Renewable Feedstock Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1892689

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

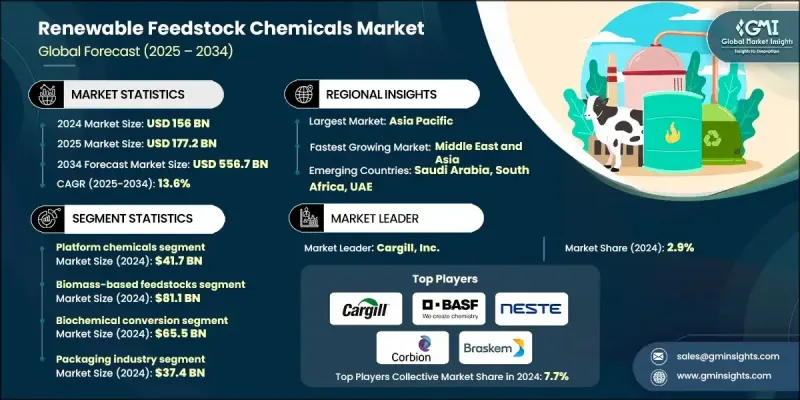

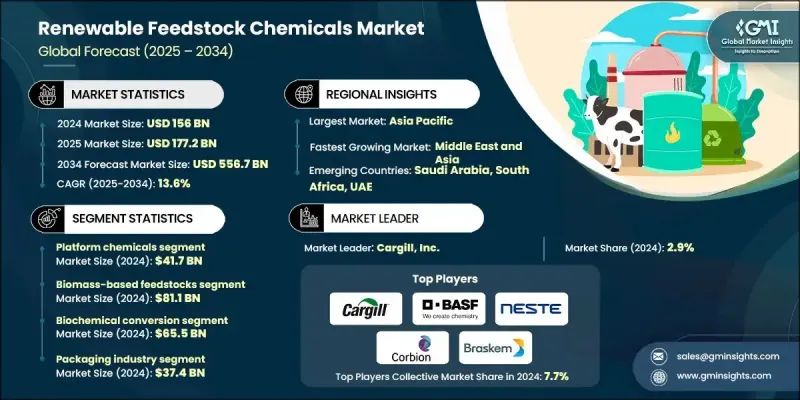

세계의 재생 원료 화학제품 시장은 2024년에 1,560억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 13.6%로 성장하여 5,567억 달러에 이를 것으로 예측됩니다.

재생가능 원료 화학제품은 바이오매스, 농업잔재물, 유기폐기물, 바이오 중간체 등 지속가능한 비화석 자원으로 제조됩니다. 기존 석유화학제품과 달리, 이 화학제품들은 탄소 발자국을 줄이고, 자원 효율적인 생산을 촉진하며, 전 세계의 지속가능성 요구에 부응하기 위해 고안된 제품입니다. 생명공학, 생화학, 열화학 변환 방법의 혁신으로 시장이 크게 성장하고 있으며, 효소 변환, 정밀 발효, 가스화, 폐기물 화학제품화 기술이 수율과 원료의 다양성을 향상시키고 있습니다. 포장, 자동차, 건설, 섬유, 소비재 등의 산업에서 수요가 증가하면서 채택이 가속화되고 있습니다. 기업들은 가동 중단 없이 배출량을 줄이기 위해 기존 생산 라인에 드롭인 바이오 소재를 통합하는 움직임이 가속화되고 있습니다. 강력한 규제 지원, 기업의 ESG에 대한 노력, 친환경 제품에 대한 소비자 선호도 변화는 시장 성장을 더욱 촉진하고 순환형 산업 밸류체인로의 전환을 형성하고 있습니다.

시장 범위

개시 연도

2024년

예측 연도

2025-2034년

개시 연도 시장 규모

1,560억 달러

예측 금액

5,567억 달러

CAGR

13.6%

플랫폼 화학제품 부문은 2024년 417억 달러 규모로, 광범위한 다운스트림 바이오 화학제품의 필수적인 구성 요소로 작용했습니다. 지속 가능한 소재를 장려하는 규제에 따라 포장용 바이오 폴리머 및 수지의 채택이 가속화되고 있습니다. 생산 효율이 향상되고 재생 가능 플라스틱의 생산 경로가 확립됨에 따라 바이오 폴리 에스테르 및 고부가가치 재료 생산에서 바이오 방향족 화합물, 올레핀, 디올, 디카 르 복실 산의 중요성이 증가하고 있습니다.

생화학 변환 부문은 2024년 655억 달러 규모 시장을 창출했으며, 발효 및 효소 경로를 이용한 바이오매스로부터 고부가가치 화학제품을 생산하는 데 있어 바이오매스의 역할을 강조하고 있습니다. 열화학 변환은 다양한 원료로부터 합성가스, 바이오 오일, 첨단 연료를 생산할 수 있는 범용성 때문에 주목받고 있습니다. 화학적 변환 기술은 정밀한 분자 변환을 가능하게 하여 제품의 수율과 성능 향상에 기여하고 있습니다.

