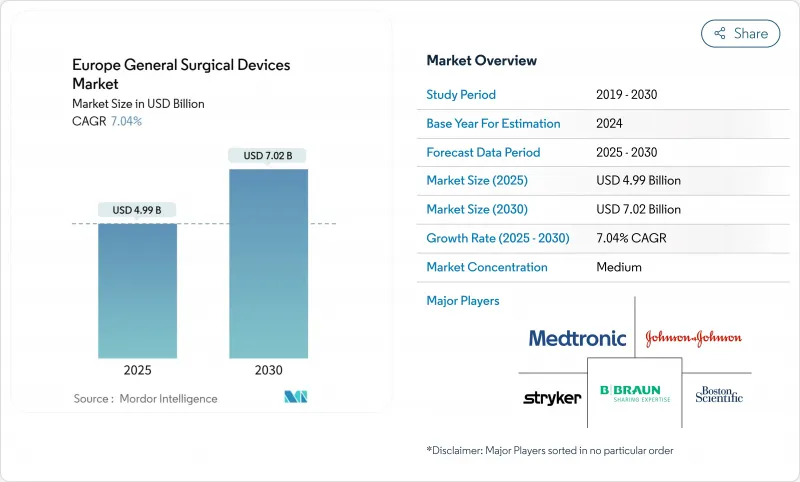

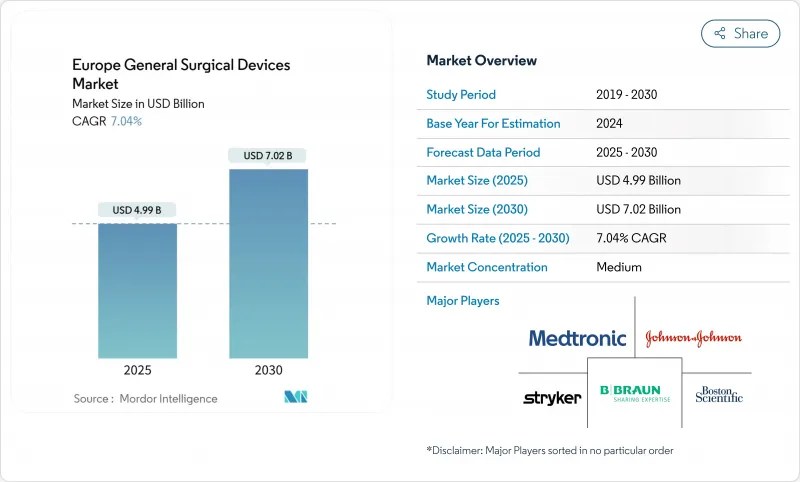

유럽의 일반 외과용 기기 시장 규모는 2025년에 49억 9,000만 달러에 달하고, 예측 기간(2025-2030년)의 CAGR은 7.04%를 나타내, 2030년에는 70억 2,000만 달러에 달할 것으로 전망됩니다.

낮은 침습 수술과 로봇 수술의 견조한 성장은 급속한 고령화와 임상 적응증의 확대와 함께이 확대를 지원합니다. EU-MDR의 컴플라이언스 비용이 동시에 전략적 통합을 촉진하고 자본력 있는 다국적 기업이 규제 오버헤드를 흡수하는 반면 중소기업은 철수하거나 제휴를 모색하게 됩니다. 병원 구매자는 가격 협상을 강화하고 있지만 의료 시스템이 용량 제약을 완화하기 위해 당일치기 모델로 이동하고 있기 때문에 수술 건수는 증가의 길을 따라가고 있습니다. 공급망의 회복력은 이사회 수준의 우선사항이 되고 있으며, 제조업체는 현재 연간 매출의 3-5%를 물류의 다양화에 충당하고 있습니다.

유럽의 건강 관리 제공업체는 회복 시간 단축과 입원 환자의 정원 감소를 목표로 개복 수술에서 낮은 침습 절차로의 전환을 계속하고 있습니다. NHS 잉글랜드는 2035년까지 연간 50만 건의 로봇 지원 수술을 계획하고 있으며, 설비 갱신 사이클을 가속화하는 가파른 채용 곡선을 보여줍니다. 북유럽 센터는 이러한 동향을 반영하여 120대 이상의 로봇 플랫폼을 도입하고 탈장 수리 및 기타 연부 조직 인터벤션을 지원합니다. 올림푸스 ESG-410과 같은 하이브리드, 바이폴라 및 초음파 모달리티를 결합한 에너지 기반 기기는 외과의사가 다기능 도구를 요구하기 때문에 광범위한 변화의 이점을 누리고 있습니다. 보스턴 사이언티픽의 워크플로우 자문 솔루션을 도입한 병원에서는 경 카테터 치료 건수가 40% 증가한 것으로 보고되어 디지털 통합이 처리량을 향상시키는 방법을 보여줍니다.

