수산양식 사료용 단백질 가수분해물 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

Protein Hydrolysates in Aquaculture Feed Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1885824

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

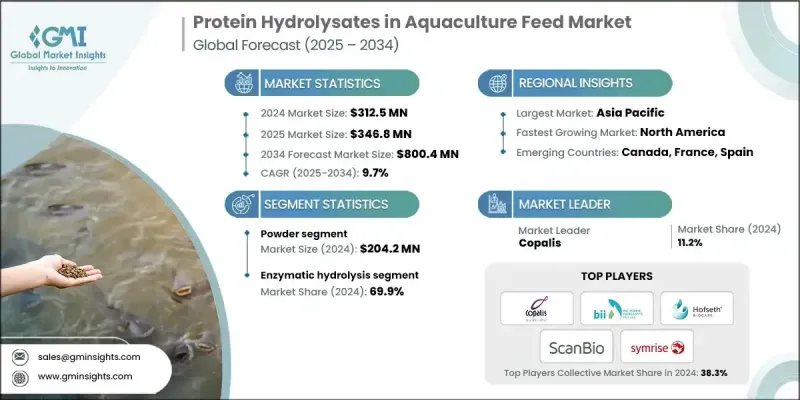

세계의 수산양식 사료용 단백질 가수분해물 시장은 2024년 3억 1,250만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 9.7%로 성장할 전망이며, 8억 40만 달러에 이를 것으로 예측됩니다.

본 원료는 단백질을 풍부하게 포함하는 해양 및 육생 자원을 효소 또는 화학적 분해에 의해 제어된 방법으로 보다 작고 소화성이 높은 펩티드나 아미노산으로 분해하여 제조됩니다. 양식 수산 생물에서 영양 흡수 촉진, 성장 성능 향상, 질병 저항성 강화에 기여하기 때문에 현대적인 지속 가능한 수산 양식 시스템에 필수적인 존재입니다. 시장 확대는 자원 순환 이용을 촉진하는 규제 프레임워크에 의해 지원되는 책임있는 양식 기술에 대한 중시 증가에 크게 영향을 받고 있습니다. 북미는 어업 폐기물을 고부가가치 가수분해물로 전환하고 환경 부하를 저감함과 동시에 지속가능성 기준에 준거를 지원하는 정책에 따라 가장 성장이 큰 지역으로 대두하고 있습니다. 친환경 사료 원료에 대한 수요 증가 및 천연 유래의 고성능 첨가물로의 이행이 채용 확대를 추진하고 있습니다. 세계의 양식 업계가 건강, 면역, 효율적인 사료 이용에 주력하는 자세를 강화하고 있는 것도, 생물활성 단백질 가수분해물의 필요성을 한층 더 가속시키고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

시작 시 가치

3억 1,250만 달러

예측 금액

8억 40만 달러

CAGR

9.7%

분말 기반 가수분해물은 2024년에 2억 420만 달러의 수익을 창출했습니다. 분말 형태는 장기 보존 기간 동안 안정성 및 영양가를 유지하며 농축되어 운송이 용이합니다. 사료 제조업체는 분말 제형을 선호하고 채용하고 있습니다. 이는 첨단 혼합 공정에 원활하게 통합되어 일관된 품질 관리를 지원하고 지역에 관계없이 꾸준한 시장 성장을 가능하게 하기 때문입니다.

2024년에는 효소 가수분해법이 69.9%의 점유율을 차지했습니다. 이 기술은 제어된 펩티드 프로파일과 우수한 소화성 및 생체이용률을 갖춘 고기능성 가수분해물을 생성합니다. 이 과정은 주요 생물 활성 성분을 보유하고 양식 종에서 최적의 건강 상태와 생산성을 지원하는 표적 펩타이드 분획의 창출을 가능하게합니다.

북미의 수산양식 사료용 단백질 가수분해물 시장은 2025-2034년 연평균 복합 성장률(CAGR) 10%로 확대될 것으로 예측됩니다. 지속 가능한 양식법에 대한 의식의 고조 및 천연 유래로 생분해성 사료 원료에 대한 선호 증가가 수요 증가의 요인이 되고 있습니다. 지역의 생산자 및 사료 제조업체는 사료 품질을 향상시키면서 생태계에 대한 영향을 저감하는 환경에 배려한 원료를 우선적으로 채용하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

수산 양식 생산량과 사료 수요 증가

질병 예방 및 면역 시스템 강화

수산가공 제품별 지속가능한 이용

업계의 잠재적 위험 및 과제

높은 생산 비용 및 복잡한 가공 요건

원재료 공급 제약 및 계절적인 이용가능성

시장 기회

종 특이적인 가수분해물 개발

생물활성 펩티드 분획의 용도 분야

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재의 기술 동향

신흥 기술

가격 동향

지역별

형태별

장래 시장 동향

특허 상황

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성 및 환경면

지속가능한 대처

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경에 배려한 대처

탄소발자국 고려

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

확대 계획

제5장 시장 추계 및 예측 : 형태별(2021-2034년)

