자동차 AI 시장 : 제공 제품별, 기술별, 자율주행 수준별, 용도별, 지역별 예측(-2030년)

Automotive AI Market by Offerings (Compute, Memory, Software), Level of Autonomy (L1, L2, L3, L4, L5), Technology (Deep Learning, ML, Computer Vision, Context-aware Computing, NLP), Application (ADAS, Infotainment, Telematics) - Global Forecast to 2030

상품코드:1790685

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 265 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

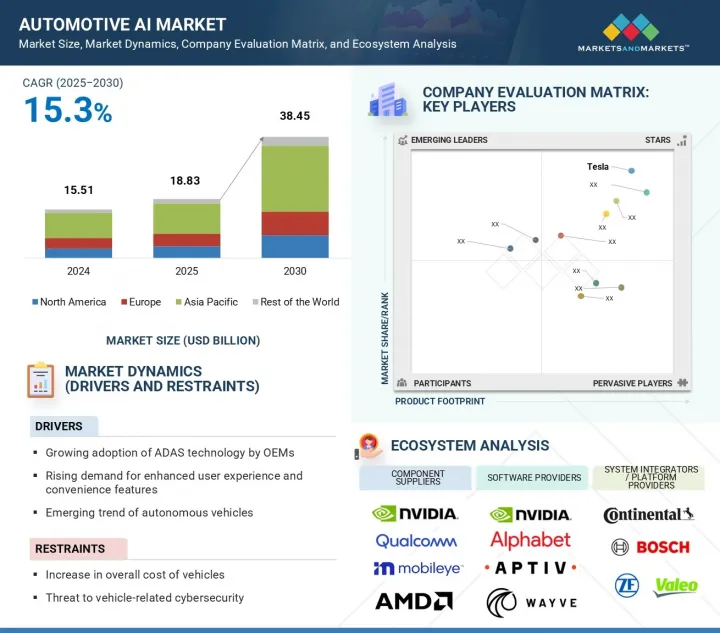

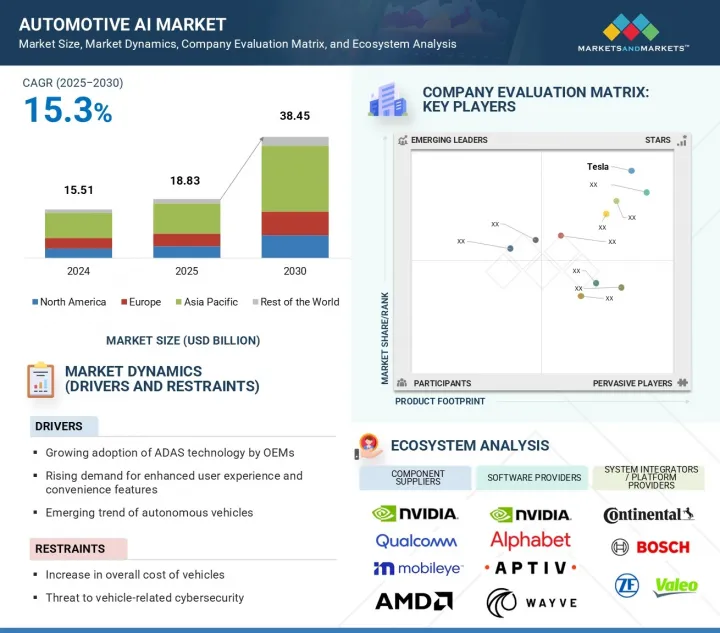

세계의 자동차 AI 시장 규모는 2025년 188억 3,000만 달러에서 2030년까지 384억 5,000만 달러로 확대되었으며, CAGR 15.3%를 보일 것으로 예측됩니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문별

제공 제품별, 기술별, 자율주행 수준별, 용도별, 지역별

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

시장은 지각, 네비게이션, 실시간 의사결정에서 AI에 크게 의존하는 자율주행차의 새로운 동향에 힘쓰고 있습니다. 업계가 보다 정교한 자율성을 향해 나가면서 지능형 시스템에 대한 수요가 증가하고 있습니다. 동시에 센서, 카메라, 커넥티드 시스템에서 생성되는 자동차 데이터의 양이 증가함에 따라 안전성, 효율성 및 개인화를 강화하기 위한 AI 주도 분석 요구가 증가하고 있습니다.

