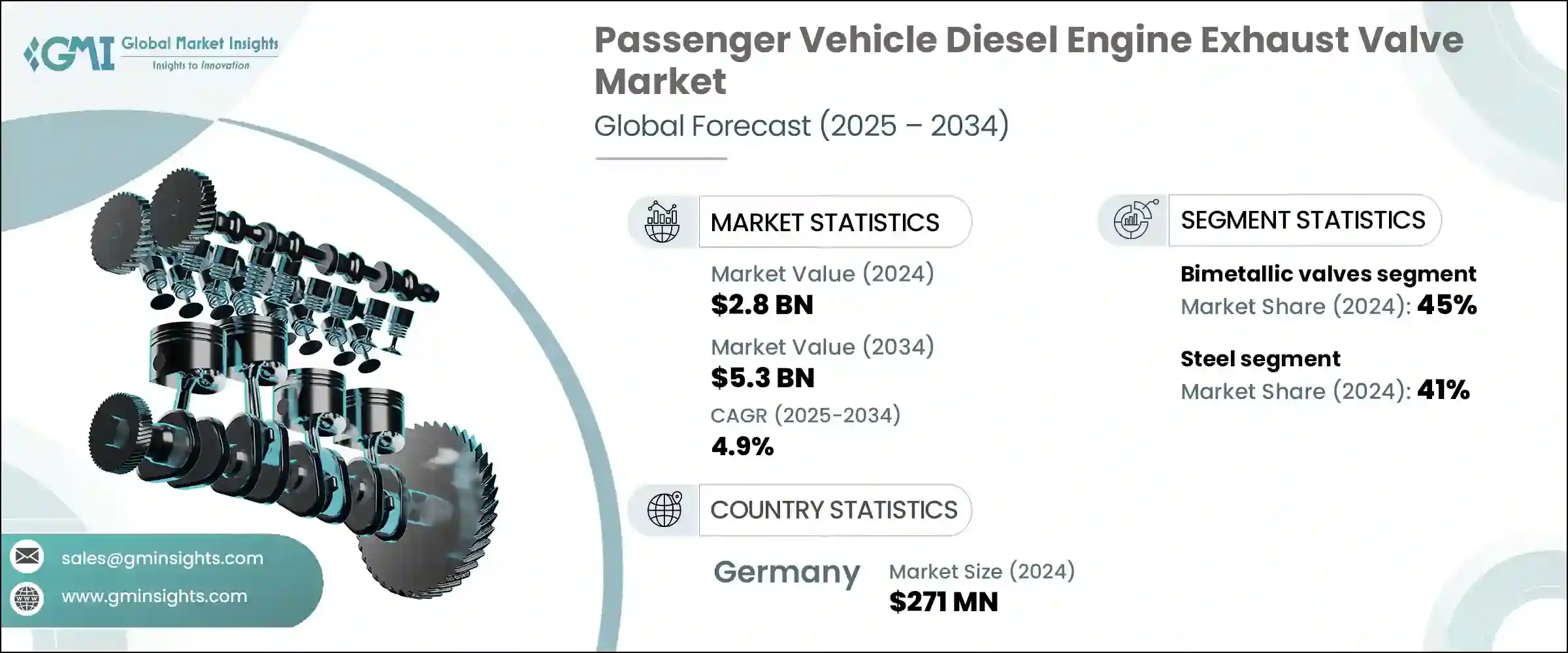

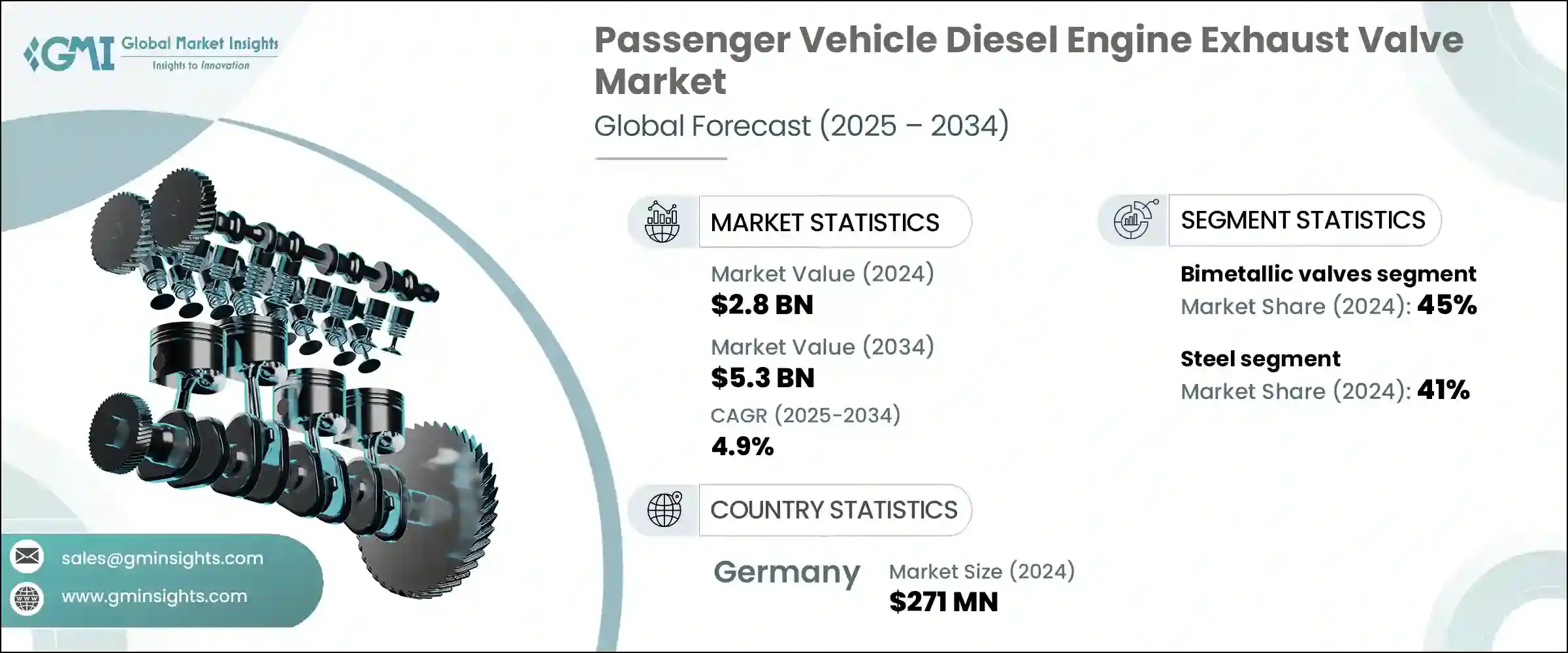

세계의 승용차용 디젤 엔진 배기 밸브 시장 규모는 2024년에 28억 달러에 달하였고, CAGR 4.9%로 성장하여 2034년에는 53억 달러에 이를 것으로 예측되고 있습니다.

이 꾸준한 성장은 특히 디젤 승용차가 오랫동안 사용되어 온 지역에서의 자동차 애프터마켓 서비스의 확대가 큰 요인이 되고 있습니다. 유통 채널의 대두와 지역 내 수리공장의 보급에 의해 교환 부품에 대한 접근성이 한층 더 향상되어, 밸브 제조업체에 있어서는 주문자 상표 부착 생산(OEM) 계약으로부터 독립적인 신뢰성이 높은 수익원이 형성되고 있습니다.

연구개발의 진보는 배기 밸브의 성능 향상에 중요한 역할을 하고 있습니다. 특수한 표면 코팅, 바이메탈 밸브 설계, 내열강 합금의 사용 등의 기술 혁신에 의해 밸브의 내구성이 향상되어 배기가스 규제에 대한 적합성이 개선되어 엔진 전체의 효율이 최적화되었습니다. 따라서 제조업체는 연소 압력 상승과 배출가스 규제 강화 하에서 운행되는 현대 디젤 엔진의 엄격한 조건을 충족하기 위해 밸브의 형상을 미세 조정할 수 있게 되었습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 28억 달러 |

| 예측금액 | 53억 달러 |

| CAGR | 4.9% |

