Battery Materials Market by Battery Type (Lead-Acid, Lithium-Ion), Material [Cathode (LFP, LCO, NMC, NCA, LMO), Anode, Electrolyte], Application (Automotive, Electric Vehicles, Portable Devices, Industrial), and Region - Global Forecast to 2030

상품코드:1807081

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 293 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

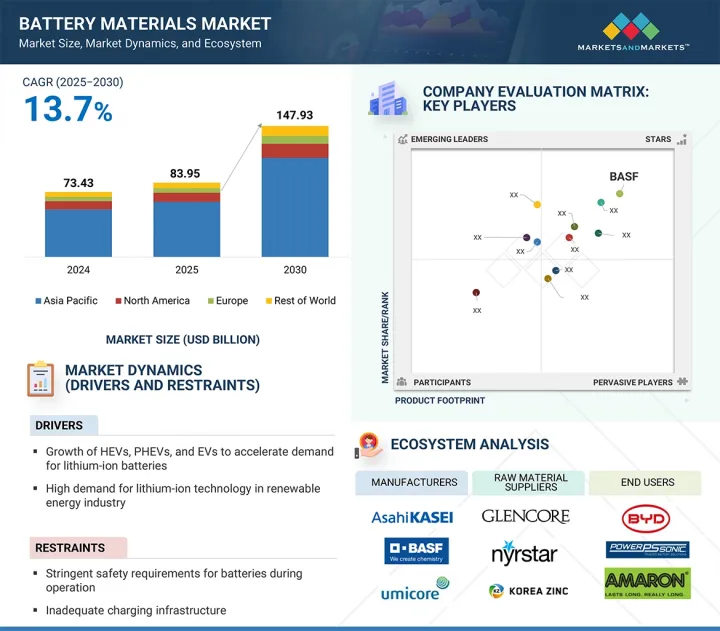

세계의 배터리 재료 시장 규모는 2025년 839억 5,000만 달러에서 2030년까지 1,479억 3,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 13.7%로 성장이 예상됩니다.

시장은 세계적인 전기, 청정 에너지, 디지털 기술로의 전환으로 강력한 성장을 보여줍니다. 전기자동차, 휴대용 전자기기, 에너지 저장 시스템에 대한 수요 증가는 고성능 재료에 대한 요구를 증가시키고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

100만 달러, 킬로톤

부문

재료, 배터리 유형, 용도

대상 지역

북미, 아시아태평양, 유럽 및 기타 지역

정부와 산업계는 배터리 생산 능력, 원재료 조달, 재활용 인프라에 많은 투자를 하고 있습니다.

"배터리 유형별로는 납축배터리 부문이 예측 기간에 금액 기준으로 2위 점유율을 차지할 것으로 추정됩니다."

납축배터리 부문은 자동차, 산업용 백업 전원, 오프 그리드 에너지 저장 용도로 널리 사용되고 있기 때문에 예측 기간에 배터리 재료 시장에서 금액 기준으로 2위의 점유율을 차지할 전망입니다. 신뢰성, 저비용, 확립된 재활용 인프라로 인해 납 축배터리는 개발 도상 지역과 높은 서지 전류가 필요한 용도에서 선호되는 옵션이 되었습니다. 개선된 FLA 및 AGM 기술을 포함한 납 축배터리 설계의 지속적인 발전은 시장 성장을 가속하고 있습니다.

"용도별로는 휴대용 기기 부문이 예측 기간에 금액 기준으로 2위 점유율을 차지할 것으로 보입니다."

스마트폰, 노트북, 태블릿, 웨어러블, 무선 액세서리의 소비자 수요가 증가함에 따라 휴대용 장치 부문은 예측 기간 동안 금액 기준으로 배터리 재료 시장의 두 번째로 큰 점유율을 차지할 전망입니다. 이 부문은 안정적인 배터리 사용을 유지합니다. 소형화, 배터리 수명, 급속 충전 기능의 진보에 의해 고성능으로 컴팩트한 배터리 재료의 요구도 높아지고 있습니다. 디지털 연결성과 모바일 라이프 스타일이 전 세계적으로 확대됨에 따라 휴대용 장치 용도는 배터리 재료 시장에 크게 기여할 것으로 보입니다.

"북미가 예측 기간에 수량 기준으로 2위 점유율을 차지할 것으로 추정됩니다."

북미는 EV 채용 증가, 신재생에너지 수요, 정부 지원으로 예측 기간 동안 배터리 재료 시장에서 수량 기준으로 2위 점유율을 차지할 전망입니다. 미국은 강력한 정책과 발달한 국내 공급망에서 주도하고, 캐나다는 리튬 생산에 투자하고, 멕시코는 비용 우위를 위해 주요 건배터리 제조를 유치하고 있습니다. 이러한 요인은 총체적으로 이 지역의 배터리 재료 수요를 밀어 올리고, 북미는 세계의 배터리 생태계에서 주요 국가로서의 지위를 확립하고 있습니다.

