가구용 플라스틱 시장 : 플라스틱 유형별, 조성별, 가구 유형별, 용도별, 최종 이용 산업별, 지역별 - 예측(-2030년)

Furniture Plastic Market by Plastic Type (Virgin Grade, Compounded Grade), Composition (Unfilled, Mineral Filled, Glass Fiber Reinforced, Other Compositions), Furniture Type, Application, End-use Industry, and Region - Global Forecast to 2030

상품코드:1928857

리서치사:MarketsandMarkets

발행일:2026년 01월

페이지 정보:영문 299 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

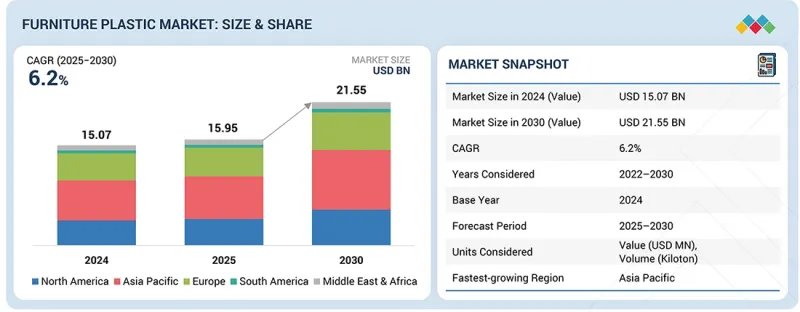

가구용 플라스틱 시장 규모는 2025년 159억 5,000만 달러에서 예측 기간 중에 CAGR6.2%로 성장하여 2030년까지 215억 5,000만 달러에 이를 것으로 예측됩니다.

조사 범위

조사 대상 기간

2022년-2030년

기준 연도

2024년

예측 기간

2025년-2030년

대상 단위

금액(100만 달러) 및 킬로톤

부문

플라스틱 유형별, 조성별, 가구 유형별, 용도별, 최종 이용 산업별, 지역별

대상 지역

북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미

가구용 플라스틱은 주거, 사무실, 호텔, 의료, 교육 시설 등 다양한 분야에 침투하고 있으며, 이러한 추세는 끊임없이 변화하는 안전, 내구성, 지속가능성에 대한 요구사항에 의해 뒷받침되고 있습니다. 제조업체들은 경량성, 무한한 디자인 가능성, 내수성, 긴 수명 등의 장점을 고객에게 제공하기 위해 폴리프로필렌(PP), 폴리에틸렌(PE), ABS, 엔지니어링 플라스틱 컴파운드 등의 소재로 전환하고 있습니다. 이 소재들은 의자, 테이블, 수납 유닛, 모듈형 가구 시스템, 실내 및 실외용 가구 등 가구 부품의 가능성을 넓혀주며, 특히 유지보수의 편의성과 대량생산성 분야에서 주목받고 있습니다.

ISO, ASTM, EN 등 국제적인 제품 안전 및 재료 표준을 준수하는 것도 가구 생산에서 일정 기준을 충족하는 플라스틱 재료의 사용을 더욱 촉진하는 요인입니다. 또한, 산업 및 지속가능성 관련 가이드라인은 플라스틱이 재료 사용량 감소, 경량화를 통한 운송 배출량 감소, 생산 효율성 향상에 중요한 역할을 한다는 것을 인식하고 있으며, 이는 전 세계 가구 제조 가치사슬에서 플라스틱의 중요성이 증가하는 주요 요인으로 작용하고 있습니다. 되고 있습니다.

버진 그레이드 플라스틱은 예측 기간 동안 플라스틱 유형별 시장 성장에 가장 큰 기여를 할 것으로 예상되는 가구용 플라스틱 시장 부문이 될 것으로 예측됩니다. 지속적인 재료 품질로의 전환, 기계적 성능 향상, 견고한 안전 및 내구성 기준 충족이 이러한 성장을 가속하는 주요 요인이 될 것으로 예측됩니다. 정밀한 성형, 균일한 표면 마감, 긴 수명이 요구되는 용도, 특히 주거용 및 시설용 가구에서 가구 제조업체들은 버진 폴리프로필렌, 폴리에틸렌, ABS의 사용을 늘리고 있습니다. 재활용 플라스틱과 비교하여, 버진그레이드 플라스틱은 높은 내충격성, 우수한 색상 안정성, 예측 가능한 가공 특성을 제공하여 대량 생산 사출 성형 및 복잡한 가구 형상의 주요 선택이 되고 있습니다. 또한, ISO, ASTM, EN 표준과 같은 국제적인 재료 및 제품 안전 기준을 준수하는 것도 전 세계 가구 생산에 버진로드 플라스틱의 사용을 촉진하는 요인으로 작용하고 있습니다.

