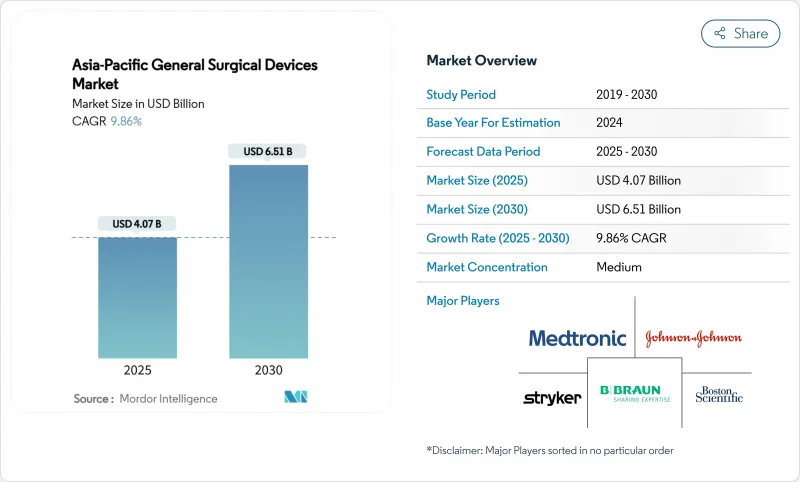

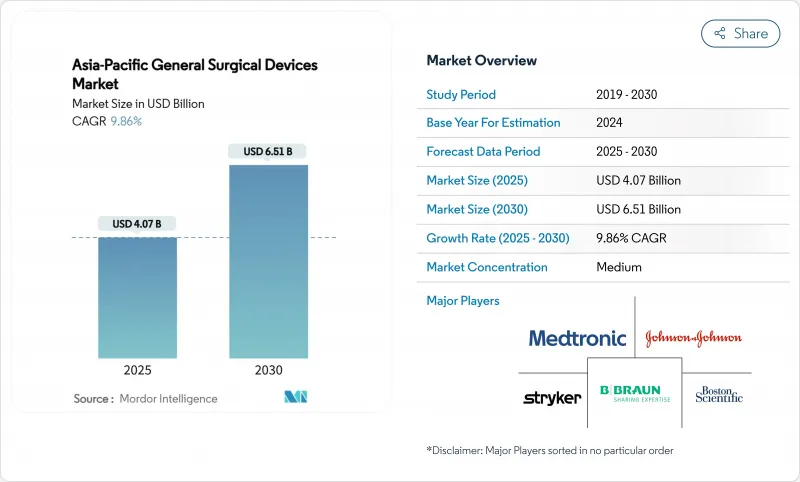

아시아태평양의 일반 외과용 기기 시장 규모는 2025년에 40억 7,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 9.86%로, 2030년에는 65억 1,000만 달러에 달할 것으로 예상됩니다.

수술의 지속적인 현대화, 인구 노령화, 낮은 침습 및 로봇 플랫폼의 급속한 채용은 성장의 주요 원동력입니다. 특히 ASEAN 의료기기지령과 같은 규제제도의 수렴은 다국적 기업이나 지역의 혁신자에게 시장 투입까지의 타임라인을 단축하고 있습니다. 중국은 2024년에 31.97%의 점유율을 획득해 지역별 매출을 이끌었지만, 인도는 2자리수의 의료 지출 증가와 강력한 현지화 정책을 배경으로 가장 빠른 궤도를 보였습니다. 낮은 침습 수술이 수술실의 주류를 차지하고 복강경과 에너지 기반 도구의 견조한 수요를 뒷받침하고 있지만, 고가의 로봇 시스템이 가장 높은 성장을 기록하고 있습니다. 외래환자의 외래 수술 센터(ASC)로의 전환으로 컴팩트하고 워크플로우를 중시한 기기에 대한 조달 전략이 재구성되어 세계 제조업체와 국내 기업과의 범지역적 파트너십으로 차세대 기술에 대한 접근이 확대되고 있습니다.