하드웨어 분야는 자율 주행 시스템과 지능형 차량 기능을 강화하는 데 필요한 고급 센서, AI 가속기, 고성능 컴퓨팅 칩의 통합이 진행됨에 따라 자동차 AI 시장에서 높은 성장이 전망되고 있습니다. 자동차가 데이터 집약적인 플랫폼으로 진화함에 따라 카메라, LiDAR, 레이더 및 초음파 센서에서 실시간 데이터를 처리하기 위한 GPU, ASIC, FPGA, 에지 AI 칩과 같은 강력한 하드웨어 인프라에 대한 요구가 커지고 있습니다. 또한 소프트웨어 정의 자동차로의 전환은 자동차 제조업체에게 강력한 도메인 컨트롤러와 중앙 집중식 컴퓨팅 아키텍처를 채택하도록 촉구하고 있습니다.

컴퓨터 비전은 자율주행과 ADAS(첨단 운전 지원 시스템) 모두에 필수적인 실시간 환경인식을 가능하게 하는데 필수적인 역할을 하기 때문에 자동차 AI 시장 전체에서 큰 점유율을 차지하고 있습니다. 이 기술은 카메라와 센서의 시각 데이터를 분석하여 차선 감지, 보행자 인식, 교통 표지 식별, 장애물 회피 등 중요한 기능을 강화합니다. 자동차가 지능화되고 안전 규제가 세계적으로 강화되고 있는 가운데, OEM과 Tier 1 공급업체는 차량의 인식과 의사 결정 능력을 강화하기 위해 견고한 컴퓨터 비전 시스템에 대한 투자를 선호합니다.

유럽은 견고한 자동차 제조거점, 엄격한 안전·배기 가스 규제, 첨단 운전 지원 및 자율 주행 기술의 조기 도입에 의해 세계의 자동차 AI 시장에서 2위의 점유율을 차지하고 있습니다. 독일, 프랑스, 영국과 같은 국가들은 운전자의 안전성, 에너지 효율성, 차량 내 경험을 향상시키기 위해 차량 플랫폼에 AI를 적극적으로 통합하는 주요 OEM 및 Tier-1 공급업체의 본거지입니다. 이 지역에서는 프리미엄 자동차, 전기자동차, 소프트웨어 정의형 자동차에 주력하고 있으며, AI 주도의 기능에 대한 높은 수요가 탄생하고 있습니다.

본 보고서에서는 세계의 자동차 AI 시장에 대해 조사했으며, 제공 제품별, 기술별, 자율주행 수준별, 용도별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

고객사업에 영향을 주는 동향/혼란

밸류체인 분석

생태계 분석

Porter's Five Forces 분석

특허 분석

규제 상황

무역 분석

가격 분석

기술 분석

사례 연구 분석

2025-2026년의 주된 회의와 이벤트

주요 이해관계자와 구매 기준

2025년 미국 관세가 자동차 AI 시장에 미치는 영향

제6장 자동차 AI 시장의 아키텍처

소개

폰 노이만 아키텍처

뉴로모픽 아키텍처

제7장 자동차 AI 시장(제공 제품별)

소개

하드웨어

소프트웨어

제8장 자동차 AI 시장(기술별)

소개

딥러닝

머신러닝

컴퓨터 비전

컨텍스트 인식 컴퓨팅

자연언어처리

제9장 자동차 AI 시장(자동 운전 수준별)

소개

L1

L2

L3

L4

L5

제10장 자동차용 AI 시장(용도별)

소개

AD 및 ADAS

인포테인먼트 시스템

차량 텔레매틱스

기타

제11장 자동차 AI 시장(지역별)