주택 부문은 예측 기간 동안 가구용 플라스틱 시장을 주도하는 주요 최종 사용 산업이 될 것이며, 가장 높은 성장률을 보일 것으로 예측됩니다. 이 시장 부문의 급속한 발전에 기여하는 주요 요인은 도시화, 저렴한 주택의 확대, 경량 및 공간 절약형 가구에 대한 소비자의 선호도 증가입니다. 방수성, 쉬운 유지 보수, 모듈 식 및 조립식 형식과의 호환성으로 인해 플라스틱 가구는 가정에서 점점 더 많은 인기를 얻고 있습니다. 전자상거래를 통한 가구 판매 증가와 소비자 직접 배송 모델의 부상은 주택 수요의 성장에 큰 영향을 미치고 있으며, 운송 비용 절감 및 손상 발생률 감소와 같은 플라스틱 가구의 장점은 이를 더욱 촉진하고 있습니다. 또한, 주로 인테리어 디자인 트렌드 변화와 라이프스타일의 향상으로 인한 교체 주기의 가속화는 도시 및 준도시 주택 시장에서 지속적인 소비를 견인하는 요인으로 작용하고 있습니다.

아시아태평양은 예측 기간 동안 성장률에서 전 세계 다른 지역을 능가할 것으로 예측됩니다. 이러한 상황을 초래한 주요 요인으로는 대규모 도시 개발, 인구 증가, 중산층의 소비 확대 등이 있습니다. 중국, 인도, 인도네시아, 베트남 등의 지역에서는 주거, 상업, 공공시설 부문이 빠르게 성장하고 있으며, 비용 효율적인 가구에 대한 수요가 크게 증가하고 있습니다. 이 지역에는 원자재 가용성과 원가경쟁력 있는 생산체제를 바탕으로 한 플라스틱 제조기반이 잘 갖춰져 있습니다. 이 모든 것이 이 지역이 대량 가구 생산의 모멘텀을 유지할 수 있는 좋은 조건이 되고 있습니다. 정부의 주택 개발, 인프라 확장, 국내 제조 촉진 노력은 시장 성장을 가속화할 뿐만 아니라 아시아태평양을 미래 세계 가구용 플라스틱 시장에서 가장 중요한 거점 중 하나로 만들고 있습니다.

대상 기업 : Keter(이스라엘), Nilkamal(인도), The Supreme Industries Limited(인도), Tramontina(브라질), Cello(인도), Inter IKEA Systems B.V.(네덜란드), MillerKnoll, Inc. MillerKnoll, Inc.(미국), Grosfillex(프랑스), Poly-Wood, LLC(미국), NARDI S.p.A.(이탈리아), Harwal Group of Companies(아랍에미리트) 등이 본 보고서에서 다루고 있습니다.

가구용 플라스틱 시장의 주요 기업들에 대해 기업 프로파일, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석을 실시하였습니다.

조사 범위

본 보고서는 플라스틱 유형(버진 그레이드, 컴파운드 그레이드), 구성(무충진, 미네랄 충전, 유리섬유 강화, 기타 구성), 가구 유형(정원용 가구, 가정용 가구, 상업용 가구, 주거용 가구), 용도(실내, 실외), 최종 이용 산업(주거용, 상업용, 공공시설)에 따라 가구용 플라스틱 시장을 분류하고 있습니다. 가구용 플라스틱 시장을 분류하고 있습니다. 이 보고서의 조사 범위에는 가구용 플라스틱 시장의 성장에 영향을 미치는 촉진요인, 제약 요인, 과제 및 성장 기회에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 진입업체에 대한 상세한 분석을 실시하여 사업 개요, 제공 제품, 인수합병, 제품 출시, 사업 확장 등 가구용 플라스틱 시장과 관련된 주요 전략에 대한 인사이트를 제공합니다. 본 보고서에서는 가구용 플라스틱 시장 생태계 내 신흥 스타트업 기업의 경쟁 분석도 다루고 있습니다.

