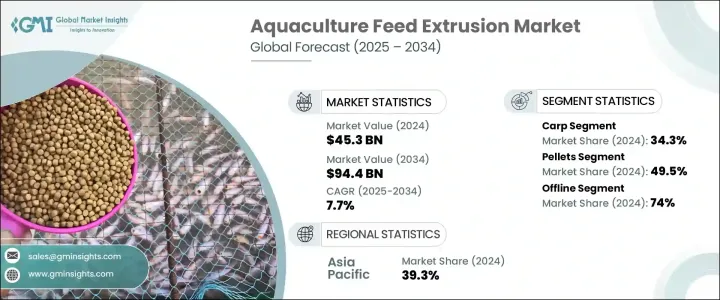

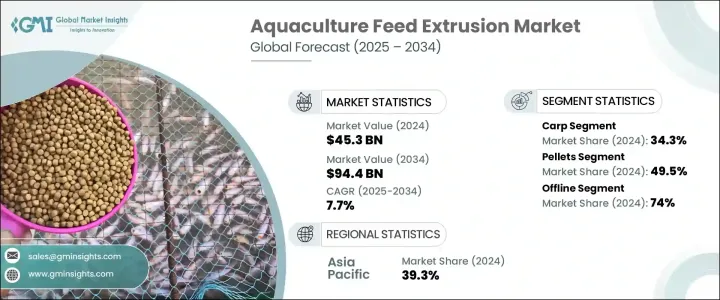

세계의 수산 양식 사료 압출 시장은 2024년 453억 달러로 평가되었으며, 2034년에는 944억 달러에 이를 것으로 추정되며, CAGR 7.7%로 성장할 전망입니다.

지난 10년 동안 이 시장은 고단백 해산물에 대한 수요 증가와 집중적인 양식 관행으로의 전 세계적인 변화에 힘입어 꾸준히 확장되었습니다. 전통적인 사료 공급 방식은 영양이 풍부하고 물이 안정된 사료 옵션을 제공하는 첨단 압출 기술로 대체되었습니다. 이러한 혁신은 사료 효율과 동물의 건강을 개선했을 뿐만 아니라 양식 시스템이 환경에 미치는 영향도 최소화했습니다. 정밀한 배합과 표적 영양 공급을 가능하게 하는 사료 압출은 다양한 수생 어종의 식이 요구를 충족하는 데 매우 중요해졌습니다. 압출 사료는 소화율, 안정성 및 전환율 측면에서 이점을 제공하기 때문에 상업적 운영 전반에 걸쳐 선호되는 선택입니다. 향상된 장비 기술은 전 세계 및 지역 사료 생산업체가 맞춤형 사료 솔루션을 대규모로 생산할 수 있는 능력을 제공함으로써 이러한 전환을 더욱 뒷받침하고 있습니다.

어종별 사료 수요는 계속해서 시장 역학 관계를 형성하고 있습니다. 2024년 어종별 시장 점유율은 잉어가 34.3%로 가장 높았는데, 이는 사료 생산의 비용 효율성과 적용의 용이성에 힘입은 결과입니다. 각 수생 어종은 서로 다른 영양 및 성장 문제를 안고 있어 사료 배합 및 압출 요건의 복잡성을 야기합니다. 육식성 어종은 단백질이 풍부한 압출 배합의 이점을 누리는 반면, 제조업체는 특히 비용에 민감한 지역에서 경제성을 유지해야 하는 압박을 받고 있습니다. 영양학적으로 우수하고 물에 안정된 사료로의 전환은 어류의 건강을 개선하고 수중 환경의 주요 관심사로 남아 있는 영양소 침출을 최소화하는 데 핵심적인 역할을 합니다. 동시에 양식업자들은 소비 중 모니터링이 용이하고 특히 대량 양식 시설에서 전반적인 낭비를 줄이는 데 기여하는 사료를 찾고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 453억 달러 |