2024년에는 바이메탈 밸브 점유율이 45%로 시장을 독점하였고 2034년까지 연평균 복합 성장률(CAGR) 5%를 보일 것으로 예측됩니다. 바이메탈 밸브의 인기는 강도와 내열성이 매우 뛰어나기 때문에 극단적인 열과 압력 하에서 작동하는 디젤 엔진에 이상적입니다.

스틸 밸브 분야는 2024년에 41%의 점유율을 차지하였으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 4%를 보일 것으로 예측됩니다. 스틸 밸브는 티타늄 및 니켈 합금과 같은 고가의 대체품보다 전통적인 단조 및 가공 공정을 선호하는 기존 제조 인프라로 인해 가장 비용효율적인 선택이 되고 있습니다. 크롬, 몰리브덴, 바나듐 합금의 배합에 의해 내구성, 크리프 저항, 피로 수명이 향상되어 특히 린번 디젤 엔진이나 터보차저 디젤 엔진에 고가의 재료를 대체하는 장점을 제공합니다.

독일의 2024년 승용차용 디젤 엔진 배기 밸브 시장 점유율은 25%였으며, 매출은 2억 7,100만 달러를 달성하였습니다. 독일의 자동차 섹터는 확립된 생산 에코시스템의 혜택을 받고 있으며, 디젤 기술에 대한 지속적인 노력이 배기 밸브의 안정적인 수요를 지지해 독일의 제조업체는 동유럽, 라틴아메리카, 아프리카 등의 수출 시장을 위한 프리미엄 디젤 SUV, 다목적 차량, 세단의 생산량을 늘리는데 주력하고 있습니다. 또한 유로 6d 기준에 맞추어 디젤 엔진 분야에서의 지위를 강화하고 있습니다.

