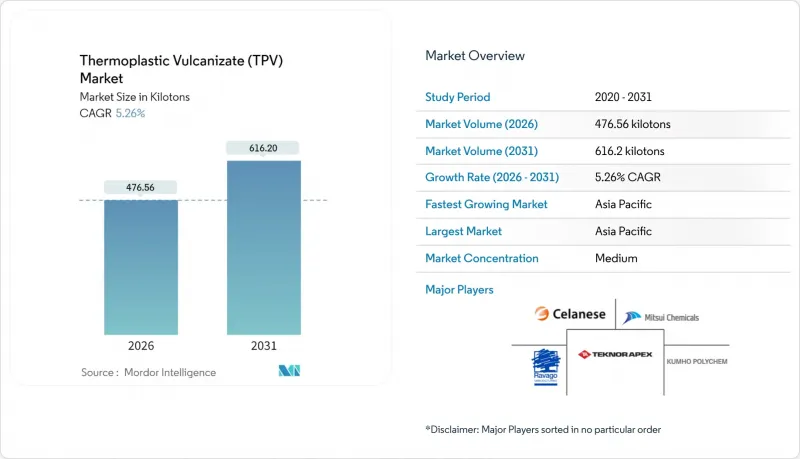

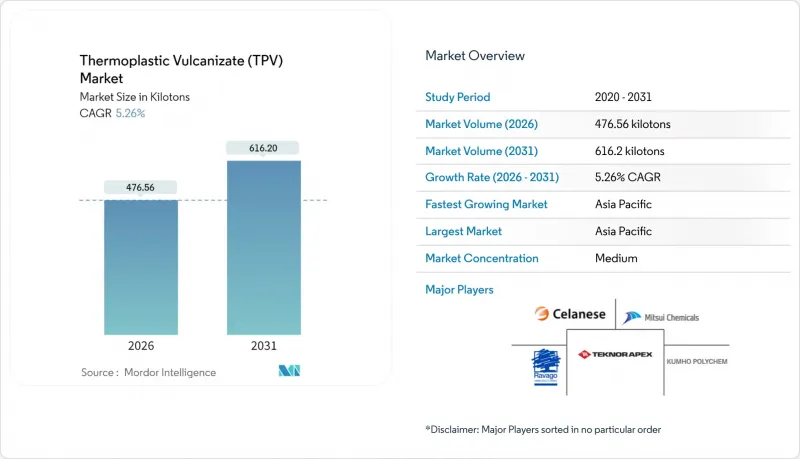

2026년 동적 가교형 열가소성 엘라스토머(TPV) 시장 규모는 476.56 킬로톤으로 추정되며, 2025년 452.75 킬로톤에서 2031년에는 616.2 킬로톤에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR)은 5.26%를 나타낼 것으로 예측됩니다.

이러한 꾸준한 확대는 자동차, 의료기기, 소비재 제조업체들이 전체 시스템 비용을 낮추면서 열경화성 수지에 필적하는 성능을 제공하는 재생 가능한 엘라스토머로 결정적으로 전환하고 있다는 것을 반영합니다. 전기자동차의 경량화 요구, 순환 경제에 대한 규제 압력, 전자제품의 소프트 터치 마감재에 대한 수요 증가로 인해 지역과 상관없이 채택이 가속화되고 있습니다. 비용 분석에 따르면, TPV는 주로 사이클 시간 단축과 후경화 공정의 생략으로 EPDM 고무에 비해 부품 제조 비용을 60% 이상 절감할 수 있습니다. 현재 공급업체들은 바이오 및 재생 소재 함유 등급을 추진하고 있으며, 제조 공정에서 탄소 발자국을 최대 50%까지 줄일 수 있습니다. 이를 통해 OEM 제조업체가 과학적 근거에 기반한 배출량 목표를 달성할 수 있는 확실한 경로를 제공합니다. 이러한 특성으로 인해 동적 가교형 열가소성 엘라스토머(TPV) 시장은 최적의 소재 솔루션으로 자리매김하고 있습니다. 한편, 프로파일렌 및 EPDM 원료의 가격 변동은 기존 열경화성 수지의 매력에 제한을 가져왔습니다.

