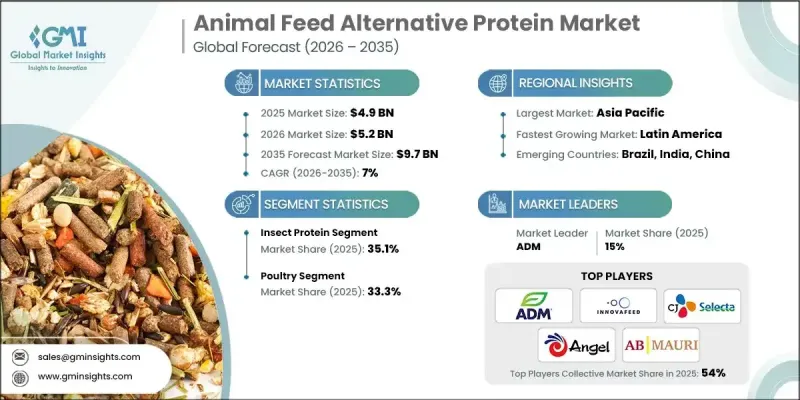

세계의 동물사료 대체 단백질 시장은 2025년에 49억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7%로 성장하여 97억 달러에 이를 것으로 예측됩니다.

시장 성장은 사료 공급망 전반의 단백질 조달 전략을 재구성한 지속가능성에 대한 요구로 인해 주도되고 있습니다. 전통적인 축산업에 따른 배출량 및 토지 이용과 관련된 환경적 압력은 통합 사업자, 제조업체 및 소매업체가 단백질 투입원을 재평가하는 주요 요인으로 인식되고 있습니다. 대체 사료 단백질은 제품별 자원에 의존하고, 헥타르당 단백질 수율이 높으며, 장기적인 공급 회복력을 뒷받침하고, 환경 부하가 적은 솔루션으로 자리매김하고 있습니다. 이 논의는 이 기간 동안 지속가능성 목표, 규제 모멘텀, 혁신이 결합하여 전통적인 사료 단백질로부터의 다각화가 가속화되고 전 세계 여러 동물 생산 시스템에서 더 광범위한 상업적 채택을 위한 기반이 마련되었습니다는 점을 강조합니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 49억 달러 |

| 예측 금액 | 97억 달러 |

| CAGR | 7% |

시장 채택 현황은 식량 안보와 비용 변동성 측면에서 더 설명할 수 있습니다. 공급의 혼란과 지정학적 불확실성으로 인해 2021년부터 2023년까지 사료비 상승으로 인해 생산자들의 리스크 관리 압박이 가중되고 있습니다. 대체 단백질은 주요 축산 분야 전반에 걸쳐 시험이 가능한 안정적인 공급원으로 자리매김하고 있습니다. 곤충 유래 사료, 발효 식물성 단백질, 미생물 유래 원료의 성능 결과는 기존 수입 단백질 사료와 동등한 수준으로 설명되는 동시에 외부 공급망에 대한 의존도를 낮추고 있습니다. 소화 기능, 장 기능, 항생제 의존도 감소에 초점을 맞춘 연구는 대체 사료 단백질이 동물의 건강, 복지 성과, 프리미엄 제품 포지셔닝을 지원할 수 있다는 확신을 강화했습니다.

곤충 단백질 부문은 2025년 35.1%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 6.8%로 성장할 것으로 전망됩니다. 시장 동향에서 단일 단백질 공급원에 대한 의존에서 벗어나 다양한 원료 포트폴리오로 전환하는 뚜렷한 경향을 읽을 수 있습니다. 대형 사료업체들은 곤충 유래 원료를 미생물, 조류, 곰팡이, 효모 유래, 가공된 콩 단백질과 함께 배합하고 있다고 설명합니다. 이 복합적인 접근 방식은 비용 관리, 지속가능성, 영양가 안정성, 아미노산 최적화, 장 건강 및 사료 효율과 관련된 기타 혜택의 균형을 맞추기 위한 포지셔닝입니다.

가금류 부문은 2025년 33.3%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 6.8%의 성장률을 보일 것으로 전망됩니다. 전략적 투자는 고부가가치 사료 배합으로 원료비 상승을 정당화할 수 있는 고수익 축산 분야에 집중하고 있다는 설명입니다. 생산자와 사료 배합사료 제조업체 간의 공동 개발은 대체 단백질을 통합한 균형 잡힌 사료를 만드는 방법으로 주목받고 있습니다. 이를 통해 지속가능성, 기존 해양 단백질에 대한 의존도 감소, 동물 영양 및 반려동물 시장에서의 새로운 사료 원료 도입 등의 주장을 뒷받침할 수 있습니다.

북미 동물사료 대체 단백질 시장은 2024년 11억 9,000만 달러에 달할 것으로 예측됩니다. 이 지역의 성장은 공급 안정성과 친환경을 추구하는 수직 통합형 생산자들에 기인합니다. 가금류 사료, 특수 사료, 반려동물 영양 분야의 강력한 수요가 발효 단백질, 효모 유래 단백질, 단세포 단백질의 채택을 지속적으로 뒷받침하고 있습니다. 미국은 주요 내수 시장으로 선진화된 발효 인프라, 소매업 중심의 지속가능성 노력, 기존 대두박을 부분적으로 대체하는 무항생제 및 프리미엄 포지셔닝의 사료 솔루션에 대한 안정적인 수요에 힘입어 성장하고 있습니다.

