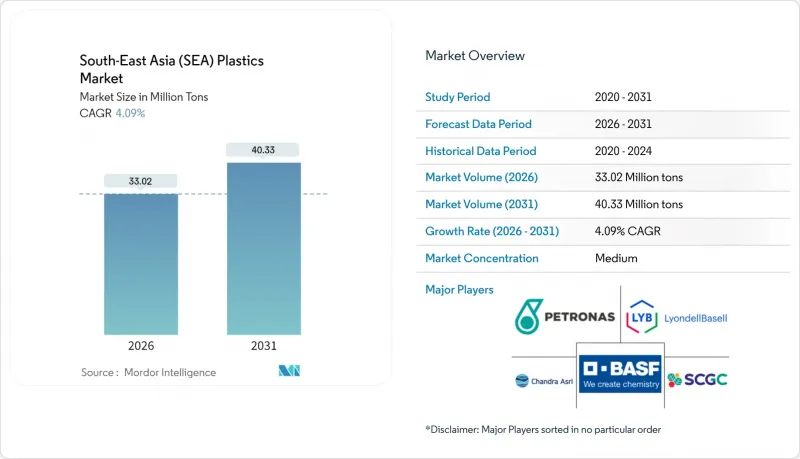

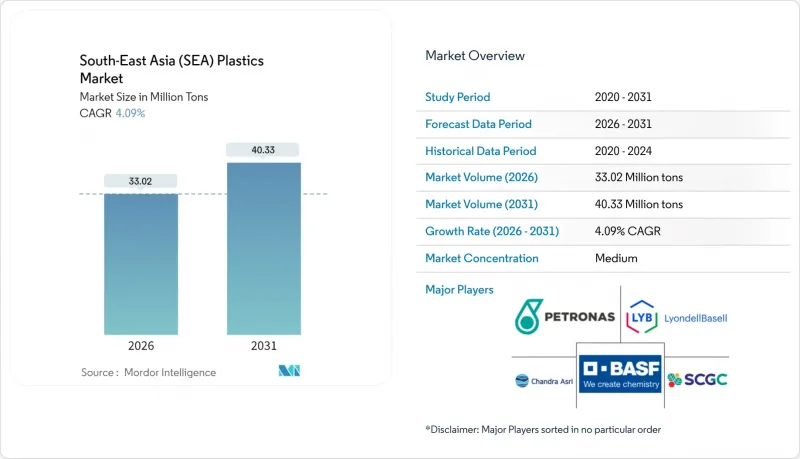

동남아시아의 플라스틱 시장은 2025년 3,170만 톤에서 2026년에는 3,302만 톤으로 성장하여 2026년부터 2031년까지 CAGR 4.09%를 기록하며 2031년까지 4,033만 톤에 달할 것으로 예측됩니다.

성장의 기반은 소비지출 증가, 수출 지향적 제조업의 확대, 그리고 가공업체 가동률을 높은 수준으로 유지하는 꾸준한 인프라 투자에 있습니다. 현지 생산능력 증대는 수입 의존도 감소와 원료의 안정적 공급에 기여하는 한편, 순환경제에 대한 규제 강화 흐름은 생산자들에게 기술 혁신과 재활용에 대한 투자를 유도하고 있습니다. 인도네시아의 투자 붐과 베트남의 급속한 공장 건설이 생산량 증가를 뒷받침하고 있지만, 아세안 주요 회원국들은 모두 지역 공급망을 확보하기 위해 석유화학 산업 다운스트림부문에 대한 특혜를 추진하고 있습니다. 실시간 공정 모니터링에서 예지보전에 이르는 디지털 제조 이니셔티브도 생산성 격차를 확대하여 대규모 통합 사업자의 비용 우위를 강화하고 있습니다.

가속화되는 도시 생활 방식과 지속적인 중산층 성장으로 인해 간편식 및 즉석 음료에 대한 수요가 증가함에 따라 컨버터는 다층 필름 및 경질 PET 용기의 생산량을 늘리고 있습니다. 베트남은 2024년 이후 포장 분야에 대한 외국인 직접투자(FDI)가 유입되고 있으며, 세계 브랜드 소유주들이 아세안 및 수출 시장을 위한 공급 기지를 설립하고 있습니다. 규제 당국은 식품 접촉 기준을 강화하고 있으며, 태국에서는 현재 식품과 접촉하는 모든 포장재에 대해 ISO 22000 인증이 의무화되어 있습니다. 이에 따라 가공업체들은 고기능성 배리어 수지와 항균 첨가제로의 전환을 추진하고 있습니다. 유통기한 연장 노력은 소매 체인 전체에 파급되어 산소 및 내습성이 강화된 폴리프로필렌 및 폴리에틸렌 등급에 대한 수요를 증가시키고 있습니다. 식료품 EC의 급격한 성장에 따라 가볍고 천공에 강한 포장 형태에 대한 이해관계자들의 요구가 높아지면서, 강도를 유지하면서 두께를 얇게 만들 수 있는 고탄성률 블렌드 소재로 빠르게 대체되고 있습니다.