자동차 제조업체들은 차량 중량 감소와 탄소 배출량 목표 달성을 위해 소재 대체에 박차를 가하고 있습니다. TPV 부품은 동급 EPDM 씰에 비해 약 30% 가벼우면서도 압축 영구 변형에 대한 내성을 유지하여 배터리 전기자동차의 항속거리를 더욱 늘릴 수 있습니다. 최근 동적 가황 기술의 발전으로 장기 피로 성능의 차이가 해소되어 금형을 변경하지 않고도 도어, 유리 러너, 선루프 시스템에서 TPV가 열경화성 수지를 대체할 수 있게 되었습니다. 유럽 연합의 2025년 CO2 배출량 상한 규제에 따른 압력은 이러한 변화를 가속화하여 열가소성 가황 고무 시장에 지속적인 수요 유입을 보장하고 있습니다.

휴대용 전자기기 브랜드는 재활용 공정을 복잡하게 만드는 도장이나 오버몰드 공정을 피하면서 고급스러운 촉감을 구현하기 위해 TPV를 채택하고 있습니다. 수지의 직접 성형 가능한 표면은 2차 코팅이 필요 없어 그립, 범퍼, 웨어러블 기기 케이스의 부품 총비용을 절감할 수 있습니다. 25-40%의 재활용 재료 함량을 통합하면 제품 내재 배출량을 더욱 줄일 수 있으며, 아시아에 위치한 위탁 성형 업체는 표준 사출 성형기를 사용할 수 있어 자본 장벽을 낮출 수 있습니다. 사이클 타임 단축과 RoHS·REACH 규제에 대한 적합성이 더욱 보급을 촉진하고 있습니다.

고산성, 유전 또는 연마성 환경에서는 TPV가 150 ℃ 이상에서 점차적으로 특성을 잃을 수 있기 때문에 특수 열경화성 수지가 여전히 선호됩니다. 폴리아크릴레이트 변성 TPV는 서비스 수명을 연장하지만, 부식성 매체의 서비스 라인에서는 여전히 이차적 인 선택입니다.

표준 EPDM/PP 컴파운드는 저렴한 비용과 광범위한 금형 호환성으로 인해 2025년 열가소성 가황 고무 시장 규모의 45.05%를 차지할 것으로 예측됩니다. 성숙한 배합은 대부분의 웨더 씰 및 인테리어 트림 사양을 충족하고 OEM 인증 성능 인증을 제공합니다. 제조업체는 이축 컴파운딩 라인을 활용하여 가교 밀도와 폴리프로필렌의 용융 유동성의 균형을 맞추어 높은 처리량에서 엄격한 치수 공차를 실현하고 있습니다. 그 결과, 비용 경쟁력이 성능 향상에 따른 잉여 효과를 능가하는 프로그램에서 전 세계 가공업체들은 표준 등급을 계속 선호하고 있습니다.

생산량 증가는 기업의 배출 목표에 따라 바이오 및 재생 소재 함유 제품에 의한 비율이 증가할 것으로 예측됩니다. 유럽의 순환경제 준수 의무화로 인해 바이오 유래 TPV는 6.76%의 가장 빠른 CAGR을 나타낼 것으로 예측됩니다. 산업폐기물 유래 소재를 최대 40%까지 함유한 재활용 소재 함유 등급은 OEM이 부품 설계 변경 없이 재활용 소재 사용률 기준을 달성할 수 있는 즉각적인 수단을 제공합니다. 고온용 TPV 등급은 틈새 시장이지만 전략적으로 150℃의 연속 사용이 요구되는 터보차저 호스 및 보닛 하부 개스킷에 공급됩니다.

동적 가교형 열가소성 엘라스토머(TPV) 보고서는 제품 유형(표준 EPDM/PP TPV, 고성능/내열 TPV 등), 용도(씰링 시스템/웨더스트립, 인테리어/외장 트림 등), 최종사용자 산업(자동차, 건축/건설, 소비재 등), 지역(아시아태평양, 북미 등) 등) 별로 분류되어 있습니다. 시장 예측은 킬로톤 단위로 제공됩니다.