경쟁사로는 ADM, 칼리스타, 엔젤 이스트, 이노바 피드, CJ 셀렉타, 햄릿 단백질 A/S, 타이탄 바이오텍, CHS, E.I. 듀폰 드 네무르 앤 컴퍼니, 애그리프로틴, 딥브랜치 바이오테크놀러지, AB 모리, 크레센트 바이오텍, 크레센트 바이오테크 등이 있습니다. 딥브랜치 바이오테크놀러지, AB 모리, 크레센트 바이오테크 등 세계 시장에서 대체 사료 단백질 솔루션 개발 및 상용화를 적극적으로 추진하고 있습니다. 동물사료 대체 단백질 시장에서 사업을 전개하는 기업들은 생산 능력 확대, 기술 투자, 전략적 제휴를 통해 자사의 입지를 강화하고 있다는 설명입니다. 많은 업체들이 비용 경쟁력과 공급 안정성을 높이기 위해 발효 및 곤충 생산 시스템의 규모 확대에 주력하고 있습니다. 기업들이 다양한 영양 요구 사항과 규제 요건을 충족하기 위해 여러 단백질 형태를 통합하면서 포트폴리오의 다양화가 강조되고 있습니다.

The Global Animal Feed Alternative Protein Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 9.7 billion by 2035.

Market growth is driven by sustainability demands that reshaped protein sourcing strategies across feed supply chains. Environmental pressures related to emissions and land utilization associated with traditional livestock production are acknowledged as major drivers encouraging integrators, manufacturers, and retailers to reassess protein inputs. Alternative feed proteins are positioned as lower-impact solutions because they rely on side-stream resources and deliver higher protein yields per hectare, while supporting long-term supply resilience. The discussion emphasizes that sustainability goals, regulatory momentum, and innovation collectively accelerated diversification away from conventional feed proteins during this timeframe, laying the foundation for broader commercial adoption across multiple animal production systems worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $9.7 Billion |

| CAGR | 7% |

Market adoption is further explained through the lens of food security and cost volatility. Rising feed expenses between 2021 and 2023, driven by supply disruptions and geopolitical uncertainty, increased pressure on producers to manage risk. Alternative proteins are portrayed as stabilizing inputs that enabled trials across major animal production categories. Performance outcomes from insect-derived meals, fermented plant proteins, and microbial-based ingredients are described as comparable to traditional imported protein meals, while also reducing dependency on external supply chains. Scientific research focused on digestion, gut functionality, and reduced antibiotic reliance strengthened confidence that alternative feed proteins can support animal health, welfare outcomes, and premium product positioning.

The insect protein segment held 35.1% share in 2025 and is projected to grow at a CAGR of 6.8% from 2026 to 2035. The market description highlights a clear transition away from reliance on single protein sources toward diversified ingredient portfolios. Large-scale feed manufacturers are described as blending insect-based inputs with microbial, algal, fungal, yeast-derived, and processed soy proteins. This combined approach is positioned to balance cost management, sustainability messaging, nutritional consistency, amino acid optimization, and additional functional benefits related to gut health and feed efficiency.

The poultry segment held 33.3% share in 2025, with a CAGR of 6.8% through 2035. Strategic investment is described as concentrated in high-margin animal sectors where premium feed formulations can justify higher ingredient costs. Collaborative development between producers and feed formulators is highlighted as a method for creating balanced diets that integrate alternative proteins while supporting claims related to sustainability, reduced reliance on conventional marine proteins, and novel feed inputs within both animal nutrition and companion animal markets.

North America Animal Feed Alternative Protein Market reached USD 1.19 billion in 2024. Growth in the region is attributed to vertically integrated producers seeking supply security and environmental alignment. Strong demand from poultry, specialty feed, and pet nutrition segments continues to support the adoption of fermented, yeast-based, and single-cell proteins. The United States is identified as the dominant national market, supported by advanced fermentation infrastructure, retailer-led sustainability commitments, and consistent demand for antibiotic-free and premium-positioned feed solutions that partially replace conventional soymeal.

The competitive landscape includes ADM, Calysta Inc, Angel Yeast, Innova Feed, CJ Selecta, Hamlet Protein A/S, Titan Biotech Ltd, CHS Inc, E.I. Du Pont De Nemours And Company, Agriprotein GmbH, Deep Branch Biotechnology, AB Mauri, and Crescent Biotech, all of which are actively shaping the development and commercialization of alternative feed protein solutions across global markets. Companies operating in the animal feed alternative protein market are described as strengthening their positions through capacity expansion, technology investment, and strategic partnerships. Many players are focusing on scaling fermentation and insect production systems to improve cost competitiveness and supply reliability. Portfolio diversification is emphasized as firms integrate multiple protein formats to meet varying nutritional and regulatory requirements.