EdTech 및 스마트 교실 시장 : 솔루션별, 최종사용자별, 전개 유형별 - 예측(-2030년)

Edtech and Smart Classrooms Market by Solution (Projection & Display Systems, Adaptive & Personalized Learning, Augmented Reality (AR), Virtual Reality (VR) & Simulations), End User, and Deployment Type - Global Forecast to 2030

상품코드:1816008

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 301 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

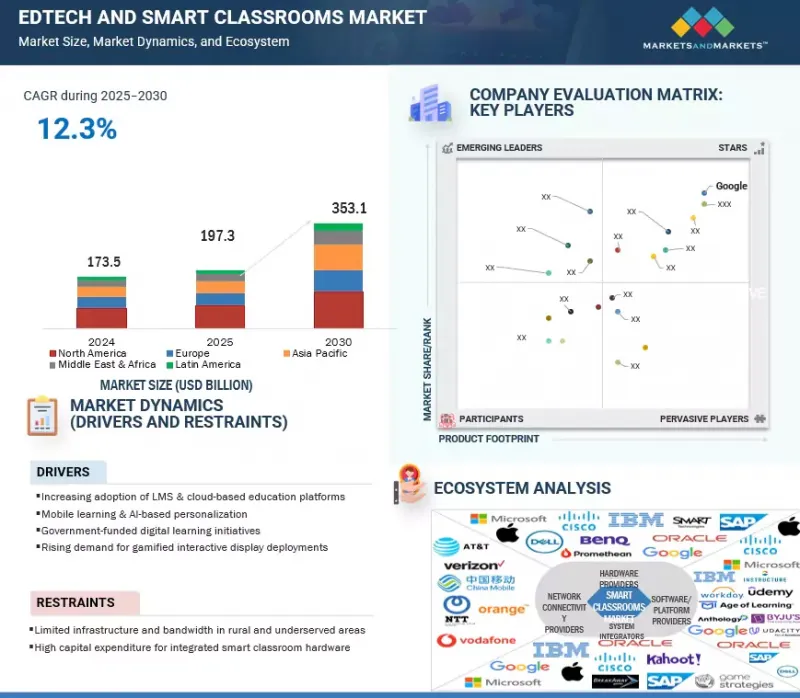

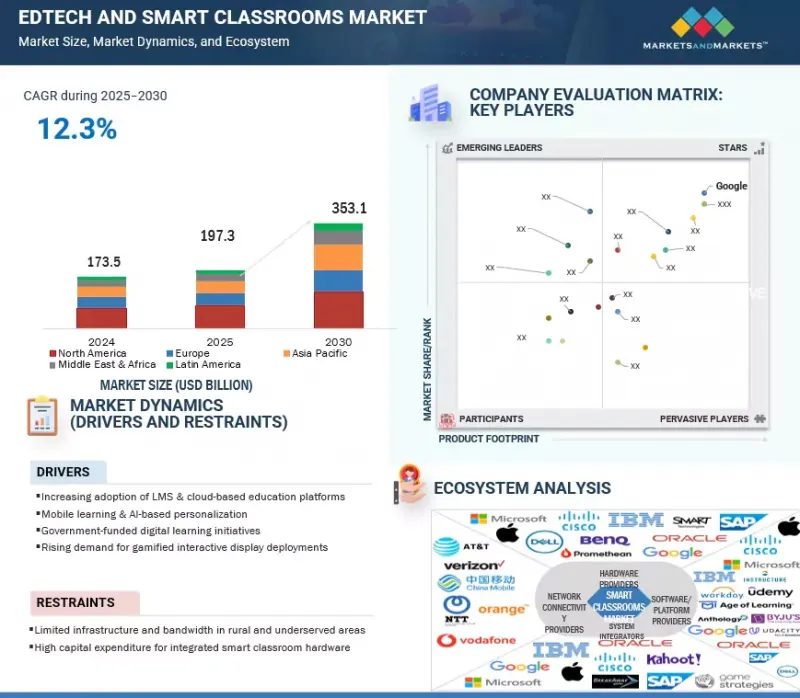

세계의 EdTech 및 스마트 교실 시장 규모는 2025년에 추정 1,973억 달러, 2030년까지 3,531억 달러에 이를 것으로 예측되어 CAGR 12.3%의 성장이 전망됩니다.