| 예측 금액 | 944억 달러 |

| CAGR | 7.7% |

예를 들어, 틸라피아 사료 생산은 어분 의존도를 줄이기 위해 식물성 단백질로 전환하여 보다 지속 가능한 사료 원료로의 전환을 지원하고 있습니다. 일반적으로 단백질 함량이 낮고 가라앉는 펠렛 형태로 제공되는 메기 사료는 집약적인 양식장에서 소화가 잘되는 사료에 대한 수요 증가를 충족하기 위해 재평가되고 있습니다. 사료 전환율이 더욱 면밀히 조사됨에 따라 생산자들은 비용 증가 없이 효율성을 유지하기 위해 품질과 비용 간의 균형을 맞추기 위해 노력하고 있습니다.

사료 유형별로 분류하면(2024년) 양식용 사료 압출 시장은 펠렛이 49.5%의 점유율로 선두를 차지했습니다. 펠렛은 사료 공급의 일관성과 성능을 추구하는 대규모 양식 시설의 수요에 힘입어 7.3%의 연평균 성장률로 계속 확대될 것으로 예상됩니다. 펠렛은 부력, 물의 안정성, 높은 영양분을 운반할 수 있는 능력으로 다양한 수생 어종에 이상적입니다. 압출 기술의 지속적인 발전으로 특정 먹이 행동과 환경 조건을 충족하는 특수 부유형 및 천천히 가라앉는 펠렛 유형을 개발할 수 있게 되었습니다. 그러나 프리미엄 펠렛 사료는 생산 비용이 높기 때문에 예산이 제한된 소규모 생산자에게는 장애물이 될 수 있습니다.

과립은 크기가 작고 섭취하기 쉽기 때문에 어린 어종에 여전히 널리 사용되고 있습니다. 편리하지만 충분한 수분 안정성이 부족하여 낭비가 많고 고밀도 시스템에서 세심한 관리가 필요한 경우가 많습니다. 일반적으로 부화장에서 초기 단계의 어류와 새우를 위해 사용되는 분말 사료는 필수 영양소를 공급하지만 과잉 공급과 수질 악화를 피하기 위해 정밀한 적용이 필요합니다.

시장의 유통 채널은 온라인과 오프라인으로 나뉩니다. 2024년에는 오프라인 판매가 전체 매출의 74%를 차지하며 시장을 지배했습니다. 이 채널은 주요 양식 지역에서의 강력한 입지로 인해 8.9%의 강력한 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다. 오프라인 채널은 유연한 결제 조건, 맞춤형 영양 계획, 준비된 재고 공급 등 맞춤형 지원을 제공하기 때문에 인기가 높습니다. 이러한 요소는 양식 인프라가 잘 구축된 지역에서 특히 중요합니다.

지역별로는 아시아태평양이 2024년 매출액 점유율 39.3%로 세계 시장을 선도하고 있습니다. 이 지역은 높은 양식 생산량과 사료 현대화 및 지속 가능성을 목표로 하는 정부의 우호적인 이니셔티브의 혜택을 받고 있습니다. 중국, 인도, 동남아시아 등의 시장은 해산물 소비 증가와 사료 효율성 향상을 위한 노력으로 지역 지배력을 계속 이어갈 것입니다. 반면 북미와 같은 지역은 지속 가능한 양식 관행에 대한 인식이 높아지고 현지에서 공급되는 해산물에 대한 관심이 높아지면서 완만하지만 꾸준한 성장세를 보이고 있습니다.

시장을 선도하는 기업은 ADM, Cargill, Biomar, Purina Animal Nutrition LLC, Skretting, DSM, Aller Aqua 그룹 등이 있습니다. 이 기업들은 혁신, 단백질 공급원의 다양화, 환경을 고려한 사료 제품 개발을 통해 시장 지형을 형성하고 있습니다. 이들의 노력은 글로벌 규모의 운영과 현지화된 사료 맞춤화를 모두 지원하여 전반적인 양식 사료 압출 생태계를 강화합니다.

