Digital Freight Brokerage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1892882

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 225 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

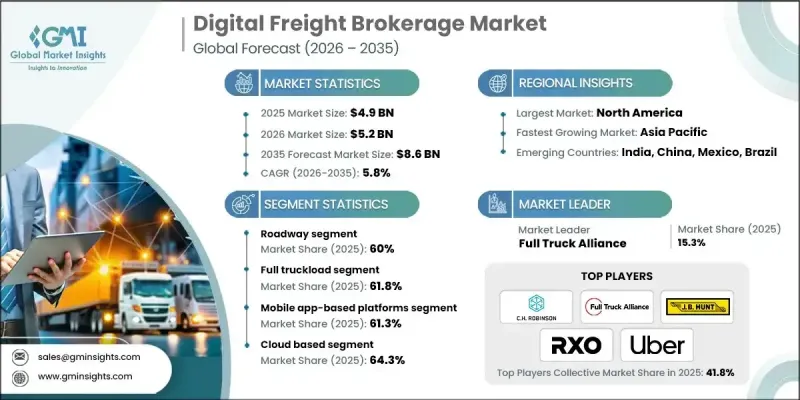

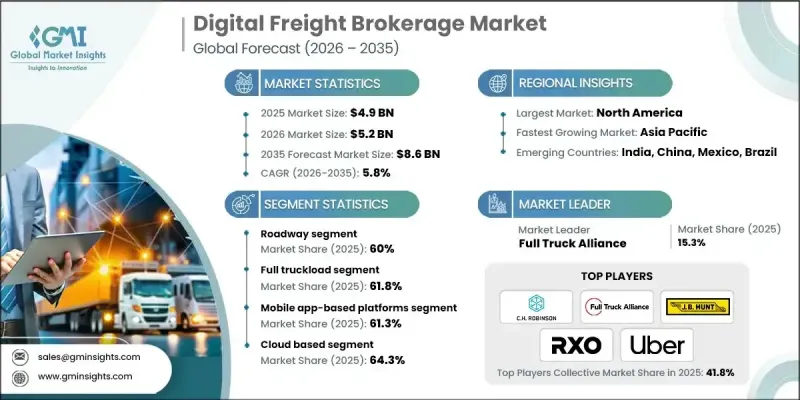

세계의 디지털 화물 중개 시장은 2025년에 49억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.8%로 성장하여 86억 달러에 이를 것으로 예측됩니다.

화주들이 자동화된 화물 매칭 시스템과 운송업체의 가용 용량을 실시간으로 확인할 수 있는 디지털 툴에 대한 의존도가 높아짐에 따라 시장 성장이 가속화되고 있습니다. 비용 효율성은 여전히 주요 동기이며, 화주들은 업무 효율화, 수작업 프로세스 최소화, 운송 비용 절감을 위해 온라인 플랫폼을 활용하고 있습니다. 디지털 중개 플랫폼은 화물 배정을 최적화하여 공회전 거리를 줄이고, 자산 활용률 향상, 운송업체 수익 증대, 서비스 전체 신뢰도 향상에 기여합니다. 디지털로 처리되는 국제화물 증가와 컴플라이언스 모니터링 강화의 추진도 자동 할당 기술의 채택을 촉진하고 있습니다. 동시에 업계는 가격 책정 정확도와 노선 수준의 성능 가시성을 향상시키는 AI 기반 예측 모델로 빠르게 전환하고 있습니다. 이러한 예측 기능은 비용 안정화 및 서비스 효율성 강화에 기여하며, 모든 화물 카테고리에서 디지털 중개 도구에 대한 수요를 더욱 증가시키고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 시장 규모

49억 달러

예측 금액

86억 달러

CAGR

5.8%

클라우드 기반 카테고리는 클라우드 지원 화물 시스템으로의 빠른 전환으로 강화되어 2025년 64.3%의 점유율을 차지할 것으로 예측됩니다. 현재 새로운 화물 관리 플랫폼의 대부분은 클라우드 아키텍처에 의존하고 있으며, 물류 업무의 현대화를 가속화하는 세계 클라우드 투자에 의해 뒷받침되고 있습니다.

모바일 앱 기반 플랫폼 부문은 2025년 61.3%의 점유율을 차지했습니다. 스마트폰의 보급과 운전자를 위한 참여 도구가 지속적으로 이용률을 높이고 있으며, 적재 정보에 대한 즉각적인 접근, 서류 관리, 위치 정보 기반 매칭 기능을 실현하고 있습니다.

미국 디지털 화물 중개 시장은 2025년 86.2%의 점유율을 차지하며 17억 6,000만 달러 규모에 달할 것으로 예측됩니다. 강력한 디지털 네트워크, 높은 도로 화물 운송량, 확대되는 라스트마일 수요는 지역 전체에서 플랫폼 도입을 뒷받침하고 있습니다. 개인 트럭 운전사 및 소규모 운송업체는 안정적인 운송 능력을 확보하기 위해 모바일 지원 적재 알림 및 텔레매틱스 연결을 점점 더 많이 활용하고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률 분석

비용 구조

각 단계별 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

FMCSA 규제

캐나다 운송청(CTA) 가이드라인

유럽

EU 운송 규제

전자 화물 지침

일반 데이터 보호 규칙(GDPR(EU 개인정보보호규정))

영국 일반 데이터 보호 규칙(UK GDPR(EU 개인정보보호규정))

