지속가능한 제지용 화학제품 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Sustainable Paper Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1797719

리서치사:Global Market Insights Inc.

발행일:2025년 07월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

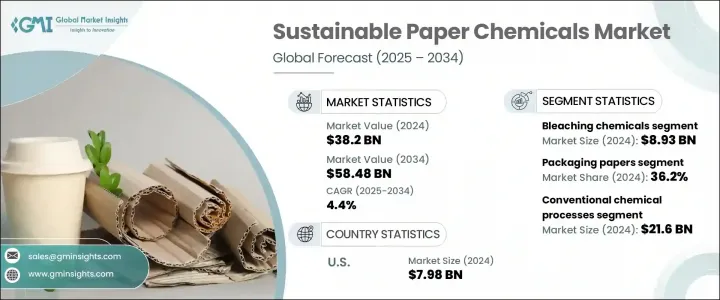

세계의 지속가능한 제지용 화학제품 시장 규모는 2024년 382억 달러에 달했고, CAGR 4.4%로 성장하여 2034년까지 584억 8,000만 달러에 달할 것으로 예측되고 있습니다.

환경 친화적인 솔루션에 대한 세계 선호도 증가는 제지 제조에서 지속가능한 대체품에 대한 수요를 계속 증가하고 있습니다. 재생 가능한 자원에서 유래하여 물 소비량과 에너지 효율을 줄이는 화학제품은 보다 깨끗한 생산을 위한 세계의 노력에 부합하고 있습니다. 생태학적 과제에 대한 의식 증가, 환경 규제 강화, 순환형 경제 모델로 증가가 지속가능한 제제로의 전환을 뒷받침하고 있습니다.

제조업체가 기존 제지용 첨가제에서 생분해성, 재활용성 및 무독성 대체품으로 이동함에 따라 시장은 지속적인 확대를 기대하고 있습니다. 이러한 진보는 종이 생산에서 생태계에 미치는 영향을 개선할 뿐만 아니라 내구성, 인쇄 품질, 재활용성 등 종이 제품의 기능성을 높여줍니다. 세계 각국의 정부는 그린 케미컬 대체물 및 기능성 첨가물 연구에 투자하고 있으며, 제지 부문의 지속가능한 변화에 대한 노력을 더욱 강화하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

382억 달러

예측 금액

584억 8,000만 달러

CAGR

4.4%

2024년, 포장용지 분야의 점유율은 36.2%에 달할 전망입니다. 이 분야에서는 친환경 코팅제, 장벽제, 강도 향상제 등 수요가 가속화되고 있으며, 재활용성과 퇴비화를 지원하면서 패키지의 성능을 유지하기 위해 급성장하고 있습니다. 온라인 소매 및 식품 택배 서비스의 상승은 기능성과 지속가능성 목표에 대한 적합성을 결합한 종이 포장의 필요성을 더욱 향상시키고 있습니다. 브랜드는 내습성, 내구성, 인쇄 적성 등의 성능에 대한 기대에 부응하면서, 환경 실적를 삭감하는 바이오의 화학 투입물에 대한 기울기를 강화하고 있습니다.

기존의 화학처리 분야는 2024년 216억 달러를 창출했습니다. 이러한 확립된 방법은 확장성, 비용 이점, 기존 제지 공장의 운영에 통합의 용이성으로 인해 여전히 지배적입니다. 전통에 뿌리를 두면서도 깨끗하고 자원 효율적인 방법을 요구하는 규제 개혁의 영향으로 이러한 시스템은 진화하고 있습니다. 생명공학, 나노기술, AI를 활용한 생산감시 등의 혁신은 제조업체 사이클에서 화학물질의 사용을 더욱 최적화하기 위해 응용되고 있습니다. 그 결과, 기존의 방법이 점차 적응되어 사업의 연속성을 저해하지 않고 지속가능성의 지표를 충족하게 되었습니다.

미국의 지속가능한 제지용 화학제품 시장은 2024년에 79억 8,000만 달러를 창출하여 지속가능한 제지용 화학제품 시장을 견인했습니다. 이 나라의 지위는 개발된 생산 인프라, 규정 준수의 중요성, 환경적으로 안전한 종이 및 포장 제품에 대한 소비자 선호 증가로 인한 것입니다. 인쇄, 포장, 출판 분야에서 그린 케미스트리가 대규모로 채택됨에 따라 수요가 더욱 커지고 있습니다. 한편 캐나다에서는 지역 프로그램이 보다 깨끗한 기술과 순환형 관행을 추진하고, 현지 제지 제조업체가 보다 안전하고 재생 가능한 화학물질 투입으로 이행하도록 촉구하고 있어 꾸준한 진전을 볼 수 있습니다.

