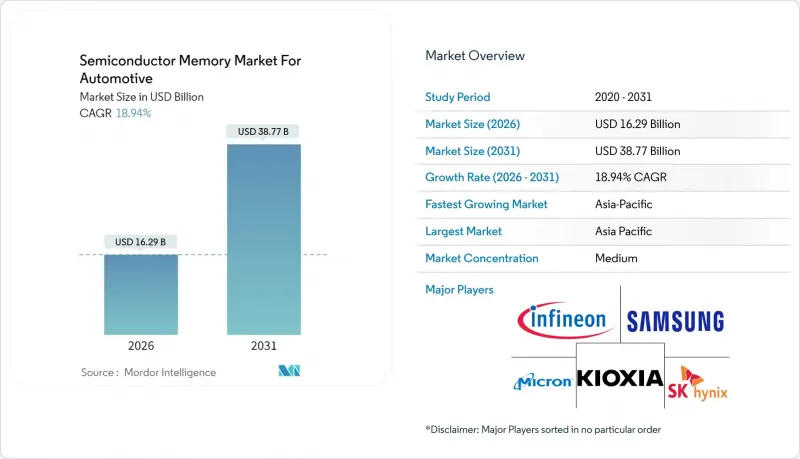

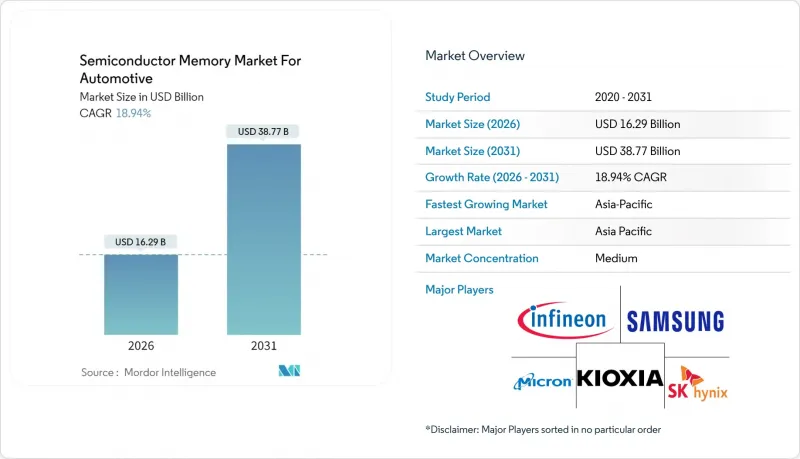

자동차용 반도체 메모리 시장은 2025년 137억 달러에서 2026년에는 162억 9,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 18.94%를 기록하며 2031년에는 387억 7,000만 달러에 달할 것으로 예측됩니다.

이러한 급격한 성장은 수십 개의 전자 기능을 중앙 집중식 컴퓨팅 영역에 통합하는 소프트웨어 정의 차량으로의 전환으로 인해 차량 당 메모리 밀도와 대역폭 요구사항이 크게 증가함에 따라 주도되고 있습니다. 중국, 미국, 유럽연합에서 레벨 2+ 이상의 운전 지원 시스템을 강화하는 규제 움직임은 기능 안전 기준을 충족하는 기가바이트 규모의 작업용 메모리에 대한 수요를 가속화하고 있습니다. 한편, 비용 최적화된 3D NAND와 향후 출시될 MRAM 옵션은 지원 가능한 애플리케이션 기반을 확대하여 자동차 제조업체가 성능과 부품 비용의 균형을 보다 효과적으로 조정할 수 있게 해줍니다. 미국과 유럽에서의 공급망 현지화도 강화하여, 특정 지역에 대한 과도한 의존도를 낮추기 위해 다양한 공급처의 자동차 인증 메모리로 조달 전략을 전환하고 있습니다. 마지막으로, 프리미엄 차량 프로그램에서는 플래시 용량 요구 사항을 높이고 차세대 모듈의 내구성있는 교체주기를 구축하기 위해 무선 소프트웨어 전략을 선구적으로 도입했습니다.

