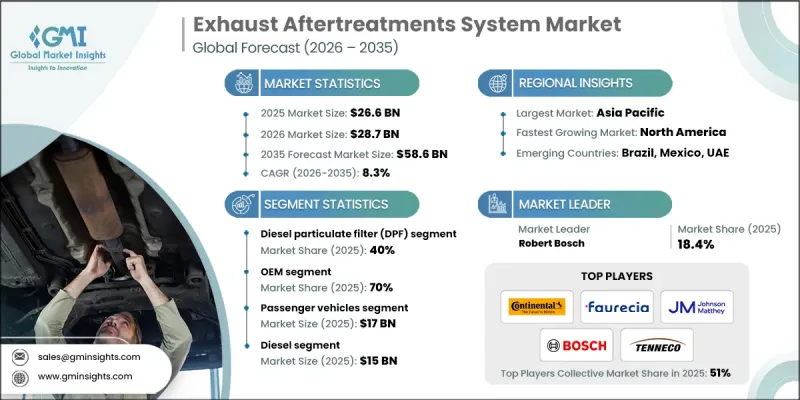

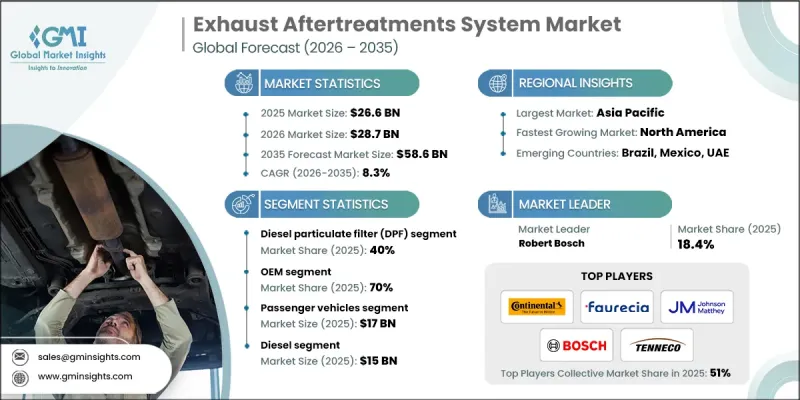

세계의 배기 후처리 시스템 시장은 2025년에 266억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 8.3%로 성장하여 586억 달러에 이를 것으로 예측됩니다.

주요 자동차 시장의 배출가스 규제 강화, 세계 자동차 생산량 증가, 질소산화물, 미립자 물질, 일산화탄소, 미연소 탄화수소 등 유해 배기가스 최소화에 대한 관심 증가가 성장의 배경입니다. 자동차 제조업체와 차량 운영자는 실제 주행 조건에서 규제 목표를 달성하는 동시에 더 깨끗하고 효율적인 차량을 제공해야 한다는 지속적인 압박에 직면해 있습니다. 이에 따라 승용차 및 상용차 부문 모두에서 첨단 배기가스 후처리 솔루션의 통합이 가속화되고 있습니다. 각 제조업체들은 시스템의 내구성, 연비 효율 향상, 배기가스 성능 최적화를 점점 더 우선순위로 삼고 있습니다. 또한, 촉매 조성, 시스템 통합, 센서 기반 제어, 디지털 진단 기술의 지속적인 혁신은 배기가스 모니터링 및 관리 방법을 재정의하고 있습니다. 이러한 발전은 시스템 효율성 향상, 규제 준수 가속화, 장기적인 성능 개선을 가능하게 하며, 진화하는 세계 자동차 산업 생태계에서 배기가스 후처리 기술의 중요성이 더욱 커지고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 266억 달러 |

| 예측 금액 | 586억 달러 |

| CAGR | 8.3% |

제조업체들이 다양한 엔진 플랫폼과 운전 조건에 대응할 수 있는 솔루션을 찾는 가운데, 첨단 배기 후처리 시스템에 대한 수요는 지속적으로 증가하고 있습니다. 디젤 미립자 필터, 선택적 촉매 환원 시스템, 디젤 산화 촉매, 가솔린 미립자 필터, 삼원 촉매 등의 기술은 통합 배출가스 제어 아키텍처의 일부로 점점 더 많이 도입되고 있습니다. 상용차의 디젤 파워트레인 보급 확대와 승용차의 가솔린 직분사 엔진 채택 증가는 고성능 후처리 시스템 도입을 더욱 촉진하고 있습니다. 촉매 효율, 모듈식 시스템 설계, 실시간 배출가스 감지, 차량 진단 시스템의 지속적인 발전은 시스템의 신뢰성과 규제 적합성을 향상시키는 동시에 라이프사이클 비용을 절감하고 있습니다.

디젤 미립자 필터(DPF) 부문은 2025년 40%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 8.1%를 나타낼 것으로 예측됩니다. 이 부문은 디젤 엔진의 미립자 배출을 효과적으로 포집하는 특성으로 인해 중요성이 유지되고 있으며, 여러 차량 카테고리에서 배출가스 규제를 준수하기 위한 핵심 요건입니다. 입증된 성능과 규제적 필요성으로 인해 제조업체와 공급업체들 사이에서 강력한 수요가 계속 증가하고 있습니다.