지속가능한 제지 화학 시장 경쟁 구도를 형성하는 주요 기업으로는 Dow Inc., Solenis LLC, SNF Group, Buckman Laboratories International, Inc., Kemira Oyj, Ashland Global Holdings Inc., Nouryon, Ecolab Inc., Clariant AG, BASF SE 등이 있습니다. 지속가능한 제지용 화학제품 시장의 선두 기업은 세계의 존재감을 높이기 위해 다방면에 걸친 전략을 채택하고 있습니다. 이러한 기업들은 진화하는 규제기준과 지속가능성 벤치마크에 적합한 첨단 바이오 생분해성 화학제품을 개발하기 위해 연구개발에 많은 투자를 하고 있습니다. 생산 능력을 확대하고 지역적인 파트너십을 연결함으로써 유통망을 개선하고 신흥 시장에 접근할 수 있습니다. 전략적 인수 및 합작 투자는 또한 그린 케미컬 솔루션을 보다 광범위한 포트폴리오에 통합하는 데 사용됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 리스크 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTLE 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

가격 동향

지역별

소재 유형별

미래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)

(참고: 무역 통계는 주요 국가에서만 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속가능한 관행

폐기물 감축 전략

생산에서의 에너지 효율

환경 친화적인 노력

탄소발자국의 고려

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

주요 동향

표백제

이산화염소

과산화수소

산소계 표백제

효소 기반 표백 시스템

코팅 화학약품

전분계 코팅

라텍스 코팅

배리어 코팅

바이오 코팅 솔루션

프로세스 화학제품

펄프화 화학약품

탈묵제

부선 화학약품

세정용 화학약품

기능성 화학제품

습윤강도 증강제

건조강도 증강제

유지 및 배수 보조제

사이즈제

특수첨가제

소포제

살생물제

부식 억제제

pH 조정제

제6장 시장 추계 및 예측 : 용도별, 2021-2034년

주요 동향

포장지

골판지 포장

접이식 판지

식품 포장

공업용 포장

티슈 및 위생 용품

티슈 페이퍼

화장지

종이 타월

냅킨

인쇄 및 필기 용지

코팅지

비코팅지

신문 용지

서적논문

특수지

보안 서류

여과지

장식지

기술지

제7장 시장 추계 및 예측 : 기술별, 2021-2034년

주요 동향

기존 화학 공정

크래프트 펄프

아황산 펄프화

기계 펄프화

지속가능한 화학 공정

효소 프로세스

바이오 화학 공정

그린케미스트리 응용

폐루프 시스템

신흥기술

나노기술 응용

생명공학 솔루션

디지털 프로세스 제어

인공지능 통합

제8장 시장 추계 및 예측 : 최종 이용 산업별, 2021-2034년

주요 동향

식품 및 음료 업계

식품 포장

음료 포장

퀵 서비스 레스토랑

헬스케어 및 의약품

의료용 포장

의약품 포장

헬스케어 위생 제품

소비재

퍼스널케어 제품

가정용품

전자상거래 포장

산업용도

자동차산업

일렉트로닉스 업계

건설 업계

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

Kemira Oyj

BASF SE

Solenis LLC

Nouryon(formerly AkzoNobel Specialty Chemicals)

Ecolab Inc.

SNF Group

Ashland Global Holdings Inc.

Clariant AG

Dow Inc.

Buckman Laboratories International, Inc.

JHS

영문 목차

영문목차

The Global Sustainable Paper Chemicals Market was valued at USD 38.2 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 58.48 billion by 2034. The increasing global preference for environmentally responsible solutions continues to elevate demand for sustainable alternatives in paper manufacturing. Chemicals derived from renewable sources that support lower water consumption and energy efficiency are aligning well with global efforts toward cleaner production. Rising awareness of ecological challenges, stricter environmental mandates, and a growing push toward circular economy models are reinforcing the switch to sustainable formulations.

The market is expected to experience continuous expansion as manufacturers shift away from conventional paper-making additives in favor of biodegradable, recyclable, and non-toxic substitutes. These advancements are not only improving the ecological impact of paper production but are also boosting the functional capabilities of paper products in terms of durability, print quality, and recyclability. Governments around the world are also channeling investments into research for green chemical alternatives and functional additives, further strengthening the paper sector's commitment to sustainable transformation.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$38.2 Billion

Forecast Value

$58.48 Billion

CAGR

4.4%

In 2024, the packaging paper segment represented a 36.2% share. This segment has witnessed rapid growth as demand accelerates for eco-friendly coatings, barrier agents, and strength enhancers that maintain package performance while supporting recyclability and compostability. The rise of online retail and food delivery services has only intensified the need for paper packaging that is both functional and compliant with sustainability goals. Brands are increasingly leaning toward bio-based chemical inputs that reduce their environmental footprint while still meeting performance expectations for moisture resistance, durability, and printability.

