Peptide Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1876810

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 142 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

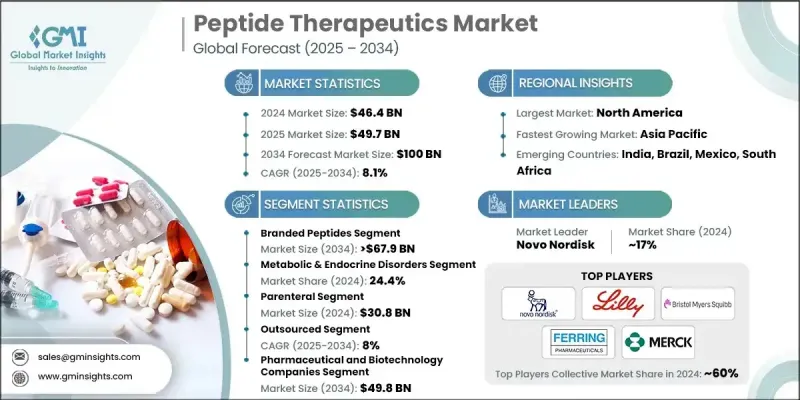

세계의 펩타이드 치료제 시장은 2024년에 464억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 8.1%로 성장하여 1,000억 달러에 이를 것으로 예측되고 있습니다.

당뇨병, 암, 비만 등 만성질환과 생활습관병 증가가 주요 성장 요인으로 작용하고 있습니다. 펩타이드 치료제는 짧은 아미노산 사슬로 구성되어 특정 분자 경로를 표적으로 하여 기존 치료법에 비해 높은 효능과 부작용 감소를 실현합니다. 이러한 치료는 대사장애, 심혈관질환, 소화기질환, 감염질환, 암, 희귀유전성질환 등 다양한 치료 영역에 적용되고 있습니다. 전자 건강 기록, AI 기반 임상 의사결정 지원 도구, 실제 증거 플랫폼의 통합은 펩타이드 치료의 개발, 모니터링 및 처방 방법을 재구성하고 있습니다. 분자진단, 맞춤의료, 희귀질환 치료에 대한 접근성을 강화하는 정부 프로그램 및 민관 협력은 성장을 더욱 가속화시키고 있습니다. 생물학에서 영감을 얻은 정밀의료에 대한 수요가 증가하는 가운데, 펩타이드 치료제는 안전성, 특이성, 광범위한 치료 가능성으로 인해 현대 헬스케어의 중요한 솔루션으로 부상하고 있습니다.

시장 범위

개시 연도

2024년

예측 기간

2025-2034년

시작 금액

464억 달러

예측 금액

1,000억 달러

CAGR

8.1%

브랜드 펩타이드 부문은 혁신성, 높은 특이성, 입증된 임상적 효능으로 인해 2024년 69.2%의 점유율을 차지했습니다. 이러한 치료법은 정밀한 타겟팅과 최소한의 오프타겟 효과가 필수적인 복잡하고 만성적인 질환의 치료에 점점 더 선호되고 있습니다. 브랜드 펩타이드는 강력한 R&D 파이프라인, 지속적인 제형 개선, 첨단 전달 메커니즘을 통해 환자의 치료 결과와 치료의 신뢰성을 높이고 있습니다.

비경구 투여 부문은 펩타이드의 낮은 안정성과 낮은 경구 생체 이용률로 인해 정맥, 피하, 근육 내 투여가 선호되는 투여 방법으로 2024년 308억 달러 시장 규모를 형성했습니다. 비경구 투여는 대사 장애, 암, 희귀 내분비 질환 등 중요한 적응증에서 빠른 흡수, 정확한 용량, 높은 효능을 보장합니다.

북미 펩타이드 치료제 시장은 2024년 42.1%의 점유율을 차지했습니다. 이 지역의 성장은 첨단 바이오의약품 인프라, 빠른 규제 승인, 강력한 R&D 투자, 암, 대사성 질환, 희귀질환의 유병률 증가에 힘입어 성장하고 있습니다. 미국, 캐나다 등의 국가에서 브랜드화되고 혁신적인 펩타이드 치료제의 개발은 표적 지향적이고 독성이 낮은 치료법에 대한 수요를 뒷받침하고 있습니다.