특히 독일, 이탈리아, 스페인에서는 65세 이상의 인구가 빠르게 증가하고 있으며, 이 인구 역학의 변화는 인공관절 치환술, 심혈관 인터벤션, 복잡한 종양 절제술 증가에 박차를 가하고 있습니다. 프랑스는 진료 보상 인하에도 불구하고 인공 고관절 치환술의 실시율로 OECD 회원국 중 8위에 랭크되어 잠재적인 수요를 뒷받침하고 있습니다. 외래수술센터(ASC)는 메디케어와 연동한 호조건의 지불과 미공개주에 대한 투자를 몰아치며 가장 성장률이 높은 전문분야로 심장병학을 꼽고 있습니다. 집중 치료 전문의 부족은 외과 및 중증 환자 서비스의 긴밀한 통합을 촉진하고 마취과 의사는 현재 유럽 전체 ICU 병상의 70%를 관리하고 있습니다.

적합성 보증은 기본적인 분석으로 5,000유로에서 클래스 III 시험에서 50만 유로의 비용이 들고, 중소기업의 현금 흐름을 압박하고, 포트폴리오의 합리화를 촉진하고 있습니다. 예상 50만 대의 기기를 검토할 수 있는 43개의 노티파이드 바디가 남아 있기 때문에 승인 사이클이 연장되고 상시가 연기되었습니다. 업계 조사에 따르면 기기 제조업체의 절반이 규제 부담으로 인해 EU에서 포트폴리오 철수 및 제한을 계획하고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

핸드헬드 기구는 루틴 수술에 있어서의 편재성을 반영해, 2024년의 유럽의 일반 외과용 기기 시장 점유율로 34.57%를 유지했습니다. 그러나 로봇 및 컴퓨터 지원 시스템은 보다 광범위한 임상적 수용과 절차 당 비용 저하로 2030년까지 연평균 복합 성장률(CAGR) 9.11%를 나타내 모든 카테고리를 능가합니다. 올림푸스의 THUNDERBEAT와 VISERA 4K 플랫폼은 이미징과 에너지 기술의 융합을 통한 조직 취급과 시각화의 강화를 보여줍니다. 메드트로닉의 PlasmaBlade는 기존의 전기 암보다 상당히 낮은 온도에서 작동하여 부수적인 손상을 줄입니다. 센서와 무선 연결을 통합한 하이브리드 기기는 프리미엄 가격대와 가치 가격대 사이의 경쟁 격차를 넓히는 태세를 갖추고 있습니다.

2세대 로봇 공학은 이전 비용과 설치 면적 제한을 해결하고 중형 센터에서의 채용을 확대합니다. 유럽의 일반 외과용 기기 시장 공급업체는 디지털 워크플로우 소프트웨어에 자본 기기를 번들어 보다 강력한 고객 관계를 구축하는 경향이 커지고 있습니다. CE 마크를 취득한 Virtual-Port사의 복강경용 액세서리나, 존슨 엔드 존슨사의 Ottava 대응 제너레이터는 새로운 로봇의 에코시스템에 적합하는 적정한 제품 업데이트의 일례입니다. 상처 폐쇄 시스템과 트로커 라인은 멸균 병목 현상과 감염 위험을 줄이는 단일 사용 옵션으로 데이 케이스 푸시의 이점을 누리고 있습니다.

낮은 침습 절차는 2024년 유럽의 일반 외과용 기기 시장 규모의 71.24%를 차지했고 CAGR 8.22%를 나타내 전진하고 있으며 선호되는 표준 치료로서의 입지를 강화하고 있습니다. 향상된 광학 시스템, 에너지 공급 및 촉각 피드백을 통해 외과의사는 더 작은 절개로 복잡한 병태를 해결할 수 있습니다. 개복 수술은 외상과 큰 종양 절제에 중요한 역할을 담당하지만 수술 건수는 꾸준히 감소하고 있습니다.

Hugo 플랫폼에서 보고된 고속 도킹 시간은 마취 시간을 단축하고 회전 속도를 향상시키는 누적 효율 향상을 보여줍니다. HoloSurge의 3D 홀로그래피는 시험 단계에 들어가 간담 췌장 사례에서보다 안전한 절제면을 지원합니다. 유럽의 일반 외과용 기기 시장 진출 기업은 외과 의사가 새로운 학습 곡선을 신속하게 오를 수 있도록 교육 센터에 많은 투자를 하고 있습니다.