미국 재생가능 원료 화학제품 시장은 2024년 566억 달러로 북미 성장을 주도했습니다. 이 지역은 야심찬 지속가능성 목표, 바이오 소재로의 산업 전환, 지원적인 규제, 기업의 탈탄소화 이니셔티브 등의 혜택을 누리고 있습니다. 연방 정부의 인센티브, 바이오 폴리머, 재생 가능 중간체 및 탄소 네거티브 공정에 대한 민간 부문 수요 증가와 함께 미국은 북미 시장 확대의 주요 견인차 역할을 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계별 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재 기술 동향

신기술

가격 동향

지역별

제품 유형별

향후 시장 동향

기술과 혁신 동향

현재 기술 동향

신기술

특허 동향

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

확대 계획

제5장 시장 추산 및 예측 : 제품 유형별, 2021-2034

주요 동향

플랫폼 화학제품

알코올류

에탄올(바이오 에탄올, 셀룰로오스계 에탄올)

메탄올(바이오 메탄올)

부탄올(바이오 부탄올)

유기산

젖산

석신산

구연산

이타콘산

글리세롤 및 폴리올

글리세롤(글리세린)

소르비톨

자일리톨

바이오폴리머 및 수지

생분해성 폴리머

폴리유산(PLA)

폴리 하이드록시 알카노에이트(PHA)

전분계 폴리머

드롭 인 바이오폴리머

바이오 폴리에틸렌(바이오 PE, 바이오 HDPE, 바이오 LDPE)

바이오 폴리에틸렌 테레프탈레이트(바이오 PET)

바이오 에틸렌초산비닐(바이오 EVA)

바이오 유래 방향족 화합물 및 올레핀류

방향족 화합물(BTX)

바이오 벤젠

바이오 톨루엔

바이오 크실렌(바이오 PX)

리그닌 유래 방향족 화합물

올레핀류

바이오 에틸렌

바이오 프로파일렌

디올 및 지카르본산

디올

모노에틸렌글리콜(바이오 MEG)

프로파일렌 글리콜(1,2-프로판디올)

1,3-프로판디올

1,4-부탄디올(바이오 유래 BDO)

이소소르비드

이산

플랜지 카복실산(FDCA)

아디핀산

세바신산

아제라인산

지방산 및 그 유도체

지방산

지방산 유도체

지마 지방산

지방 알코올

지방산 에스테르(FAME, FAEE)

특수 화학제품

바이오 용제

계면활성제

폴리우레탄용 폴리올

윤활유

바이오 중간체

액체 바이오 중간체(바이오 클래드, 바이오 오일)

기체 바이오 중간체(합성가스, 바이오가스)

고체/반고체 바이오 중간체(당류, 유리 지방산, 라크치드)

제6장 시장 추산 및 예측 : 원료 유형별, 2021-2034

주요 동향

바이오매스 유래 원료

농업 원료

전분 작물(옥수수, 수수, 보리)

당류 작물(사탕수수, 사탕무, 당수수)

유량작물(대두, 카놀라, 카멜리나, 야자)

농업 잔류물

옥수수짚

밀짚

바가스 및 당밀

삼림 유래 원료

벌목 잔여물

제재소 잔여물(톱밥, 나무껍질, 흑액)

전용 에너지 작물

스위치그라스 및 미스칸투스

단기 회전 목질 작물

조류(Algae) 및 해양 바이오테크놀러지 매스

폐기물 유래 원료

일반 폐기물 및 유기 폐기물(일반 폐기물, 식품 폐기물)

산업 폐기물(폐식용유, 동물성 지방, 증류 잔류유)

농업 및 축산 폐기물(퇴비, 깔짚)

바이오가스(매립지, 소화조)

재생 탄소 원료

기계적 재활용

화학적 재활용(열분해, 가스화)

포집된 탄소 원료

대기/직접 공기 회수(DAC)

산업 배출원(배기 가스, 부산 가스)

생물 유래 CO2(발효, 혐기성 소화)

제7장 시장 추산 및 예측 : 변환 기술별, 2021-2034

주요 동향

생화학적 변환

발효(알코올 발효, 젖산 발효, 첨단 발효)

효소 가수분해

혐기성 소화

열화학적 변환

가스화

열분해(고속, 저속)

열촉매 변환(바이오 TCat)

화학적 변환

에스테르 교환 반응

수소화 처리 및 수소화 처리

Fischer-tropsch 합성

탈수

메탄올에서 올레핀/방향족 화합물로의 변환(MTO/MTA)

전기화학적&CCU 프로세스

전기분해(재생 수소 제조)

이산화탄소 전기화학적 환원

CO2+H2 합성

기계적/물리적 프로세스

기계적 재활용

화학적 재활용

제8장 시장 추산 및 예측 : 최종 이용 산업별, 2021-2034

주요 동향

포장 업계

자동차 산업

섬유 및 의류 산업

건설 업계

식품 및 음료 업계

의약품 및 의료 업계

퍼스널케어 및 화장품 산업

페인트 및 코팅 산업

농업 산업

화학 산업

전자 산업

석유 및 가스 산업

제9장 시장 추산 및 예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 개요

Amyris, Inc.