소개

북미

북미의 거시경제 전망

미국

캐나다

멕시코

유럽

유럽의 거시 경제 전망

독일

프랑스

영국

기타

아시아태평양

아시아태평양의 거시 경제 전망

중국

일본

한국

기타

기타 지역

기타 지역의 거시 경제 전망

남미

중동 및 아프리카

제12장 경쟁 구도

개요

주요 참가 기업의 전략/강점, 2021-2025년

수익 분석, 2021-2024년

시장 점유율 분석, 2024년

기업평가와 재무지표

브랜드/제품 비교

기업평가 매트릭스 : 주요 진입기업, 2024년

기업평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제13장 기업 프로파일

주요 진출기업

TESLA

NVIDIA CORPORATION

MOBILEYE

QUALCOMM TECHNOLOGIES, INC.

ADVANCED MICRO DEVICES, INC.

ALPHABET INC.

APTIV

MICRON TECHNOLOGY, INC.

MICROSOFT

IBM

기타 기업

NAUTO

AURORA OPERATIONS, INC.

WAYVE

NURO, INC.

PONY.AI

HELM.AI

TACTILE MOBILITY

DEEPROUTE.AI

COGNATA

NULLMAX

COMMA_AI

MOTIONAL, INC.

OXA AUTONOMY LIMITED

IMAGRY AUTONOMOUS DRIVING SOFTWARE COMPANY

APPLIED INTUITION, INC.

제14장 부록

JHS

영문 목차

영문목차

The automotive AI market is projected to expand from USD 18.83 billion in 2025 to USD 38.45 billion by 2030, registering a CAGR of 15.3%.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Offering, Architecture, Level of Autonomy, Technology, Application, and Region

Regions covered

North America, Europe, APAC, RoW

The market is being propelled by the emerging trend of autonomous vehicles, which rely heavily on AI for perception, navigation, and real-time decision-making. As the industry moves toward higher levels of autonomy, the demand for intelligent systems continues to rise. Simultaneously, the growing volume of in-vehicle data generated from sensors, cameras, and connected systems is fueling the need for AI-driven analytics to enhance safety, efficiency, and personalization.

"Hardware segment projected to record highest CAGR during forecast period"

The hardware segment is expected to grow at a high rate in the automotive AI market due to the increasing integration of advanced sensors, AI accelerators, and high-performance computing chips required to power autonomous driving systems and intelligent vehicle features. As vehicles evolve into data-intensive platforms, there is a rising need for robust hardware infrastructure, such as GPUs, ASICs, FPGAs, and edge AI chips, to process real-time data from cameras, LiDAR, radar, and ultrasonic sensors. Moreover, the transition toward software-defined vehicles is pushing automakers to adopt powerful domain controllers and centralized computing architectures.

"Computer vision technology to hold significant market share in 2025"

Computer vision holds a significant share in the overall automotive AI market due to its indispensable role in enabling real-time environmental perception, which is critical for both autonomous driving and advanced driver assistance systems (ADAS). The technology powers essential functionalities such as lane detection, pedestrian recognition, traffic sign identification, and obstacle avoidance by analyzing visual data from cameras and sensors. As vehicles become more intelligent and safety regulations tighten globally, OEMs and Tier 1 suppliers are prioritizing investments in robust computer vision systems to enhance vehicle awareness and decision-making capabilities.

"Europe to be second-largest market for automotive AI in 2025"

Europe accounts for the second-largest share of the global automotive AI market owing to its strong automotive manufacturing base, stringent safety and emissions regulations, and early adoption of advanced driver assistance and autonomous driving technologies. Countries like Germany, France, and the UK are home to leading OEMs and Tier-1 suppliers that are aggressively integrating AI into vehicle platforms to enhance driver safety, energy efficiency, and in-cabin experience. The region's focus on premium, electric, and software-defined vehicles is creating a high demand for AI-driven functionalities.