The Europe General Surgical Devices Market size is estimated at USD 4.99 billion in 2025, and is expected to reach USD 7.02 billion by 2030, at a CAGR of 7.04% during the forecast period (2025-2030).

Robust procedure growth in minimally invasive and robotic platforms, coupled with a rapidly aging population and widening clinical indications, underpins this expansion. EU-MDR compliance costs have simultaneously driven strategic consolidation, positioning well-capitalized multinationals to absorb regulatory overheads while smaller firms either exit or seek partnerships. Hospital purchasers intensify price negotiations, yet procedure volumes keep climbing as health systems shift toward day-case models to relieve capacity constraints. Supply-chain resilience has become a board-level priority, with manufacturers now directing 3-5% of annual revenue to logistics diversification.

Healthcare providers across Europe continue to transition from open to minimally invasive techniques, aiming to cut recovery times and free inpatient capacity. NHS England projects 500,000 robotic-assisted operations annually by 2035, signaling a steep adoption curve that will accelerate capital equipment refresh cycles. Nordic centers mirror this trend, installing more than 120 robotic platforms to support hernia repairs and other soft-tissue interventions. Energy-based devices such as Olympus ESG-410, which combine hybrid, bipolar, and ultrasonic modalities, are benefiting from the broader shift as surgeons seek multifunctional tools. Hospitals deploying Boston Scientific workflow-advisory solutions report 40% higher transcatheter volumes, illustrating how digital integration multiplies throughput.

Citizens aged >= 65 represent a fast-growing cohort, particularly in Germany, Italy, and Spain, and this demographic shift fuels an uptick in joint replacements, cardiovascular interventions, and complex oncology resections. France still ranks 8th among OECD nations for hip replacement rates despite reimbursement cuts, underscoring latent demand. Ambulatory surgery centers (ASCs) have flagged cardiology as their highest-growth specialty, aided by favorable Medicare-aligned payments and private equity investment. Intensivist shortages prompt a tighter integration of surgery and critical-care services, with anesthesiologists now managing 70% of ICU beds across Europe.

Conformity assurance can cost from EUR 5,000 for basic analyses to EUR 500,000 for Class III trials, squeezing SME cash flows and prompting portfolio rationalization. Only 43 notified bodies remain to review an estimated 500,000 devices, leading to extended approval cycles and deferred launches. Industry surveys show half of device makers plan to withdraw or limit EU portfolios due to regulatory burdens.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hand-held instruments retained a 34.57% Europe general surgical devices market share in 2024, reflecting their ubiquity in routine interventions. Robotic and computer-assisted systems, however, are set to outpace all categories at a 9.11% CAGR to 2030, powered by broader clinical acceptance and falling per-procedure costs. Olympus THUNDERBEAT and VISERA 4K platforms illustrate how imaging and energy technologies converge to enhance tissue handling and visualization. Medtronic's PlasmaBlade operates at significantly lower temperatures than legacy electrocautery, reducing collateral damage. Hybrid devices that integrate sensors and wireless connectivity are poised to stretch the competitive gap between premium and value tiers.

Second-generation robotics address prior cost and footprint limitations, opening adoption among mid-sized centers. Europe general surgical devices market vendors increasingly bundle capital equipment with digital workflow software to create stickier customer relationships. Virtual-Ports' CE-marked laparoscopic accessories and Johnson & Johnson's Ottava-compatible generator exemplify targeted product updates that fit new robotic ecosystems. Wound-closure systems and trocar lines benefit from the day-case push, with single-use options mitigating sterilization bottlenecks and infection risk.

Minimally invasive techniques accounted for 71.24% of the Europe general surgical devices market size in 2024 and are advancing at an 8.22% CAGR, consolidating their position as the preferred standard of care. Improved optics, energy delivery, and haptic feedback allow surgeons to tackle complex pathologies with smaller incisions. Open surgery maintains a vital role for trauma and large tumor resections but is ceding volume steadily.

Fast docking times reported for the Hugo platform illustrate cumulative efficiency gains that reduce anesthesia duration and improve turnover. HoloSurge's 3D holography enters pilot phases, supporting safer resection planes in hepatobiliary cases. Europe general surgical devices market participants invest heavily in training centers to help surgeons climb new learning curves quickly, a prerequisite for payer support and technology credentialing.

The Europe General Surgical Devices Market Report is Segmented by Product (Hand-Held Surgical Instruments, Laparoscopic Devices, Electrosurgical Devices, Wound Closure Devices, and More), Procedure Approach (Open Surgery, and Minimally Invasive Surgery), Application (Gynecology and Urology, Cardiology, Orthopedic, and More) and Country (Germany, United Kingdom, and More). The Market Forecasts are Provided in Terms of Value (USD).