포스 피드백 장비와 인공지능 지원 지침이 절제 정밀도를 향상시키고 학습 곡선을 단축시키는 증거가 축적됨에 따라 이 지역의 병원은 로봇 시스템의 조달을 가속화하고 있습니다. 일본에서는 2025년에 5세대 다빈치에 의한 최초의 대장 수술이 기록되어, 복잡한 종양 증례에 데이터 풍부한 콘솔이 받아들여지고 있는 것이 밝혀졌습니다. 중국의 국가 의료 제품 관리국은 0.1mm의 정밀도를 제공하는 국산 로봇 플랫폼을 승인하고 국산 하이테크 솔루션에 대한 정책 지원을 제시했습니다. 국경을 넘어선 5G 실증실험으로 전문 외과의사가 1,000km 이상 떨어진 곳에서도 복강경 검사를 감독할 수 있음이 증명돼 전임 전문의가 없는 원격지에서도 서비스를 제공할 수 있는 현실적인 모델이 막을 열었습니다. 현재 내시경 타워에 내장된 AI 이미지 분석 모듈은 실시간 마진 평가를 제공하고 기존 복강경 워크플로우와 원활하게 통합하여 중견 병원 업그레이드 경로를 가속화합니다. 아시아태평양의 일반 외과용 기기 시장은 디지털 수술 기술 혁신의 온상이되었습니다.

주요 국가의 의료 예산은 매년 증가하고 있으며, 수술실의 증설이 진행되고 있습니다. 인도에서는 2024-2025년도의 중앙의료예산이 12.59% 증액되어 새롭게 5개의 AIIMS가 가동해 각각 고도의 에너지기기나 로봇카트에 대응한 다과목 수술실이 설치되었습니다. 중국의 연결조정지표는 공급과 고령화 관련 수요 사이의 무결성 개선을 보여주고 있지만 서부 지방에서는 자원 사막화가 계속되고 있으며 서비스 격차를 시정하는 기기 입찰을 신속하게 진행하는 정책에 박차를 가하고 있습니다. 메드트로닉과 같은 다국적 기업은 싱가포르와 한국에 로봇 공학 교육 스튜디오를 개설하고, 벤더와의 관계를 강화하고, 장래의 기기 표준화 결정을 자사의 플랫폼으로 유도하는 데모 허브를 구축함으로써 대응하고 있습니다. 사립 병원에 병설된 당일치기 수술 전용 센터의 건설도 마찬가지로 활발하고, 회전율이 높은 소모품에 특화한 공급자에게 증가분공급을 실시했습니다.

ASEAN의 수렴을 향한 움직임과는 달리, 기업은 여전히 각국 특유의 서식, 기기 분류, 수입 체크의 모자이크를 네비게이트하고, 이것이 상업적 발매를 장기화시키고 있습니다. 중국의 의료기기법 개정에서는 시판 후 조사가 강화되어 수익을 연장하는 반복 테스트가 추가되었습니다. 인도의 새로운 판매 약관은 가치 이전의 명시적인 공개를 의무화하고 있으며 임상의의 참여 전략을 복잡하게 만듭니다. 일본에서는 미국과 유럽에서 이미 승인된 승인 신청 이외에도 국내에서의 철저한 심사가 이루어지기 때문에 「디바이스 러그」가 계속되고 있습니다. 제3자 기관에 의한 적합성 평가는 여러 법역에서 인정되고 있지만, 그 채용에는 변동이 있어, 시간 단축의 가능성은 한정되어 있습니다. 그 결과 아시아태평양의 일반 외과용 기기 시장, 특히 전임 규제 담당자가 없는 중소기업의 기세를 깎고 있습니다.

로봇 지원 플랫폼은 CAGR 12.11%에서 가장 급성장하고 있는 제품 라인이지만, 복강경 기기는 2024년에 26.65%의 점유율을 획득했으며 여전히 절대 수익이 가장 높습니다. 병원은 부인과, 소화기과, 비뇨기과에 걸친 복강경 수술의 범용성을 높이 평가하며, 트로커 세트와 클립 어플라이어의 기준선 주문을 보장합니다. 핸드헬드 기구는 기본적인 조직 조작에 필수적이며 소규모 시설에서도 사용하기 쉬운 가격대를 유지하고 있습니다. 전기 수술용 발전기는 파형 변조를 개선하여 부수적인 열 손상을 줄이고 안전 의무화를 지원합니다.