The Global Aquaculture Feed Extrusion Market was valued at USD 45.3 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 94.4 billion by 2034. Over the last decade, this market has witnessed steady expansion, largely fueled by the rising demand for high-protein seafood and the global shift toward intensive aquaculture practices. Traditional feeding methods have given way to more advanced extrusion techniques that provide nutrient-dense, water-stable feed options. These innovations have not only improved feed efficiency and animal health but have also minimized the environmental impact of aquaculture systems. Feed extrusion, which allows for precise formulation and targeted nutrition, has become critical to meeting the dietary needs of diverse aquatic species. Extruded feeds offer advantages in terms of digestibility, stability, and conversion rates, making them the preferred choice across commercial operations. Enhanced equipment technology has further supported this transition by giving both global and regional feed producers the ability to create tailored feed solutions at scale.

Species-specific feed demand continues to shape market dynamics. In 2024, carp held the largest market share by species at 34.3%, driven by the cost-effectiveness of feed production and ease of application. Each aquatic species poses different nutritional and growth challenges, contributing to the complexity of feed formulation and extrusion requirements. While carnivorous species benefit from protein-rich extruded formulations, manufacturers are also being pushed to maintain affordability-particularly in cost-sensitive regions. The shift toward nutritionally superior, water-stable feeds is central to improving fish health and minimizing nutrient leaching, which remains a key concern in aquatic environments. At the same time, farmers seek feeds that are easy to monitor during consumption and contribute to reducing overall wastage, especially in high-volume farming setups.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $45.3 Billion |

| Forecast Value | $94.4 Billion |

| CAGR | 7.7% |

Tilapia feed production, for instance, has seen a transition toward plant-based proteins to reduce reliance on fishmeal, supporting the move toward more sustainable feed ingredients. Catfish feeds, typically lower in protein and presented in sinking pellet forms, are being re-evaluated to meet the rising need for highly digestible feed in intensive farming operations. As feed conversion ratios come under greater scrutiny, producers are working to strike a balance between quality and cost, aiming to maintain efficiency without driving up expenses.

When categorized by feed type, pellets led the aquaculture feed extrusion market in 2024 with a 49.5% share. Pellets are expected to continue expanding at a CAGR of 7.3%, driven by demand from large-scale aquaculture facilities seeking consistency and performance in feed delivery. Their buoyancy, water stability, and ability to carry high nutrient loads make them ideal for a broad range of aquatic species. Ongoing advances in extrusion allow for the development of specialized floating and slow-sinking pellet types that meet specific feeding behaviors and environmental conditions. However, premium pellet feeds come with high production costs, which can be a hurdle for small-scale producers with limited budgets.

Granules remain widely used for juvenile aquatic species due to their small size and ease of intake. Although they are convenient, they often lack sufficient water stability, leading to higher waste and requiring careful management in high-density systems. Powdered feed, generally used in hatcheries for early-stage fish and shrimp, delivers essential nutrients but demands precise application to avoid overfeeding and deterioration in water quality.

The market's distribution channels are divided into online and offline modes. In 2024, offline sales dominated the market, accounting for 74% of total revenue. This channel is expected to grow at a robust CAGR of 8.9% due to its strong presence in key aquaculture regions. Offline channels are popular due to the personalized support they provide, including flexible payment terms, customized nutritional planning, and ready inventory supply. These factors are especially important in regions with well-established aquaculture infrastructure.

Regionally, Asia Pacific led the global market with a 39.3% revenue share in 2024. The region benefits from high aquaculture output and favorable government initiatives aimed at feed modernization and sustainability. Markets such as China, India, and Southeast Asia continue to drive regional dominance, with increasing seafood consumption and efforts to enhance feed efficiency. In contrast, regions like North America show moderate but steady growth, driven by growing awareness of sustainable aquaculture practices and a focus on locally sourced seafood.

Leading market players include ADM, Cargill, Biomar, Purina Animal Nutrition LLC, Skretting, DSM, and Aller Aqua Group. These companies shape the market landscape through innovation, diversification of protein sources, and development of environmentally conscious feed products. Their efforts support both global scale operations and localized feed customization, strengthening the overall aquaculture feed extrusion ecosystem.