestic robotic challengers that aim to lower acquisition costs. Japan's aging demographic catalyzes spine and cardiac device demand, and India's private chains expand operating theatre capacity to capture elective orthopedic work. This momentum elevates the region's contribution to overall general surgical devices market size and heightens competitive jockeying among multinationals and local entrants alike.