본 보고서 구매 이유

이 보고서는 시장 리더와 신규 시장 진출기업에게 가구용 플라스틱 시장 전체 및 하위 부문의 수익 수치에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁 구도를 이해하고, 자사의 포지셔닝에 대한 인사이트를 높이고, 적절한 시장 진출 전략을 수립할 수 있습니다. 본 보고서는 시장 동향을 파악하고 주요 시장 성장 촉진요인, 억제요인, 과제, 기회에 대한 정보를 이해관계자에게 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다.

주요 촉진요인(급속한 도시화와 저렴한 주택 증가, 모듈형 및 조립식(RTA) 가구에 대한 수요 증가, 목재 및 금속에 비해 비용, 무게, 물류 측면에서 우위), 제약 요인(환경 문제 및 플라스틱 폐기물에 대한 인식, 엄격한 플라스틱 및 재활용 규제), 기회(재활용 플라스틱 및 바이오플라스틱의 채택, 전자상거래 및 플랫팩 가구의 성장, 상업 및 공공시설의 확대), 과제(혼합 플라스틱 재활용, 전자상거래 및 플랫팩 가구의 성장, 재활용 플라스틱 및 바이오플라스틱의 채택) 플라스틱 및 재활용성에 대한 엄격한 규제), 기회(재활용 플라스틱 및 바이오플라스틱 채택, 전자상거래 및 플랫팩 가구의 성장, 상업 및 공공시설 인프라 확대), 과제(혼합 플라스틱 재활용 및 폐기물 관리, 내구성, 미학, 지속가능성의 균형)에 대한 분석이 이루어졌습니다. 분석합니다.

제품 개발/혁신 : 가구용 플라스틱 시장의 신기술 동향, 연구개발 활동, 제품 및 서비스 출시에 대한 상세한 분석.

시장 개발: 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 가구용 플라스틱 시장을 분석합니다.

시장 다각화 : 가구용 플라스틱 시장의 신제품 및 서비스, 미개척 지역, 최근 동향, 투자에 대한 종합적인 정보를 제공합니다.

경쟁사 평가: 주요 기업 - Keter Group(이스라엘), Nilkamal(인도), The Supreme Industries Limited(인도), Tramontina(브라질), Cello(인도), Inter IKEA Systems B.V.(네덜란드), MillerKnoll, Inc. MillerKnoll, Inc.(미국), Grosfillex(프랑스), Poly-Wood, LLC(미국), NARDI S.p.A.(이탈리아), Harwal Group of Companies(아랍에미리트) 등 주요 기업들 시장 점유율, 성장 전략, 서비스 제공 내용에 대해 상세하게 분석합니다.

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

제5장 업계 동향

Porter의 Five Forces 분석

거시경제 전망

밸류체인 분석

생태계 분석

가격 분석

무역 분석

2025년-2026년 주요 컨퍼런스 및 이벤트

고객의 비즈니스에 영향을 미치는 동향/혼란

투자 및 자금조달 시나리오

사례 연구 분석

2025년 미국 관세가 가구용 플라스틱 시장에 미치는 영향

제6장 기술, 특허, 디지털, AI 도입에 의한 전략적 파괴

주요 신기술

보완적 기술

인접 기술

기술/제품 로드맵

특허 분석

향후 응용

AI/생성형 AI가 가구용 플라스틱 시장에 미치는 영향

성공 사례와 실세계에의 응용

제7장 지속가능성과 규제 상황

지역 규제와 컴플라이언스

지속가능성 이니셔티브

지속가능성에 대한 영향과 규제 정책 대처

인증, 라벨, 환경기준

제8장 고객 상황과 구매 행동

의사결정 프로세스

구입자 이해관계자와 구입 평가 기준

채택 장벽과 내부 과제

다양한 최종 이용 산업으로부터 미충족 요구

시장 수익성

제9장 가구용 플라스틱 시장(플라스틱 유형별)

버진 등급

복합 등급

제10장 가구용 플라스틱 시장(구성별)

