자동차 데이터 로깅 및 애널리틱스 하드웨어 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)

Automotive Data Logging and Analytics Hardware Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871180

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

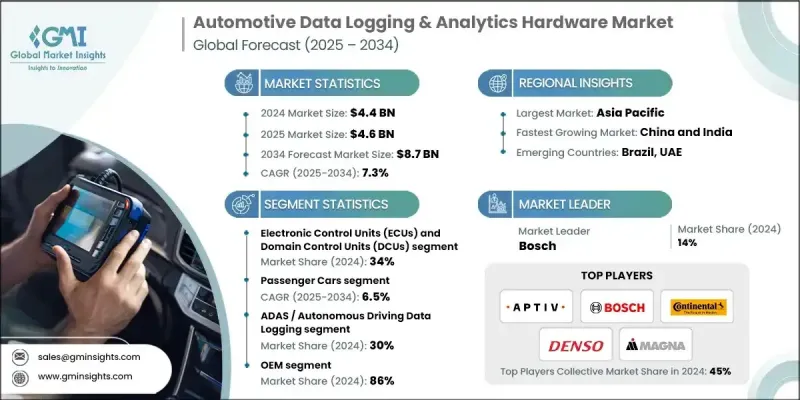

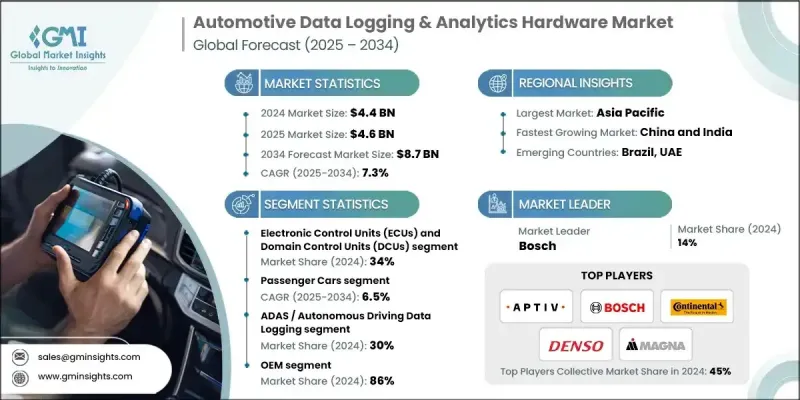

세계의 자동차 데이터 로깅 및 애널리틱스 하드웨어 시장은 2024년 44억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 7.3%로 성장해 87억 달러에 이를 것으로 예측되고 있습니다.

자동차 산업은 차량의 전동화, 자동화, 커넥티드 모빌리티의 진전에 의해 근본적인 변화를 맞이하고 있습니다. 이러한 진화의 핵심은 성능 향상, 컴플라이언스 확보, 차량 안전 향상에 필수적인 데이터 로깅 및 분석 하드웨어에 대한 의존도가 높아집니다. 세계 각국의 정부는 투명성과 추적성을 확보하기 위해 차량에 데이터 로깅 시스템을 설치할 것을 의무화하는 보다 엄격한 규제를 실시했습니다. 소프트웨어 정의 차량(SDV)으로의 전환은 무선 업데이트(OTA), 라이프사이클 관리, 실시간 원격 측정을 지원할 수 있는 하드웨어에 대한 수요를 재구성합니다. UNECE 규칙 R155 및 R156 등 국제 안전 및 사이버 보안 표준을 준수하는 것은 자동차 제조업체에 안전하고 고성능 데이터 기록 플랫폼을 채택하고 있습니다. 현대 차량의 AI와 엣지 컴퓨팅의 급속한 보급으로 센서 생성 데이터의 로컬 처리가 가속화되고 있습니다. 첨단 데이터 로깅 시스템은 하루에 테라바이트 규모의 정보를 수집하면서 1.2GB/s 이상의 네트워크 처리량을 유지하고 30개 이상의 채널간에 정밀한 동기화를 실현해야 하며, 자동차 생태계의 중요성이 더욱 높아지고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

시작 금액

44억 달러

예측 금액

87억 달러

CAGR

7.3%

전자제어장치(ECU) 및 도메인 제어 유닛(DCU) 부문은 2024년 34%의 점유율을 차지했습니다. 자동차 설계는 분산형 ECU에서 중앙 집중식 도메인 아키텍처로 전환하고 있으며, 이를 통해 데이터 로깅 기능의 고급 통합이 가능합니다. 이러한 시스템은 여러 통신 프로토콜을 관리하고 데이터 보호를 보장하며 정보를 신속하게 처리해야 합니다. 세계 기준을 기반으로 하는 사이버 보안 프레임워크의 채택은 데이터 무결성을 보장하기 위해 보안 하드웨어 모듈, 변조 방지 로깅 및 인증된 시스템 부팅을 갖춘 ECU의 도입을 촉진합니다.

