내시경 재처리 시장(-2030년) : 제품 유형(AER, HLD 및 테스트 스트립, 세제 및 물티슈, 내시경 건조/보관/컨베이어 시스템, 트래킹 솔루션), 내시경 유형(연성, 경성), 최종사용자(병원, ASC, 전문 클리닉)

Endoscope Reprocessing Market by Product (AER, HLD & Test Strip, Detergent & Wipe, Endoscope Drying, Storage, & Transport System, Tracking Solution), Endoscope Type (Flexible, Rigid), End User (Hospital, ASC, Specialty Clinic) - Global Forecast to 2030

상품코드:1811755

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 298 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

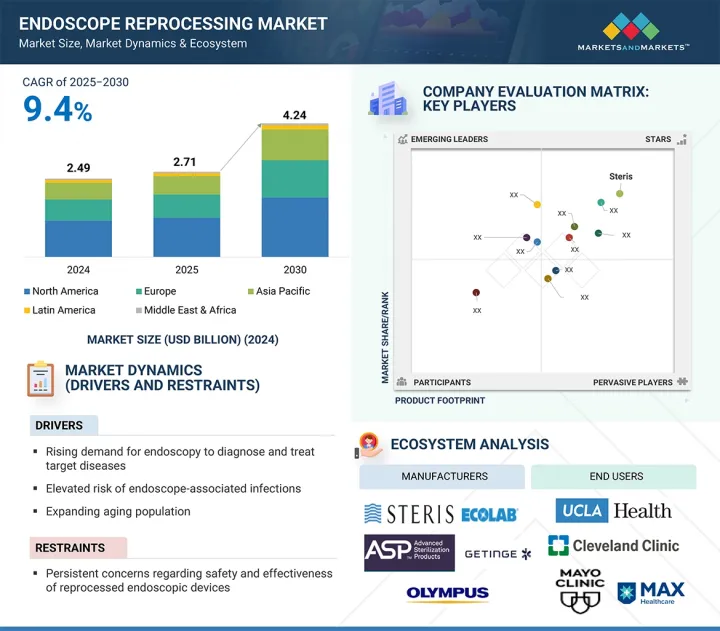

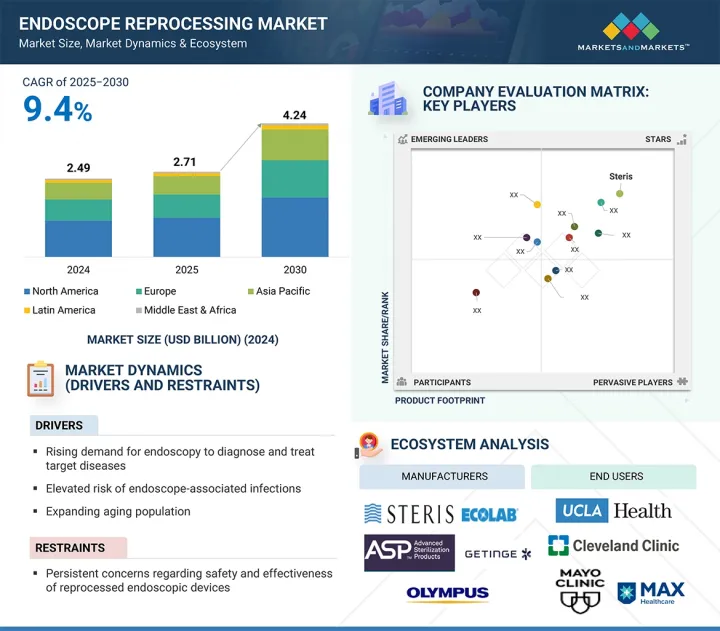

세계의 내시경 재처리 시장 규모는 2025년 27억 1,000만 달러에서 예측 기간 중 CAGR 9.4%로 성장을 지속하여, 2030년에는 42억 4,000만 달러에 이를 것으로 예측됩니다.

조사 범위

조사 대상 연도

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

금액(달러)

부문

제품 유형, 내시경 유형, 최종사용자

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동&아프리카

세계 내시경 재시술 시장의 성장은 주로 소화기, 호흡기, 비뇨기 질환의 유병률 증가와 전 세계 노인 인구 증가에 따른 내시경 시술 건수 증가에 의해 주도되고 있습니다. 또한, 오염되거나 부적절하게 소독된 내시경과 관련된 감염 위험에 대한 인식이 높아짐에 따라 의료 기관은 더욱 엄격한 재처리 프로토콜을 도입하고 있으며, 이는 고급 재처리 솔루션에 대한 수요를 더욱 증가시키고 있습니다.

