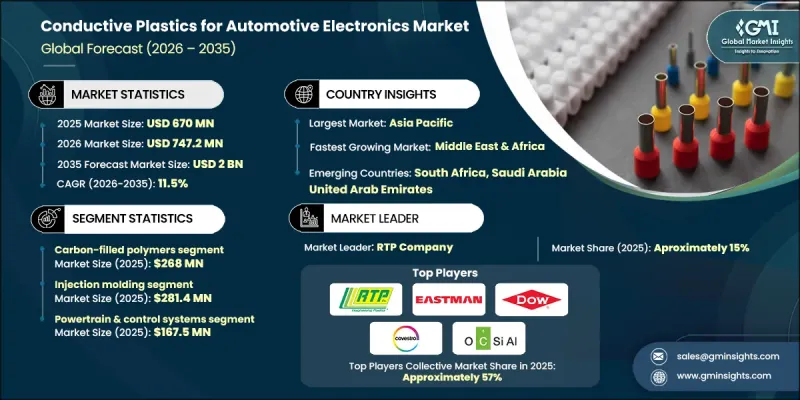

세계의 자동차 일렉트로닉스용 전도성 플라스틱 시장은 2025년에 6억 7,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 11.5%로 성장하여 20억 달러에 이를 것으로 예측됩니다.

이러한 성장은 자동차 산업이 에너지 효율 향상, 차량 중량 감소, 설계 유연성 확대를 위해 경량화 및 고성능 소재에 대한 의존도를 높이고 있기 때문입니다. 전도성 플라스틱은 전자기기 케이스, 커넥터, 구조 부품에서 기존 금속을 대체하는 경우가 증가하고 있으며, 동등한 성능을 대폭 경량화하여 제공합니다. 이러한 전환은 열효율, 컴팩트한 패키징, 복잡한 전자 아키텍처의 원활한 통합과 같은 OEM 제조업체의 우선순위와 일치합니다. 차량 플랫폼의 모듈화 및 전동화가 진행되면서 전도성, 내구성, 제조성을 겸비한 다기능 소재에 대한 수요가 지속적으로 증가하고 있습니다. 첨단운전자보조시스템(ADAS), 커넥티비티 솔루션, 인포테인먼트 시스템, 파워일렉트로닉스 등 차량 내 전자기기가 급증함에 따라 효과적인 전자기 및 고주파 간섭 차폐의 필요성도 증가하고 있습니다. 전도성 플라스틱은 컴팩트한 시스템 설계를 가능하게 하면서도 민감한 부품을 보호하는 데 중요한 역할을 하고 있으며, 현대 자동차 일렉트로닉스 개발에 필수적인 역할을 하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 6억 7,000만 달러 |

| 예측 금액 | 20억 달러 |

| CAGR | 11.5% |

탄소 충전 폴리머 부문은 2025년 2억 6,800만 달러에 달할 것으로 예측됩니다. 이러한 재료는 전기 전도성, 비용 효율성, 저밀도의 균형 잡힌 특성으로 인해 널리 채택되고 있으며, EMI 및 ESD 차폐 응용 분야에 적합합니다. 다른 전도성 플라스틱 유형은 서로 다른 성능 요구 사항을 충족하며, 높은 전도성 재료는 까다로운 전기적 및 열적 조건을 지원하는 반면, 유연한 전도성 폴리머는 내식성 및 조정 가능한 성능 특성이 필요한 특수 응용 분야에서 점점 더 중요해지고 있습니다.

파워트레인 및 제어 시스템 분야는 2025년 1억 6,750만 달러로 2026년부터 2035년까지 연평균 12.1%의 성장률을 보일 것으로 예측됩니다. 이러한 시스템 내에서는 열적, 기계적 스트레스 하에서도 안정적인 전기적 성능이 필수적이기 때문에 센서, 제어 장치, 전자 모듈에 전도성 플라스틱의 사용이 증가하고 있습니다. 또한, 안전 관련 전자기기 및 운전지원 시스템에서도 채용이 확대되고 있으며, 안정적인 동작을 위해서는 안정적인 신호 전송과 효과적인 차폐가 중요합니다.