상처 폐쇄 기술 혁신에는 만성 상처의 육아 형성을 촉진하는 전기 치료 드레싱 재료가 포함되어 있으며, 적응은 수술실뿐만 아니라 수술 후 병동까지 퍼져 있습니다. 감염 관리위원회가 무균성 보증과 폐기물 관리 비용을 비교 검토하는 동안, 단일 청소년 보조기구가 급성장하고 있습니다. 제조업체 각 회사는 현재 지속가능성에 대한 반대 의견을 극복하기 위해 재활용 인수 제도를 발표하고 있습니다. AI 대응 로봇 인클로저는 모듈식으로 업그레이드 가능한 투자 대상으로 판매되고 있으며, 자본 예산은 데이터 주도형 수술에 대한 미래 기대에 대응할 수 있는 시스템으로 향하는 경향이 강해지고 있으며, 아시아태평양의 일반 외과용 기기 시장에서 장기적인 가치 획득을 뒷받침하고 있습니다.

저침습 수술은 2024년 아시아태평양 일반 외과용 기기 시장의 62.43%를 차지했으며 CAGR 10.57%로 가장 높은 성장 예측을 유지하고 있습니다. 병원은 복강경하 담낭 적출술의 평균 재원일수를 개복술과 비교하여 최대 2일 단축했다고 보고하고, 고화질 카메라 헤드와 기복기 조달을 강화하고 있습니다. 로봇 플랫폼은 손목에 관절이 있는 기구로 MIS의 장점을 보강해, 이전에는 개복으로 밖에 할 수 없었던 봉합 정밀도를 실현하고 있습니다.

상처 살균을 위한 콜드 아토모스페릭 플라즈마와 같은 기술 혁신이 MIS의 수술 후 프로토콜에 가세해 코어 스코프와 나란히 판매되는 기기 바구니의 폭을 넓히고 있습니다. AI 가이드 하 대장 내시경 시스템은 폴립에 실시간으로 플래그를 지정하여 선종 검출률을 높이고 호환되는 프로세서 수익을 확대합니다. 개복 수술은 광범위한 종양 절제와 다발 외상에 대한 관련성을 유지하지만, 이러한 경우에는 배연 및 초음파 박리와 같은 보조 기술이 점점 더 많이 도입되고 있으며, 모든 유형의 수술에서 장비가 계속 소비되고 있습니다.

The Asia-Pacific General Surgical Devices Market size is estimated at USD 4.07 billion in 2025, and is expected to reach USD 6.51 billion by 2030, at a CAGR of 9.86% during the forecast period (2025-2030).

Sustained modernisation of surgical care, an ageing population, and rapid adoption of minimally invasive and robotic platforms are the primary engines of growth. Converging regulatory regimes, particularly the ASEAN Medical Device Directive, are shortening go-to-market timelines for multinational and regional innovators. China leads regional revenue with a 31.97% stake in 2024, while India shows the fastest trajectory on the back of double-digit healthcare spending increases and strong localisation policies. Minimally invasive procedures dominate operating theatres, underpinning resilient demand for laparoscopic and energy-based tools, even as premium-priced robotic systems register the highest growth. Outpatient migration to ambulatory surgical centres (ASCs) is reshaping procurement strategies toward compact, workflow-oriented equipment, and pan-regional partnerships between global manufacturers and domestic firms are widening access to next-generation technology.

Hospitals across the region are accelerating procurement of robotic systems as evidence mounts that force-feedback instrumentation and AI-assisted guidance improve resection accuracy and shorten learning curves. Japan recorded its first colorectal procedure with the fifth-generation da Vinci in 2025, underscoring acceptance of data-rich consoles for complex oncology cases. China's National Medical Products Administration cleared domestic robotic platforms offering 0.1 mm precision, signalling policy support for indigenous high-tech solutions. Cross-border 5G demonstrations have proven that expert surgeons can supervise laparoscopy at distances over 1,000 km, opening a viable model for serving remote areas without full-time specialists. AI image-analysis modules now embedded in endoscopic towers provide real-time margin assessment, integrating seamlessly with existing laparoscopic workflows and accelerating the upgrade path for mid-tier hospitals. These gains collectively reinforce the Asia Pacific General Surgery Devices market as a hotbed for digital surgical innovation.