2025년 아시아태평양이 45.70%의 매출 점유율을 차지하며 6.10%의 연평균 복합 성장률(CAGR)로 성장하여 다른 지역을 앞지를 것으로 예측됩니다. 중국의 연간 2,500만대 이상의 자동차 생산이 TPV 웨더스트립 수요 증가를 뒷받침하고 있으며, 일본의 재료과학 전문지식이 특수 등급의 개발을 촉진하고 있습니다. 인도의 신흥 자동차 시장에서는 사이클 타임 단축을 위해 EPDM 프로파일을 TPV로 대체하는 현지 압출 제조업체가 증가하면서 수요가 증가하고 있습니다. 지역적 원료 통합으로 폴리프로필렌과 EPDM의 원가가 낮아져 단가 우위를 확보하여 유럽과 북미 수출을 견인하고 있습니다. 아비엔트가 2025년 중국에서 의료용 TPU 생산을 확대한 것은 아시아 지역 의료기기 OEM 업체에 대한 공급 체제를 강화한 것으로 풀이됩니다.

북미에서는 미시간 주를 중심으로 한 자동차 산업 거점과 멕시코의 확대되는 조립 회랑에 수요가 집중되어 안정적인 수요를 기록하고 있습니다. 인플레이션 억제법의 EV 우대 조치로 배터리 팩 생산이 가속화되면서 저전도성 TPV 냉각 호스의 주문이 증가하고 있습니다. 쑤저우에 신설된 셀레네즈의 공인 컴파운더는 아시아산 산토프렌 펠릿을 현지 및 수출용 성형 공정에 공급하여 지역 간 공급망 설계를 구현하고 있습니다. 유럽은 지속가능성 도입의 지표적 지역으로, ISCC-PLUS 인증 TPV는 고급차 라인과 그린빌딩 외벽에서 두 자릿수 성장세를 보이고 있습니다. 폐차 지침에 따라 OEM 제조업체들은 재생재 함유량 증명이 의무화됨에 따라 PCR 배합 TPV 등급 수요가 증가하고 있습니다. 남미, 중동 및 아프리카는 동적 가교형 열가소성 엘라스토머(TPV) 시장에서 점유율이 작지만 증가 추세에 있습니다. 브라질에서는 자동차 생산 회복에 따라 현지 압출 공장에 대한 투자가 활발히 이루어지고 있습니다. 걸프 지역 생산자들은 풍부한 C3 및 디엔 원료를 활용하여 다운스트림 공정인 TPV 컴파운딩 사업 진출을 검토 중입니다. 아프리카에서는 건설 붐으로 인해 인프라 프로젝트를 위한 TPV 방수 프로파일의 소비가 증가하고 있지만, 재활용 물류의 제약으로 인해 완전한 순환 경제의 혜택이 지연되고 있습니다.

Thermoplastic Vulcanizate market size in 2026 is estimated at 476.56 kilotons, growing from 2025 value of 452.75 kilotons with 2031 projections showing 616.2 kilotons, growing at 5.26% CAGR over 2026-2031.

This steady expansion reflects a decisive shift by automakers, medical-device firms, and consumer-goods producers toward recyclable elastomers that offer thermoset-like performance at lower overall system costs. Lightweighting imperatives in electric vehicles, regulatory pressure for circular-economy compliance, and rising demand for soft-touch finishes in electronics amplify adoption across regions. Cost analyses show that TPVs can lower part manufacturing expenses by more than 60% versus EPDM rubber, mainly through shorter cycle times and elimination of post-curing steps. Suppliers now promote bio-based and recycled-content grades that cut cradle-to-gate carbon footprints by as much as 50%, providing a credible path for original equipment manufacturers (OEMs) to meet science-based emissions targets. These attributes position the Thermoplastic Vulcanizate market as a material solution of choice, while propylene and EPDM feedstock volatility limits the attractiveness of legacy thermosets.