디지털 타코그래프 규칙

아시아태평양

도로 화물 운송에 관한 행정 조치

사이버 보안법

물류 효율화에 관한 시책 시행

자동차법 2019

운송 사업법

스마트 물류 구상

라틴아메리카

국가 육상 운송 청(ANTT) 규제

연방 도로 운송법

USMCA 규제

중동 및 아프리카

아랍에미리트 연방 운송법

사우디아라비아 운송 및 물류 규제

도로 교통법

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재 기술 동향

신기술

비용 내역 분석

운송 비용

기술 및 플랫폼 비용

운영비용

규제 및 컴플라이언스 관련 비용

연료 및 에너지 비용

특허 분석

지속가능성과 환경 측면

지속가능한 실천

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국에 관한 고려사항

가격 분석

지역별

서비스별

이용 사례

베스트 케이스 시나리오

시장 진출 전략

지역별 시장 침투 전략

신규 참여 기업 주요 규제상 고려사항

가격 결정, 서비스, 차별화 전략

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

사업 확대 계획과 자금조달

제5장 시장 추산 및 예측 : 운송 수단별, 2022-2035

주요 동향

도로 운송

해상 운송

항공 운송

철도

제6장 시장 추산 및 예측 : 서비스별, 2022-2035

주요 동향

풀 트럭 로드(FTL)

소량 화물 운송(LTL)

인터 모달 운송

제7장 시장 추산 및 예측 : 플랫폼별, 2022-2035

주요 동향

모바일 앱 기반 플랫폼

웹 기반 플랫폼

제8장 시장 추산 및 예측 : 도입 모델별, 2022-2035

주요 동향

클라우드 기반

On-Premise

하이브리드

제9장 시장 추산 및 예측 : 기업 규모별, 2022-2035

주요 동향

중소기업(SME)

대기업

제10장 시장 추산 및 예측 : 용도별, 2022-2035

주요 동향

화물 관리

운송 회사 및 하주 매칭

가격 입찰 및 경매

실시간 추적 및 분석

자동화된 문서화

기타

제11장 시장 추산 및 예측 : 최종 용도별, 2022-2035

주요 동향

소매업 및 전자상거래

자동차

제조업

소비재

헬스케어

식품 및 음료

기타

제12장 시장 추산 및 예측 : 지역별, 2022-2035

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

네덜란드

스웨덴

아시아태평양

중국

인도

일본

호주

한국

싱가포르

태국

인도네시아

베트남

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트(UAE)

튀르키예

제13장 기업 개요

세계 기업

C.H. Robinson

Coyote Logistics

Echo Global Logistics

Hub Group

J.B. Hunt

Landstar System

Total Quality Logistics

Uber

Worldwide Express

XPO

지역 기업-

Allen Lund

ArcBest

BNSF Logistics

England Logistics

GlobalTranz Enterprises

MATSON Logistics

Schneider

Transplace

Werner Enterprises

신규 기업/디스럽터

Armstrong Transport Group

Ascent Global Logistics

Expeditors International

NTG Freight

Trinity Logistics

LSH

영문 목차

영문목차

The Global Digital Freight Brokerage Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 8.6 billion by 2035.

Market growth is accelerating as shippers increasingly rely on automated freight-matching systems and digital tools that provide real-time access to carrier capacity. Cost efficiency remains a major motivation, with shippers turning to online platforms to streamline operations, minimize manual processes, and lower transportation expenses. Digital brokerage platforms help reduce empty miles by optimizing load assignments, which enhances asset utilization, raises carrier earnings, and improves overall service dependability. The rise in international shipments processed digitally and the push for stronger compliance oversight have also reinforced the adoption of automated allocation technologies. At the same time, the industry is moving rapidly toward AI-driven forecasting models that improve pricing accuracy and lane-level performance visibility. These predictive capabilities help stabilize costs while strengthening service efficiency, further boosting the demand for digital brokerage tools across all freight categories.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$4.9 Billion

Forecast Value

$8.6 Billion

CAGR

5.8%

The cloud-based category accounted for a 64.3% share in 2025, strengthened by the rapid shift toward cloud-enabled freight systems. A significant portion of new freight management platforms now depend on cloud architecture, supported by global cloud investments that are accelerating the modernization of logistics operations.

The mobile app-based platforms segment held a 61.3% share in 2025. Widespread smartphone adoption and driver engagement tools continue to drive usage, allowing instant access to load postings, documents, and location-based matching capabilities.

U.S. Digital Freight Brokerage Market held 86.2% share and generated USD 1.76 billion in 2025. Strong digital networks, high road freight volumes, and expanding last-mile demand support platform adoption throughout the region. Independent truckers and smaller fleets are increasingly using mobile-enabled load notifications and telematics connectivity to secure consistent capacity.

Key companies in the Global Digital Freight Brokerage Market include C.H. Robinson, Coyote Logistics, Echo Global Logistics, Full Truck Alliance, J.B. Hunt, Landstar System, RXO, Total Quality Logistics (TQL), Uber, and XPO. Market leaders are strengthening their competitive positions by investing in AI-based matching engines, predictive analytics, and automated pricing tools that enhance operational accuracy and provide faster load-to-carrier pairing. Companies are expanding cloud-native platforms to improve scalability and reliability for shippers and carriers. Many are integrating telematics data, real-time tracking, and digital documentation to create seamless end-to-end workflows. Strategic partnerships with carriers, logistics service providers, and supply chain software companies also help expand network density and load availability. Businesses are focusing on mobile-first solutions to support driver engagement and speed up transactions. Continuous enhancements in compliance automation, platform security, and user experience further support market differentiation and long-term customer retention.