자동차 제조업체들은 지속적인 소프트웨어 업데이트와 기능 배포에 의존하는 자동차를 이동식 데이터센터로 전환하고 있습니다. 테슬라의 하드웨어 4.0은 여러 개의 LPDDR5 스택을 통합하여 메모리 집적도를 획기적으로 향상시켰으며, 12대의 카메라 영상과 레이더 입력을 실시간으로 처리합니다. 중앙집중식 설계를 통해 기존 100개 이상의 ECU 네트워크가 몇 개의 고성능 도메인 컨트롤러로 통합되고, 탑재된 DRAM 용량은 메가바이트 단위에서 멀티기가바이트 규모로 확대되고 있습니다. 고급형에는 이미 총 32GB의 메모리가 탑재되어 있으며, 2027년까지 주류 모델도 비슷한 용량의 메모리를 탑재할 것으로 예상됩니다. 이 업그레이드 경로는 소프트웨어 유지보수 주기가 길어짐에 따라 고 대역폭 AEC-Q100 Grade 1 모듈에 대한 지속적인 수요를 보장합니다.

BMW가 곧 선보일 차세대 iDrive는 각 서브시스템에 개별 모듈을 할당하는 것이 아니라, 존 설계를 통해 메모리 자원을 효율적으로 배분하는 방식을 보여주고 있습니다. 통합을 통해 중복을 제거하고 부품 수를 최대 30%까지 줄일 수 있습니다. 그러나 각 모듈은 더 높은 처리량을 달성하고 더 무거운 열 부하를 견뎌내야 합니다. 그 결과, 특히 인포테인먼트 및 ADAS 분야에서 64비트 폭의 DRAM 인터페이스와 6Gb/s에 육박하는 고속 액세스 속도에 대한 수요 변화가 일어나고 있습니다. 티어1 공급업체들은 메모리와 프로세서를 고밀도 기판에 공동 실장하는 추세로 대응하고 있으며, 이러한 추세는 10nm 공정 이하의 첨단 기술을 보유한 업체들에게 유리하게 작용할 것입니다. 이 아키텍처는 고급 차종에 우선적으로 도입되고 있으며, 4년 이내에 대중 시장 부문으로 확산될 것으로 예상됩니다.

2024년 대만 지진은 지리적으로 집중된 팹(제조 공장)의 취약성을 드러냈고, 컨트롤러 생산에 차질을 빚어 1등급 메모리의 리드타임을 20주 연장시켰습니다. 전체 웨이퍼 수요의 10% 미만을 차지하는 자동차용 라인은 공급 부족이 발생하면 공급업체의 우선순위가 낮아지는 경향이 있습니다. 이에 따라 OEM 업체들은 한국과 미국에서 듀얼 소싱을 진행하고 있으며, 인증 주기 연장으로 인해 이 조치는 적어도 2026년까지 지속될 것으로 보입니다. 수출 규제 차이와 지정학적 불확실성이 단기적으로 성장률을 100-150bp 낮출 수 있습니다.

워킹 메모리는 ADAS(첨단 운전자 보조 시스템)와 인포테인먼트 장치의 높은 실시간 처리량으로 인해 2025년 반도체 메모리 시장의 38.72%를 차지하며 선두를 지켰습니다. 고급 전기자동차(EV)에는 중앙집중형 컴퓨팅 클러스터에 최대 32GB의 LPDDR5가 탑재되는 반면, 양산형 모델에는 2027년까지 16GB가 주류가 될 것으로 예상됩니다. 코드 스토리지는 펌웨어 용량이 8-16GB로 정점을 찍으며 안정세를 보이고 있는 반면, 데이터 스토리지는 엣지 분석을 위해 테라바이트급 센서 데이터를 수집하는 차량이 증가하면서 CAGR 20.02%로 급성장하고 있습니다. 반도체 메모리 시장 규모는 데이터 스토리지와 연동되어 있으며, 대용량 3D NAND 디바이스의 장기적인 수요를 견인하고 있습니다.

