연료전지 전기자동차 파워트레인 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)

Fuel Cell Electric Vehicle (FCEV) Powertrain Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871219

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

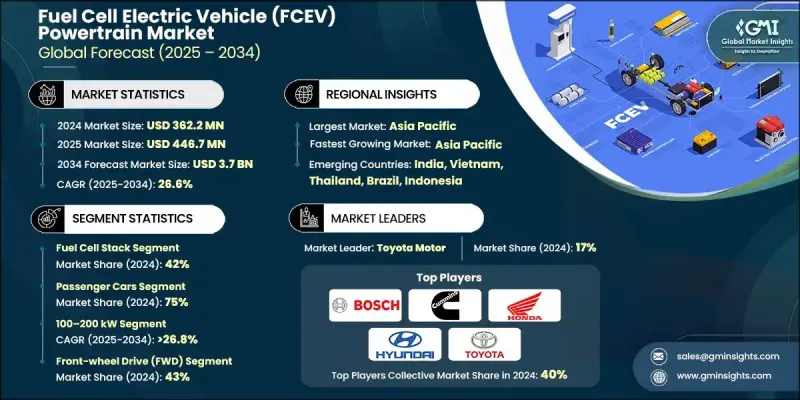

세계 연료전지 전기자동차 파워트레인 시장은 2024년 3억 6,220만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 26.6%로 성장해 37억 달러에 이를 것으로 예측됩니다.

이 시장은 급속한 기술 진보에 견인되고 있으며, 자동차 제조업체는 보다 효율적이고 컴팩트하고 확장 가능한 차세대 연료전지 시스템을 도입하고 있습니다. 최근의 동향에서는 승용차, 상용차, 고정식 용도에 통합이 가능한 모듈 설계가 중시되어 성능과 제조 효율이 모두 향상되고 있습니다. 촉매 기술의 개선과 귀금속 사용량의 감소로 시스템 비용이 저하되는 반면, 수소 인프라에 대한 정부 지원과 자금 제공은 시장 보급을 가속화하고 있습니다. 자동화 생산 기술과 롤 투 롤 제조 공정은 연료전지 부품의 생산을 변화시켜 일관성과 효율성을 향상시킵니다. 고출력 밀도와 고급 시스템에 최적화된 통합은 특히 수소 이동성 및 청정 에너지 정책에 투자하는 지역에서 채택을 더욱 촉진하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

3억 6,220만 달러

예측 금액

37억 달러

CAGR

26.6%

2024년, 승용차 부문은 75%의 점유율을 차지했고 2025년부터 2034년에 걸쳐 CAGR 27.1%를 보일 것으로 예측됩니다. 이 부문은 모델 라인업 확충, 인프라 확대, 효율성, 항속 거리, 급유 속도를 향상시키는 기술 진보의 혜택을 받고 있습니다. 고급차 및 프리미엄 모델에서는 진화하는 에너지 관리 기준과 소비자의 기대에 부응하기 위해 모듈형 연료전지 파워트레인의 채택이 확대되고 있습니다.

100-200kW 파워트레인 부문은 2024년에 1억 5,010만 달러 시장 규모를 기록했고 중형 상용차, 고급 승용차, 소형 상용 유닛에 대한 적응성으로 성장이 전망됩니다. 표준화된 설계와 규모의 경제성으로 인해 이 출력대는 범용성을 발휘하여 주류 용도에 고성능, 비용 효율적, 효과적인 패키징을 제공합니다.

아시아태평양의 연료전지 전기자동차 파워트레인 시장은 정부 지원 정책, 수소 인프라 투자, 자동차 제조업체의 노력을 배경으로 2024년 46%의 점유율을 차지했습니다. 현지 생산 증가, R&D 투자, 자동차 제조업체와 에너지 공급업체간의 제휴로 견고한 수소 생태계가 성장하고 있습니다. 이 지역 최대 시장인 중국은 함대의 전동화 이니셔티브와 FCEV 도입에 대한 정부 우대 조치의 혜택을 받고 있으며, 상업 및 물류 부문 수요 증가가 성장을 더욱 뒷받침하고 있습니다.