세계의 승용차용 디젤 엔진 배기 밸브 시장에서 경쟁하는 주요 기업은 Mahle, Aisan, Fuji Oozx, Eaton, Rane, Nittan, Dengyun Auto Parts, SSV, Yangzhou Guanghui, Tenneco 등입니다. 이러한 기업은 지속적인 제품 혁신과 전략적 제휴를 통해 시장 역학을 형성하고 있습니다. 각사는 밸브의 내구성과 배출가스 규제에 대한 적합성을 향상시키기 위해 재료와 제조 공정의 혁신을 우선하고 있습니다. 기업들은 또한 현지 서비스 제공업체와 제휴하여 전자상거래 플랫폼을 강화하여 애프터마켓 유통망을 확장하고 세계적으로 교체 부품에 대한 액세스를 용이하게 하는 데 주력하고 있습니다. OEM과의 전략적 제휴는 이러한 제조업체가 장기 공급 계약을 확보할 수 있게 하는 동시에 디젤 자동차가 노후화되는 지역에서 애프터마켓의 성장을 노리고 있습니다.

The Global Passenger Vehicle Diesel Engine Exhaust Valve Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 5.3 billion by 2034. This steady growth is largely fueled by the expansion of automotive aftermarket services, especially in regions where diesel passenger vehicles have been in use for many years. Instead of purchasing new cars, vehicle owners increasingly prefer maintaining and replacing key components like exhaust valves, ensuring ongoing demand in the aftermarket sector. The rise of online distribution channels and the widespread availability of local repair shops has further enhanced access to replacement parts, creating reliable revenue streams for valve manufacturers independent of original equipment manufacturer (OEM) contracts. This trend is particularly significant in markets with stagnant new vehicle sales but rising aftermarket maintenance activities.

Advancements in research and development are playing a critical role in enhancing exhaust valve performance. Innovations such as specialized surface coatings, bimetallic valve designs, and the use of heat-resistant steel alloys have extended valve durability, improved emissions compliance, and optimized overall engine efficiency. The precision afforded by CNC machining and digital inspection technologies has allowed manufacturers to fine-tune valve geometries to meet the demanding conditions of modern diesel engines, which operate under increased combustion pressures and tighter emissions standards. These technological improvements enable OEMs to continue integrating diesel engines into power-dense passenger vehicles while meeting regulatory requirements.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 4.9% |

In 2024, bimetallic valves dominated the market by 45% share and are forecasted to grow at a CAGR of 5% through 2034. Their popularity stems from their exceptional blend of strength and thermal resistance, making them ideal for diesel engines operating under extreme heat and pressure. These valves typically feature a heat-resistant austenitic steel head combined with a martensitic or chrome steel stem, offering superior performance and longevity in demanding engine environments.

The steel valve segment accounted for 41% share in 2024 and is projected to grow at a CAGR of 4% between 2025 and 2034. Steel valves remain the most cost-effective option due to existing manufacturing infrastructure that favors traditional forging and machining processes over more expensive alternatives like titanium or nickel alloys. High-grade steel valves demonstrate remarkable resistance to harsh operating conditions, corrosion, and wear. The inclusion of chromium, molybdenum, and vanadium alloys enhances their durability, creep resistance, and fatigue life, particularly benefiting lean burn and turbocharged diesel engines without the need for costly materials.

Germany Passenger Vehicle Diesel Engine Exhaust Valve Market held a 25% share and generated USD 271 million in 2024. Germany's automotive sector benefits from a well-established production ecosystem and its continued commitment to diesel technology supports steady demand for exhaust valves. German manufacturers are poised to increase the output of premium diesel SUVs, multi-purpose vehicles, and sedans destined for export markets including Eastern Europe, Latin America, and Africa. While much of Europe shifts toward electric mobility, Germany maintains a strong focus on clean diesel compliance, aligning with Euro 6d standards and reinforcing its position in the diesel engine segment.

Key players competing in the Global Passenger Vehicle Diesel Engine Exhaust Valve Market include Mahle, Aisan, Fuji Oozx, Eaton, Rane, Nittan, Dengyun Auto Parts, SSV, Yangzhou Guanghui, and Tenneco. These companies collectively shape market dynamics through continuous product innovation and strategic collaborations. To strengthen their foothold in the passenger vehicle diesel engine exhaust valve market, companies prioritize innovation in materials and manufacturing processes to improve valve durability and emissions compliance. They invest heavily in R&D to develop advanced surface coatings and bimetallic designs that meet increasingly strict regulatory standards. Firms also focus on expanding aftermarket distribution networks by partnering with local service providers and enhancing e-commerce platforms, ensuring easier access to replacement parts worldwide. Strategic alliances with OEMs enable these manufacturers to secure long-term supply contracts while simultaneously targeting aftermarket growth in regions with aging diesel vehicle fleets.