작업 메모리의 전망은 안전, 조종석, 파워트레인 도메인 간에 공유되는 메모리 풀을 표준화하는 존 아키텍처의 등장으로 더욱 힘을 얻게 될 것입니다. 이러한 통합은 모듈당 고성능을 요구하며, 와이드 I/O 인터페이스와 내장 ECC 엔진의 채택을 촉진합니다. 듀얼 패스 DRAM-NAND 조합을 제공하는 공급업체들은 인증 프로세스의 효율화를 추구하는 OEM 업체들 사이에서 시장 점유율을 확대할 수 있는 기회를 포착할 준비가 되어 있습니다. 평가 중인 HBM-Lite 컨셉은 열적 문제가 해결되면 2028년 이후에 등장할 수 있으며, 반도체 메모리 시장 내에서 새로운 수익원을 개척할 수 있습니다.

DRAM은 2025년 매출의 31.85%를 차지할 것으로 예상되며, 센서 융합 및 차량 다이나믹스와 같이 지연 시간이 중요한 워크로드에서 선두를 유지하고 있습니다. 한편, 3D NAND는 비트 단가 하락과 AEC-Q100 표준 적용 범위 확대를 배경으로 19.25%의 성장세를 보이고 있습니다. 4,200MB/s의 읽기 속도를 제공하는 자동차 등급 UFS 4.1 드라이브는 데이터 레코더 및 무선 펌웨어 리포지토리의 표준 스토리지 솔루션으로 부상하고 있습니다.

NOR 플래시는 부팅 및 복구 작업을 지속적으로 담당하고 있지만, 용량 제한으로 인해 연간 성장이 억제되고 있습니다. MRAM을 비롯한 신흥 NVM은 페일세이프 레코드, 인스턴트 온 대시보드와 같은 틈새 분야에서 입지를 다지고 있습니다. DRAM은 연산 집약적인 AI 블록을 지원하고, 3D NAND는 지속적 스토리지에 대한 수요 증가를 지원함으로써 반도체 메모리 시장의 핵심에서 상호 보완적인 두 가지 요소를 형성하고 있습니다.

자동차용 반도체 메모리 시장 보고서는 기술 역할(코드 스토리지, 워킹 메모리 등), 메모리 유형(DRAM, NAND 플래시 등), 애플리케이션(ADAS 및 자율주행, 디지털 콕핏 등), 차종(승용차, 소형 상용차 등), 지역(아메리카, 유럽 등)별로 세분화되어 있습니다. 유럽 등) 별로 세분화되어 있습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

아시아태평양은 2025년 반도체 메모리 시장 점유율 37.95%로 1위를 차지할 것으로 예상되며, 중국의 적극적인 EV 보급 목표와 한국의 제조 기반 강점을 바탕으로 19.88%의 CAGR로 선두를 확대할 것으로 전망됩니다. 중국만 하더라도 지역 전체 생산량에서 큰 비중을 차지하고 있지만, 선진국에 대한 수출 규제 조치로 인해 지속적인 역풍을 맞고 있습니다. 한국은 수직계열화 된 주요 기업인 삼성과 SK하이닉스를 활용하여 세계 1등 기업과의 장기 계약을 확보하고 있습니다. 한편, 일본에서는 메모리 제조 공장과 자동차 부품 공급업체의 긴밀한 협력으로 제품 인증의 리드 타임이 단축되고 있습니다.