미충전

미네랄 충전

유리섬유 강화

기타 작품

제11장 가구용 플라스틱 시장(가구 유형별)

가든 퍼니쳐

가정용 가구

시설용 가구

주택 가구

제12장 가구용 플라스틱 시장(용도별)

실내

야외

제13장 가구용 플라스틱 시장(최종 이용 산업별)

주택

상업

기관

제14장 가구용 플라스틱 시장(지역별)

북미

미국

캐나다

멕시코

유럽

독일

프랑스

영국

이탈리아

스페인

폴란드

기타

남미

브라질

아르헨티나

기타

아시아태평양

중국

일본

인도

한국

기타

중동 및 아프리카

GCC 국가

기타

제15장 경쟁 구도

주요 시장 진출기업의 전략/강점

매출 분석, 2020년-2024년

시장 점유율 분석, 2024년

제품 비교

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

기업 평가와 재무 지표

경쟁 시나리오

제16장 기업 개요

주요 시장 진출기업

KETER GROUP

NILKAMAL

THE SUPREME INDUSTRIES LIMITED

TRAMONTINA

CELLO

INTER IKEA SYSTEMS B.V.

MILLERKNOLL, INC.

GROSFILLEX

POLY-WOOD, LLC

NARDI S.P.A.

HARWAL GROUP OF COMPANIES

기타 기업

PRIMA PLASTICS

VONDOM

SOTUFAB PLAST.

OTOBI

MODERN INDUSTRIES

GRACIOUS LIVING

METE PLASTIK

KAYALAR MUTFAK

C.R. PLASTIC PRODUCTS

KARTELL S.P.A.

KING OF PLASTIC

RESOL

GRUPO DUNA SA DE CV

MARMAX RECYCLED PLASTIC PRODUCTS

제17장 조사 방법

제18장 부록

LSH

영문 목차

영문목차

The furniture plastic market is projected to reach USD 21.55 billion by 2030 from USD 15.95 billion in 2025, at a CAGR of 6.2% during the forecast period.

Scope of the Report

Years Considered for the Study

2022-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million) and Volume (Kiloton)

Segments

Plastic Type, Composition, Furniture Type, Application, End-Use Industry, and Region.

Regions covered

North America, Asia Pacific, Europe, Middle East & Africa, and South America

Furniture plastics have penetrated various sectors like residential housing, offices, hospitality, healthcare, and educational facilities, the trend being supported by ever-changing safety, durability, and sustainability requirements. Manufacturers are moving to materials such as polypropylene (PP), polyethylene (PE), ABS, and engineered plastic compounds to give the customers the benefits of a light product, unlimited design possibilities, water resistance, and a longer service life. These materials open up the possibilities in furniture components such as chairs, tables, storage units, modular furniture systems, and indoor and outdoor furnishings, with the areas of maintenance simplicity and high-volume manufacturability being the most addressed.

The observance of international product safety and material standards such as ISO, ASTM, and EN regulations also acts as a further incentive for the use of plastic materials of a certain standard in furniture production. Besides that, industry and sustainability guidelines recognize the importance of plastics in enabling the reduction of material usage, cutting of transportation emissions through lightweighting, and bettering production efficiency, thus being a major factor behind their rise in significance across global furniture manufacturing value chains.

"Virgin grade are projected to be the fastest-growing plastic type in the furniture plastic market during the forecast period."

Virgin-grade plastics are anticipated to become the furniture plastics market segment, contributing most to the market growth of plastic types during the forecast period. It is to be expected that the shift towards a continuous material quality, a better mechanical performance and a firm safety and durability standard compliance will be the key drivers for this growth. For the applications that require precise molding, uniform surface finish, and long service life, especially in residential and institutional furniture, furniture manufacturers are now using more and more virgin polypropylene, polyethylene, and ABS. As compared with recycled ones, virgin-grade plastics offer larger impact resistance, better color stability, and more predictable processing behavior, thus, they are the primary choice in high-volume injection molding and complex furniture geometries. Besides, the adherence to global material and product safety standards such as ISO, ASTM, and EN norms is another factor that paves the way for the use of virgin-grade plastics in furniture production worldwide.

"Residential is projected to be the fastest-growing end-use industry in the furniture plastic market during the forecast period."