본 보고서에서는 세계의 배터리 재료 시장에 대해 조사 분석했으며, 주요한 촉진요인과 억제요인, 경쟁 구도, 장래의 동향 등의 정보를 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 지견

배터리 재료 시장의 기업에게 매력적인 기회

배터리 재료 시장 : 지역별

배터리 재료 시장 : 배터리 유형별

배터리 재료 시장 : 리튬 이온 배터리 용도별

배터리 재료 시장 : 납축배터리 용도별

배터리 재료 시장 : 주요 국가별

제5장 시장 개요

시장 역학

성장 촉진요인

억제요인

기회

과제

제6장 산업 동향

세계의 거시경제 전망

공급망 분석

원재료

배터리 재료

배터리 제조

유통 네트워크

최종 이용 산업

생태계 분석

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

가격 설정 분석

천연 흑연의 평균 판매 가격 : 지역별(2022-2024년)

배터리 재료의 평균 판매 가격 : 부극 재료별(2024년)

탄산 리튬의 평균 판매 가격 : 주요 기업별

코발트의 평균 판매 가격 : 지역별

니켈의 평균 판매 가격 : 지역별

관세 및 규제 상황

관세 분석

배터리 재료 관련 관세

규제기관, 정부기관, 기타 조직

주요 컨퍼런스 및 이벤트(2025-2026년)

특허 분석

기술 분석

주요 기술

보완 기술

사례 연구 분석

FPORTERA의 TOYOTA 리튬 이온 배터리의 케이스 스터디

REDWOOD MATERIALS의 배터리 금속 회수가 광산의 오염을 경감

개인용 전동 스쿠터용 커스텀 리튬 배터리 솔루션

무역 데이터

수입 시나리오(HS 코드 850650)

수출 시나리오(HS 코드 850650)

고객사업에 영향을 주는 동향/혼란

투자 및 자금조달 시나리오

배터리 재료 시장에 대한 생성형 AI의 영향

소개

데이터 수집 및 구조화

재료 특성 예측 모델링

신재료의 제네레티브 디자인

실험 우선순위 지정 및 검증

재료 제조에서의 공정 최적화

배터리 시스템에 통합

배터리의 라이프사이클과 재활용

지속적인 학습과 피드백 루프

배터리 재료 시장에 대한 트럼프 관세의 영향

시장에 영향을 미치는 주요 관세율

가격의 영향 분석

다양한 지역에 중요한 영향

배터리 재료 시장의 최종 이용 산업에 대한 영향

제7장 배터리 재료 시장 : 재료별

소개

리튬 이온 배터리 재료

양극 재료

음극 재료

전해질 재료

기타 재료

납 축배터리 재료

양극 재료

음극 재료

전해질 재료

기타 재료

기타 배터리 재료

제8장 배터리 재료 시장 : 용도별

소개

리튬 이온 배터리

휴대용 장치

전기자동차

산업

기타 용도

납축배터리

자동차

산업

기타 용도

제9장 배터리 재료 시장 : 배터리 유형별

소개

리튬 이온

납축배터리

기타 배터리 유형

제10장 배터리 재료 시장 : 지역별

소개

아시아태평양

중국

한국

일본

인도

기타 아시아태평양

북미

미국

기타 북미

유럽

독일

프랑스

영국

기타 유럽

기타 지역

브라질

기타 국가

제11장 경쟁 구도

소개

주요 진입기업의 전략/강점

수익 분석

시장 점유율 분석

브랜드 및 제품 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

기업 평가 및 재무 지표

경쟁 시나리오

제12장 기업 프로파일

주요 기업

UMICORE

ASAHI KASEI CORPORATION

MITSUBISHI CHEMICAL GROUP CORPORATION

POSCO FUTURE M

EV METALS GROUP

RESONAC HOLDINGS CORPORATION

KUREHA CORPORATION

SUMITOMO METAL MINING CO., LTD.

TORAY INDUSTRIES, INC.

MITSUI MINING & SMELTING CO., LTD.

UBE CORPORATION

BASF

L&F CO., LTD.

TODA KOGYO CORP.

NEI CORPORATION

TANAKA CHEMICAL CORPORATION

NINGBO SHANSHAN CO., LTD.

HAMMOND GROUP, INC.

SINOMA SCIENCE & TECHNOLOGY CO., LTD.

SHANGHAI ENERGY NEW MATERIALS TECHNOLOGY CO., LTD.

PENOX GROUP

GRAVITA INDIA LTD.