Extensive primary interviews were conducted with key industry experts in the automotive AI market space to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

By Company Type: Tier 1-50%, Tier 2-30%, and Tier 3-20%

By Designation: C-level Executives-40%, Directors-30%, and Others-30%

By Region: Asia Pacific-40%, Europe-30%, North America-20%, and RoW-10%

The automotive AI market is dominated by a few globally established players, such as Tesla (US), NVIDIA Corporation (US), Mobileye (Israel), Qualcomm Technologies, Inc. (US), Advanced Micro Devices, Inc. (US), Alphabet Inc. (US), Aptiv (Switzerland), Micron Technology, Inc. (US), Microsoft (US), IBM (US), Nauto (US), Aurora Operations, Inc. (US), Wayve (UK), Nuro, Inc. (US), Pony.ai (China), HELM.AI (US), Tactile Mobility (Israel), DeepRoute.ai (China), Cognata (Israel), Nullmax (US), comma ai (US), Motional, Inc. (US), Oxa Autonomy Limited (UK), Imagry Autonomous Driving Software Company (US), and Applied Intuition, Inc. (US).

The study includes an in-depth competitive analysis of these key players in the automotive AI market, with their company profiles, recent developments, and key market strategies.

Research Coverage:

The report segments the automotive AI market based on offering (hardware, software), architecture (von neumann architecture, neuromorphic architecture), level of autonomy (L1, L2, L3, L4, L5), technology (deep learning, machine learning, computer vision, context-aware computing, natural language processing), and application (autonomous driving (AD)/advanced driver assistance systems (ADAS), infotainment systems, vehicle telematics, others). It also discusses the market's drivers, restraints, opportunities, and challenges. It gives a detailed view of the market across four main regions (North America, Europe, Asia Pacific, and RoW). The report includes an ecosystem analysis of key players.

Key Benefits of Buying the Report:

Analysis of key drivers (Growing adoption of ADAS technology by OEMS, Rising demand for enhanced user experience and convenience features, Emerging trend of autonomous vehicles, growing volume of in-vehicle data), restraints (Increase in overall cost of vehicles, Threat to vehicle-related cybersecurity, Inability to identify human signals), opportunities (Increasing demand for premium vehicles, Growing need for sensor fusion, High potential of in-car payments), challenges (Limited real-world testing and validation frameworks, AI model explainability and trust issues)

Service Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the automotive AI market

Market Development: Comprehensive information about lucrative markets through the analysis of the automotive AI market across varied regions

Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the automotive AI market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, such as Tesla (US), NVIDIA Corporation (US), Mobileye (Israel), Qualcomm Technologies, Inc. (US), Advanced Micro Devices, Inc. (US), Alphabet Inc. (US), Aptiv (Switzerland), Micron Technology, Inc. (US), Microsoft (US), IBM (US), Nauto (US), Aurora Operations, Inc. (US), Wayve (UK), Nuro, Inc. (US), and Pony.ai (China), among others

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of major secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 List of primary interview participants

2.1.2.2 Breakdown of primaries

2.1.2.3 Key data from primary sources

2.1.2.4 Key industry insights

2.1.3 SECONDARY AND PRIMARY RESEARCH

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to estimate market size using top-down analysis (supply side)