또한, FDA, CDC, SGNA와 같은 국제 보건 당국의 규제 강화와 최신 가이드라인의 업데이트는 보다 안전하고 표준화된 재처리 방법을 촉진하고 있습니다. 자동 재처리 시스템 도입 확대, 의료 인프라에 대한 투자 증가, 환자 안전 향상을 위한 전 세계적인 노력도 시장 성장을 견인하고 있습니다. 그러나 고가의 설비 투자 및 복잡한 재처리 워크플로우와 같은 문제는 시장 확대를 제약할 수 있으며, 특히 자원이 한정된 지역에서 더욱 두드러집니다.

"내시경 유형별로는 연성 내시경 부문이 2024년 가장 큰 점유율을 차지했습니다."

2024년에는 소화기내과, 호흡기내과, 비뇨기과에서 진단 및 치료에 널리 사용되는 연성 내시경 부문이 시장을 주도했습니다. 연성 내시경은 해부학적으로 접근이 어려운 부위에 쉽게 접근할 수 있고, 환자의 편안함을 높일 수 있다는 점에서 선호되고 있습니다. 대장내시경이나 기관지 내시경과 같은 일상적 및 고급 시술이 증가함에 따라 교차 감염을 방지하고 안전을 보장하는 효과적인 재처리 솔루션에 대한 수요도 증가하고 있습니다. 또한, 십이지장경과 같은 복잡한 기기에 대한 엄격한 세척 기준에 대한 규제 강화로 인해 연성 내시경에 대응하는 재처리 시스템의 도입이 촉진되고 있습니다.

"최종 사용자별로는 병원 및 외래수술센터(ASC) 부문이 2024년 가장 큰 점유율을 차지할 것으로 예상되며, 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다."

이러한 성장은 고도의 인프라 구축, 감염 예방에 대한 자금 투입, 자동 재처리 장비 도입을 통한 규제 및 인증 기준 대응 등의 요인에 의해 뒷받침되고 있습니다. 또한, 병원은 의료 관련 감염(HAI) 감소와 최신 재처리 프로토콜 준수를 중요시하고 있으며, 이에 따라 적합하고 효율적인 시스템에 대한 요구가 빠르게 증가하고 있습니다. 외래 수술센터 역시 비용 절감과 환자 회전율 향상 등의 장점으로 내시경 시술 건수가 증가하고 있으며, 높은 처리 능력을 갖춘 재처리 솔루션에 대한 수요가 증가하고 있습니다.

세계의 내시경 재처리 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

고객 사업에 영향을 미치는 동향/혼란

가격 분석

밸류체인 분석

공급망 분석

생태계 분석

투자 및 자금조달 시나리오

기술 분석

특허 분석

무역 분석

2025-2026년 주요 컨퍼런스 및 이벤트

규제 분석

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

AI/생성형 AI가 내시경 재처리 시장에 미치는 영향

2025년 미국 관세 규제가 내시경 재처리 시장에 미치는 영향

제6장 내시경 재처리 시장 : 제품별

내시경 재처리 장비

자동 내시경 재처리 장비

내시경 건조, 보관 및 운송 시스템

내시경 재처리 소모품

세제와 웨트 티슈

고수준 소독제 및 테스트 스트립

기타

내시경 추적 솔루션

제7장 내시경 재처리 시장 : 내시경 유형별

연성 내시경

경성 내시경

제8장 내시경 재처리 시장 : 최종사용자별

병원 및 ASC

전문 클리닉

기타

제9장 내시경 재처리 시장 : 지역별

북미

거시경제 전망

미국

캐나다

유럽

거시경제 전망

독일

영국

프랑스

이탈리아

스페인

기타

아시아태평양

거시경제 전망

일본

중국

인도

호주

기타

라틴아메리카

거시경제 전망

브라질

멕시코

기타

중동 및 아프리카

제10장 경쟁 구도

주요 시장 진출기업의 전략/강점

매출 분석

시장 점유율 분석

기업 평가와 재무 지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 기업

기업 평가 매트릭스 : 스타트업/중소기업

경쟁 시나리오

제11장 기업 개요

주요 기업

STERIS

ASP

OLYMPUS CORPORATION

GETINGE AB

ECOLAB INC.