세계의 연료전지자동차(FCEV) 파워트레인 시장에서 사업을 전개하고 있는 주요 기업으로는 니콜라, 혼다, 발라드 파워, 파워셀, 도요타 자동차, 보쉬, 커민스, 제너럴 모터스, 플러그 파워, 현대 자동차 등이 있습니다. 각 사는 연료전지의 효율, 내구성, 출력밀도를 높이기 위해 연구개발에 많은 투자를 하고 그 지위를 강화하고 있습니다. 에너지 공급업체, 정부 기관 및 자동차 제조업체와의 전략적 제휴는 수소 연료 공급 네트워크와 공급망 구축에 기여하고 있습니다. 각 회사는 여러 차량 부문에 대한 모듈식 확장 가능한 파워트레인을 도입하여 승용차, 상용차 및 산업 용도를 포함한 포트폴리오를 확대하고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정에서의 주요 동향

1차 조사 및 검증

1차 정보

예측 모델

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

정부 인센티브 및 제로 방출 규제

수소 제조 및 충전 인프라의 진전

연료전지 비용의 저하와 효율의 향상

장거리·대형 수송 솔루션에 대한 수요 증가

자동차 제조업체와 에너지 기업과의 제휴

업계의 잠재적 위험 및 과제

수소 생산 및 저장 비용의 높이

수소 연료 보급 인프라의 부족

시장 기회

그린 수소 생산 확대

수소 인프라 개발 파트너십

연료전지 부품의 기술 혁신

재생에너지 시스템과의 통합

성장 가능성 분석

규제 상황

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

PEM 연료전지 기술의 성숙도

수소 저장 기술의 현상

플랜트 전체의 최적화

통합 및 제어 시스템

신흥기술

고체 연료전지

첨단 막 기술

차세대 스토리지 솔루션

AI를 활용한 시스템 최적화

가격 동향

부품 레벨에서의 가격 분석

시스템 레벨의 가격 동향

지역별 가격 변동

가격 전략 분석

가치 기반 가격 설정 모델

경쟁력 있는 가격 전략

수량 할인 체계

생산 통계 및 제조 분석

세계 생산 개요

제조 능력 분석

생산기술평가

공급망 제조

코스트 내역 분석

연료전지 스택의 비용구조

플랜트 관련 설비 비용 분석

조립·통합 비용

총소유비용분석

특허 분석

특허 정세의 개요

주요기술특허

지적재산 라이선싱 전략

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

R&D 투자 분석

세계 연구개발 지출 동향

기업의 연구개발(R&D) 이니셔티브

정부 조사 프로그램

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협력관계

신제품 발매

확대계획과 자금조달

제5장 시장 추정 및 예측 : 컴포넌트별, 2021년-2034년

주요 동향

연료전지 스택

수소 저장 탱크

전기 모터

파워 컨트롤 유닛(PCU)

배터리 시스템

공기 압축기 및 가습기

제6장 시장 추정 및 예측 : 차량별, 2021년-2034년

주요 동향

승용차

해치백 자동차

세단

SUV

상용차

소형 상용차

중형 상용차

대형 상용차

제7장 시장 추정 및 예측 : 출력별, 2021년-2034년

주요 동향

100kW 미만

100-200kW

200kW 이상

제8장 시장 추정 및 예측 : 구동별, 2021년-2034년

주요 동향

전륜 구동(FWD)

후륜 구동(RWD)

전륜 구동(AWD)

제9장 시장 추정 및 예측 : 주행 거리별, 2021년-2034년

주요 동향

400km 미만

400-600km

600킬로미터 이상

제10장 시장 추정 및 예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

포르투갈

크로아티아

아시아태평양

중국

인도

일본

호주

한국

싱가포르

태국

인도네시아

베트남

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

튀르키예

제11장 기업 프로파일

Major fuel cell powertrain manufacturers

Ballard Power

Bloom Energy

Bosch

Cummins

Honda Motor

Horizon Fuel Cell Technologies

Hyundai Motor

Intelligent Energy

ITM Power

Plug Power

SFC Energy

Toyota Motor

Weichai Power

General Motor

Component and technology suppliers

Aisin

Denso

Mahle

Mitsubishi Heavy

PowerCell

Schaeffler

Toshiba Energy

Emerging and innovative fuel cell companies

GenCell Energy

Hydrogenious

Hyster-Yale

Nikola

Nuvera Fuel

SHW

영문 목차

영문목차

The Global Fuel Cell Electric Vehicle (FCEV) Powertrain Market was valued at USD 362.2 million in 2024 and is estimated to grow at a CAGR of 26.6% to reach USD 3.7 Billion by 2034.