조사 범위

조사 대상 연도

2020-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

100만/10억 달러

부문

솔루션, 최종사용자, 전개 유형, 지역

대상 지역

북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카

세계 각국의 정부는 에듀테크 스마트 교실의 채택을 가속화하는 데 중요한 역할을 하고 있습니다. 디지털 교육 인프라에 대한 공공 부문의 투자, 정책 프레임워크, 자금 지원이 이 시장에 활력을 불어넣고 있습니다. 예를 들어, 인도의 PM eVidya 이니셔티브는 모든 학생들에게 온라인 교육에 대한 멀티모드 접근을 제공하는 것을 목표로 하고 있으며, 유럽연합의 Digital Education Action Plan(2021-2027)은 고성능 디지털 생태계의 육성에 초점을 맞추었습니다. 초점을 맞추었습니다. 마찬가지로 미국은 STEM 교육 및 농촌 지역 학교의 광대역 접속을 지원하는 프로그램에 많은 투자를 하고 있습니다.

각국 정부는 태블릿, 전자칠판, 와이파이 접속 등 하드웨어에 대한 보조금을 지원함으로써 기술을 활용한 학습을 보다 종합적으로 활용하고 있습니다. 이러한 노력은 AI, AR/VR, 클라우드 플랫폼 등 신기술의 교실 내 활용을 촉진하고 있습니다. 학교 외에도 직업훈련과 스킬업 프로그램도 정부 지원으로 운영되고 있어 보다 폭넓은 학습자층을 확보하고 있습니다. 이러한 노력은 디지털 격차를 해소할 뿐만 아니라, 에듀테크 기업의 장기적인 성장 기회도 보장하고 있습니다.

"AR-VR-시뮬레이션 부문이 예측 기간 동안 가장 빠르게 성장할 것으로 예측됩니다. "

AR-VR-시뮬레이션 툴은 몰입감 있는 체험형 학습 환경을 제공함으로써 교실을 변화시키고 있습니다. 이 솔루션은 헤드셋, 모바일 앱, 3D 시뮬레이션을 사용하여 가상 실험실, 역사 재현, 대화형 기술 기반 훈련 모듈을 생성합니다. AR 앱은 교과서에 디지털 컨텐츠를 중첩시킬 수 있고, VR은 의대생들이 가상 수술실에서 수술 연습을 할 수 있게 해줍니다. ClassVR, zSpace, Meta와 같은 벤더들은 보다 저렴한 하드웨어와 클라우드 기반 시뮬레이션 라이브러리를 통해 AR/VR의 채택을 촉진하고 있습니다. 이 부문은 특히 STEM 교육 및 직업 훈련에서 개인화된 체험형 학습에 대한 수요가 증가함에 따라 가장 높은 CAGR을 보일 것으로 예측됩니다. 능력 기반 학습과 게임화로의 전환으로 인해 채택이 더욱 가속화되고 있습니다. 또한, 몰입형 기술을 교실에 통합하려는 정부 및 기관의 노력이 급속히 확대되고 있으며, AR/VR은 에듀테크 및 스마트 교실 생태계에서 중요한 차세대 솔루션으로 자리 잡고 있습니다.

"K-12 부문이 예측 기간 동안 가장 큰 시장 규모를 형성할 것으로 예측됩니다. "

K-12 부문은 초중등 교육에서의 기술 채택을 의미하며, 스마트 도구의 통합을 통해 교육의 질과 학생 참여도를 향상시킬 수 있습니다. 이 범주의 학교들은 디지털 컨텐츠 제공 플랫폼, 게임화된 학습 도구, 교실 협업 솔루션 등을 빠르게 도입하여 기술에 정통한 학습자를 수용하고 있습니다. 이 분야의 강력한 트렌드는 스마트 칠판, 태블릿, AI를 활용한 적응형 시스템으로 지원되는 대화형 학습 환경의 통합으로, 개인별 학습 속도에 맞추어 교육을 개별화할 수 있습니다. 구글(Google Classroom 제공) 및 SMART Technologies와 같은 벤더들은 K-12 생태계에 깊숙이 통합되어 있으며, 저렴한 가격에 확장 가능한 도구를 제공합니다. 인도의 디지털 인디아(Digital India), 미국의 E-rate 프로그램 등 각 지역 정부는 학교의 디지털 인프라에 자금을 지원함으로써 채택을 더욱 가속화하고 있습니다. 혁신적인 교육에 대한 학부모 수요가 증가함에 따라, K-12는 여전히 에듀테크 솔루션의 가장 큰 소비층으로, 세계 시장의 꾸준한 성장을 가속하고 있습니다.