HOYA CORPORATION

CONMED CORPORATION

THE MIELE GROUP

ARC HEALTHCARE SOLUTIONS

METREX RESEARCH, LLC

기타 기업

MEDALKAN

MICRO-SCIENTIFIC, LLC

ENDO-TECHNIK W. GRIESAT GMBH

BES HEALTHCARE LTD

FUJIFILM HOLDINGS CORPORATION

BORER CHEMIE AG

MEDONICA CO. LTD

TUTTNAUER

SHINVA MEDICAL INSTRUMENT CO., LTD.

SBSYSTEM

OLIVE HEALTH CARE

MMM GROUP

AMITY INTERNATIONAL

MIXTA MEDIKAL

MEDICAL DEVICES GROUP SRL

제12장 부록

LSH

영문 목차

영문목차

The global endoscope reprocessing market is projected to reach USD 4.24 billion by 2030 from USD 2.71 billion in 2025, at a CAGR of 9.4% during the forecast period.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Product, type of endoscope, end user

Regions covered

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

The global endoscope reprocessing market growth is mainly driven by the increasing number of endoscopic procedures, supported by the rising prevalence of gastrointestinal, respiratory, and urological conditions, as well as the growing geriatric population worldwide. Additionally, increased awareness of infection risks linked to contaminated or improperly disinfected endoscopes has led healthcare facilities to implement stricter reprocessing protocols, further increasing the demand for advanced reprocessing solutions.

Furthermore, regulatory pressures and updated guidelines from global health authorities such as the FDA, CDC, and SGNA are encouraging safer and more standardized reprocessing practices. The rising adoption of automated reprocessing systems, higher investments in healthcare infrastructure, and the worldwide effort to improve patient safety are also fueling market growth. However, challenges like high capital costs and the complexity of reprocessing workflows may limit market expansion, especially in resource-limited regions.

The flexible endoscopes segment accounted for the largest market share in the endoscope reprocessing market in 2024.

The endoscope reprocessing market, by type of endoscope, is divided into flexible endoscopes and rigid endoscopes. In 2024, the flexible endoscopes segment led the market due to their widespread use in diagnostic and therapeutic procedures across gastroenterology, pulmonology, and urology. These scopes are favored because of their ability to access difficult-to-reach anatomical areas and provide greater patient comfort. The rising number of routine and advanced procedures, such as colonoscopies and bronchoscopies, which mainly use flexible scopes, has further increased the demand for effective reprocessing solutions to ensure safety and prevent cross-contamination. Additionally, regulatory focus on strict cleaning standards for complex devices like duodenoscopes is strengthening the adoption of reprocessing systems designed for flexible endoscopes.

The hospitals & ambulatory surgery centers segment commanded the largest market share in 2024 and is expected to witness the highest CAGR from 2025 to 2030.

By end user, the endoscope reprocessing market is segmented into hospitals & ambulatory surgery centers, specialty clinics, and other end users. The hospitals and ambulatory surgery centers segment holds the largest share of the endoscope reprocessing market in 2024 and is expected to grow faster during the forecast period, driven by the high volume of endoscopy procedures in these settings. Its growth is supported by factors such as the availability of advanced infrastructure, increased funding for infection prevention, and the adoption of automated reprocessing equipment to meet regulatory and accreditation standards. Furthermore, as hospitals seek to reduce healthcare-associated infections (HAIs) and comply with updated reprocessing protocols, the need for compliant and efficient systems is rapidly increasing. ASCs, offering cost savings and shorter patient turnaround times, are also experiencing a rise in endoscopic procedures, boosting the demand for high-throughput reprocessing solutions.

Europe accounted for the second-largest share of the endoscope reprocessing market by region in 2024.

The global endoscope reprocessing market is divided into five main regions: North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2024, Europe's endoscope reprocessing market is the second-largest regional market. This strong position is supported by robust healthcare infrastructure, regulatory enforcement on infection control, and the increasing burden of chronic diseases that require frequent endoscopic procedures and examinations. Among the European countries, Germany has the largest share, driven by its growing elderly population and increasing surgical procedures. According to the United Nations Population Division, Germany's population aged 65 and older is expected to increase by 41%, reaching roughly 24 million by 2050, which will be about 30% of the total population. Additionally, the Financial Times reports that by 2050, more than half of Germany's population will be aged 48 and older, with nearly a third exceeding 60 years. This demographic change is leading to a rise in age-related gastrointestinal, orthopedic, and cardiovascular conditions, resulting in greater demand for endoscopic procedures and boosting the need for advanced and reliable endoscope reprocessing systems to ensure infection control and safety standards.