주요 동향

분말

액체

페이스트

제6장 시장 추계 및 예측 : 제조 공정별(2021-2034년)

주요 동향

효소 가수분해

화학적 가수분해

산 가수분해

알칼리 가수분해

자기 가수분해

기타

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

유생용 사료

스타터 사료

육성용 사료

기능성 사료

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Alfa Laval AB

Bio-Marine Ingredients Ireland Ltd

Copalis

Hofseth Biocare

Janatha Fish Meal

Kemin Industries

SAMPI

Scanbio

Sopropeche

Symrise

AJY

영문 목차

영문목차

The Global Protein Hydrolysates in Aquaculture Feed Market was valued at USD 312.5 million in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 800.4 million by 2034.

The ingredients are produced through controlled enzymatic or chemical breakdown of protein-rich marine and terrestrial sources into smaller, highly digestible peptides and amino acids. Their use enhances nutrient absorption, boosts growth performance, and strengthens disease resistance in farmed aquatic species, making them essential for modern, sustainable aquaculture systems. Market expansion is strongly influenced by growing emphasis on responsible farming practices, supported by regulatory frameworks that encourage circular resource use. North America is emerging as the fastest-growing region as policies encourage transforming fishery waste into high-value hydrolysates, reducing environmental impact, and supporting compliance with sustainability standards. Rising demand for eco-friendly feed inputs and the shift toward natural, high-performance additives are driving increased adoption. The global aquaculture sector's heightened focus on health, immunity, and efficient feed utilization further accelerates the need for bioactive protein hydrolysates.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$312.5 Million

Forecast Value

$800.4 Million

CAGR

9.7%

The powder-based hydrolysates generated USD 204.2 million in 2024. The powdered form maintains stability and nutritional integrity over long storage periods and is easier to transport due to its concentrated nature. Feed manufacturers prefer powder formulations because they integrate smoothly into advanced mixing operations, supporting consistent quality control and enabling steady market growth across regions.

The enzymatic hydrolysis accounted for a 69.9% share in 2024. This method produces highly functional hydrolysates with controlled peptide profiles and superior digestibility and bioavailability. The process preserves key bioactive components and allows the creation of targeted peptide fractions that support optimal health and performance in aquaculture species.

North America Protein Hydrolysates in Aquaculture Feed Market is projected to grow at a CAGR of 10% from 2025 to 2034. Rising awareness of sustainable aquaculture practices and the increasing preference for natural, biodegradable feed ingredients are contributing to strong demand. Regional producers and feed manufacturers are prioritizing environmentally responsible inputs that enhance feed quality while lowering ecological impact.

Key companies in the Protein Hydrolysates in Aquaculture Feed Market include Scanbio, Symrise, Kemin Industries, Copalis, SAMPI, Alfa Laval AB, Hofseth Biocare, Bio-Marine Ingredients Ireland Ltd, Sopropeche, and Janatha Fish Meal. Companies in the protein hydrolysates in aquaculture feed market enhance their competitiveness through investments in advanced enzymatic processing, expansion of production capacity, and optimization of raw material utilization. Many emphasize sustainable sourcing by converting fishery by-products into high-value hydrolysates, aligning with circular economy goals. Strategic collaborations with aquaculture producers help tailor hydrolysate profiles for specific species and life stages, improving performance outcomes. Firms adopt strict quality certification systems to meet global regulatory expectations and build customer confidence. Product diversification aimed at functional, nutrient-dense peptide solutions strengthens their presence across premium feed categories.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Form trends

2.2.2 Process trends

2.2.3 Application trends

2.2.4 Regional trends

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing aquaculture production & feed demand

3.2.1.2 Disease prevention & immune system enhancement

3.2.1.3 Sustainable utilization of fish processing by-products

3.2.2 Industry pitfalls and challenges

3.2.2.1 High production costs & complex processing requirements

3.2.2.2 Raw material supply constraints & seasonal availability

3.2.3 Market opportunities

3.2.3.1 Species-specific hydrolysate development

3.2.3.2 Bioactive peptide fraction applications

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By form

3.9 Future market trends

3.10 Patent landscape

3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Form, 2021-2034 (USD Million) (Kilo Tons)

5.1 Key trends

5.2 Powder

5.3 Liquid

5.4 Paste

Chapter 6 Market Estimates and Forecast, By Process, 2021-2034 (USD Million) (Kilo Tons)

6.1 Key trends

6.2 Enzymatic hydrolysis

6.3 Chemical hydrolysis

6.3.1 Acid hydrolysis

6.3.2 Alkaline hydrolysis

6.4 Autolytic hydrolysis

6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

7.1 Key trends

7.2 Larval feeds

7.3 Starter feeds

7.4 Grow-out feeds

7.5 Functional feeds

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)