ADAS와 자율주행 데이터 로깅 분야는 2024년 30%의 점유율을 차지했습니다. 차세대 차량의 고급 센서와 실시간 컴퓨팅의 통합이 진행됨에 따라 정교한 데이터 로깅 솔루션에 대한 수요가 가속화되고 있습니다. 자율주행 및 준자율주행 기술의 지속적인 진화에 따라 레이더, LiDAR, 카메라 시스템을 동시에 커버하는 고속 멀티채널 데이터 캡처가 필수적입니다. 이를 통해 자율주행 알고리즘의 정확한 분석과 검증이 가능해 차량의 안전성과 자율성의 지속적인 혁신을 지원하고 있습니다.

중국의 자동차 데이터 로깅 및 애널리틱스 하드웨어 시장은 2024년에 큰 점유율을 창출했습니다. 이는 일본의 광범위한 자동차 생산 기반과 지능적인 연결성에 대한 강한 중점화 때문입니다. 정부 주도의 이니셔티브는 지능적이고 연결된 차량 기술을 촉진하고 실시간 차량 데이터 수집 및 중앙 집중식 관리 기준을 강화하고 있습니다. 국가 지능화 차량 개발 전략에 근거한 정책은 첨단 로깅 하드웨어의 도입을 가속화하고, 플릿 전체에서 안전 컴플라이언스, 자동화, 데이터 추적성을 확보하고 있습니다.

세계의 자동차 데이터 로깅 및 애널리틱스 하드웨어 시장을 견인하는 주요 기업으로는 Continental, Denso, ZF Friedrichshafen, Aptiv, Hyundai Mobis, Lear, Bosch, Magna, Valeo, Vector Informatik 등이 있습니다. 이 시장의 리더 기업은 시장 지위 강화를 위해 혁신, 파트너십, 제품 다양화에 주력하고 있습니다. 많은 기업들이 자율주행차와 커넥티드카가 생성하는 복잡한 데이터 스트림을 관리할 수 있는 고속 AI 대응 하드웨어 솔루션의 개발에 투자하고 있습니다. 자동차 제조업체와 기술 제공업체와의 전략적 제휴로 실시간 분석, 사이버 보안, 에지 프로세싱의 진보가 촉진되고 있습니다. 또한 진화하는 소프트웨어 정의 차량 아키텍처에 대응하는 모듈식으로 확장 가능한 하드웨어를 설계하기 위해 연구 개발 능력을 강화하기 위해 노력하고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝의 출처

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정에서의 주요 동향

1차 조사 및 검증

1차 정보

예측

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

ADAS 및 자율주행 시스템 채용 확대

전기자동차(EV) 및 배터리 관리 시스템 확대

확대하는 플릿의 디지털화와 예지 보전

소프트웨어 정의 차량(SDV)의 도입 상황

업계의 잠재적 위험 및 과제

고급 로깅 하드웨어의 높은 비용

하드웨어와 소프트웨어의 통합에 있어서의 복잡성

시장 기회

커넥티드카 인프라의 확충

애프터마켓용 개조 솔루션의 성장

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 분석

지속가능성과 환경면

탄소발자국 평가

순환형 경제로의 통합

전자폐기물 관리 요건

그린 제조 이니셔티브

이용 사례와 응용 분야

최상의 시나리오

가격 분석 및 동향

과거의 가격 추이(2019-2024년)

부품 가격 상승의 영향

반도체 부족에 의한 비용 영향

수량별 가격 설정 전략

지역별 가격 변동

미래의 가격 예측(2025-2034년)

세계 무역 분석

수입 및 수출 수량 및 금액 분석

주요 수출국

주요 수입 시장

무역 흐름의 패턴과 의존 관계

관세 영향 분석

공급망 혼란의 영향

원재료 및 부품 분석

반도체 재료의 필요량

희토류 원소에 대한 의존도

플라스틱 및 금속 케이스 재료

배터리 및 전력 관리 부품

재료 가격 변동의 영향

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병

제휴 및 협력관계

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 컴포넌트별, 2021-2034년

주요 동향

전자제어장치(ECU) 및 도메인 제어 유닛(DCU)

텔레매틱스 제어 유닛(TCU) 및 커넥티비티 하드웨어

센서 인터페이스 및 데이터 수집 하드웨어

게이트웨이 및 네트워크 하드웨어

기타

제6장 시장 추계 및 예측 : 차량별, 2021-2034년

주요 동향

승용차

해치백

세단

SUV

상용차

소형 상용차(LCV)

중형 상용차(MCV)

대형 상용차(HCV)