Axens

Avantium N.V.

BASF SE

Braskem S.A.

Cargill, Incorporated

Corbion N.V.

Covation Bio

dsm-firmenich

Genomatica, Inc.

India Glycols Limited

NatureWorks LLC

Neste Corporation

Novamont S.p.A.

Qore-Cargill/HELM Joint Venture

Roquette

Toray Industries

UPM Biochemicals

LSH

영문 목차

영문목차

The Global Renewable Feedstock Chemicals Market was valued at USD 156 billion in 2024 and is estimated to grow at a CAGR of 13.6% to reach USD 556.7 billion by 2034.

Renewable feedstock chemicals are derived from sustainable, non-fossil sources, including biomass, agricultural residues, organic waste, and bio-based intermediates. Unlike conventional petrochemical products, these chemicals are designed to lower carbon footprints, promote resource-efficient production, and meet global sustainability mandates. Innovations in biotechnological, biochemical, and thermochemical conversion methods have significantly boosted the market, with enzymatic conversion, precision fermentation, gasification, and waste-to-chemicals technologies enhancing yield and feedstock diversity. Rising demand from industries such as packaging, automotive, construction, textiles, and consumer goods is accelerating adoption. Companies are increasingly integrating drop-in bio-based materials into existing production lines to reduce emissions without operational disruption. Strong regulatory support, corporate ESG commitments, and shifting consumer preferences toward green products are further driving market growth and shaping the transition toward circular industrial value chains.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$156 Billion

Forecast Value

$556.7 Billion

CAGR

13.6%

The platform chemicals segment accounted for USD 41.7 billion in 2024, acting as essential building blocks for a wide range of downstream bio-based chemical products. Regulations favoring sustainable materials are accelerating the adoption of biopolymers and resins for packaging applications. Improved production efficiency and established pathways for renewable plastics have elevated the importance of bio-based aromatics, olefins, diols, and dicarboxylic acids in bio-polyester and value-added material production.

The biochemical conversion segment generated USD 65.5 billion in 2024, highlighting its role in producing high-value chemicals from biomass using fermentation and enzymatic pathways. Thermochemical conversion is gaining traction for its versatility in producing syngas, bio-oils, and advanced fuels from diverse feedstocks. Chemical conversion techniques enable precise molecular transformations, boosting product yield and performance.

U.S. Renewable Feedstock Chemicals Market accounted for USD 56.6 billion in 2024, leading North America's growth. The region benefits from ambitious sustainability targets, industrial transitions to bio-based materials, supportive regulations, and corporate decarbonization initiatives. Federal incentives, rising private-sector demand for biopolymers, renewable intermediates, and carbon-negative processes are positioning the U.S. as a key driver of market expansion in North America.

Major players operating in the Global Renewable Feedstock Chemicals Market include Amyris, Inc., Axens, Avantium N.V., BASF SE, Braskem S.A., Cargill, Incorporated, Corbion N.V., Covation Bio, DSM-Firmenich, Genomatica, Inc., India Glycols Limited, NatureWorks LLC, Neste Corporation, Novamont S.p.A., Qore (Cargill/HELM Joint Venture), Roquette, Toray Industries, and UPM Biochemicals. Companies in the Global Renewable Feedstock Chemicals Market are adopting strategies such as expanding production capacity, investing in R&D for novel feedstocks and conversion technologies, and forming strategic alliances to broaden distribution networks. They focus on developing drop-in bio-based alternatives compatible with existing infrastructure, enhancing product portfolio diversification, and emphasizing regulatory compliance and sustainability certifications. Firms are leveraging circular economy principles, optimizing process efficiencies, and utilizing digital solutions for supply chain traceability.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Product Type

2.2.2 Feedstock Type

2.2.3 Conversion Technology

2.2.4 End use Industry

2.2.5 Regional

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing adoption of bio-based polymers & drop-in chemicals

3.2.1.2 Advancements in biochemical & thermochemical technologies

3.2.1.3 Expanding availability of waste & residue feedstocks

3.2.2 Industry pitfalls and challenges

3.2.2.1 High production costs limit competitiveness

3.2.2.2 Inconsistent product quality

3.2.3 Market opportunities

3.2.3.1 Integration with circular economy solutions

3.2.3.2 Development of specialty bio-based chemicals

3.2.3.3 Leveraging digital traceability for premium products

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By product type

3.9 Future market trends

3.10 Technology and innovation landscape

3.10.1 Current technological trends

3.10.2 Emerging technologies

3.11 Patent landscape

3.12 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

3.12.1 Major importing countries

3.12.2 Major exporting countries

3.13 Sustainability and environmental aspects

3.13.1 Sustainable practices

3.13.2 Waste reduction strategies

3.13.3 Energy efficiency in production

3.13.4 Eco-friendly initiatives

3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)