엔드 투 엔드 신경망 자율 주행 시스템 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

End-to-End Neural Network Autonomous Driving System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936479

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

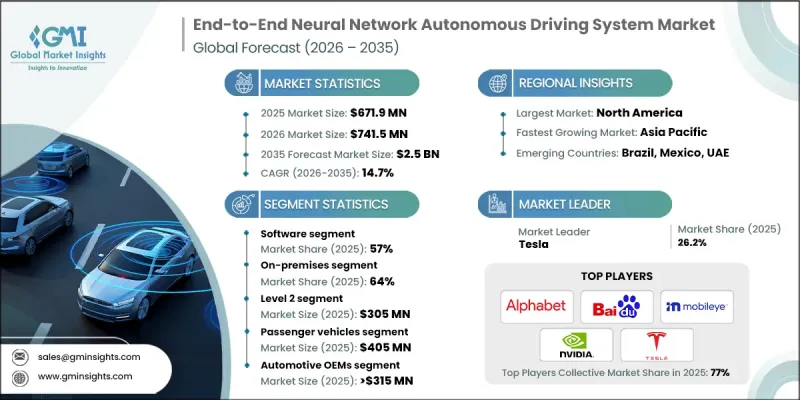

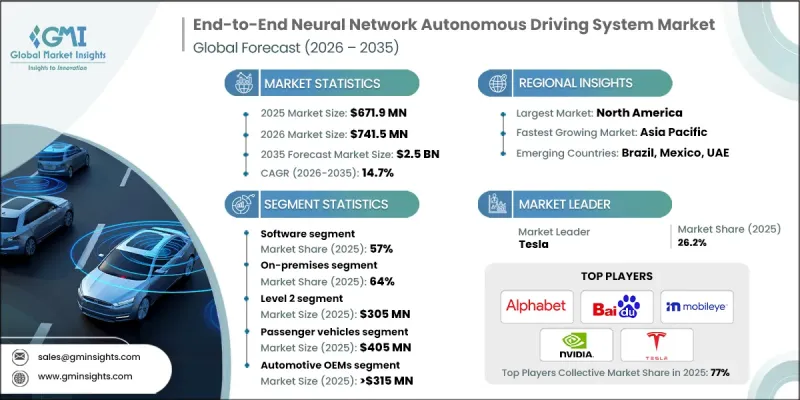

세계의 엔드 투 엔드 신경망 자율 주행 시스템 시장은 2025년에 6억 7,190만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 14.7%로 성장할 전망이며, 25억 달러에 이를 것으로 예측됩니다.

시장 성장은 자율 이동 수단으로의 전환 가속, 도로 안전 및 운영 효율성 중시, 인공지능 구동 차량 지능으로의 자본 유입 증가를 반영합니다. 자동차 제조업체와 이동성 사업자는 실시간 차량 인식, 의사결정 수행, 제어 정확도를 지원하는 엔드 투 엔드 신경망 시스템에 대한 의존도를 높이고 있습니다. 이러한 시스템을 통해 차량은 동적 운전 상황에 즉시 대응하면서 에너지 사용을 최적화하고 인적 개입을 줄일 수 있습니다. 자율 주행의 도입이 세계적으로 확대되고 있는 가운데, 이해관계자들은 안전성, 적응성, 장기적인 비용 효율성을 향상시키는 지능형 소프트웨어 아키텍처를 계속해서 선호하고 있습니다. AI 컴퓨팅, 데이터 교육 능력 및 소프트웨어 정의 차량 플랫폼의 지속적인 발전은 자율 주행 인텔리전스의 설계, 도입 및 업그레이드 방법을 변화시키고 있습니다. 차량 탑재, 클라우드 지원 모델 개발, 원활한 차량 통합을 융합한 에코시스템이 시장에 혜택을 가져오고, 엔드 투 엔드 신경망 솔루션은 완전 자율 주행 운용의 기반 요건으로 자리매김하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 가치

