VaaP(Vehicle-as-a-Platform) 하드웨어 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

Vehicle-as-a-Platform Hardware Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871245

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

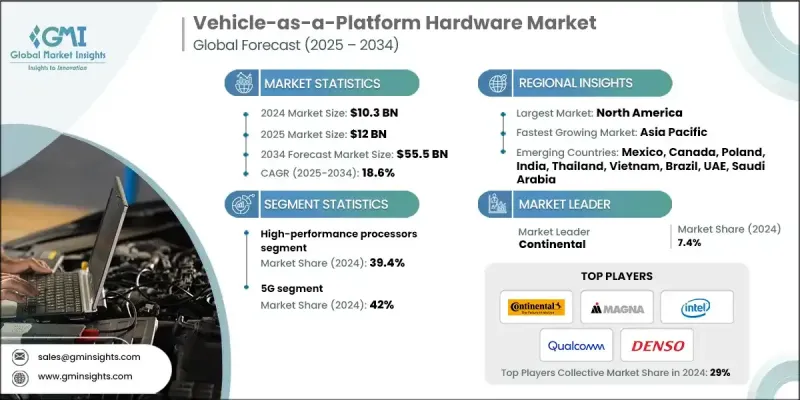

세계의 VaaP(Vehicle-as-a-Platform) 하드웨어 시장은 2024년 103억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 18.6%로 성장해 555억 달러에 달할 것으로 예측되고 있습니다.

자동차 업계는 변화하는 사용자의 기대에 부응하기 위해 설계된 지능형 플랫폼으로 차량이 진화하면서 큰 기술적 변화를 이루고 있습니다. VaaP(Vehicle-as-a-Platform) 하드웨어는 인포테인먼트, 차량 커넥티비티, ADAS(첨단 운전 지원 시스템)등의 첨단 시스템을 실현하는 것으로, 드라이버와 승객의 체험 향상에 중심적인 역할을 하고 있습니다. 도로의 안전성이 긴급한 과제가 되는 가운데, 레이더, 라이더, 초음파 센서, 카메라를 갖춘 ADAS(첨단 운전 지원 시스템)의 통합은 차선, 신호기, 주변 물체에 대한 정확한 감시를 확보합니다. 연결성과 지능화 기능에 대한 소비자의 관심이 높아짐에 따라 OEM 제조업체 및 애프터마켓 공급업체는 편안함, 안전성 및 편의성을 향상시키는 통합 솔루션 제공을 추진하고 있습니다. 확대를 계속하는 자율주행차의 정세는 새로운 투자 기회를 창출하고 있으며, 커넥티드카에 대한 수요 증가가 시장의 기세를 더욱 가속화하고 있습니다. 차량 간, 인프라 및 클라우드 플랫폼 간의 원활한 통신을 실현하기 위해 제조업체는 초고속 데이터 처리, 보안 연결성, 효율적인 엣지 컴퓨팅 기능을 지원할 수 있는 고성능 하드웨어 시스템 개발에 주력하고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

시작 금액

103억 달러

예측 금액

555억 달러

CAGR

18.6%

고성능 프로세서 부문은 인공지능 워크로드를 처리하고 차량 시스템 전체에서 안전하고 집중적인 처리를 보장하는 능력으로 2024년에 39.4%의 점유율을 차지했습니다. 이러한 프로세서는 카메라, 센서, LiDAR 기술에 의해 생성된 엄청난 데이터 흐름을 관리하여 차량이 정밀하고 실시간 운전 판단을 할 수 있도록 합니다. 복잡한 알고리즘을 순간적으로 실행하는 능력은 특히 업계가 고급 자동화 수준으로 전환하는 동안 자동 운전 기능과 고급 차량 조작에 필수적입니다.

5G 하드웨어 분야는 상용차와 승용차 모두에 빠르게 통합된 결과, 2024년에는 42%의 점유율을 차지했습니다. 자동차 제조업체는 저지연 5G 컴포넌트를 차량 컴퓨팅 아키텍처에 통합하여 실시간 통신, 무선 시스템 업데이트 및 클라우드 지원 인텔리전스를 실현합니다. 이러한 전환으로 네트워크 지연을 최소화하면서 연결된 자동 운전 차량이 고급 센서 퓨전과 의사 결정을 수행할 수 있습니다. 차량에는 여러 모듈, 센서, 제어 장치를 원활하게 연동시키는 내장 Wi-Fi 메쉬 하드웨어가 설계되는 경우가 증가하고 있습니다.