2025년 기준 OEM 부문은 70%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 복합 성장률(CAGR) 8.6%를 나타낼 것으로 예측됩니다. OEM의 장점은 차량 생산 단계에서 배기가스 후처리 시스템을 통합하여 최적화된 캘리브레이션, 시스템 내구성 및 일관된 배기가스 성능을 보장하는 데 있습니다. OEM 장착 시스템은 더 나은 품질 관리, 엔진 관리 시스템과의 원활한 호환성, 장기적인 규제 적합성 보장을 제공하기 때문에 첨단 배기가스 솔루션의 우선 공급 경로가 되고 있습니다.

중국 배기 후처리 시스템 시장은 2025년 41%의 점유율을 차지하며 42억 달러에 달할 것으로 예측됩니다. 시장을 선도하는 배경에는 대규모 자동차 생산, 첨단 배기가스 제어 기술의 급속한 보급, 자동차 제조업체, 부품 공급업체, 촉매 개발업체 간의 강력한 협력이 있습니다. 정부 지원, 높은 생산량, 확립된 공급망은 국내 현대식 후처리 시스템의 도입을 가속화하고 있습니다.

The Global Exhaust Aftertreatment System Market was valued at USD 26.6 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 58.6 billion by 2035.

Growth is driven by tightening emission requirements across major automotive regions, increasing global vehicle production, and a growing focus on minimizing harmful exhaust emissions, including nitrogen oxides, particulate matter, carbon monoxide, and unburned hydrocarbons. Automakers and fleet operators are under continuous pressure to deliver cleaner and more efficient vehicles while meeting compliance targets under real-world operating conditions. This has accelerated the integration of advanced exhaust aftertreatment solutions across both passenger and commercial vehicle segments. Manufacturers are increasingly prioritizing system durability, fuel efficiency improvement, and emission performance optimization. The market is also benefiting from ongoing innovation in catalyst formulations, system integration, sensor-based control, and digital diagnostics, which are redefining how exhaust emissions are monitored and managed. These developments are enabling higher system efficiency, faster regulatory compliance, and improved long-term performance, reinforcing the importance of exhaust aftertreatment technologies within the evolving global automotive ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26.6 Billion |

| Forecast Value | $58.6 Billion |

| CAGR | 8.3% |

Demand for advanced exhaust aftertreatment systems continues to rise as manufacturers seek solutions capable of addressing diverse engine platforms and operating conditions. Technologies such as diesel particulate filters, selective catalytic reduction systems, diesel oxidation catalysts, gasoline particulate filters, and three-way catalysts are increasingly deployed as part of integrated emission control architectures. The growing use of diesel powertrains in commercial vehicles and gasoline direct injection engines in passenger cars is further supporting the adoption of high-performance aftertreatment systems. Continuous advancements in catalyst efficiency, modular system design, real-time emission sensing, and onboard diagnostics are enhancing system reliability and compliance while reducing lifecycle costs.

The diesel particulate filter segment held a 40% share in 2025 and is expected to grow at a CAGR of 8.1% between 2026 and 2035. This segment remains critical due to its effectiveness in capturing fine particulate emissions from diesel engines, making it a core requirement for emission compliance across multiple vehicle categories. Its proven performance and regulatory necessity continue to drive strong demand among manufacturers and suppliers.

The original equipment manufacturers segment accounted for 70% share in 2025 and is projected to grow at a CAGR of 8.6% through 2035. OEM dominance is supported by the integration of aftertreatment systems during vehicle production, ensuring optimized calibration, system durability, and consistent emission performance. OEM-installed systems offer better quality control, seamless compatibility with engine management systems, and long-term compliance assurance, making this channel the preferred route for advanced emission solutions.

China Exhaust Aftertreatment System Market held a 41% share in 2025 and reached USD 4.2 billion. Market leadership is supported by large-scale vehicle manufacturing, rapid adoption of advanced emission control technologies, and strong collaboration between automakers, component suppliers, and catalyst developers. Government support, high production volumes, and established supply chains continue to accelerate the deployment of modern aftertreatment systems across the country.

Key companies operating in the Global Exhaust Aftertreatment System Market include Robert Bosch, BorgWarner, Tenneco, Johnson Matthey, Continental, Cummins, Faurecia, Eberspacher, MANN+HUMMEL, and HJS Emission Technology. Companies in the exhaust aftertreatment system market are strengthening their market position through continuous investment in technology innovation and system integration. Manufacturers are focusing on developing compact, lightweight, and modular solutions that improve efficiency while reducing overall system costs. Strategic collaborations with automakers help align product development with evolving engine platforms and emission targets. Firms are also expanding global manufacturing footprints to improve supply reliability and reduce lead times. Enhanced digital monitoring, diagnostics, and sensor integration are being used to improve system performance and compliance over vehicle lifecycles. In addition, companies emphasize research into advanced catalyst materials and durability improvements to meet long-term regulatory and customer requirements, reinforcing competitiveness in a highly regulated market environment.