북미는 2위를 차지했으며, 텍사스, 애리조나, 인디애나 주에서 자동차 전용 생산라인을 포함한 반도체 생산의 국내 회귀를 목적으로 한 520억 달러 규모의 CHIPS법 보조금에 힘입어 2위를 차지했습니다. 테슬라의 수직 통합 모델과 디트로이트의 Ultium BEV 플랫폼이 주요 수요처가 되어 1등급 LPDDR5-X 및 고주기 SSD에 대한 국내 수요를 주도하고 있습니다. 캐나다와 멕시코는 각각 배터리 모듈 조립과 비용 효율적인 전자기기 통합을 통해 지역을 보완하고 3국 간 공급망의 탄력성을 촉진하고 있습니다.

유럽은 430억 유로 규모의 유럽칩스법으로 전략적 자율성을 구축하고 있으며, 독일 자동차 및 메모리 제조업체를 중심으로 컨소시엄을 구성하여 공급망 일부를 현지화하고 있습니다. ISO 26262 및 ISO/SAE 21434에 대한 규제 강화로 인해 인증된 메모리 솔루션에 대한 수요가 증가하고 있습니다. 한편, 중동 및 아프리카는 절대적인 물량에서는 뒤쳐져 있지만, 아랍에미리트와 남아프리카공화국의 전기자동차 제조 우대 정책으로 인해 탄력을 받고 있으며, 2020년대 말까지 반도체 메모리 시장의 신흥 프론티어가 될 조짐을 보이고 있습니다.

The semiconductor memory market for automotive is expected to grow from USD 13.7 billion in 2025 to USD 16.29 billion in 2026 and is forecast to reach USD 38.77 billion by 2031 at 18.94% CAGR over 2026-2031.

The surge is fueled by the shift toward software-defined vehicles, which bundle dozens of electronic functions into centralized compute domains, sharply increasing memory density and bandwidth requirements per car. Regulatory momentum behind Level 2+ driver assistance in China, the United States, and the European Union is accelerating demand for gigabyte-scale working memory that can meet functional-safety standards. Meanwhile, cost-optimized 3D NAND and upcoming MRAM options are expanding the addressable base of applications, letting automakers balance performance and bill-of-materials pressures more effectively. Intensifying supply-chain localization in the United States and Europe is also steering procurement strategies toward multi-sourced, automotive-qualified memory, reducing overreliance on any single region. Finally, premium vehicle programs are pioneering over-the-air software strategies that multiply flash capacity requirements and build a durable replacement cycle for next-generation modules.

Automakers are transforming cars into rolling data centers that rely on continuous software updates and feature deployment. Tesla's Hardware 4.0 showcases a significant leap in memory intensity by integrating multiple LPDDR5 stacks, which stream 12 camera feeds and radar inputs in real-time. Centralized designs slash the traditional network of more than 100 ECUs to a handful of high-performance domain controllers, raising installed DRAM from megabyte ranges to multi-gigabyte footprints. Luxury trims are already equipped with 32 GB of total memory, and mainstream models are expected to trend toward similar capacities by 2027. The upgrade path aligns with longer software maintenance cycles, ensuring recurring demand for high-bandwidth, AEC-Q100 Grade 1 modules.

BMW's forthcoming iDrive generation demonstrates how zonal designs allocate memory resources efficiently, rather than assigning discrete modules to each subsystem. Consolidation eliminates duplication, reducing part counts by up to 30%. However, each surviving module must deliver higher throughput and withstand heavier thermal loads. The net effect is a shift in demand toward 64-bit-wide DRAM interfaces and faster access speeds, approaching 6 Gb/s, particularly in the infotainment and ADAS domains. Tier-1 suppliers are adapting by co-packaging memory and processors on high-density substrates, a trend that favors vendors with advanced capabilities at the 10 nm node and below. The architecture is rolling out first in premium nameplates but is expected to penetrate mass-market segments within four years.