미국의 Vaas(Vehicle-as-a-Platform) 하드웨어 시장은 2024년 29억 1,000만 달러 규모에 이를 전망입니다. 미국은 첨단 연구 인프라와 기술 기업과 OEM 간의 강력한 협력에 힘입어 자동차 하드웨어 혁신의 기반이 되고 있습니다. 인공지능, 고성능 컴퓨팅, 센서 기술의 지속적인 발전으로 미국은 스마트 차량 개발의 세계 리더로서의 지위를 확립하고 있습니다. 국내 시장에서는 실시간 데이터 처리와 완전 자율 운전 기능을 제공하는 도메인 컨트롤러, 존 아키텍처 및 칩렛 기반 시스템 온칩(SoC)의 통합이 큰 이점을 제공합니다.

세계의 VaaP(Vehicle-as-a-Platform) 하드웨어 시장을 견인하는 주요 기업으로는 Bosch, Denso, Texas Instruments, NVIDIA, Continental, Intel, Renesas Electronics, Qualcomm Technologies, Magna International 등이 있습니다. 이 시장의 리더 기업은 경쟁 우위를 강화하기 위해 혁신 주도의 성장 전략을 적극적으로 추진하고 있습니다. 각 회사는 AI 기반의 자율주행과 고급 연결성을 지원하는 확장 가능하고 에너지 효율적인 하드웨어 시스템 개발을 위해 연구 개발에 많은 투자를 하고 있습니다. 자동차 제조업체, 반도체 제조업체, 소프트웨어 개발자와의 전략적 제휴와 장기적인 파트너십은 신제품의 신속한 투입과 상용화의 가속에 기여하고 있습니다. 많은 기업들이 인수합병 및 지역 전개를 통해 생산 능력과 세계한 존재감을 확대하고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝의 출처

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정에서의 주요 동향

1차 조사 및 검증

1차 정보

예측

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

ADAS(첨단 운전 지원 시스템)의 보급 확대

자율주행차에 대한 유리한 정부정책

고급 인포테인먼트 시스템에 대한 소비자의 관심 증가

커넥티드 차량 생태계

업계의 잠재적 위험 및 과제

사이버 보안 및 데이터 프라이버시에 대한 우려 사항

고급 하드웨어 컴포넌트의 고비용

시장 기회

전기자동차(EV) 성장

MaaS(Mobility-as-a-Service) 확대

AI 및 엣지 컴퓨팅 진전

5G 및 V2X 통신 출현

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현행 기술

신흥기술

가격 동향

지역별

제품별

생산 통계

생산 거점

소비 허브

수출과 수입

코스트 내역 분석

특허 분석

지속가능성과 환경면

지속가능한 실천

폐기물 감축 전략

생산에 있어서의 에너지 효율화

환경에 배려한 대처

탄소발자국에 관한 고려 사항

시장 진입·확대 전략

신규 시장 진입 모델

지역 확대 로드맵

투자환경과 시장 기회

투자 생태계 개관과 시장 역학

벤처 캐피탈 및 프라이빗 주식 활동 분석

전략적 투자 기회와 우선순위

시장 진출 전략과 타이밍 분석

파트너십 및 협업 기회 매핑

전략적 실시·실행 로드맵

전략적 시장 진입 및 포지셔닝 전략

기술 투자 우선순위와 배분

파트너십 및 생태계 구축 전략

리스크 경감과 긴급시 대응 계획의 틀

실시 스케줄 및 마일스톤 계획

디지털 전환과 혁신 생태계

디지털 전환 전략과 로드맵

혁신 관리 및 개발 프로세스

기술 스카우팅 및 신흥 트렌드 분석

스타트업 에코시스템과 파트너십의 기회

오픈 이노베이션 및 협업 플랫폼

고객 경험과 시장 도입

고객 여정 매핑과 체험 설계

시장 침투 패턴과 행동 분석

고객 세분화 및 타겟팅 전략

가치 제안의 개발과 전달

고객 의사결정 프로세스 분석

리스크 관리와 사업 계속

종합적인 리스크 평가와 특정

리스크 분류 및 우선순위화 프레임워크

리스크 경감 전략과 실시

사업 계속 계획과 준비 체제

공급망 리스크 관리 및 탄력성

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 컴포넌트별, 2021-2034년

주요 동향

고성능 프로세서

GPU

엣지 컴퓨팅 모듈

센서

카메라

LiDAR

RADAR

텔레매틱스 기기

기타

제6장 시장 추계 및 예측 : 접속 방식별, 2021-2034년

주요 동향

5G

Wi-Fi

V2X

위성 통신 시스템

제7장 시장 추계 및 예측 : 인터페이스별, 2021-2034년

주요 동향

전자제어유닛(ECU)

포트

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

주요 동향

승용차

세단

해치백

SUV

상용차

LCV

MCV

HCV

전기자동차

BEV

PHEV

연료전지 자동차(FCEV)