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RISK ASSESSMENT

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE AI MARKET

4.2 AUTOMOTIVE AI MARKET, BY OFFERING AND LEVEL OF AUTONOMY

4.3 AUTOMOTIVE AI MARKET, BY TECHNOLOGY

4.4 AUTOMOTIVE AI MARKET, BY APPLICATION

4.5 AUTOMOTIVE AI MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Growing adoption of ADAS technology by OEMs

5.2.1.2 Rising demand for enhanced user experience and convenience features

5.2.1.3 Emerging trend of autonomous vehicles

5.2.1.4 Growing volume of in-vehicle data

5.2.2 RESTRAINTS

5.2.2.1 Increase in overall cost of vehicles

5.2.2.2 Threat to vehicle-related cybersecurity

5.2.2.3 Inability to identify human signals

5.2.3 OPPORTUNITIES

5.2.3.1 Increasing demand for premium vehicles

5.2.3.2 Growing need for sensor fusion

5.2.3.3 High potential of in-car payments

5.2.4 CHALLENGES

5.2.4.1 Limited real-world testing and validation frameworks

5.2.4.2 AI model explainability and trust issues

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 VALUE CHAIN ANALYSIS

5.5 ECOSYSTEM ANALYSIS

5.6 PORTER'S FIVE FORCES ANALYSIS

5.6.1 INTENSITY OF COMPETITIVE RIVALRY

5.6.2 BARGAINING POWER OF SUPPLIERS

5.6.3 BARGAINING POWER OF BUYERS

5.6.4 THREAT OF SUBSTITUTES

5.6.5 THREAT OF NEW ENTRANTS

5.7 PATENT ANALYSIS

5.8 REGULATORY LANDSCAPE

5.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.8.2 STANDARDS

5.8.3 REGULATIONS

5.8.3.1 North America

5.8.3.1.1 US

5.8.3.1.2 Canada

5.8.3.2 Europe

5.8.3.2.1 Germany

5.8.3.2.2 UK

5.8.3.2.3 France

5.8.3.3 Asia Pacific

5.8.3.3.1 China

5.8.3.3.2 South Korea

5.8.3.4 RoW

5.8.3.4.1 United Arab Emirates (UAE)

5.8.3.4.2 Brazil

5.9 TRADE ANALYSIS

5.9.1 IMPORT SCENARIO (HS CODE 8471)

5.9.2 EXPORT SCENARIO (HS CODE 8471)

5.10 PRICING ANALYSIS

5.10.1 INDICATIVE PRICING ANALYSIS OF KEY PLAYERS, BY COMPUTE, (2024)

5.10.1.1 Indicative pricing analysis of GPU-dominant SOCs, by key players (2024)

5.10.1.2 Indicative pricing analysis of ASIC-dominant SOCs, by key players (2024)

5.10.1.3 Indicative pricing analysis of FPGA-dominant SOCs, by key players (2024)

5.10.2 PRICING RANGE OF COMPUTE, BY KEY PLAYERS, 2024

5.10.3 AVERAGE SELING PRICE TREND, BY REGION, 2021-2024 (USD)

5.11 TECHNOLOGY ANALYSIS

5.11.1 KEY TECHNOLOGIES

5.11.1.1 Edge AI processing

5.11.1.2 Sensor fusion algorithms

5.11.2 COMPLEMENTARY TECHNOLOGIES

5.11.2.1 Vehicle-to-Everything (V2X) communication

5.11.2.2 Cybersecurity for AI models

5.11.3 ADJACENT TECHNOLOGIES

5.11.3.1 Digital twin technology

5.11.3.2 Human-Machine Interface (HMI)

5.12 CASE STUDY ANALYSIS

5.12.1 HONDA MOTOR CO., LTD. - ACCELERATING KNOWLEDGE TRANSFER WITH GENERATIVE AI, SLASHING DOCUMENTATION TIME BY 67%

5.12.2 ECARX - REVOLUTIONIZING IN-VEHICLE EXPERIENCE WITH AMD-POWERED IMMERSIVE DIGITAL COCKPIT PLATFORM

5.12.3 SUBARU CORPORATION - ELEVATING EYESIGHT ADAS WITH AMD VERSAL AI EDGE GEN 2 FOR SMARTER, SAFER DRIVING

5.13 KEY CONFERENCES AND EVENTS, 2025-2026