기타 기업

NICHIA CORPORATION

PULEAD TECHNOLOGY INDUSTRY

ENTEK

NEXEON LTD.

ZHANGJIAGANG GUOTAI HUARONG CHEMICAL NEW MATERIAL

ECOPRO BM

ASCEND ELEMENTS, INC.

제13장 인접 시장과 관련 시장

소개

제한 사항

상호연결된 시장

리튬 이온 배터리 시장

시장의 정의

시장 개요

리튬 이온 배터리 시장 : 유형별

리튬 니켈 망간 코발트(NMC)

인산철 리튬(LFP)

코발트산리튬(LCO)

티타네이트리튬(LTO)

망간산 리튬(LMO)

니켈산리튬(NCA)

제14장 부록

JHS

영문 목차

영문목차

The global battery materials market is projected to grow from USD 83.95 billion in 2025 to USD 147.93 billion by 2030, at a CAGR of 13.7% during the forecast period. The battery materials market is experiencing strong growth, driven by the worldwide shift toward electrification, clean energy, and digital technology. Increasing demand for electric vehicles, portable electronics, and energy storage systems is boosting the need for high-performance materials.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million), Volume (Kiloton)

Segments

Material, Battery Type, and Application

Regions covered

North America, Asia Pacific, Europe, and the Rest of World

Governments and industries are making significant investments in battery production capacity, raw material sourcing, and recycling infrastructure.

"Lead-acid segment, by battery type, is estimated to account for the second-largest share during the forecast period in terms of value."

The lead-acid segment is expected to hold the second-largest share in the battery materials market by value during the forecast period, due to its widespread use in automotive, industrial backup power, and off-grid energy storage applications. Its reliability, low cost, and well-established recycling infrastructure make it a preferred choice in developing regions and for applications that require high surge currents. Ongoing advancements in lead-acid battery design, including improved flooded and AGM technologies, are also driving market growth.

"By application, the portable device segment will account for the second-largest share during the forecast period in terms of value."

The portable device segment is expected to hold the second-largest share in the battery materials market by value during the forecast period, driven by rising consumer demand for smartphones, laptops, tablets, wearables, and wireless accessories. This segment sustains steady battery usage. Advances in miniaturization, battery life, and fast-charging features are also increasing the need for high-performance, compact battery materials. As digital connectivity and mobile lifestyles expand worldwide, applications for portable devices are likely to contribute significantly to the battery material market.

"The North America region is estimated to account for the second-largest share during the forecast period in terms of volume."

The North America region is expected to hold the second-largest share in the battery materials market by volume during the forecast period, driven by increasing EV adoption, renewable energy demand, and government support. The US leads with strong policies and a developed domestic supply chain, while Canada invests in lithium production, and Mexico draws major battery manufacturing due to its cost advantages. These factors collectively boost regional demand for battery materials, establishing North America as a key player in the global battery ecosystem.

Profile break-up of primary participants for the report:

By Company Type: Tier 1 - 65%, Tier 2 - 20%, and Tier 3 - 15%

By Designation: Directors- 25%, Managers- 30%, and Others - 45%

By Region: North America - 30%, Asia Pacific - 40%, Europe - 20%, and Rest of the World - 10%

BASF (Germany), POSCO Future M (South Korea), Asahi Kasei Corporation (Japan), Umicore (Belgium), and Sumitomo Metal Mining Co., Ltd. (Japan) are some of the major players in the battery materials market. These players have adopted agreements, joint ventures, expansions, and other strategies to increase their market share and business revenue.

Research Coverage:

The report defines, segments, and projects the size of the battery materials market based on material, battery type, application, and region. It offers detailed information on key factors affecting the market's growth, such as drivers, restraints, opportunities, and challenges. It strategically profiles battery materials manufacturers, thoroughly analyzing their market shares and core competencies, and monitors and assesses competitive developments, including agreements, joint ventures, partnerships, expansion, and others.

Reasons to Buy the Report:

The report aims to assist market leaders and new entrants by providing the most accurate estimates of revenue figures for the battery materials market and its segments. It is also designed to help stakeholders gain a better understanding of the market's competitive landscape, acquire insights to enhance their business positioning, and develop effective go-to-market strategies. Additionally, it enables stakeholders to gauge market trends and offers information on key drivers, restraints, challenges, and opportunities.