Automakers accelerate material substitution to cut vehicle mass and meet carbon-dioxide fleet targets. TPV components weigh roughly 30% less than comparable EPDM seals yet maintain compression-set resilience, allowing battery-electric models to gain additional driving range. Recent dynamic-vulcanization advances have closed the gap in long-term fatigue performance, enabling TPVs to replace thermosets in door, glass-run, and sunroof systems without altering tooling. Regulatory pressure under the European Union's 2025 CO2 cap magnifies this shift, ensuring sustained demand inflow to the Thermoplastic Vulcanizate market.

Handheld electronics brands adopt TPVs to deliver a premium tactile feel while avoiding paint or over-mold steps that complicate recycling streams. The resin's direct-moldable surface eliminates secondary coatings and drops total part cost for grips, bumpers, and wearable-device housings. Integrating 25%-40% recycled content further slashes embodied emissions, and Asia-based contract molders can use standard injection machines, reducing capital barriers. Faster cycle times and compliance with RoHS and REACH regulations reinforce momentum.

High-acid, oil-field, or abrasive environments still favor specialty thermosets because TPVs can suffer gradual property loss beyond 150 °C. Although polyacrylate-modified TPVs extend service life, they remain a secondary choice for aggressive-media service lines.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Standard EPDM/PP compounds accounted for 45.05% of the Thermoplastic Vulcanizate market size in 2025, thanks to lower cost and broad tooling compatibility. The mature formulations meet the majority of weather-seal and interior-trim specifications, offering OEM-qualified performance certifications. Manufacturers leverage twin-screw compounding lines to balance crosslink density and polypropylene melt-flow, enabling tight dimensional tolerances at high throughputs. As a result, global processors continue to prioritize standard grades for programs where cost competitiveness outweighs incremental performance gains.

Volume growth will increasingly originate from bio-based and recycled-content offerings that align with corporate emissions goals. Bio-attributed TPVs are projected to post the fastest 6.76% CAGR, aided by European mandates for circular-economy compliance. Recycled-content variants containing up to 40% post-industrial material give OEMs an immediate path to hit recycled-material thresholds without redesigning parts. High-temperature TPV grades remain niche but strategic, supplying turbo-charger hoses and under-hood gaskets that demand 150 °C continuous use.

The Thermoplastic Vulcanizate Report is Segmented by Product Type (Standard EPDM/PP TPV, High-Performance/Heat-Resistant TPV, and More), Application (Sealing Systems and Weather-Strips, Interior and Exterior Trim, and More), End-User Industry (Automotive, Building and Construction, Consumer Goods, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Kilo Tons).

Asia-Pacific led with a 45.70% revenue share in 2025 and is forecast to grow at 6.10% CAGR, outpacing other regions. China's annual production of over 25 million vehicles underpins surging demand for TPV weatherstrips, while Japan's material-science expertise spurs specialty-grade development. India's emerging car market adds incremental volume through local extrusion houses that substitute EPDM profiles with TPV to trim cycle times. Regional feedstock integration lowers polypropylene and EPDM costs, creating a unit-cost advantage that drives exports to Europe and North America. Avient's 2025 expansion of medical-grade TPU output in China evidences supplier commitment to serve Asia-based medical-device OEMs.

North America records steady demand concentrated in Michigan-centric automotive hubs and Mexico's expanding assembly corridors. The Inflation Reduction Act's EV incentives accelerate battery-pack production, boosting call-offs for low-conductivity TPV coolant hoses. Celanese's newly qualified compounder in Suzhou provides Asian-sourced Santoprene pellets for local and export molding operations, illustrating cross-regional supply-chain design. Europe remains the bellwether for sustainability adoption, where ISCC-PLUS-certified TPVs enjoy double-digit growth in premium vehicle lines and green-building facades. The End-of-Life Vehicles Directive pushes OEMs to document recycled content, lifting demand for PCR-infused TPV grades. South America, the Middle East, and Africa together occupy a smaller but rising stake in the Thermoplastic Vulcanizate market. Brazil's revived auto output sparks investments in local extrusion plants, while Gulf-region producers consider downstream TPV compounding leveraging abundant C3 and diene feedstocks. Africa's construction boom increases consumption of TPV water-stop profiles in infrastructure projects, yet limited recycling logistics delay full circularity benefits.