제7장 시장 추계 및 예측 : 용도별, 2021-2034년

주요 동향

ADAS 및 자동 운전 데이터 기록

플릿 관리 및 텔레매틱스

전기자동차 배터리 관리 시스템

소프트웨어 정의 차량(SDV) 지원

기타

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

주요 동향

OEM

애프터마켓

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

러시아

아시아태평양

중국

인도

일본

호주

한국

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

세계 기업

Aptiv

Bosch

Continental

Denso

Harman International(Samsung)

Lear

Magna

Panasonic Automotive Systems

Valeo

ZF Friedrichshafen

지역 기업

Geotab

Vector Informatik

Verizon Connect

Webfleet Solutions

기술전문기업 및 신흥기업

Intrepid Control Systems

IPETRONIK

National Instruments

Samsara

Spireon

Trimble

아시아 시장 리더

BYD Electronic

Huawei Technologies

Hyundai Mobis

LG Electronics

Pioneer

플릿 관리 스페셜리스트

Azuga

Fleet Complete

Omnitracs

JHS

영문 목차

영문목차

The Global Automotive Data Logging & Analytics Hardware Market was valued at USD 4.4 Billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 8.7 Billion by 2034.

The automotive industry is undergoing a fundamental transformation driven by vehicle electrification, automation, and connected mobility. At the core of this evolution lies the increasing reliance on data logging and analytics hardware, which is essential for enhancing performance, ensuring compliance, and improving vehicle safety. Governments worldwide are enforcing stricter regulations that require data logging systems in vehicles to ensure transparency and traceability. The transition toward software-defined vehicles (SDVs) is reshaping the demand for hardware capable of handling over-the-air updates, lifecycle management, and real-time telemetry. Compliance with global safety and cybersecurity standards, such as UNECE Regulations R155 and R156, is compelling automakers to adopt secure, high-performance data recording platforms. The rapid adoption of AI and edge computing in modern vehicles allows for faster local processing of sensor-generated data. Advanced data logging systems are now expected to capture terabytes of information daily while maintaining network throughput exceeding 1.2 GB/s and precise synchronization across more than 30 channels, reinforcing their critical role in the automotive ecosystem.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$4.4 Billion

Forecast Value

$8.7 Billion

CAGR

7.3%

The Electronic Control Units (ECUs) and Domain Control Units (DCUs) segment held a share of 34% in 2024. Automotive design is increasingly shifting from distributed ECUs to centralized domain architectures that enable advanced integration of data logging features. These systems are required to manage multiple communication protocols, ensure data protection, and process information rapidly. The adoption of cybersecurity frameworks under global standards is encouraging the implementation of ECUs equipped with secure hardware modules, tamper-resistant logging, and authenticated system booting to ensure data integrity.

The ADAS and Autonomous Driving Data Logging segment accounted for a 30% share in 2024. The growing integration of advanced sensors and real-time computing in next-generation vehicles is accelerating demand for sophisticated data logging solutions. The continuous evolution of autonomous and semi-autonomous technologies necessitates high-speed, multi-channel data capture across radar, LiDAR, and camera systems simultaneously. This enables accurate analysis and validation of automated driving algorithms, supporting ongoing innovation in vehicle safety and autonomy.

China Automotive Data Logging & Analytics Hardware Market generated a significant share in 2024, owing to its extensive automotive production base and strong emphasis on intelligent connectivity. Government-led initiatives promoting intelligent and connected vehicle technologies have reinforced standards for real-time vehicle data collection and centralized management. Policies under the national intelligent vehicle development strategy accelerate the deployment of advanced logging hardware, ensuring safety compliance, automation, and data traceability across fleets.

Key companies shaping the Global Automotive Data Logging & Analytics Hardware Market include Continental, Denso, ZF Friedrichshafen, Aptiv, Hyundai Mobis, Lear, Bosch, Magna, Valeo, and Vector Informatik. Leading companies in the Automotive Data Logging & Analytics Hardware Market are focusing on innovation, partnerships, and product diversification to strengthen their market position. Many are investing in developing high-speed, AI-enabled hardware solutions capable of managing complex data streams generated by autonomous and connected vehicles. Strategic collaborations with automakers and technology providers are fostering advancements in real-time analytics, cybersecurity, and edge processing. Companies are also enhancing their R&D capabilities to design modular, scalable hardware compatible with evolving software-defined vehicle architectures.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Vehicle

2.2.4 Application

2.2.5 End Use

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing adoption of ADAS and autonomous driving systems

3.2.1.2 Expansion of electric vehicles (EVs) and battery management systems

3.2.1.3 Growing fleet digitization and predictive maintenance

3.2.1.4 Software-defined vehicle (SDV) adoption

3.2.2 Industry pitfalls and challenges

3.2.2.1 High cost of advanced logging hardware

3.2.2.2 Complexity in hardware-software integration

3.2.3 Market opportunities

3.2.3.1 Expansion of connected vehicle infrastructure