The 2024 Taiwan earthquake exposed the fragility of geographically concentrated fabs, disrupting controller output and inflating lead times for Grade-1 memory by 20 weeks. Automotive lines, which account for under 10% of total wafer demand, often drop in supplier priority when shortages occur. OEMs are therefore dual-sourcing between South Korea and the United States, but qualification cycles extend this mitigation effort to at least 2026. Divergent export-control regimes and geopolitical uncertainty could shave 100-150 basis points off near-term growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Working memory dominated the semiconductor memory market, accounting for a 38.72% share in 2025, due to the high real-time processing loads in ADAS and infotainment units. Luxury EVs now integrate up to 32 GB of LPDDR5 for centralized compute clusters, while mass-market models are expected to trend toward 16 GB by 2027. Code storage remains stable as firmware footprints plateau around 8-16 GB, while data storage rockets at a 20.02% CAGR as vehicles harvest terabytes of sensor data for edge analytics. The semiconductor memory market size is tied to data storage, reinforcing long-term demand for high-capacity 3D NAND devices.

The outlook for working memory is further buoyed by the arrival of zonal architectures that standardize memory pools shared across safety, cockpit, and powertrain domains. This consolidation demands higher per-module performance, driving a pivot toward wide-I/O interfaces and built-in ECC engines. Suppliers offering dual-purpose DRAM-NAND combinations are poised to capture incremental market share among OEMs seeking to streamline their qualification pipelines. HBM-Lite concepts under evaluation could emerge after 2028 if thermal hurdles are resolved, potentially opening an adjacent revenue stream within the semiconductor memory market.

DRAM delivered 31.85% of 2025 revenue, maintaining its leading position in latency-critical workloads, such as sensor fusion and vehicle dynamics. Simultaneously, 3D NAND is advancing at a 19.25% growth pace, driven by declining cost-per-bit and broader AEC-Q100 coverage. Automotive-grade UFS 4.1 drives, which offer 4,200 MB/s read speeds, are emerging as the default storage solutions for data recorders and over-the-air firmware repositories.

NOR flash continues to fulfill boot and recovery tasks, but density limitations restrict its annual expansion. MRAM and other emerging NVMs are carving niche footholds in fail-safe logging and instant-on dashboards. The overarching dynamic is clear: DRAM feeds compute-intensive AI blocks, while 3D NAND underpins the escalating appetite for persistent storage, forming a complementary duo at the heart of the semiconductor memory market.

The Semiconductor Memory Market for Automotive Report is Segmented by Technology Role (Code Storage, Working Memory, and More), Memory Type (DRAM, NAND Flash, and More), Application (ADAS and Automated Driving, Digital Cockpit, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific led with 37.95% semiconductor memory market share in 2025 and is expected to broaden its lead at a 19.88% CAGR, buoyed by China's aggressive EV penetration targets and South Korea's manufacturing depth. China alone represents a significant share of regional volume but faces continuing headwinds from export-control measures on advanced nodes. South Korea leverages its vertically integrated champions, Samsung and SK Hynix, to secure long-term contracts with global Tier-1s, while Japan's close collaboration between memory fabs and automotive suppliers compresses qualification lead times.

North America ranks second, backed by USD 52 billion CHIPS Act subsidies aimed at reshoring semiconductor output, including dedicated automotive lines in Texas, Arizona, and Indiana. Tesla's vertically integrated model and Detroit's Ultium BEV platform are major off-takers, pushing domestic demand for Grade-1 LPDDR5-X and high-cycle SSDs. Canada and Mexico complement the region through battery-module assembly and cost-efficient electronics integration, respectively, fostering trilateral supply resiliency.

Europe is carving strategic autonomy via the EUR 43 billion European Chips Act, with consortia forming around German OEMs and memory makers to localize parts of the supply chain. The regulatory emphasis on ISO 26262 and ISO/SAE 21434 has elevated the demand for certified memory solutions. Meanwhile, the Middle East and Africa trail in absolute volume but are gaining traction through EV manufacturing incentives in the United Arab Emirates and South Africa, signaling an emerging frontier for the semiconductor memory market by the end of the decade.