Annual health-budget increases in major economies are translating into bricks-and-mortar expansion of operating suites. India raised central health outlays by 12.59% for FY 2024-25 and activated five new AIIMS institutes, each housing multi-specialty theatres ready for advanced energy devices and robotic carts. China's coupling-coordination metrics show improved alignment between supply and ageing-related demand, but resource deserts in western provinces persist, spurring policy to fast-track equipment tenders that close service gaps. Multinationals such as Medtronic have responded by opening robotics training studios in Singapore and Korea, creating demonstration hubs that anchor vendor relationships and swing future device standardisation decisions toward their platforms. Construction of dedicated day-surgery centres attached to private hospitals is equally brisk, feeding incremental volumes to suppliers focused on high-turnover consumables.

Despite ASEAN moves toward convergence, firms still navigate a mosaic of country-specific forms, device classifications, and import checks that prolong commercial launches. China's updated medical-device law tightened post-market surveillance, adding iterative testing that can postpone revenue. India's new marketing code requires explicit disclosure of value transfers, complicating clinician-engagement strategies. Japan continues to experience "device lag" as thorough domestic reviews extend beyond submissions already cleared in the United States or Europe. While third-party conformity assessments are authorised in several jurisdictions, uneven adoption limits their time-saving potential. The net effect clips momentum in the Asia Pacific General Surgery Devices market, especially for SMEs lacking dedicated regulatory staff.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Robotic-assisted platforms represent the fastest-rising product line at a 12.11% CAGR, yet laparoscopic devices still supply the highest absolute revenue with 26.65% share in 2024. Hospitals appreciate laparoscopy's versatility across gynaecology, GI, and urology, guaranteeing baseline orders for trocar sets and clip appliers. Hand-held instruments remain indispensable for basic tissue manipulation, keeping entry price points accessible in smaller centres. Electrosurgical generators are benefiting from refinements in waveform modulation that cut collateral thermal injury, aligning with safety mandates.

Wound-closure innovations include electroceutical dressings that accelerate chronic-wound granulation, widening indications beyond theatre into postoperative wards. Single-use ancillaries are growing rapidly as infection-control committees weigh sterility assurance against waste-management costs; manufacturers now publicise recycling take-back schemes to overcome sustainability objections. With AI-ready robotic chassis marketed as modular, upgradeable investments, capital budgets are increasingly earmarked for systems that future-proof against data-driven surgical expectations, bolstering long-run value capture in the Asia Pacific General Surgery Devices market.

Minimally invasive surgery accounted for 62.43% of the Asia Pacific General Surgery Devices market in 2024 and retains the highest growth forecast at 10.57% CAGR. Hospitals report reduced average length of stay by up to two days for laparoscopic cholecystectomy compared with open techniques, reinforcing procurement of high-definition camera heads and insufflators. Robotic platforms augment the MIS advantage with articulated wrist instruments that deliver suturing accuracy previously possible only via open access.

Innovations such as cold atmospheric plasma for wound sterilisation are entering MIS postoperative protocols, broadening device baskets sold alongside core scopes. AI-guided colonoscopy systems now flag polyps in real time, increasing adenoma-detection rates and expanding revenue for compatible processors. Open surgery retains relevance for extensive oncological resections and polytrauma, but these cases increasingly incorporate adjunct technologies such as smoke evacuation and ultrasonic dissection, ensuring all procedure types continue to consume devices.

The Asia Pacific General Surgery Devices Market Report is Segmented by Product (Hand-Held Devices, Laparoscopic Devices, Electrosurgical Devices, and More), Procedure Approach (Open Surgery, Minimally Invasive Surgery), Application (Gynecology & Urology, and More), End User (Hospitals, Ambulatory Surgical Centres, Specialty Clinics), and Geography (China, Japan, and More). The Market Forecasts are Provided in Terms of Value (USD).