세계의 EdTech-스마트 교실 시장에 대해 조사 분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 지견

EdTech 및 스마트 교실 시장 기업에 있어서 매력적인 기회

EdTech 및 스마트 교실 시장 : 전개 방식별

EdTech 및 스마트 교실 시장 : 솔루션별

EdTech 및 스마트 교실 시장 : 최종사용자별

북미 EdTech 및 스마트 교실 시장 : 최종사용자별, 지역별

제5장 시장 개요와 산업 동향

서론

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

사례 연구 분석

생태계 분석

공급망 분석

기술 분석

주요 기술

보완 기술

인접 기술

Porter의 Five Forces 분석

가격 결정 분석

평균 판매 가격 : 주요 기업, 지역별

EdTech 및 스마트 교실 솔루션 참고 가격 분석

특허 분석

무역 분석

수입 시나리오

수출 시나리오

규제 상황

규제기관, 정부기관, 기타 조직

주요 규제

규제 : 지역별

고객의 비즈니스에 영향을 미치는 동향과 혼란

주요 이해관계자와 구입 기준

주요 컨퍼런스 및 이벤트(2025년-2026년)

EdTech 및 스마트 교실 시장에 대한 생성형 AI의 영향

EdTech 및 스마트 교실 시장에서의 생성형 AI 이용 사례

사례 연구

벤더 대처

비즈니스 모델

투자 상황과 자금조달 시나리오

2025년 미국 관세의 영향

서론

주요 관세율

국가/지역에 대한 영향

최종 이용 산업에 대한 영향

제6장 EdTech 및 스마트 교실 시장 : 솔루션별

서론

학습 컨텐츠 및 커리큘럼 관리

교실 인터랙션 및 협업 툴

프로젝션 및 디스플레이 시스템

학생 모니터링 및 참가 관리

평가 및 채점 툴

학생 정보 시스템(SIS) 및 학교 ERP

적응형/개별 학습

AR/VR/시뮬레이션

특별 교육 및 접근성 툴

기타 솔루션

제7장 EdTech 및 스마트 교실 시장 : 최종사용자별

서론

K-12

고등교육

직업 훈련 센터

제8장 EdTech 및 스마트 교실 시장 : 전개 유형별

서론

On-Premise

클라우드

제9장 EdTech 및 스마트 교실 시장 : 지역별

서론

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시경제 전망

영국

독일

프랑스

이탈리아

기타 유럽

아시아태평양

아시아태평양의 거시경제 전망

중국

인도

일본

호주 및 뉴질랜드

한국

기타 아시아태평양

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

아랍에미리트(UAE)

사우디아라비아

남아프리카공화국

기타 중동 및 아프리카

라틴아메리카

라틴아메리카의 거시경제 전망

브라질

멕시코

기타 라틴아메리카

제10장 경쟁 구도

서론

주요 시장 진출기업의 전략/강점(2022년-2025년)

매출 분석(2020년-2024년)

시장 점유율 분석(2024년)

브랜드/제품 비교

기업 평가와 재무 지표

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제11장 기업 개요

서론

주요 기업

MICROSOFT

GOOGLE

PEARSON

ANTHOLOGY

INSTRUCTURE

CISCO

IBM

MCGRAW HILL

ORACLE

POWERSCHOOL

기타 기업

2U INC

ELLUCIAN

TURNITIN

KAHOOT!

SMART TECHNOLOGIES

IXL LEARNING

D2L

WORKDAY

PROMETHEAN

DISCOVERY EDUCATION

BYJU'S

YUANFUDAO

VIPKID

17ZUOYE

SEESAW

UDACITY

AGE OF LEARNING

NEARPOD

제12장 인접 시장/관련 시장

서론

학습 관리 시스템 시장

시장의 정의

시장 개요

학습 관리 시스템 시장 : 제공 별

학습 관리 시스템 시장 : 딜리버리 방식별

학습 관리 시스템 시장 : 조직 규모별

학습 관리 시스템 시장 : 전개 유형별

학습 관리 시스템 시장 : 응용 분야별

학습 관리 시스템 시장 : 사용자 유형별

학습 관리 시스템 시장 : 지역별

스마트 러닝 시장

시장의 정의

시장 개요

스마트 러닝 시장 : 제공 별

스마트 러닝 시장 : 하드웨어별

스마트 러닝 시장 : 솔루션별

스마트 러닝 시장 : 서비스별

스마트 러닝 시장 : 학습 유형별

스마트 러닝 시장 : 최종사용자별

스마트 러닝 시장 : 지역별

제13장 부록

LSH

영문 목차

영문목차

The edtech and smart classrooms market is estimated at USD 197.3 billion in 2025 and is expected to reach USD 353.1 billion by 2030 at a CAGR of 12.3%.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD) Million/Billion