세계 펩타이드 치료제 시장의 주요 기업으로는 노보노디스크, 폴리펩타이드 그룹, 리듬 파마슈티컬스, 아스칸디스파마, 자이더스 생명과학, 페링제약, 아스트라제네카, X-GEN 파마슈티컬스, 에릴릴리 릴리, 레퓨리젠, 사노피, 암젠, 브리스톨 마이어스 스퀴브, 펩타드림, 펩타이드 드림, 에릴릴리 릴리, 레퓨리젠 코퍼레이션, 암젠, 사노피, Amgen, Bristol Myers Squibb, 펩타이드드림, 에스티팜, 에이치엘비, 에이치알파, 에이치엘비 Eli Lilly and Company, 레퓨리젠 코퍼레이션, 사노피, 암젠, 브리스톨 마이어스 스퀴브, 펩타이드림, 머크 앤 컴퍼니 등을 꼽을 수 있습니다. 펩타이드 치료제 시장의 기업들은 신규 펩타이드 제제 개발을 위한 R&D 투자, 혁신 가속화를 위한 바이오테크 스타트업과의 협력, 세계 유통을 위한 전략적 제휴 등의 전략을 채택하고 있습니다. 많은 기업들이 고순도 펩타이드 생산 능력을 강화하는 한편, 희귀질환 및 만성질환에 대한 제품 포트폴리오를 확대하는 데 주력하고 있습니다. 시장 진출기업들은 정밀한 의약품 개발, 환자 모니터링, 실제 데이터 수집을 위해 디지털 플랫폼과 AI를 점점 더 많이 활용하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

각 단계 부가가치

밸류체인에 영향을 미치는 요인

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

향후 시장 동향

기술적 상황

현행 기술

신기술

특허 분석

파이프라인 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협력 관계

신제품 발매

확대 계획

제5장 시장 추산·예측 : 유형별, 2021-2034

주요 동향

브랜드 펩타이드

제네릭 펩타이드

제6장 시장 추산·예측 : 용도별, 2021-2034

주요 동향

대사 및 내분비 질환

암

심혈관 질환

소화기계 질환

중추신경계 질환

호흡기 질환

통증 관리

기타 용도

제7장 시장 추산·예측 : 투여 경로별, 2021-2034

주요 동향

주사제

경구

기타 투여 경로

제8장 시장 추산·예측 : 제조업체 유형별, 2021-2034

주요 동향

자사 개발

외부 위탁

제9장 시장 추산·예측 : 합성 기술별, 2021-2034

주요 동향

액상 펩타이드 합성(LPPS)

고상 펩타이드 합성(SPPS)

하이브리드 기술

제10장 시장 추산·예측 : 최종 용도별, 2021-2034

주요 동향

병원 및 진료소

제약 기업 및 바이오테크놀러지 기업

기타 최종 용도

제11장 시장 추산·예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트(UAE)

제12장 기업 개요

Amgen

Ascendis Pharma

AstraZeneca

Bristol-Myers Squibb

Eli Lilly and Company

Ferring Pharmaceuticals

Merck &Co.

Novo Nordisk

PeptiDream

PolyPeptide Group

Repligen Corporation

Rhythm Pharmaceuticals

Sanofi

X-GEN Pharmaceuticals

Zydus Lifesciences

LSH

영문 목차

영문목차

The Global Peptide Therapeutics Market was valued at USD 46.4 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 100 billion by 2034.

The increasing prevalence of chronic and lifestyle-related diseases, including diabetes, cancer, and obesity, is a significant growth driver. Peptide therapeutics, composed of short chains of amino acids, target specific molecular pathways, offering high efficacy and reduced side effects compared to conventional therapies. These treatments are applied across diverse therapeutic areas such as metabolic disorders, cardiovascular diseases, gastrointestinal conditions, infectious diseases, cancer, and rare genetic disorders. The integration of electronic health records, AI-based clinical decision-making tools, and real-world evidence platforms is reshaping the development, monitoring, and prescription of peptide therapies. Government programs and public-private partnerships enhancing access to molecular diagnostics, personalized medicine, and rare disease treatments further accelerate growth. With rising demand for biologically inspired and precision medicines, peptide therapeutics are emerging as critical solutions in modern healthcare due to their safety, specificity, and wide-ranging therapeutic potential.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$46.4 Billion

Forecast Value

$100 Billion

CAGR

8.1%

The branded peptides segment held a 69.2% share in 2024, driven by its strong focus on innovation, high specificity, and proven clinical efficacy. These therapies are increasingly preferred for the treatment of complex and chronic conditions, where precise targeting and minimal off-target effects are essential. Branded peptides benefit from robust research and development pipelines, continuous formulation improvements, and advanced delivery mechanisms, which enhance patient outcomes and therapeutic reliability.