6억 7,190만 달러

예측 금액

25억 달러

CAGR

14.7%

심층 학습 아키텍처의 진보, 실시간 센서 데이터 처리, 통합된 지각에서 제어까지의 파이프라인, 클라우드 지원 모델 최적화는 자율 주행 성능을 재정의합니다. 이러한 기술을 통해 차량은 복잡한 환경을 해석하고 신속한 운전 판단을 수행하며 낮은 지연 및 고정밀도로 작동을 수행할 수 있습니다. 엔드 투 엔드 신경망 시스템은 지각, 계획 및 제어를 단일 학습 프레임워크 내에서 통합하여 시스템의 신뢰성을 높이면서 엔지니어링의 복잡성을 줄입니다. AI 네이티브 플랫폼은 또한 데이터 중심의 트레이닝 사이클을 통한 지속적인 개선을 지원하여 차량이 다양한 도로 상황 및 운영 시나리오에 적응할 수 있도록 합니다. 소프트웨어 정의 차량이 보급되고 있는 동안, 이러한 지능형 시스템은 제조업체가 개발 기간을 단축하고, 차량 효율을 향상시키며, 여러 시장에서 진화하는 안전 요건을 충족하는 데 기여합니다.

소프트웨어 분야는 2025년에 57%의 점유율을 차지하였고, 2026-2035년 CAGR 15.2%를 나타낼 것으로 예측됩니다. 소프트웨어 솔루션은 지각 모델링, 센서 퓨전, 운동 계획 및 차량 제어 로직을 관리하기 위해 자율 주행 성능의 핵심입니다. 고급 신경망은 원시 센서 입력을 실용적인 운전 판단으로 변환하여 정밀하고 안전한 차량 작동을 가능하게 합니다. 자동차 제조업체 및 자율 주행 서비스 제공업체는 AI 프로세서, 센서 하드웨어, 클라우드 기반 교육 환경과 효율적으로 통합되는 종합적인 소프트웨어 플랫폼을 점차 채용하고 있습니다. 지속적인 소프트웨어 업그레이드 및 라디오 배포(OTA) 기능은 이 부문의 이점을 더욱 강화합니다.

온프레미스 도입 모델은 2025년에 64%의 점유율을 차지하였고, 2035년까지 연평균 복합 성장률(CAGR) 13.8%로 성장이 전망되고 있습니다. 이 이점은 업계에서 가장 낮은 지연, 향상된 사이버 보안 및 직접 시스템 모니터링을 제공하는 로컬 컴퓨팅을 선호하는 경향을 반영합니다. 온프레미스 아키텍처를 통해 차량은 외부 연결에 의존하지 않고 신경망 추론과 안전상 중요한 운전 작업을 자율적으로 수행할 수 있습니다. 자율 주행 작업 계산 부하의 높이 및 미션 크리티컬한 특성을 고려하여, 로컬 배치는 다양한 운영 조건에서 컴플라이언스, 신뢰성 및 일관된 성능을 보장합니다.

북미의 엔드 투 엔드 신경망 자율 주행 시스템 시장은 83%의 점유율을 차지했으며, 2025년에는 2억 1,540만 달러의 규모에 이르렀습니다. 이 지역은 자동차 제조업체, 자율 기술 개발자, 이동성 사업자에 의한 적극적인 참여와 AI 탑재 차량 시스템에 대한 지속적인 투자에 힘입어 주도적 지위를 유지하고 있습니다. 차재 신경 처리의 고수준 도입, 지속적인 소프트웨어 갱신, 대규모 자율주행차 도입 계획이 지역 전체 시장 확대를 견인하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

자율주행차의 보급 확대

AI 및 심층 학습의 진전

센서 기술 및 자동차 컴퓨팅에 대한 투자 증가

보다 안전하고 효율적인 이동성에 대한 수요 증가

업계의 잠재적 위험 및 과제

규제 및 안전 우려 사항

높은 개발 및 도입 비용

시장 기회

자율 주행 차량군 및 로보 택시 확대

클라우드 기반 AI 교육 및 OTA 업데이트

AI 컴퓨팅 플랫폼 및 클라우드 기반 모델 교육에 대한 수요 증가

신흥 시장 및 스마트 모빌리티 에코시스템

성장 가능성 분석

규제 상황

북미

미국-NHTSA, DOT 및 AI 안전규제

캐나다-운송성 및 자동차 안전 규제

유럽

독일-BMDV 및 자율주행법

프랑스-운수성 및 AI 모빌리티 틀

영국-운수성(DfT) 및 자율주행차 규제

이탈리아-인프라 및 운수성의 규제

아시아태평양

중국-공업 정보화부(MIIT)