2023년부터 2025년까지 가동될 대규모 크래커 및 폴리머 공장은 역내 무역의 흐름을 재편할 것입니다. 베트남 롱손 단지는 2023년 말 연간 165만 톤의 에틸렌 생산능력을 추가해 국내 가공업체들이 동북아시아에서 조달하던 원료를 안정적으로 공급할 수 있게 됐습니다. 인도네시아에서는 TPPI가 방향족 화학제품 라인의 병목현상을 해소하고, 롯데케미컬이 2025년 하반기에 연간 100만톤 규모의 크래커를 가동하면 연간 200만톤 이상의 모노머 증산이 가능할 것으로 예상됩니다. 중국의 석유화학제품 과잉 생산능력과 시기가 겹치면서 이들 프로젝트는 관세 다변화를 추구하는 세계 컨버터들에게 동남아시아 플라스틱 시장을 대체 공급 플랫폼으로 자리매김하고 있습니다. 5억 달러 이상의 프로젝트에 대한 면세 혜택과 경제특구 내 허가 절차 간소화 등 정부의 특혜로 인해 건설 일정이 단축되고, 건설 허들이 낮아져 지역 가공업체들이 장기적인 오프 테이크 계약을 체결할 수 있게 되었습니다.

태국의 비닐봉지 규제(2025년 3월 시행)는 생분해성 첨가제 사용과 최소 두께 기준을 의무화하여 쇼핑백 제조업체의 원재료 비용을 15-20% 상승시키고 있습니다. 싱가포르는 2025년 1월부터 플라스틱 폐기물 수입 금지 범위를 확대하여 국경을 넘는 스크랩 유입에 의존하던 지역 재활용 업체들을 압박하고 있습니다. 말레이시아에서 2026년부터 시행될 예정인 생산자책임재활용법(EPR)은 회수 및 재활용에 대한 재정적 책임을 제조업체에 이전하는 법입니다. 이 의무는 컴플라이언스 비용을 흡수할 수 있는 규모가 큰 사업자에게 유리하게 작용합니다. 이러한 조치는 일회용 제품 카테고리를 위협하고 있으며, 컨버터는 선반 공간을 유지하기 위해 재사용 및 퇴비화 가능한 옵션으로 전환해야 합니다.

2025년 기준 폴리에틸렌, 폴리프로필렌, PVC와 같은 전통적인 등급이 동남아시아 플라스틱 시장의 63.05%를 차지할 것으로 예상됩니다. 이는 포장재 및 소비재 분야에서 규모의 경제가 뒷받침하고 있습니다. 인도네시아와 베트남의 여러 기존 라인 증설로 지역 내 폴리올레핀 명목 생산능력은 전반적으로 향상되었으며, 수지 가격은 수입품 대비 경쟁력을 유지하고 있습니다.

엔지니어링 플라스틱은 수량 기준으로는 틈새시장이지만 전략적으로 중요한 시장이며, 내열성과 치수 안정성이 사양을 좌우하는 자동차 엔진룸 부품 및 전자기기 인클로저 분야에서 수주를 확보하고 있습니다. 현지 컴파운더는 유리섬유 강화 나일론과 PBT 블렌드에 대한 투자를 진행하여 OEM의 현지 조달 목표를 달성할 수 있도록 지원하고 있습니다. 전기자동차 보급을 위한 규제 강화로 UL 94V-0 규격에 부합하는 난연성 등급의 수요 확대가 가속화될 가능성이 있습니다.

바이오플라스틱은 동남아시아 플라스틱 시장에서 가장 빠른 CAGR 4.42%로 성장하고 있지만, 비용 프리미엄과 산업 퇴비화 인프라 부족이 보급을 억제하고 있습니다. SCG케미컬이 건설한 태국의 카사바 유래 바이오에틸렌 공장은 EN 13432 퇴비화 기준을 충족하는 바이오 PE를 컨버터에 공급하여 차별화된 지속가능성 인증을 원하는 브랜드 오너들의 소재 선택의 폭을 넓혀주고 있습니다. 말레이시아의 팜유 혁신 기금은 PHA와 PBS를 지원하고 있지만, 상업화 일정은 EU의 삼림 파괴 방지 규정에 따른 원료 인증 기준에 의존하고 있습니다.