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

러시아

폴란드

아시아태평양

중국

인도

일본

한국

ANZ

베트남

태국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

글로벌 기업

NVIDIA

Qualcomm Technologies

Intel

Mobileye(Intel Company)

Bosch

Infineon Technologies

STMicroelectronics

Texas Instruments

지역 기업

Continental

Denso

Aptiv

Visteon

Magna International

ZF Friedrichshafen

Valeo

Hyundai Mobis

Panasonic Automotive Systems

신흥 기업

Horizon Robotics

Black Sesame Technologies

Hailo Technologies

Ambarella

Renesas Electronics

NXP Semiconductors

Xilinx(AMD Company)

Arm

JHS

영문 목차

영문목차

The Global Vehicle-as-a-Platform Hardware Market was valued at USD 10.3 Billion in 2024 and is estimated to grow at a CAGR of 18.6% to reach USD 55.5 Billion by 2034.

The automotive sector is undergoing a major technological transformation as vehicles evolve into intelligent platforms designed to meet changing user expectations. Vehicle-as-a-platform hardware plays a central role in enhancing driver and passenger experiences by enabling advanced systems such as infotainment, vehicle connectivity, and driver assistance technologies. As road safety becomes an urgent priority, the integration of advanced driver assistance systems (ADAS) featuring radar, lidar, ultrasonic sensors, and cameras ensures accurate monitoring of lanes, traffic signals, and surrounding objects. The increasing consumer interest in connected and intelligent features is driving OEMs and aftermarket suppliers to deliver integrated solutions that improve comfort, safety, and convenience. The expanding autonomous vehicle landscape is creating new opportunities for investment, while growing demand for connected cars continues to propel market momentum. To achieve seamless communication between vehicles, infrastructure, and cloud platforms, manufacturers are focusing on developing high-performance hardware systems capable of supporting ultra-fast data processing, secure connectivity, and efficient edge computing functions.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$10.3 Billion

Forecast Value

$55.5 Billion

CAGR

18.6%

The high-performance processors segment held 39.4% share in 2024, driven by their ability to handle artificial intelligence workloads and ensure secure, centralized processing across vehicle systems. These processors manage massive data flows generated by cameras, sensors, and LiDAR technologies, allowing vehicles to make real-time driving decisions with high precision. Their capacity to execute complex algorithms instantly makes them essential for autonomous driving functions and advanced vehicle operations, especially as industry transitions toward higher levels of automation.

The 5G hardware segment held a 42% share in 2024, owing to rapid integration across both commercial and passenger vehicles. Automakers are embedding low-latency 5G components into vehicle compute architectures, enabling real-time communication, over-the-air system updates, and cloud-assisted intelligence. This shift allows connected and self-driving vehicles to perform advanced sensor fusion and decision-making with minimal network delays. Vehicles are increasingly being designed with in-built Wi-Fi mesh hardware that links multiple modules, sensors, and control units for seamless operation.

U.S. Vehicle-as-a-Platform Hardware Market USD 2.91 Billion in 2024. The country remains a hub for automotive hardware innovation, supported by advanced research infrastructure and strong collaborations between technology firms and original equipment manufacturers. Continuous advancements in artificial intelligence, high-performance computing, and sensor technologies have positioned the U.S. as a global leader in smart vehicle development. The domestic market benefits from the integration of domain controllers, zonal architecture, and chiplet-based systems-on-chip (SoCs) that enable real-time data processing and fully autonomous capabilities.

Prominent companies shaping the Global Vehicle-as-a-Platform Hardware Market include Bosch, Denso, Texas Instruments, NVIDIA, Continental, Intel, Renesas Electronics, Qualcomm Technologies, and Magna International. Leading companies in the Vehicle-as-a-Platform Hardware Market are actively pursuing innovation-driven growth strategies to strengthen their competitive edge. Firms are channeling significant investments into research and development to create scalable, energy-efficient hardware systems capable of supporting AI-based autonomous driving and advanced connectivity. Strategic collaborations and long-term partnerships with automakers, semiconductor producers, and software developers are helping them accelerate new product launches and achieve faster commercialization. Many players are expanding their production capabilities and global presence through mergers, acquisitions, and regional expansion.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Connectivity

2.2.4 Interface

2.2.5 End use

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Supplier landscape

3.2.1 Profit margin

3.2.2 Cost structure

3.2.3 Value addition at each stage

3.2.4 Factor affecting the value chain

3.2.5 Disruptions

3.3 Industry impact forces

3.3.1 Growth drivers

3.3.1.1 Growing adoption of Advanced Driver Assistance Systems (ADAS)

3.3.1.2 Favorable Government Policies for Autonomous Vehicles

3.3.1.3 Increasing Consumer Interest in Advanced Infotainment Systems