The residential segment is expected to be the leading end-use industry in the furniture plastics market, with the fastest growth rate over the forecast period. The main factors that contribute to the rapid development of this market segment are urbanization, affordable housing expansion, and increasing consumer preference for lightweight and space-efficient furniture. Plastic furniture is becoming more and more popular among households thanks to its waterproof feature, simple maintenance, and compatibility with modular and ready-to-assemble formats. The rise of e-commerce furniture sales and the direct-to-consumer delivery model have a major impact on residential demand growth, which is further augmented by the advantages of plastic furniture in cutting transportation costs and lessening the occurrence of damage. Besides, the accelerated replacement cycles that are mostly due to the changing interior design trends and lifestyle upgrades act as a continuous consumption driver in the urban and semi-urban residential markets.

"Asia Pacific is projected to be the fastest-growing region in the furniture plastic market during the forecast period."

Asia Pacific is set to outpace the rest of the world in the furniture plastics market in terms of growth over the forecast period. The key factors that have led to this situation include large-scale urban development, population growth, and the expanding middle-class consumption. The demand for cost-efficient furniture is very strong in areas like China, India, Indonesia, and Vietnam, where the residential, commercial, and institutional sectors are booming. The region has a full-fledged plastics manufacturing base, which is supported by the availability of the raw materials and cost-competitive production. All these are good conditions for the region to keep up the momentum of high-volume furniture manufacturing. The governments' efforts to promote housing development, infrastructure expansion, and domestic manufacturing not only speed up the market growth but also make Asia Pacific one of the most important future global furniture plastics market hubs.

By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 30%

By Designation: Directors: 30%, Managers: 20%, and Others: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and the Middle East & Africa 20%

Notes: Others include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 Million-1 Billion; and Tier 3: <USD 500 Million

Companies Covered: Keter (Israel), Nilkamal (India), The Supreme Industries Limited (India), Tramontina (Brazil), Cello (India), Inter IKEA Systems B.V. (Netherlands), MillerKnoll, Inc. (US), Grosfillex (France), Poly-Wood, LLC (US), NARDI S.p.A. (Italy) and Harwal Group of Companies (UAE) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the furniture plastic market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the furniture plastic market based on plastic type (virgin grade, compounded grade), composition (unfilled, mineral filled, glass fiber reinforced, other compositions) , furniture type (garden furniture, household, institutional furniture, residential furniture), application (indoor, outdoor), and end-use industry (residential, commercial, institutional). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the furniture plastic market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as mergers, acquisitions, product launches, and expansions, associated with the furniture plastic market. This report covers a competitive analysis of upcoming startups in the furniture plastic market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall furniture plastic market and the subsegments. It will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points.

Analysis of key drivers (Rapid urbanization and growth in affordable housing, Rising demand for modular and ready-to-assemble (RTA) furniture, Cost, weight, and logistics advantages over wood and metal), restraints (Environmental concerns and plastic waste perception, and Stringent regulations on plastics and recyclability), opportunities (Adoption of recycled and bio-based plastics, Growth of e-commerce and flat-pack furniture, and Expansion of commercial and institutional infrastructure), and challenges (Recycling and end-of-life management of mixed plastics and Balancing durability, aesthetics, and sustainability).

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the furniture plastic market.

Market Development: Comprehensive information about profitable markets - the report analyzes the furniture plastic market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the furniture plastic market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Keter Group (Israel), Nilkamal (India), The Supreme Industries Limited (India), Tramontina (Brazil), Cello (India), Inter IKEA Systems B.V. (Netherlands), MillerKnoll, Inc. (US), Grosfillex (France), Poly-Wood, LLC (US), NARDI S.p.A. (Italy) and Harwal Group of Companies (UAE).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 UNITS CONSIDERED

1.3.4.1 Currency/Value unit

1.3.4.2 Volume unit

1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS SHAPING MARKET

2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR FURNITURE PLASTIC MARKET PLAYERS