The market is being driven by rapid technological advancements, with automakers introducing next-generation fuel cell systems that are more efficient, compact, and scalable. Recent developments emphasize modular designs that can be integrated into passenger vehicles, commercial fleets, and stationary applications, enhancing both performance and manufacturing efficiency. Improvements in catalyst technology, along with reduced use of precious metals, have lowered system costs, while government support and funding for hydrogen infrastructure have accelerated market adoption. Automated production techniques and roll-to-roll manufacturing processes are transforming fuel cell component production, ensuring better consistency and efficiency. High power density and optimized integration in advanced systems have further enhanced adoption, particularly in regions investing in hydrogen mobility and clean energy policies.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$362.2 Million

Forecast Value

$3.7 Billion

CAGR

26.6%

In 2024, the passenger cars segment held a 75% share and is expected to grow at a CAGR of 27.1% from 2025 to 2034. The segment benefits from increased model availability, infrastructure expansion, and technological advances that improve efficiency, range, and refueling speed. Luxury and premium models increasingly utilize modular fuel cell powertrains to meet evolving energy management standards and consumer expectations.

The 100-200 kW powertrain segment generated USD 150.1 million in 2024 and is poised to grow owing to its suitability for medium-duty commercial vehicles, luxury passenger cars, and smaller commercial units. Standardized designs and economies of scale make this range versatile, offering high performance, cost-efficiency, and effective packaging for mainstream applications.

Asia Pacific Fuel Cell Electric Vehicle (FCEV) Powertrain Market held 46% share in 2024, driven by supportive government policies, investments in hydrogen infrastructure, and automaker initiatives. Increased local production, R&D investment, and partnerships between automakers and energy providers are fostering a robust hydrogen ecosystem. China, the largest market in the region, is benefiting from fleet electrification initiatives and government incentives for FCEV adoption, with rising demand in commercial and logistics sectors further boosting growth.

Key players operating in the Global Fuel Cell Electric Vehicle (FCEV) Powertrain Market include Nikola, Honda Motor, Ballard Power, PowerCell, Toyota Motor, Bosch, Cummins, General Motors, Plug Power, and Hyundai Motor. Companies are strengthening their position by investing heavily in research and development to enhance fuel cell efficiency, durability, and power density. Strategic partnerships with energy providers, government agencies, and automotive manufacturers are helping build hydrogen refueling networks and supply chains. Firms are introducing modular and scalable powertrains for multiple vehicle segments, expanding their portfolio to include passenger, commercial, and industrial applications.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Vehicle

2.2.4 Power Output

2.2.5 Drive

2.2.6 Range

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1.1 Growth drivers

3.2.1.2 Government incentives and zero-emission regulations

3.2.1.3 Advancements in hydrogen production and refueling infrastructure

3.2.1.4 Declining fuel cell costs and improved efficiency

3.2.1.5 Rising demand for long-range and heavy-duty mobility solutions

3.2.1.6 Collaboration between automakers and energy companies

3.2.2 Industry pitfalls and challenges

3.2.2.1 High hydrogen production and storage costs

3.2.2.2 Limited hydrogen refueling infrastructure

3.2.3 Market opportunities

3.2.3.1 Green hydrogen production expansion

3.2.3.2 Hydrogen infrastructure development partnerships

3.2.3.3 Technological innovation in fuel cell components

3.2.3.4 Integration with renewable energy systems

3.3 Growth potential analysis

3.4 Regulatory landscape

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.1.1 PEM fuel cell technology maturity

3.7.1.2 Hydrogen storage technology status

3.7.1.3 Balance of plant optimization

3.7.1.4 Integration and control systems

3.7.2 Emerging technologies

3.7.2.1 Solid-state fuel cells

3.7.2.2 Advanced membrane technologies

3.7.2.3 Next-generation storage solutions

3.7.2.4 AI-driven system optimization

3.8 Price trends

3.8.1 Component-level pricing analysis

3.8.2 System-level pricing trends

3.8.3 Regional price variations

3.9 Pricing strategy analysis

3.9.1 Value-based pricing models

3.9.2 Competitive pricing strategies

3.9.3 Volume discount structures

3.10 Production statistics and manufacturing analysis