일본-국토교통성 및 자율주행차 가이드라인

한국-국토교통부(MOLIT)

인도-도로 운수 및 고속도로성(MoRTH)

라틴아메리카

브라질-국가교통국(DENATRAN)

멕시코-통신운송성

중동 및 아프리카

아랍에미리트(UAE)-RTA(도로 교통청) 및 국가 AI 전략

사우디아라비아-통신 교통부

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

신흥 기술

가격 동향

지역별

제품별

비용 내역 분석

특허 분석

지속가능성 및 환경면

지속가능한 대처

폐기물 감축 전략

생산에 있어서 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

이용 사례 시나리오

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 컴포넌트별(2022-2035년)

소프트웨어

인식

결정

제어

하드웨어

센서

GPU

AI 칩

서비스

제6장 시장 추계 및 예측 : 자동화 레벨별(2022-2035년)

레벨 2

레벨 3

레벨 4

레벨 5

제7장 시장 추계 및 예측 : 도입 모델별(2022-2035년)

온프레미스

클라우드 기반

제8장 시장 추계 및 예측 : 차량별(2022-2035년)

승용차

해치백 자동차

세단

SUV

상용차

소형 상용차(LCV)

중형 상용차(MCV)

대형 상용차(HCV)

제9장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

자동차 제조업체

플릿 사업자

이동성 서비스 제공업체

기타

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

벨기에

네덜란드

스웨덴

아시아태평양

중국

인도

일본

호주

싱가포르

한국

베트남

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카(MEA)

아랍에미리트(UAE)

남아프리카

사우디아라비아

제11장 기업 프로파일

세계 기업

Alphabet

Aurora Innovation

Baidu

Cruise(GM)

Huawei Technologies

Mobileye

NVIDIA Corporation

Tesla, Inc.

XPeng Motors

Zoox(Amazon)

지역 기업

AutoX

Hyundai Motor Group

Nuro, Inc.

Pony.ai

SAIC Motor Corporation

Tata Elxsi

Wayve Technologies

ZF Friedrichshafen AG

신흥 기업

DeepRoute.ai

Momenta

Oxbotica

PlusAI

WeRide

AJY

영문 목차

영문목차

The Global End-to-End Neural Network Autonomous Driving System Market was valued at USD 671.9 million in 2025 and is estimated to grow at a CAGR of 14.7% to reach USD 2.5 billion by 2035.

Market growth reflects the accelerating shift toward autonomous mobility, the rising emphasis on road safety and operational efficiency, and the growing flow of capital into AI-driven vehicle intelligence. Automakers and mobility operators increasingly rely on end-to-end neural network systems to support real-time vehicle perception, decision execution, and control accuracy. These systems enable vehicles to respond instantly to dynamic driving conditions while optimizing energy usage and reducing human intervention. As autonomous deployments scale globally, industry stakeholders continue to prioritize intelligent software architectures that improve safety, adaptability, and long-term cost efficiency. Continuous progress in AI computing, data training capabilities, and software-defined vehicle platforms is reshaping how autonomous intelligence is designed, deployed, and upgraded. The market benefits from an ecosystem that blends onboard processing, cloud-supported model development, and seamless vehicle integration, positioning end-to-end neural network solutions as a foundational requirement for fully autonomous driving operations.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$671.9 Million

Forecast Value

$2.5 Billion

CAGR

14.7%

Advancements in deep learning architectures, real-time sensor data processing, integrated perception-to-control pipelines, and cloud-assisted model optimization are redefining autonomous driving performance. These technologies allow vehicles to interpret complex environments, make rapid driving decisions, and execute actions with reduced latency and improved precision. End-to-end neural network systems unify perception, planning, and control within a single learning framework, which enhances system reliability while lowering engineering complexity. AI-native platforms also support continuous improvement through data-driven training cycles, enabling vehicles to adapt to diverse road conditions and operational scenarios. As software-defined vehicles gain traction, these intelligent systems help manufacturers reduce development timelines, improve vehicle efficiency, and meet evolving safety requirements across multiple markets.