북미 자동차 전장용 전도성 플라스틱 시장은 2025년 1억 2,090만 달러 규모에 달할 것으로 예상되며, 예측 기간 동안 지속적인 성장이 예상됩니다. 이 지역은 첨단 자동차 전장 도입, 성숙한 제조 인프라, 전기자동차 생산에 대한 강력한 투자로 혜택을 받고 있습니다. 미국은 잘 구축된 공급망과 전기적 안전과 차폐 성능을 향상시키는 경량화 및 고성능 소재에 집중하여 지역 수요의 가장 큰 비중을 차지하고 있습니다.

The Global Conductive Plastics for Automotive Electronics Market was valued at USD 670 million in 2025 and is estimated to grow at a CAGR of 11.5% to reach USD 2 billion by 2035.

Growth is driven by the automotive industry's increasing reliance on lightweight, high-performance materials to improve energy efficiency, reduce vehicle mass, and enable greater design flexibility. Conductive plastics are increasingly replacing conventional metals in electronic housings, connectors, and structural components, offering comparable performance with significantly lower weight. This transition aligns with OEM priorities around thermal efficiency, compact packaging, and seamless integration of complex electronic architectures. As vehicle platforms become more modular and electrified, demand for multifunctional materials that combine conductivity, durability, and manufacturability continues to rise. The rapid increase in onboard electronics, including advanced driver assistance, connectivity solutions, infotainment systems, and power electronics, has heightened the need for effective electromagnetic and radio-frequency interference shielding. Conductive plastics play a critical role in protecting sensitive components while enabling compact system designs, making them essential to modern automotive electronics development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $670 Million |

| Forecast Value | $2 Billion |

| CAGR | 11.5% |

The carbon-filled polymers segment reached USD 268 million in 2025. These materials are widely adopted due to their balanced electrical conductivity, cost efficiency, and low density, making them suitable for EMI and ESD shielding applications. Other conductive plastic types address different performance requirements, with higher conductivity materials supporting demanding electrical and thermal conditions, while flexible conductive polymers are gaining relevance in specialized applications that require corrosion resistance and tunable performance characteristics.

The powertrain and control systems segment accounted for USD 167.5 million in 2025 and is expected to grow at a CAGR of 12.1% during 2026-2035. Conductive plastics are increasingly used in sensors, control units, and electronic modules within these systems, where consistent electrical performance under thermal and mechanical stress is essential. Their adoption is also expanding across safety-related electronics and driver assistance systems, where stable signal transmission and effective shielding are critical for reliable operation.

North America Conductive Plastics for Automotive Electronics Market generated USD 120.9 million in 2025 and is expected to experience sustained growth over the forecast period. The region benefits from advanced automotive electronics adoption, mature manufacturing infrastructure, and strong investment in electric vehicle production. The United States represents the largest share of regional demand due to its well-established supply chain and focus on lightweight, high-performance materials that enhance electrical safety and shielding performance.

Key companies active in the Global Conductive Plastics for Automotive Electronics Market include Covestro AG, RTP Company, DOW, Eastman Chemical Company, Nanocyl SA, OCSiAl, Heraeus Materials Technology, SIMONA AG, and Agfa Gevaert NV. Companies in the conductive plastics for automotive electronics market are strengthening their market position through continuous material innovation and close collaboration with automotive OEMs. Manufacturers are investing in advanced polymer formulations that deliver improved conductivity, thermal stability, and weight reduction. Strategic partnerships with electronics and vehicle platform developers help align materials with next-generation design requirements. Firms are also expanding production capabilities and regional footprints to support growing EV and electronics demand. Emphasis on scalable manufacturing, cost optimization, and compliance with automotive standards enables wider adoption.