5.14 KEY STAKEHOLDERS AND BUYING CRITERIA

5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.14.2 BUYING CRITERIA

5.15 IMPACT OF 2025 US TARIFFS ON AUTOMOTIVE AI MARKET

5.15.1 KEY TARIFF RATES

5.15.2 PRICE IMPACT ANALYSIS

5.15.3 KEY IMPACTS ON VARIOUS REGIONS

5.15.3.1 US

5.15.3.2 Europe

5.15.3.3 Asia Pacific

5.15.4 IMPACT ON END-USE INDUSTRIES

6 ARCHITECTURE IN AUTOMOTIVE AI MARKET

6.1 INTRODUCTION

6.2 VON NEUMANN ARCHITECTURE

6.3 NEUROMORPHIC ARCHITECTURE

7 AUTOMOTIVE AI MARKET, BY OFFERING

7.1 INTRODUCTION

7.2 HARDWARE

7.2.1 SHIFT TOWARD SOFTWARE-DEFINED VEHICLES ACCELERATING DEMAND FOR HIGH-PERFORMANCE AI HARDWARE

7.2.2 COMPUTE

7.2.2.1 Rising demand for real-time AI processing to accelerates growth of automotive compute segment

7.2.2.2 GPU-dominant SoC

7.2.2.2.1 Need for centralized computing to fuel adoption of high-performance GPU-dominant SoCs in automotive

7.2.2.3 FPGA-dominant SoC

7.2.2.3.1 Flexible hardware architectures position FPGA-dominant SoCs as key enablers in ADAS and safety systems

7.2.2.4 ASIC-dominant SoC

7.2.2.4.1 Application-specific performance requirements boosting market for custom ASICs

7.2.2.5 NPU-dominant SoC

7.2.2.5.1 OEMs' focus on energy-efficient AI inference boosting adoption of NPU-based compute solutions

7.2.3 MEMORY

7.2.3.1 Rising AI data volume and real-time processing needs to drive demand for high-bandwidth automotive memory

7.2.4 OTHERS

7.3 SOFTWARE

7.3.1 SHIFT TOWARD SOFTWARE DEFINED VEHICLES FUELING DEMAND FOR SCALABLE AUTOMOTIVE AI SOFTWARE PLATFORMS

7.3.2 MIDDLEWARE

7.3.2.1 Shift to centralized and zonal architectures driving demand for intelligent automotive middleware platforms

7.3.3 APPLICATION SOFTWARE

7.3.3.1 Expanding AI use cases across safety and infotainment driving growth

7.3.4 OPERATING SYSTEM

7.3.4.1 OEMs' focus on platform standardization to boost market for virtualization-ready automotive OS solutions

8 AUTOMOTIVE AI MARKET, BY TECHNOLOGY

8.1 INTRODUCTION

8.2 DEEP LEARNING

8.2.1 HIGH-ACCURACY PERCEPTION AND REAL-TIME DECISION MAKING TO DRIVE ADOPTION IN AUTOMOTIVE AI

8.3 MACHINE LEARNING

8.3.1 PREDICTIVE INTELLIGENCE AND SELF-IMPROVING ALGORITHMS FUELING ADOPTION IN VEHICLES

8.4 COMPUTER VISION

8.4.1 RISING NEED FOR CAMERA-BASED INTELLIGENCE AND SCENE UNDERSTANDING DRIVING DEMAND

8.5 CONTEXT-AWARE COMPUTING

8.5.1 NEED FOR ENABLING SMARTER DECISION MAKING THROUGH ENVIRONMENTAL AND BEHAVIORAL INSIGHT TO DRIVE MARKET

8.6 NATURAL LANGUAGE PROCESSING

8.6.1 ADOPTION OF VOICE-DRIVEN CONTROL AND CONVERSATIONAL INTERFACES TO ACCELERATE DEMAND FOR NLP

9 AUTOMOTIVE AI MARKET, BY LEVEL OF AUTONOMY

9.1 INTRODUCTION

9.2 L1

9.2.1 COST-EFFECTIVE AI INTEGRATION AND SENSOR ADVANCEMENTS TO ACCELERATE ADOPTION OF LEVEL 1 SYSTEMS

9.3 L2

9.3.1 CONSUMER DEMAND FOR COMFORT AND HIGHWAY ASSISTANCE TO PROPEL SEGMENTAL GROWTH

9.4 L3

9.4.1 ADVANCEMENTS IN PERCEPTION AI AND DECISION-MAKING ALGORITHMS TO ENABLE TARGETED LEVEL 3 DEPLOYMENTS

9.5 L4