Segments

By Solution, End User, Deployment Type, and Region

Regions covered

North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America

Governments worldwide are playing a crucial role in accelerating the adoption of edtech and smart classrooms. Public sector investment in digital education infrastructure, policy frameworks, and funding support has given momentum to this market. For instance, India's PM eVidya initiative aims to provide multi-mode access to online education for all students, while the European Union's Digital Education Action Plan (2021-2027) focuses on fostering high-performing digital ecosystems. Similarly, the US invests heavily in programs supporting STEM education and broadband access to rural schools.

Governments are making technology-enabled learning more inclusive by subsidizing hardware such as tablets, digital boards, and Wi-Fi access. These initiatives also promote the use of emerging technologies like AI, AR/VR, and cloud platforms in classrooms. Beyond schools, vocational training and upskilling programs are also supported by government funding, ensuring a broader learner base. Such initiatives not only bridge the digital divide but also ensure long-term growth opportunities for edtech players.

"Augmented Reality (AR), Virtual Reality (VR) & Simulations segment will witness the fastest growth during the forecast period."

AR, VR, and simulation tools are transforming classrooms by providing immersive, experiential learning environments. These solutions use headsets, mobile apps, and 3D simulations to create virtual laboratories, historical recreations, and interactive skill-based training modules. AR apps can overlay digital content on textbooks, while VR enables medical students to practice surgeries in virtual operating rooms. Vendors such as ClassVR, zSpace, and Meta are pushing AR/VR adoption through more affordable hardware and cloud-based simulation libraries. This segment is poised for the highest CAGR due to rising demand for personalized and experiential learning, especially in STEM education and vocational training. The shift toward competency-based learning and gamification is further accelerating adoption. Additionally, government and institutional initiatives to integrate immersive technologies in classrooms are driving rapid expansion, making AR/VR a critical next-wave solution in the edtech and smart classrooms ecosystem.

"The K-12 segment is expected to have the largest market size during the forecast period."

The K-12 segment refers to technology adoption across primary and secondary education, where smart tools are integrated to improve teaching quality and student engagement. Schools in this category are rapidly embracing digital content delivery platforms, gamified learning tools, and classroom collaboration solutions to cater to tech-savvy learners. A strong trend in this segment is the integration of interactive learning environments, supported by smart boards, tablets, and AI-powered adaptive systems that personalize education to individual learning paces. Vendors like Google (with Google Classroom) and SMART Technologies are deeply embedded in K-12 ecosystems, providing affordable and scalable tools. Governments across regions, such as India's Digital India initiative and the US E-rate program, are further accelerating adoption by funding digital infrastructure in schools. With increasing parental demand for innovative education, K-12 remains the largest consumer of edtech solutions, driving consistent growth in the global market.

"Asia Pacific is expected to record the highest growth rate during the forecast period."

The edtech and smart classrooms market in Asia Pacific continues to emerge as a global hub for edtech adoption, supported by government initiatives such as India's National Education Policy (NEP) 2020 and China's emphasis on "smart education" infrastructure. Countries like South Korea and Singapore are leading with investments in AI-driven learning platforms and adaptive assessment tools, making classrooms more personalized and data-driven. Partnerships between edtech startups and telecom operators are accelerating digital access, ensuring rural and remote learners are included in the digital transformation wave. The region also witnesses active participation from players like Byju's, Yuanfudao, and ClassIn, who are expanding content libraries and offering hybrid classroom solutions to cater to a diverse student base.