The software segment held 57% share in 2025 and is projected to register a CAGR of 15.2% from 2026 to 2035. Software solutions remain central to autonomous driving performance because they manage perception modeling, sensor fusion, motion planning, and vehicle control logic. Advanced neural networks transform raw sensor inputs into actionable driving decisions, enabling precise and safe vehicle operation. Automotive manufacturers and autonomous service providers increasingly adopt comprehensive software platforms that integrate efficiently with AI processors, sensor hardware, and cloud-based training environments. Continuous software upgrades and over-the-air deployment capabilities further strengthen the dominance of this segment.

The on-premises deployment model accounted for 64% share in 2025 and is expected to grow at a CAGR of 13.8% through 2035. This dominance reflects the industry's preference for localized computing that delivers ultra-low latency, enhanced cybersecurity, and direct system oversight. On-premises architectures enable vehicles to perform neural network inference and safety-critical driving tasks independently of external connectivity. Given the computational intensity and mission-critical nature of autonomous driving operations, localized deployment ensures compliance, reliability, and consistent performance across varying operating conditions.

North America End-to-End Neural Network Autonomous Driving System Market held 83% share, generating USD 215.4 million in 2025. The country maintains its leadership position due to strong participation from automotive manufacturers, autonomous technology developers, and mobility operators, supported by sustained investment in AI-enabled vehicle systems. High adoption of onboard neural processing, continuous software updates, and large-scale autonomous fleet initiatives continues to drive market expansion across the region.

Prominent companies active in the Global End-to-End Neural Network Autonomous Driving System Market include NVIDIA, Tesla, Baidu, Mobileye, Huawei Technologies, Alphabet, Zoox, Aurora Innovation, XPeng Motors, and Cruise. To strengthen their position, companies in the end-to-end neural network autonomous driving system space focus on accelerating AI model innovation, expanding proprietary data training pipelines, and deepening integration between software and vehicle hardware. Strategic investments in high-performance computing platforms and custom AI chips allow firms to enhance real-time processing efficiency. Many players prioritize scalable software architectures that support rapid deployment across multiple vehicle platforms. Partnerships with automotive manufacturers and mobility operators help accelerate commercialization and global reach. Continuous over-the-air updates enable ongoing system improvement and regulatory compliance.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Level of Automation

2.2.4 Deployment Mode

2.2.5 Vehicle

2.2.6 End Use

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing adoption of autonomous vehicles

3.2.1.2 Advancements in AI & deep learning

3.2.1.3 Increasing investment in sensor technologies & onboard computing

3.2.1.4 Rising demand for safer and more efficient mobility

3.2.2 Industry pitfalls and challenges

3.2.2.1 Regulatory and safety concerns

3.2.2.2 High development and deployment costs

3.2.3 Market opportunities

3.2.3.1 Expansion of autonomous fleets & robotaxis

3.2.3.2 Cloud-based AI training & OTA updates

3.2.3.3 Rising demand for AI compute platforms and cloud-based model training

3.2.3.4 Emerging markets and smart mobility ecosystem

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 U.S.: NHTSA, DOT, and AI Safety Regulations

3.4.1.2 Canada: Transport Canada & Motor Vehicle Safety Regulations

3.4.2 Europe

3.4.2.1 Germany: BMDV & Autonomous Driving Act

3.4.2.2 France: Ministry of Transport & AI Mobility Frameworks

3.4.2.3 UK: Department for Transport (DfT) & AV Regulations

3.4.2.4 Italy: Ministry of Infrastructure & Transport Regulations

3.4.3 Asia Pacific

3.4.3.1 China: Ministry of Industry and Information Technology (MIIT)