The report offers insights on the following points:

Analysis of critical drivers (growth of HEVs, PHEVs, and EVs to accelerate demand for lithium-ion batteries, high demand for lithium-ion technology in renewable energy industry, growth in consumer electronic devices), restraints (stringent safety requirements for batteries during operation, inadequate charging infrastructure), opportunities (use of batteries in energy storage devices, innovation and advances in lithium-ion battery technology, declining lithium-ion battery prices), and challenges (overheating issues of lithium-ion batteries) influencing the growth of the battery materials market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the battery materials market

Market Development: Comprehensive information about lucrative markets - the report analyzes the battery materials market across varied regions

Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the battery materials market

Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players in the battery materials market, such as BASF (Germany), POSCO Future M (South Korea), Asahi Kasei Corporation (Japan), Umicore (Belgium), and Sumitomo Metal Mining Co., Ltd. (Japan)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNIT CONSIDERED

1.4 LIMITATIONS

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 List of primary interview participants-demand and supply sides

2.1.2.3 Key industry insights

2.1.2.4 Breakdown of interviews with experts

2.2 DEMAND-SIDE ANALYSIS

2.3 MARKET SIZE ESTIMATION

2.3.1 BOTTOM-UP APPROACH

2.3.2 TOP-DOWN APPROACH

2.4 SUPPLY-SIDE ANALYSIS

2.4.1 CALCULATIONS FOR SUPPLY-SIDE ANALYSIS

2.5 GROWTH FORECAST

2.6 DATA TRIANGULATION

2.7 FACTOR ANALYSIS

2.8 RESEARCH ASSUMPTIONS

2.9 RESEARCH LIMITATIONS

2.10 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN BATTERY MATERIALS MARKET

4.2 BATTERY MATERIALS MARKET, BY REGION

4.3 BATTERY MATERIALS MARKET, BY BATTERY TYPE

4.4 BATTERY MATERIALS MARKET, BY APPLICATION OF LITHIUM-ION BATTERIES

4.5 BATTERY MATERIALS MARKET, BY APPLICATION OF LEAD-ACID BATTERIES

4.6 BATTERY MATERIALS MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

5.1 MARKET DYNAMICS

5.1.1 DRIVERS

5.1.1.1 Growth of HEVs, PHEVs, and EVs to accelerate demand for lithium- ion batteries

5.1.1.2 High demand for lithium-ion technology in renewable energy industry

5.1.1.3 Growth in consumer electronic devices

5.1.2 RESTRAINTS

5.1.2.1 Stringent safety requirements for batteries during operations

5.1.2.2 Inadequate charging infrastructure

5.1.3 OPPORTUNITIES

5.1.3.1 Use of batteries in energy storage devices

5.1.3.2 Innovation and advances in lithium-ion battery technology

5.1.3.3 Declining lithium-ion battery prices

5.1.4 CHALLENGES

5.1.4.1 Overheating issues of lithium-ion batteries

6 INDUSTRY TRENDS

6.1 GLOBAL MACROECONOMIC OUTLOOK

6.2 SUPPLY CHAIN ANALYSIS

6.2.1 RAW MATERIALS

6.2.2 BATTERY MATERIALS

6.2.3 BATTERY MANUFACTURING

6.2.4 DISTRIBUTION NETWORK

6.2.5 END-USE INDUSTRIES

6.3 ECOSYSTEM ANALYSIS

6.4 PORTER'S FIVE FORCES ANALYSIS

6.4.1 BARGAINING POWER OF SUPPLIERS

6.4.2 BARGAINING POWER OF BUYERS

6.4.3 THREAT OF NEW ENTRANTS

6.4.4 THREAT OF SUBSTITUTES

6.4.5 INTENSITY OF COMPETITIVE RIVALRY

6.5 KEY STAKEHOLDERS AND BUYING CRITERIA

6.5.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.5.2 BUYING CRITERIA

6.6 PRICING ANALYSIS

6.6.1 AVERAGE SELLING PRICE OF NATURAL GRAPHITE, BY REGION, 2022-2024

6.6.2 AVERAGE SELLING PRICE OF BATTERY MATERIALS, BY ANODE MATERIAL, 2024

6.6.3 AVERAGE SELLING PRICE OF LITHIUM CARBONATE, BY KEY PLAYERS

6.6.4 AVERAGE SELLING PRICE OF COBALT, BY REGION

6.6.5 AVERAGE SELLING PRICE OF NICKEL, BY REGION

6.7 TARIFF AND REGULATORY LANDSCAPE

6.7.1 TARIFF ANALYSIS

6.7.2 TARIFF RELATED TO BATTERY MATERIALS

6.7.3 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.8 KEY CONFERENCES AND EVENTS, 2025-2026

6.9 PATENT ANALYSIS

6.9.1 METHODOLOGY

6.10 TECHNOLOGY ANALYSIS

6.10.1 KEY TECHNOLOGIES

6.10.1.1 High-nickel cathodes

6.10.2 COMPLEMENTARY TECHNOLOGIES

6.10.2.1 Lithium metal batteries

6.11 CASE STUDY ANALYSIS

6.11.1 FPORTERA CASE STUDY WITH TOYOTA LITHIUM-ION BATTERIES