Breakdown of primaries

The study contains insights from various industry experts, from solution vendors to tier 1 companies. The break-up of the primaries is as follows:

By Company Type: Tier 1 - 48%, Tier 2 - 37%, and Tier 3 - 15%

By Designation: C-level - 35%, D-level - 40%, and Others - 25%

By Region: North America - 40%, Europe - 20%, Asia Pacific - 30%, Middle East & Africa - 5%, and Latin America - 5%

The major players in the edtech and smart classrooms market include Pearson (UK), Cisco (US), Anthology (US), IBM (US), McGraw Hill Education (US), Google (US), Microsoft (US), Oracle (US), PowerSchool (US), Instructure (US), 2U (US), Ellucian (US), Turnitin (US), Kahoot (Norway), Smart Technologies (Canada), IXL Learning (US), D2L (Canada), Workday (US), Discovery Education (US), Promethean (US), Byju's (India), Yuanfudao (China), VipKid (US), 17Zuoye (China), Seesaw (US), Nearpod (US), Age of Learning (US), and Brightbytes (US). These players have adopted various growth strategies, such as partnerships, agreements, collaborations, product launches, enhancements, and acquisitions, to expand their edtech and smart classrooms market footprint.

Research Coverage

The market study covers the edtech and smart classrooms market size and growth potential across different segments, including solutions, end user, deployment type, and region. The solutions studied under the edtech and smart classrooms market include learning content & curriculum management, classroom interaction & collaboration tools, projection & display systems, student monitoring & attendance management, assessment & grading tools, student information systems (SIS) & school ERP, adaptive & personalized learning, augmented reality (AR), virtual reality (VR) & simulations, special education & accessibility tools, and other solutions. The end user segment includes K-12, higher education, and vocational training centers. The deployment type segment includes on-premises and cloud, where cloud is further segmented into private, public, and hybrid. The regional analysis of the edtech and smart classrooms market covers North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

Key Benefits of Buying the Report

This report will help market leaders and new entrants with information on the closest approximations of the global edtech and smart classrooms market's revenue numbers and subsegments. It will also help stakeholders understand the competitive landscape, gain insights, and plan suitable go-to-market strategies. Moreover, the report will provide insights for stakeholders to understand the market's pulse and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides the following insights.

1. Analysis of key drivers (increasing adoption of LMS & cloud-based education platforms, mobile learning & AI-based personalization, government-funded digital learning initiatives, and rising demand for gamified interactive display deployments), restraints (limited infrastructure and bandwidth in rural and underserved areas, and high capital expenditure for integrated smart classroom hardware), opportunities (demand for interoperable, analytics-enabled platforms, rising preference for hybrid learning models, and rising demand for AR/VR-enabled immersive learning solutions), and challenges (integration with legacy systems and cross-platform compatibility, and cybersecurity risks and regulatory compliance) influencing the growth of the edtech and smart classrooms market

2. Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the edtech and smart classrooms market

3. Market Development: The report provides comprehensive information about lucrative markets, analyzing the edtech and smart classrooms market across various regions

4. Market Diversification: Comprehensive information about new products and services, untapped geographies, recent developments, and investments in the edtech and smart classrooms market

5. Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Pearson (UK), Cisco (US), Anthology (US), IBM (US), McGraw Hill Education (US), Google (US), Microsoft (US), Oracle (US), PowerSchool (US), Instructure (US), 2U (US), Ellucian (US), Turnitin (US), Kahoot (Norway), Smart Technologies (Canada), IXL Learning (US), D2L (Canada), Workday (US), Discovery Education (US), Promethean (US), Byju's (India), Yuanfudao (China), VipKid (US), 17Zuoye (China), Seesaw (US), Nearpod (US), Age of Learning (US), and Brightbytes (US)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.2 PRIMARY DATA

2.1.2.1 Breakup of primary profiles

2.1.2.2 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.2.1 TOP-DOWN APPROACH

2.2.2 BOTTOM-UP APPROACH

2.3 MARKET FORECAST

2.4 DATA TRIANGULATION

2.5 RESEARCH ASSUMPTIONS

2.6 LIMITATIONS OF STUDY

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN EDTECH & SMART CLASSROOMS MARKET

4.2 EDTECH & SMART CLASSROOMS MARKET, BY DEPLOYMENT MODE

4.3 EDTECH & SMART CLASSROOMS MARKET, BY SOLUTION

4.4 EDTECH & SMART CLASSROOMS MARKET, BY END USER

4.5 NORTH AMERICA: EDTECH & SMART CLASSROOMS MARKET, BY END USER AND REGION

5 MARKET OVERVIEW AND INDUSTRY TRENDS

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increase in adoption of LMS and cloud-based education platforms