A breakdown of the primary participants referred to for this report is provided below:

By Company Type: Tier 1- 40%, Tier 2- 30%, and Tier 3- 30%

By Designation: C Level- 27%, Director Level- 18% and Others- 55%

By Region: North America- 35%, Europe- 30%, Asia Pacific- 22%, Latin America- 10%, and Middle East & Africa- 3%

Note 1: Companies are classified into tiers based on their total revenue. As of 2024, Tier 1 = >USD 10.00 billion, Tier 2 = USD 1.00 billion to USD 10.00 billion, and Tier 3 = <USD 1.00 billion.

Note 2: C-level primaries include CEOs, CFOs, COOs, and VPs.

Note 3: Other designations include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

The major players operating in the endoscope reprocessing market are STERIS (Ireland), ASP (US), Olympus Corporation (Japan), Ecolab (US), Getinge AB (Sweden), HOYA Corporation (Japan), Conmed Corporation (US), Miele (Germany), Endo-Technik W. Griesat GmbH (UK), Fujifilm Holdings Corporation (Japan), BES Healthcare Ltd (UK), ARC Healthcare Solutions (Canada), and Metrex Research, LLC. (Canada), Borer Chemie AG (Switzerland), Tuttnauer (Netherlands), Medonica Co., Ltd. (South Korea), Shinva Medical Instrument Co., Ltd. (China), Micro-Scientific, LLC (US), Medalkan (Greece), Medical Devices Group Srl (Italy), SBSystem (Italy), Olive Health Care (India), MMM Group (Germany), Amity International (UK), and MIXTA MEDIKAL (Turkey), among others.

Research Coverage

This report examines the endoscope reprocessing market by products, type of endoscope, end user, and region. The report also explores factors such as drivers, restraints, opportunities, and challenges that influence market growth and provides details of the competitive landscape for market leaders. Additionally, it analyzes micro markets based on their individual growth trends. The report forecasts the revenue of market segments across five major regions and the respective countries within those regions.

Reasons to Buy the Report

The report will help both established and smaller firms to understand the market trends, which can then assist them in increasing their market share. Companies purchasing the report may use one or a combination of the strategies listed below to strengthen their market position presence.

This report provides insights on the following points: analysis of key drivers (rising demand for endoscopy to diagnose and treat target diseases, elevated risk of endoscope-associated infections, expanding aging population, increasing emphasis on improving reprocessing guidelines by healthcare authorities, and rising adoption of minimally invasive surgeries), restraints (persistent concerns regarding safety and effectiveness of reprocessed endoscopic devices, potential health hazards associated with exposure to high-level chemical disinfectants, and high operational costs of endoscopic procedures coupled with limited reimbursement frameworks in emerging economies), opportunities (expanding medical devices industry in emerging economies and increased funding and investments for better healthcare infrastructure and endoscopy-related research), and challenges (rising demand for single-use endoscopes, increasing product failures and recalls, lack of adequately trained personnel, limited awareness among healthcare workers regarding standardized and effective reprocessing practices, and increasing FDA recommended measures to reduce infection transmission)

Market Penetration: Comprehensive information on the product portfolios offered by the top players in the endoscope reprocessing market

Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product launches in the endoscope reprocessing market

Market Development: Comprehensive information on lucrative emerging regions

Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the endoscope reprocessing market

Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key primary sources

2.1.2.2 Key objectives of primary research

2.1.2.3 Key data from primary sources

2.1.2.4 Key industry insights

2.1.2.5 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Company revenue estimation approach

2.2.1.1.1 Presentations of companies and primary interviews

2.2.1.1.2 Primary interviews

2.2.1.2 Growth forecast

2.2.1.3 Market segment assessment

2.2.2 TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 MARKET SHARE ANALYSIS

2.5 RESEARCH ASSUMPTIONS

2.5.1 PARAMETRIC ASSUMPTIONS

2.5.2 GROWTH RATE ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

2.6.1 METHODOLOGY-RELATED LIMITATIONS

2.6.2 SCOPE-RELATED LIMITATIONS

2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ENDOSCOPE REPROCESSING MARKET OVERVIEW