The parenteral segment generated USD 30.8 billion in 2024, owing to the poor stability and low oral bioavailability of peptides, making intravenous, subcutaneous, or intramuscular administration the preferred delivery method. Parenteral delivery ensures rapid absorption, accurate dosing, and high efficacy for critical indications such as metabolic disorders, cancer, and rare endocrine conditions.

North America Peptide Therapeutics Market held a 42.1% share in 2024. Growth in the region is fueled by advanced biopharmaceutical infrastructure, early regulatory approvals, strong R&D investments, and the rising prevalence of cancer, metabolic disorders, and rare diseases. The development of branded and innovative peptide therapies in countries like the U.S. and Canada supports demand for targeted, low-toxicity treatments.

Key players in the Global Peptide Therapeutics Market include Novo Nordisk, PolyPeptide Group, Rhythm Pharmaceuticals, Ascendis Pharma, Zydus Lifesciences, Ferring Pharmaceuticals, AstraZeneca, X-GEN Pharmaceuticals, Eli Lilly and Company, Repligen Corporation, Sanofi, Amgen, Bristol-Myers Squibb, PeptiDream, and Merck & Co. Companies in the Peptide Therapeutics Market are adopting strategies such as investing in research and development to create novel peptide formulations, collaborating with biotech startups to accelerate innovation, and forming strategic alliances for global distribution. Many firms focus on expanding their product portfolios to cover rare and chronic diseases while enhancing manufacturing capabilities for high-purity peptides. Market participants are increasingly leveraging digital platforms and AI for precision drug development, patient monitoring, and real-world data collection.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumption and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Type trends

2.2.3 Application trends

2.2.4 Route of administration trends

2.2.5 Manufacturer type trends

2.2.6 Synthesis technology trends

2.2.7 End use trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Value addition at each stage

3.1.3 Factor affecting the value chain

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing prevalence of cancer

3.2.1.2 Rising incidences of metabolic & endocrine disorders

3.2.1.3 Increasing investments in research and development of novel drugs

3.2.1.4 Technological advancement in peptide therapeutics

3.2.2 Industry pitfalls and challenges

3.2.2.1 Stringent regulatory requirements for drug approval

3.2.2.2 High cost for drug development

3.2.3 Market opportunities

3.2.3.1 Innovation in peptide-drug conjugates and radiolabelled peptides

3.2.3.2 Expansion of oral and long-acting peptide formulations

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East and Africa

3.5 Future market trends

3.6 Technological landscape

3.6.1 Current technologies

3.6.2 Emerging technologies

3.7 Patent analysis

3.8 Pipeline analysis

3.9 Porter's analysis

3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Merger and acquisition

4.6.2 Partnership and collaboration

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

5.1 Key trends

5.2 Branded peptides

5.3 Generic peptides

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

6.1 Key trends

6.2 Metabolic & endocrine disorders

6.3 Cancer

6.4 Cardiovascular disorders

6.5 Gastrointestinal disorders

6.6 Central nervous system disorders

6.7 Respiratory disorders

6.8 Pain management

6.9 Other applications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

7.1 Key trends

7.2 Parenteral

7.3 Oral

7.4 Other route of administration

Chapter 8 Market Estimates and Forecast, By Manufacturer Type, 2021 - 2034 ($ Mn)

8.1 Key trends

8.2 In-house

8.3 Outsourced

Chapter 9 Market Estimates and Forecast, By Synthesis Technology, 2021 - 2034 ($ Mn)

9.1 Key trends

9.2 Liquid phase peptide synthesis (LPPS)

9.3 Solid phase peptide synthesis (SPPS)

9.4 Hybrid technology

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

10.1 Key trends

10.2 Hospitals and clinics

10.3 Pharmaceutical and biotechnology companies

10.4 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)