5.2.1.2 Mobile learning and AI-based personalization

5.2.1.3 Government-funded digital learning initiatives

5.2.1.4 Rise in demand for gamified interactive display deployments

5.2.2 RESTRAINTS

5.2.2.1 Limited infrastructure and bandwidth in rural and underserved areas

5.2.2.2 High capital expenditure for integrated smart classroom hardware

5.2.3 OPPORTUNITIES

5.2.3.1 Demand for interoperable, analytics-enabled platforms

5.2.3.2 Rise in preference for hybrid learning models

5.2.3.3 Rise in demand for AR/VR-enabled immersive learning solutions

5.2.4 CHALLENGES

5.2.4.1 Integration with legacy systems and cross-platform compatibility

5.2.4.2 Cybersecurity risks and regulatory compliance

5.3 CASE STUDY ANALYSIS

5.3.1 GENERATION: YOU EMPLOYED, INC. EMPLOYED SCALES GLOBAL WORKFORCE TRAINING WITH INSTRUCTURE'S CANVAS LMS

5.3.2 FORT BEND ISD FUTURE-PROOFED CLASSROOMS WITH SMART TECHNOLOGIES' OPS MODULES

5.3.3 CHONG GENE HANG COLLEGE PARTNERS WITH LENOVO FOR AI-DRIVEN EDUCATION

5.3.4 AGORA CYBER CHARTER SCHOOL ENHANCED VIRTUAL SCIENCE INSTRUCTION WITH DISCOVERY EDUCATION'S MYSTERY SCIENCE

5.3.5 SAANICH SCHOOL DISTRICT STREAMLINES STUDENT PROGRESS REPORTING WITH D2L

5.4 ECOSYSTEM ANALYSIS

5.5 SUPPLY CHAIN ANALYSIS

5.6 TECHNOLOGY ANALYSIS

5.6.1 KEY TECHNOLOGIES

5.6.1.1 Learning management systems (LMS)

5.6.1.2 Interactive flat panel displays (IFPDs)

5.6.1.3 Virtual classroom platforms

5.6.1.4 Digital content creation tools

5.6.2 COMPLEMENTARY TECHNOLOGIES

5.6.2.1 AI-powered assessment tools

5.6.2.2 Classroom management software

5.6.2.3 Video-based learning platforms

5.6.2.4 Adaptive learning engines

5.6.3 ADJACENT TECHNOLOGIES

5.6.3.1 Augmented reality (AR) for experiential learning

5.6.3.2 Blockchain for academic credentialing

5.6.3.3 Learning record stores (LRS)

5.7 PORTER'S FIVE FORCES ANALYSIS

5.7.1 THREAT OF NEW ENTRANTS

5.7.2 THREAT OF SUBSTITUTES

5.7.3 BARGAINING POWER OF SUPPLIERS

5.7.4 BARGAINING POWER OF BUYERS

5.7.5 INTENSITY OF COMPETITIVE RIVALRY

5.8 PRICING ANALYSIS

5.8.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY REGION

5.8.2 INDICATIVE PRICING ANALYSIS FOR EDTECH & SMART CLASSROOM SOLUTIONS

5.9 PATENT ANALYSIS

5.10 TRADE ANALYSIS

5.10.1 IMPORT SCENARIO

5.10.2 EXPORT SCENARIO

5.11 REGULATORY LANDSCAPE

5.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.11.2 KEY REGULATIONS

5.11.2.1 North America

5.11.2.1.1 US

5.11.2.1.2 Canada

5.11.2.2 Europe

5.11.2.3 Asia Pacific

5.11.2.3.1 South Korea

5.11.2.3.2 China

5.11.2.4 Rest of the World

5.11.2.4.1 UAE

5.11.2.4.2 South Africa

5.11.2.4.3 Brazil

5.11.2.5 General Data Protection Regulation

5.11.2.6 SEC Rule 17a-4

5.11.2.7 ISO/IEC 27001

5.11.2.8 University Grants Commission Regulations, 2018

5.11.2.9 Higher Education Opportunity Act - 2008

5.11.2.10 Distance Learning and Innovation Regulation

5.11.3 REGULATIONS, BY REGION

5.12 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.13.2 BUYING CRITERIA

5.14 KEY CONFERENCES AND EVENTS, 2025-2026

5.15 IMPACT OF GENERATIVE AI ON EDTECH & SMART CLASSROOM MARKET

5.15.1 USE CASES OF GENERATIVE AI IN EDTECH & SMART CLASSROOMS MARKET

5.15.2 CASE STUDIES

5.15.2.1 iSchoolConnect and Google Cloud transform AI-driven admissions in higher education

5.15.2.2 Saxion University leverages D2L and LearnWise AI to streamline LMS transition and student support