3.2 ASIA PACIFIC: FURNITURE PLASTIC MARKET, BY PLASTIC TYPE AND COUNTRY

3.3 FURNITURE PLASTIC MARKET, BY COMPOSITION

3.4 FURNITURE PLASTIC MARKET, BY END-USE INDUSTRY

3.5 FURNITURE PLASTIC MARKET, BY APPLICATION

3.6 FURNITURE PLASTIC MARKET, BY FURNITURE TYPE

3.7 FURNITURE PLASTIC MARKET, BY COUNTRY

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Rapid urbanization and growth in affordable housing

4.2.1.2 Rising demand for modular and ready-to-assemble furniture

4.2.1.3 Cost, weight, and logistics advantages over wood and metal

4.2.2 RESTRAINTS

4.2.2.1 Environmental concerns and plastic waste perception

4.2.2.2 Stringent regulations on plastics and recyclability

4.2.3 OPPORTUNITIES

4.2.3.1 Adoption of recycled and bio-based plastics

4.2.3.2 Growth of e-commerce and flat-pack furniture

4.2.3.3 Expansion of commercial and institutional infrastructure

4.2.4 CHALLENGES

4.2.4.1 Recycling and end-of-life management of mixed plastics

4.2.4.2 Balancing durability, aesthetics, and sustainability

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 THREAT OF NEW ENTRANTS

5.1.2 THREAT OF SUBSTITUTES

5.1.3 BARGAINING POWER OF SUPPLIERS

5.1.4 BARGAINING POWER OF BUYERS

5.1.5 INTENSITY OF COMPETITIVE RIVALRY

5.2 MACROECONOMIC OUTLOOK

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS AND FORECASTS

5.3 VALUE CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.4.1 ROLE IN ECOSYSTEM

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE OF FURNITURE PLASTICS, BY END-USE INDUSTRY, 2024

5.5.2 AVERAGE SELLING PRICE TREND OF FURNITURE PLASTICS, BY REGION, 2022-2024

5.6 TRADE ANALYSIS

5.6.1 EXPORT DATA FOR HS CODE 940370, 2020-2024

5.6.2 IMPORT DATA FOR HS CODE 940370, 2020-2024

5.7 KEY CONFERENCES AND EVENTS, 2025-2026

5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

5.9 INVESTMENT & FUNDING SCENARIO

5.10 CASE STUDY ANALYSIS

5.10.1 EMECO & THE COCA-COLA COMPANY (111 NAVY CHAIR - RECYCLED PET FURNITURE)

5.10.2 BASF & EMECO (PETRA THERMOPLASTIC POLYESTER FOR SUSTAINABLE CHAIRS)

5.10.3 GLOBAL FURNITURE TRENDS (VITRA, KARTELL, HERMAN MILLER - RECYCLED PP/PE FURNITURE)

5.11 IMPACT OF 2025 US TARIFF ON FURNITURE PLASTIC MARKET

5.11.1 KEY TARIFF RATES

5.11.2 PRICE IMPACT ANALYSIS

5.11.3 IMPACT ON COUNTRY/REGION

5.11.3.1 US

5.11.3.2 China

5.11.3.3 Europe

5.11.3.4 Mexico

5.11.4 IMPACT ON END-USE INDUSTRY

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

6.1 KEY EMERGING TECHNOLOGIES

6.1.1 BIO-BASED AND RECYCLED POLYMER TECHNOLOGIES

6.1.2 ADVANCED INJECTION MOLDING AND LIGHTWEIGHT STRUCTURAL TECHNOLOGIES

6.1.3 UV-STABILIZATION, WEATHER-RESISTANCE, AND FUNCTIONAL ADDITIVE SYSTEMS

6.2 COMPLEMENTARY TECHNOLOGIES

6.2.1 ADVANCED COMPOUNDING AND MASTERBATCH TECHNOLOGIES

6.2.2 SURFACE FINISHING, TEXTURE, AND DECORATIVE TECHNOLOGIES

6.2.3 AUTOMATION, ROBOTICS, AND DIGITAL MANUFACTURING SYSTEMS

6.3 ADJACENT TECHNOLOGIES

6.3.1 CIRCULAR ECONOMY AND ADVANCED RECYCLING TECHNOLOGIES

6.3.2 ADDITIVE MANUFACTURING AND TOOLING TECHNOLOGIES

6.3.3 SMART MATERIALS AND EMBEDDED FUNCTIONALITY

6.4 TECHNOLOGY/PRODUCT ROADMAP

6.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION