자동차 사이버 보안용 AI 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2026-2035년)

AI in Automotive Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936487

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 255 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

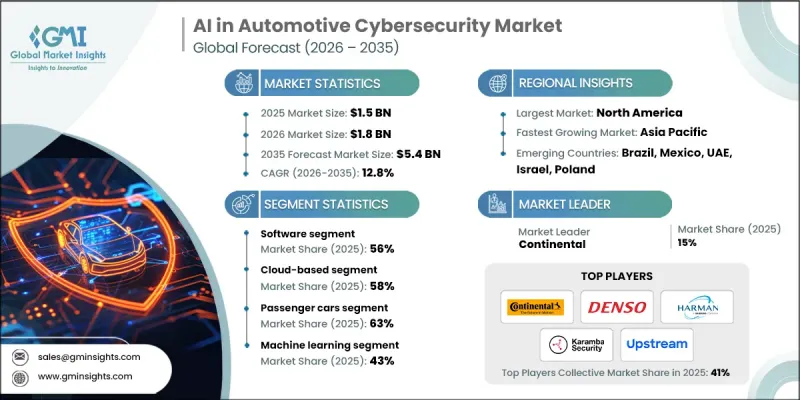

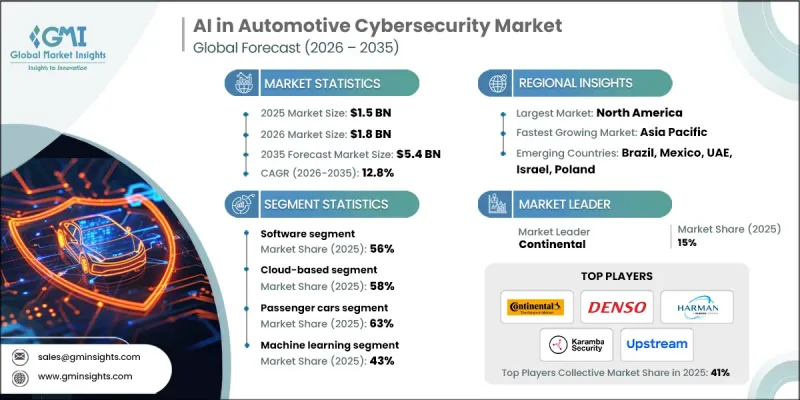

세계의 자동차 사이버 보안용 AI 시장은 2025년에 15억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 12.8%로 성장할 전망이며, 54억 달러에 이를 것으로 예측됩니다.

커넥티드 자동차, 자율 주행 기술, 소프트웨어 중심 차량 플랫폼의 급속한 보급이 시장 성장을 이끌고 있습니다. 현대 차량은 복잡한 소프트웨어 아키텍처에 크게 의존하고 있으며, 전자 제어 장치에는 1억 라인 이상의 코드가 포함되어 있어 시스템이 사이버 위험에 노출될 가능성이 크게 증가하고 있습니다. 차량의 디지털 통합이 진행됨에 따라 사이버 보안은 설계 및 운영상의 중요한 우선 순위로 진화했습니다. 인공지능은 실시간으로 사이버 위협을 모니터링, 분석 및 대응하기 위해 점점 더 많이 도입되어 사후 대응 보호가 아닌 예방적인 방어 메커니즘을 가능하게 합니다. 소프트웨어 정의 차량으로의 전환은 자동차 설계의 근본적인 변화를 의미합니다. 소프트웨어가 핵심 기능, 원격 기능 관리, 지속적인 성능 향상을 통제하기 때문입니다. 기존의 수동 소프트웨어 업데이트에 따른 비용 부담 증가는 OEM 업체들에게 연간 4억 5,000만 달러에서 5억 달러로 추정되고 있으며, 점점 연결성을 높이는 자동차 생태계에서 원격 업데이트, 위협 경감, 시스템 무결성을 지원하는 AI 탑재 사이버 보안 플랫폼의 도입을 가속화하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 금액

15억 달러

예측 금액

54억 달러

CAGR

12.8%

소프트웨어 분야의 우위성은 기계 부품이 아닌 디지털 플랫폼이 중요한 기능을 제어하는 코드 구동 차량 아키텍처로의 업계 전반적인 전환을 반영합니다. 소프트웨어 기반의 사이버 보안 솔루션은 임베디드 펌웨어 보호, 차량 탑재 애플리케이션 방어 및 인가된 코드의 동작을 검증하는 신뢰할 수 있는 실행 환경을 구축하기 위한 것입니다. 이러한 솔루션은 보안 데이터 교환 및 업데이트 배달을 보장하는 암호화 프로토콜 및 인증 프로세스를 관리합니다. 인공지능은 차량 탑재 네트워크의 동작을 지속적으로 분석하고 이상 및 잠재적인 침입을 식별함으로써 이러한 플랫폼을 강화합니다. 여러 시스템에 걸친 코드 라인 수가 1억 라인을 넘는 등 차량의 소프트웨어 컨텐츠가 급속히 확대되고 있기 때문에 시스템의 복잡화에 맞추어 확장 가능한 고급 소프트웨어 중심의 사이버 보안 솔루션에 대한 수요가 계속 증가하고 있습니다.

하드웨어 기반 솔루션 분야는 2025년 27%의 점유율을 차지했으며, 차량 보안의 기반층 역할을 강화하고 있습니다. 이러한 솔루션은 물리적 보안 메커니즘을 차량 전자 장치에 직접 통합하여 중요한 시스템을 변조 및 무단 액세스로부터 보호합니다. 하드웨어 구성 요소는 암호화 자격 증명을 안전하게 저장하고, 암호화 프로세스를 실행하며, 침해된 소프트웨어 실행을 방지하는 신뢰할 수 있는 부트 환경을 설정하도록 설계되었습니다. 추가 하드웨어 보안 요소는 자체 장치 인증을 지원하고 복잡한 암호화 처리를 오프로드하여 차량 전체의 성능을 유지합니다. 이러한 기술이 일체가 되어 AI 구동의 소프트웨어 방어를 보완하는 안전한 물리적 기반을 형성하고 있습니다.

클라우드 기반 전개 부문은 자동차 사이버 보안 전략이 대규모 차량 함대 관리에 중앙 집중식 플랫폼에 대한 의존도를 높이는 동안 2025년에 큰 점유율을 얻었습니다. 클라우드 지원 솔루션은 분산 차량 네트워크 전반에 걸쳐 실시간 위협 인텔리전스, 시스템 전체 분석 및 보안 업데이트의 신속한 전개를 제공합니다. 이 접근법은 중앙 집중식 통신 관리 및 확장 가능한 데이터 처리를 가능하게 함으로써 커넥티드 자동차 서비스와 원격 소프트웨어 전달을 지원합니다. 수백만 대의 차량에서 사이버 보안 데이터를 집계함으로써 물리적 개입 없이 새로운 위협을 파악하고 신속한 대응 조치를 조정하는 첨단 머신러닝 분석이 가능합니다.

미국의 자동차 사이버 보안 시장은 첨단 디지털 기능을 탑재한 고부가가치 차량이 1대당 사이버 보안 투자액을 밀어 올림으로써 2025년에 현저한 점유율을 차지했습니다. 광범위한 교통 인프라가 첨단 차량 연결성을 지원하고 확립된 사이버 보안 에코시스템이 전문 자동차 보호 솔루션을 개발할 수 있도록 합니다. 커넥티드 모빌리티 인프라에 대한 투자가 확대됨에 따라 차량 통신, 디지털 도로 시스템 및 지능형 교통 관리 플랫폼을 보호하는 견고한 사이버 보안 프레임워크의 필요성이 커지고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

커넥티드카, 전기자동차, 자율주행차의 보급 확대

유엔 규칙 R155/R156 ISO/SAE 21434에 대한 필수 준거

자동차를 대상으로 한 사이버 공격의 복잡화 진행

소프트웨어 정의 차량 및 OTA 업데이트의 성장

V2X 및 차재 디지털 서비스의 확대

업계의 잠재적 리스크 및 과제

높은 구현 및 통합 비용

AI 기반 사이버 보안 시스템의 복잡성

숙련된 자동차 사이버 보안 인력 부족

기존 차량 플랫폼의 호환성에 관한 과제

시장 기회

AI를 활용한 예측형 위협 감지 솔루션

실시간, 저지연 보안을 위한 엣지 AI

차량 액세스 및 결제를 위한 생체 인증

서비스로서의 보안(Security-as-a-Service) 및 구독형 모델

레거시 차량용 애프터마켓 사이버 보안

성장 가능성 분석

규제 상황

북미

미국-FMVSS 및 NHTSA 가이드라인

캐나다-자동차 안전규제(MVSR)

유럽

독일-EU 일반 안전규제(GSR)

영국-도로 차량(인가) 규칙

프랑스-EU의 자동 운전차(AV) 및 도로 안전에 관한 틀

이탈리아-국가 도로 안전 계획(PNSS)

아시아태평양

중국-GB/T 규격 및 GB 규격

인도-자동차(개정)법 및 AIS 기준

일본-도로교통법 및 국토교통성 자율 주행 가이드라인

호주-호주 설계 규칙(ADR)

LATAM

멕시코-NOM 자동차 안전 기준

아르헨티나-교통법 24.449호

중동 및 아프리카

남아프리카공화국-국가도로 교통법(1996년)

사우디아라비아-교통 법규 및 비전 2030 교통 이니셔티브

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

자동차 보안에 있어서 AI 및 머신러닝의 진화

위협 감지를 위한 심층 학습 알고리즘

보안 인텔리전스를 위한 자연 언어 처리

신흥 기술

보안 모니터링에 있어서 컴퓨터 비전 용도

컨텍스트 인식 컴퓨팅 및 자동 응답

양자 내성 암호의 개발

특허 분석

AI를 활용한 보안 특허의 동향

주요 특허 보유자 및 기술 리더

신흥 지적 재산 동향 및 출원 패턴

특허 라이선싱 및 협업 모델

가격 분석

솔루션 가격 모델(구독, 영구 라이선스, 차량 단위 과금)

하드웨어 비용 동향

서비스 가격 설정의 동향

총 소유 비용 분석

이용 사례 및 성공 사례

플릿 관리 보안의 이용 사례

자율 주행 차량 보호 시나리오

차재 결제 및 상거래 보안

OTA 업데이트 보안 구현

V2X 통신 보호의 이용 사례

커넥티드 인포테인먼트의 보안 응용

지속가능성 및 환경면

지속가능한 실천

폐기물 감축 전략

생산에 있어서 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

투자 및 자금 조달 분석

벤처 캐피탈 투자 동향

M&A 활동 및 시장 통합

전략적 제휴 및 협업

정부 자금 및 조성금

전망 및 기회

규제의 진화 및 영향

전략적 기회

장래의 위협의 전망

투자 기회

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 컴포넌트별(2022-2035년)

하드웨어

AI 가속기 프로세서

하드웨어 보안 모듈(HSM)

시큐어 게이트웨이 네트워크 장비

스토리지 및 메모리 부품

소프트웨어

AI 탑재 보안 플랫폼

독립형 보안 애플리케이션

통합 소프트웨어 솔루션

서비스

전문 서비스

컨설팅 자문 서비스

도입 및 통합 서비스

서포트 및 보수 서비스

매니지드 시큐리티 서비스

위협 모니터링 및 감지

사고 대응 서비스

보안 운영 센터(SOC) 서비스

제6장 시장 추계 및 예측 : 차량별(2022-2035년)

승용차

해치백

SUV

세단

상용차

소형 상용차(LCV)

중형 상용차(MCV)

대형 상용차(HCV)

전기자동차(EV)

제7장 시장 추계 및 예측 : 기술별(2022-2035년)

머신러닝

자연언어처리(NLP)

컴퓨터 비전

컨텍스트 인식 컴퓨팅

기타

제8장 시장 추계 및 예측 : 전개별(2022-2035년)

온프레미스

클라우드

제9장 시장 추계 및 예측 : 보안별(2022-2035년)

엔드포인트 보안

애플리케이션 보안

무선 네트워크 보안

클라우드 보안

기타

제10장 시장 추계 및 예측 : 용도별(2022-2035년)

ADAS(선진 운전 지원 시스템) 및 안전 시스템

인포테인먼트 시스템

텔레매틱스 시스템

파워트레인 시스템

바디 컨트롤 및 컴포트 시스템

기타

제11장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

네덜란드

스웨덴

덴마크

폴란드

아시아태평양

중국

인도

일본

호주

한국

싱가포르

태국

인도네시아

베트남

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

이스라엘

제12장 기업 프로파일

세계 기업

Aptiv

BlackBerry

Continental

Denso

Harman International Industries

Karamba Security

NVIDIA

Robert Bosch

Siemens

Upstream Security

지역 기업

Cybellum Technologies

ESCRYPT

GuardKnox Cyber Technologies

Infineon Technologies

Intertrust Technologies

NCC

NXP Semiconductors

Renesas Electronics

STMicroelectronics

Trillium Security

Vector Informatik

신흥 기술 혁신자

Aurora Labs

C2A Security

Cymotive Technologies

VicOneg bmhjb

AJY

영문 목차

영문목차

The Global AI in Automotive Cybersecurity Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 12.8% to reach USD 5.4 billion by 2035.

The rapid proliferation of connected vehicles, autonomous driving technologies, and software-centric vehicle platforms drives market growth. Modern vehicles now rely heavily on complex software architectures, with electronic control units containing more than 100 million lines of code, significantly increasing system exposure to cyber risks. As vehicles become more digitally integrated, cybersecurity has evolved into a critical design and operational priority. Artificial intelligence is increasingly deployed to monitor, analyze, and respond to cyber threats in real time, enabling proactive defense mechanisms rather than reactive protection. The transition toward software-defined vehicles represents a fundamental transformation of automotive design, where software governs core functionality, remote feature management, and continuous performance enhancement. The rising cost burden associated with traditional manual software updates, estimated at USD 450 million to USD 500 million annually for original equipment manufacturers, is accelerating the adoption of AI-enabled cybersecurity platforms that support remote updates, threat mitigation, and system integrity in an increasingly connected automotive ecosystem.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$1.5 Billion

Forecast Value

$5.4 Billion

CAGR

12.8%

The dominance of the software segment reflects the industry-wide movement toward code-driven vehicle architectures where digital platforms control critical functions rather than mechanical components. Software-based cybersecurity solutions are designed to secure embedded firmware, protect in-vehicle applications, and establish trusted execution environments that verify authorized code operation. These solutions also manage encryption protocols and authentication processes that ensure secure data exchange and update delivery. Artificial intelligence enhances these platforms by continuously analyzing in-vehicle network behavior to identify anomalies and potential intrusions. The rapid expansion of software content within vehicles, now exceeding 100 million lines of code across multiple systems, continues to drive demand for advanced software-focused cybersecurity solutions that can scale with increasing system complexity.

The hardware-based solutions segment held 27% share in 2025, reinforcing its role as a foundational layer of vehicle security. These solutions integrate physical security mechanisms directly into vehicle electronics to protect critical systems from tampering and unauthorized access. Hardware components are engineered to securely store cryptographic credentials, execute encryption processes, and establish trusted boot environments that prevent compromised software from running. Additional hardware security elements support unique device authentication and offload complex cryptographic operations to preserve overall vehicle performance. Together, these technologies form a secure physical backbone that complements AI-driven software defenses.

The cloud-based deployment segment reached a significant share in 2025 as automotive cybersecurity strategies increasingly rely on centralized platforms to manage large-scale vehicle fleets. Cloud-enabled solutions provide real-time threat intelligence, system-wide analytics, and rapid deployment of security updates across distributed vehicle networks. This approach supports connected vehicle services and remote software delivery by enabling centralized communication management and scalable data processing. Aggregating cybersecurity data from millions of vehicles allows for advanced machine learning analysis that identifies emerging threats and coordinates rapid response actions without requiring physical intervention.

United States AI in Automotive Cybersecurity Market held a notable share in 2025, driven by high-value vehicles equipped with advanced digital features, contributing to elevated per-unit cybersecurity investment. Extensive transportation infrastructure supports advanced vehicle connectivity, while a well-established cybersecurity ecosystem enables the development of specialized automotive protection solutions. Investments in connected mobility infrastructure are increasing the need for robust cybersecurity frameworks to safeguard vehicle communications, digital road systems, and intelligent traffic management platforms.

Key companies operating in the AI in Automotive Cybersecurity Market include NVIDIA, Robert Bosch, Continental, BlackBerry, Harman International, Denso, Upstream Security, Trillium Secure, Karamba Security, and GuardKnox Cyber Technologies. Companies in the AI in Automotive Cybersecurity Market are strengthening their competitive position through continuous innovation, strategic collaborations, and platform expansion. Leading players are investing in AI-driven threat detection, behavioral analytics, and automated response systems to stay ahead of evolving cyber risks. Many firms are forming partnerships with automakers, software vendors, and cloud service providers to integrate security solutions directly into vehicle architectures. Portfolio diversification across software, hardware, and cloud-based offerings is enabling vendors to address varied customer requirements. In parallel, companies are expanding global delivery capabilities and emphasizing regulatory compliance to support international deployments.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.3 Research trail and confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Best estimates and calculations

1.6.1 Base year calculation for any one approach

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Vehicles

2.2.4 Technology

2.2.5 Deployment Mode

2.2.6 Security

2.2.7 Application

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1.1 Growth drivers

3.2.1.2 Rising connected, electric, and autonomous vehicle adoption

3.2.1.3 Mandatory compliance with UN R155/R156 and ISO/SAE 21434