9.5.1 FLEET APPLICATIONS AND CONTROLLED URBAN ZONES TO DRIVE SCALABLE DEPLOYMENT OF LEVEL 4 AUTONOMY

9.6 L5

9.6.1 GROWING VISION FOR MOBILITY WITH ZERO HUMAN INTERVENTION TO DRIVE STRATEGIC DEVELOPMENT OF LEVEL 5 PLATFORMS

10 AUTOMOTIVE AI MARKET, BY APPLICATION

10.1 INTRODUCTION

10.2 AD/ADAS

10.2.1 SIGNIFICANT INVESTMENTS IN SENSOR FUSION ARCHITECTURE, EDGE AI INFERENCE, AND COMPUTE PLATFORMS TO SUPPORT MARKET GROWTH

10.3 INFOTAINMENT SYSTEMS

10.3.1 SHIFT TO SOFTWARE-DEFINED VEHICLES FUELING DEMAND FOR AI-DRIVEN IN-CABIN INTELLIGENCE

10.4 VEHICLE TELEMATICS

10.4.1 AI-DRIVEN TELEMATICS TO TRANSFORM VEHICLE FLEETS THROUGH PREDICTIVE MAINTENANCE AND OPERATIONAL INTELLIGENCE

10.5 OTHER APPLICATIONS

11 AUTOMOTIVE AI MARKET, BY REGION

11.1 INTRODUCTION

11.2 NORTH AMERICA

11.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

11.2.2 US

11.2.2.1 Advanced R&D ecosystems and AI compute infrastructure to boost market growth

11.2.3 CANADA

11.2.3.1 Rising adoption of ADAS and government-led innovation programs to accelerate growth

11.2.4 MEXICO

11.2.4.1 Rising investment in smart vehicle technologies to support market growth

11.3 EUROPE

11.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

11.3.2 GERMANY

11.3.2.1 Demand for premium vehicles and increasing electrification to drive scalable AI adoption

11.3.3 FRANCE

11.3.3.1 Strategic collaborations and domestic AI development to propel automotive AI transformation

11.3.4 UK

11.3.4.1 Government support and urban autonomous vehicles deployment to accelerate market growth

11.3.5 REST OF EUROPE

11.4 ASIA PACIFIC

11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

11.4.2 CHINA

11.4.2.1 Integration of OEMs, tech giants, and AI infrastructure accelerating advancement in autonomous driving

11.4.3 JAPAN

11.4.3.1 Complex urban and aging society needs to boost adoption of autonomous vehicles with AI technologies

11.4.4 SOUTH KOREA

11.4.4.1 Smart mobility pilots and software-defined platforms strengthening country's role in global automotive AI

11.4.5 REST OF ASIA PACIFIC

11.5 ROW

11.5.1 MACROECONOMIC OUTLOOK FOR ROW

11.5.2 SOUTH AMERICA

11.5.2.1 AI-enabled safety, logistics, and energy optimization emerging as key catalysts in automotive AI market

11.5.3 MIDDLE EAST & AFRICA

11.5.3.1 Smart city mega-projects and fleet digitization to accelerate automotive AI adoption

12 COMPETITIVE LANDSCAPE

12.1 OVERVIEW

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

12.3 REVENUE ANALYSIS, 2021-2024

12.4 MARKET SHARE ANALYSIS, 2024

12.5 COMPANY VALUATION AND FINANCIAL METRICS

12.6 BRAND/PRODUCT COMPARISON

12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.7.1 STARS

12.7.2 EMERGING LEADERS

12.7.3 PERVASIVE PLAYERS

12.7.4 PARTICIPANTS

12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.7.5.1 Company footprint

12.7.5.2 Region footprint

12.7.5.3 Offering footprint

12.7.5.4 Technology footprint

12.7.5.5 Application footprint

12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024