The conventional chemical processing segment generated USD 21.6 billion in 2024. These well-established methods remain dominant due to their scalability, cost advantages, and ease of integration into existing paper mill operations. While rooted in tradition, these systems are evolving under the influence of regulatory reforms that demand cleaner, more resource-efficient practices. Innovations-such as biotechnology, nanotechnology, and AI-driven production monitoring-are being applied to further optimize the use of chemicals in the manufacturing cycle. As a result, conventional methods are gradually adapted to meet sustainability metrics without disrupting operational continuity.

United States Sustainable Paper Chemicals Market generated USD 7.98 billion in 2024, driven by the sustainable paper chemicals market. The country's position stems from its well-developed production infrastructure, emphasis on regulatory compliance, and growing consumer preference for environmentally safe paper and packaging products. Demand is being further driven by large-scale adoption of green chemistry across printing, packaging, and publishing segments. Meanwhile, Canada is experiencing steady progress as regional programs promote cleaner technologies and circular practices, encouraging local paper producers to transition toward safer, renewable chemical inputs.

Key companies shaping the competitive landscape of the Sustainable Paper Chemicals Market include Dow Inc., Solenis LLC, SNF Group, Buckman Laboratories International, Inc., Kemira Oyj, Ashland Global Holdings Inc., Nouryon, Ecolab Inc., Clariant AG, and BASF SE. Leading players in the sustainable paper chemicals market are adopting multi-pronged strategies to build a strong global presence. These companies are heavily investing in R&D to develop advanced bio-based and biodegradable chemicals that align with evolving regulatory standards and sustainability benchmarks. Expanding production capacities and forming regional partnerships allow them to improve distribution networks and access emerging markets. Strategic acquisitions and joint ventures are also being used to integrate green chemistry solutions into broader portfolios.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Product type trends

2.2.2 Application trends

2.2.3 Technology trends

2.2.4 End use industry trends

2.2.5 Regional

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By material type

3.9 Future market trends

3.10 Technology and Innovation landscape

3.10.1 Current technological trends

3.10.2 Emerging technologies

3.11 Patent Landscape

3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

3.12.1 Major importing countries

3.12.2 Major exporting countries

3.13 Sustainability and environmental aspects

3.13.1 Sustainable practices

3.13.2 Waste reduction strategies

3.13.3 Energy efficiency in production

3.13.4 Eco-friendly initiatives

3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million) (Units)

5.1 Key trends

5.2 Bleaching chemicals

5.2.1 Chlorine dioxide

5.2.2 Hydrogen peroxide

5.2.3 Oxygen-based bleaching agents

5.2.4 Enzyme-based bleaching systems

5.3 Coating chemicals

5.3.1 Starch-based coatings

5.3.2 Latex coatings

5.3.3 Barrier coatings

5.3.4 Bio-based coating solutions

5.4 Process chemicals

5.4.1 Pulping chemicals

5.4.2 Deinking chemicals

5.4.3 Flotation chemicals

5.4.4 Cleaning chemicals

5.5 Functional chemicals

5.5.1 Wet strength agents

5.5.2 Dry strength agents

5.5.3 Retention and drainage aids

5.5.4 Sizing agents

5.6 Specialty additives

5.6.1 Defoamers

5.6.2 Biocides

5.6.3 Corrosion inhibitors

5.6.4 Ph control agents

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Units)

6.1 Key trends

6.2 Packaging papers

6.2.1 Corrugated packaging

6.2.2 Folding cartons

6.2.3 Food packaging

6.2.4 Industrial packaging

6.3 Tissue and hygiene products

6.3.1 Facial tissue

6.3.2 Toilet paper

6.3.3 Paper towels

6.3.4 Napkins

6.4 Printing and writing papers

6.4.1 Coated papers

6.4.2 Uncoated papers

6.4.3 Newsprint

6.4.4 Book papers

6.5 Specialty papers

6.5.1 Security papers

6.5.2 Filter papers

6.5.3 Decorative papers

6.5.4 Technical papers

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Million) (Units)

7.1 Key trends

7.2 Conventional chemical processes

7.2.1 Kraft pulping

7.2.2 Sulfite pulping

7.2.3 Mechanical pulping

7.3 Sustainable chemical processes

7.3.1 Enzymatic processes

7.3.2 Bio-based chemical processes

7.3.3 Green Chemistry applications

7.3.4 Closed-loop systems

7.4 Emerging technologies

7.4.1 Nanotechnology applications

7.4.2 Biotechnology solutions

7.4.3 Digital process control

7.4.4 Artificial intelligence integration

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million) (Units)

8.1 Key trends

8.2 Food and beverage industry

8.2.1 Food packaging

8.2.2 Beverage packaging

8.2.3 Quick service restaurants

8.3 Healthcare and pharmaceuticals

8.3.1 Medical packaging

8.3.2 Pharmaceutical packaging

8.3.3 Healthcare hygiene products

8.4 Consumer Goods

8.4.1 Personal care products

8.4.2 Household products

8.4.3 E-commerce packaging

8.5 Industrial applications

8.5.1 Automotive industry

8.5.2 Electronics industry

8.5.3 Construction industry

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Units)