4.2 ASIA PACIFIC ENDOSCOPE REPROCESSING MARKET, BY PRODUCT AND COUNTRY

4.3 ENDOSCOPE REPROCESSING MARKET, BY COUNTRY

4.4 ENDOSCOPE REPROCESSING MARKET, REGIONAL MIX, 2025 VS. 2030

4.5 ENDOSCOPE REPROCESSING MARKET: EMERGING ECONOMIES VS. DEVELOPED MARKETS

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising demand for endoscopy to diagnose and treat target diseases

5.2.1.2 Elevated risk of endoscope-associated infections

5.2.1.3 Booming geriatric population

5.2.1.4 Increasing emphasis on improving reprocessing guidelines

5.2.1.5 Growing adoption of minimally invasive surgeries

5.2.2 RESTRAINTS

5.2.2.1 Persistent concerns about safety and effectiveness of reprocessed endoscopic devices

5.2.2.2 Potential health hazards associated with exposure to high-level chemical disinfectants

5.2.2.3 High operational costs and limited reimbursement in developing economies

5.2.3 OPPORTUNITIES

5.2.3.1 Expanding medical devices industry

5.2.3.2 Increased funding and investments for healthcare infrastructure

5.2.4 CHALLENGES

5.2.4.1 Preference for single-use endoscopes

5.2.4.2 Increasing number of product failures and recalls

5.2.4.3 Lack of adequately trained personnel

5.2.4.4 Limited awareness about standardized and effective reprocessing practices

5.2.4.5 Increasing FDA-recommended measures to reduce infection transmission

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 AVERAGE SELLING PRICE TREND, BY KEY PLAYER

5.4.2 AVERAGE SELLING PRICE TREND, BY REGION

5.5 VALUE CHAIN ANALYSIS

5.6 SUPPLY CHAIN ANALYSIS

5.7 ECOSYSTEM ANALYSIS

5.8 INVESTMENT AND FUNDING SCENARIO

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGIES

5.9.1.1 Automated mechanical cleaning and disinfection

5.9.1.2 High-level chemical disinfection

5.9.2 COMPLEMENTARY TECHNOLOGIES

5.9.2.1 Low-temperature sterilization

5.10 PATENT ANALYSIS

5.11 TRADE ANALYSIS

5.11.1 IMPORT DATA FOR HS CODE 841920

5.11.2 EXPORT DATA FOR HS CODE 841920

5.12 KEY CONFERENCES AND EVENTS, 2025-2026

5.13 REGULATORY ANALYSIS

5.13.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.13.2 REGULATORY FRAMEWORK

5.13.2.1 North America

5.13.2.1.1 US

5.13.2.1.2 Canada

5.13.2.2 Europe

5.13.2.2.1 Germany

5.13.2.2.2 Rest of Europe

5.13.2.3 Asia Pacific

5.13.2.3.1 Japan

5.13.2.3.2 Australia

5.13.2.3.3 Rest of Asia Pacific

5.13.2.4 Latin America

5.13.2.5 Middle East & Africa

5.14 PORTER'S FIVE FORCES ANALYSIS

5.14.1 THREAT OF NEW ENTRANTS

5.14.2 THREAT OF SUBSTITUTES

5.14.3 BARGAINING POWER OF BUYERS

5.14.4 BARGAINING POWER OF SUPPLIERS

5.14.5 INTENSITY OF COMPETITIVE RIVALRY

5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2 KEY BUYING CRITERIA

5.16 IMPACT OF AI/GEN AI ON ENDOSCOPE REPROCESSING MARKET

5.16.1 INTRODUCTION

5.16.2 MARKET POTENTIAL OF AI/GEN AI IN ENDOSCOPE REPROCESSING MARKET

5.16.3 AI USE CASES

5.16.4 FUTURE OF AI/GEN AI IN ENDOSCOPE REPROCESSING ECOSYSTEM

5.17 IMPACT OF 2025 US TARIFF REGULATION ON ENDOSCOPE REPROCESSING MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 KEY IMPACT ON COUNTRY/REGION

5.17.4.1 North America

5.17.4.1.1 US

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON END-USE INDUSTRIES

5.17.5.1 Hospitals

5.17.5.2 Ambulatory care centers

6 ENDOSCOPE REPROCESSING MARKET, BY PRODUCT

6.1 INTRODUCTION

6.2 ENDOSCOPE REPROCESSING EQUIPMENT

6.2.1 AUTOMATED ENDOSCOPE REPROCESSORS

6.2.1.1 Automated endoscope reprocessors, by portability