동남아시아 플라스틱 시장 보고서는 종류별(재래식 플라스틱, 엔지니어링 플라스틱, 바이오플라스틱), 기술별(사출 성형, 블로우 성형 등), 용도별(포장, 전기/전자, 건축/건설, 자동차/운송 등), 지역별(인도네시아, 태국, 말레이시아, 베트남, 인도네시아, 태국, 말레이시아, 베트남 등)로 구분하여 분석하였습니다. 베트남 등)으로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

The South-East Asia Plastics market is expected to grow from 31.70 million tons in 2025 to 33.02 million tons in 2026 and is forecast to reach 40.33 million tons by 2031 at 4.09% CAGR over 2026-2031.

Growth rests on rising consumer spending, expanding export-oriented manufacturing, and steady infrastructure outlays that keep processors operating at high utilization rates. Local capacity additions trim import dependence and feedstock security, while regulatory momentum toward circular-economy practices forces producers to upgrade technology and invest in recycling. Indonesia's investment boom and Vietnam's rapid factory build-out underpin volume gains, but all major ASEAN members are channeling incentives into downstream petrochemicals to secure regional supply chains. Digital manufacturing initiatives-from real-time process monitoring to predictive maintenance-are also widening productivity differentials, reinforcing the cost advantages of large, integrated operators.

Accelerating urban lifestyles and sustained middle-class growth are intensifying demand for convenience foods and ready-to-drink beverages, prompting converters to raise runs of multi-layer films and rigid PET containers. Vietnam has attracted FDI since 2024 in packaging as global brand owners establish supply hubs to serve ASEAN and export markets. Regulators are tightening food-contact norms-Thailand now requires ISO 22000 certification on all packaging that touches edibles-nudging processors toward higher-spec barrier resins and antimicrobial additives. Shelf-life extension initiatives cascade through retail chains, boosting polypropylene and polyethylene grades engineered for oxygen and moisture resistance. With grocery e-commerce swelling, stakeholder pressure for lightweight yet puncture-resistant formats is spurring rapid material substitution toward high-modulus blends that enable downgauging without compromising integrity.

Large-scale crackers and polymer plants coming online between 2023-2025 redraw intraregional trade flows. Vietnam's Long Son complex added 1.65 million t/y of ethylene capacity in late 2023, providing domestic processors with feedstock security previously sourced from Northeast Asia. Indonesia is seeing more than 2 million t/y of extra monomer output as TPPI debottlenecks its aromatics train and Lotte Chemical inaugurates a 1 million t/y cracker in 2H 2025. Coinciding with China's petrochemical overcapacity, these projects position the South-East Asia plastics market as an alternative supply platform for global converters seeking tariff diversification. State incentives-tax holidays on projects exceeding USD 500 million and streamlined permitting inside special economic zones-have shortened build-out schedules and lowered hurdle rates, encouraging regional processors to lock in long-term offtake contracts.

Thailand's plastic bag decree, effective March 2025, mandates biodegradable additives and minimum thickness thresholds, raising input costs for shopping-bag producers by 15-20%. Singapore widened its plastic-waste import ban in January 2025, squeezing regional recyclers that relied on cross-border scrap inflows. Malaysia's forthcoming Extended Producer Responsibility (EPR) law shifts financial responsibility for collection and recycling to manufacturers starting in 2026, an obligation that favors scale players able to absorb compliance spend. These measures threaten single-use categories, forcing converters to pivot toward reusable and compostable options to keep shelf space.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Traditional grades-polyethylene, polypropylene, and PVC-held a 63.05% share of the South-East Asia plastics market in 2025, supported by scale economics in packaging and consumer goods applications. Several brownfield line extensions in Indonesia and Vietnam lift aggregate regional polyolefin nameplate capacity and keep resin pricing competitive versus imports.

Engineering plastics remain niche in volume terms yet strategically important, capturing contracts in automotive under-the-hood parts and electronics housings where heat resistance and dimensional stability drive specification. Local compounders are investing in glass-fiber reinforced nylon and PBT blends to satisfy OEM localization targets. Regulatory push for electric vehicle adoption could accelerate demand for flame-retardant grades compliant with UL 94 V-0 standards.

Bioplastics are climbing at a 4.42% CAGR, the fastest within the South-East Asia plastics market, yet cost premiums and limited infrastructure for industrial composting temper penetration. Thailand's cassava-based bio-ethylene plant, built by SCG Chemicals, supplies converters with bio-PE that meets EN 13432 compostability, widening material choice for brand owners seeking differentiated sustainability credentials. Malaysia's palm oil innovation fund backs PHAs and PBS, though commercialization schedules hinge on feedstock certification thresholds under EU deforestation rules.

The South-East Asia Plastics Market Report is Segmented by Type (Traditional Plastics, Engineering Plastics, and Bioplastics), Technology (Injection Molding, Blow Molding, and More), Application (Packaging, Electrical and Electronics, Building and Construction, Automotive and Transportation, and More), and Geography (Indonesia, Thailand, Malaysia, Vietnam, and More). The Market Forecasts are Provided in Terms of Volume (Tons).