약물유전체학 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Pharmacogenomics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1858967

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 136 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

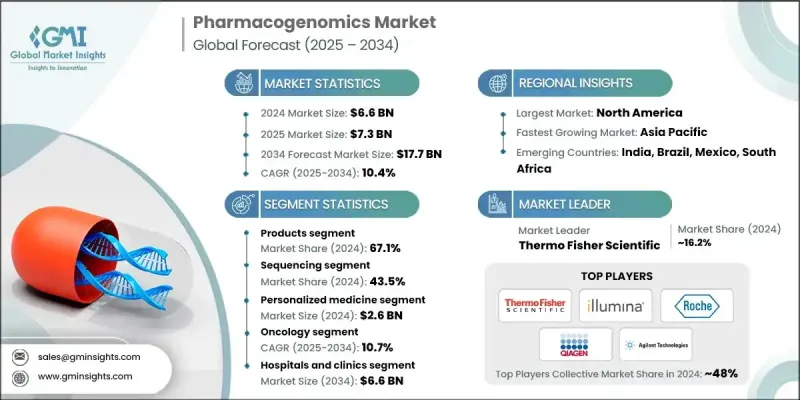

세계의 약물유전체학 시장 규모는 2024년에는 66억 달러로 평가되었고, CAGR 10.4%로 성장할 전망이며, 2034년에는 177억 달러에 이를 것으로 예측되고 있습니다.

꾸준한 성장의 원동력이 되고 있는 것은 표적 치료에 대한 수요 증가 및 유전체 기술의 개발이 진행되고 있다는 것입니다. 세계의 헬스케어 시스템이 보다 맞춤 치료 접근법을 추진하는 동안, 약물유전체 검사는 임상 및 연구 분야에서 널리 채택되고 있습니다. 의사결정에 있어서 유전체학의 역할 확대는 암, 심혈관 질환, 감염증 등의 만성질환의 부담에 의해 더욱 추진되고 있습니다. 약물유전체학은 사람의 유전자 코드가 약물 반응에 어떻게 영향을 미치는지 이해하는 데 중점을 두고 임상의가 안전과 효능을 향상시키기 위해 복용량과 치료 옵션을 미세 조정할 수 있도록 합니다. 디지털 헬스 솔루션으로의 지속적인 시프트는 AI를 활용한 임상 판단 툴과 실세계 데이터 분석의 통합과 함께 이 분야를 계속 진행하고 있습니다. 시장의 진전은 맞춤형 의료를 향한 폭넓은 움직임과 치료 성과를 높이면서 부작용을 줄일 필요성에 직접 연결되어 있습니다.

시장 규모

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

66억 달러

예측 금액

177억 달러

CAGR

10.4%

2024년에는 맞춤형 의료를 지원하는 툴에 대한 수요가 높아짐에 따라 제품 부문이 67.1%의 점유율을 차지했습니다. 이 범주에는 장비, 소모품, 광범위한 유전자 검사 키트 및 시약이 포함되며, 이들은 임상 및 연구에 필수적입니다. 시퀀싱 키트, PCR 기반 시약, 마이크로어레이 및 기타 진단 도구와 같은 하위 부문은 심장병, 종양학, 정신의학, 감염증학 등 다양한 전문 분야에서 널리 사용됩니다. 치료 의사 결정에서 정밀도 주도형 솔루션에 대한 요구가 증가함에 따라 약물유전체 제품에 대한 수요가 계속 밀어지고 있습니다.

맞춤형 의료 분야는 2024년 26억 달러를 창출했습니다. 이러한 급성장의 배경은 고급 유전체 도구에 대한 접근성 확대, 진단 방법 개선, 일상 진료에 대한 데이터 분석의 통합을 포함합니다. 국가적인 유전체학 이니셔티브를 중심으로 한 프로그램은 일상적인 임상 진료에 약물유전체 데이터를 통합하는 것을 장려합니다. 규제기관은 보다 안전한 약물 사용 및 개인화 치료를 가능하게 하는 관련 바이오마커를 승인함으로써 이러한 전환을 지원합니다. 동반진단약이나 AI를 활용한 기술의 이용이 확대됨으로써, 맞춤형 의료는 보다 확장 가능해지고, 널리 받아들여지고 있습니다.

북미의 약물유전체학 시장은 2024년 48.6%의 점유율을 차지했습니다. 미국과 캐나다 시장 확대는 유전체 혁신에 대한 강한 주력, 높은 헬스케어 지출, 고급 디지털 인프라에 의해 지원되고 있습니다. 병원 및 클리닉 전체에서 유전체 검사 및 맞춤형 치료의 도입이 증가하고 있는 것은 유리한 상환 정책에 의해 지원되고 있으며, 임상 현장에 약물유전체 패널의 광범위한 도입에 기여하고 있습니다. 시퀀싱 툴과 AI 대응 진단의 지속적인 발전은 임상 결과를 향상시키고 지역 시장 침투를 촉진합니다.

약물유전체학 시장의 주요 기업은 전략적 연구개발 투자, 제휴 및 제품 다양화를 통해 시장에서의 존재를 확대하고 있습니다. Thermo Fisher Scientific, Agilent Technologies, Illumina 및 Qiagen과 같은 기업들은 보다 빠르고 정확한 유전자 프로파일링을 가능하게 하는 종합적인 키트, 시약 및 시퀀싱 플랫폼 개발에 주력하고 있습니다. 의료 제공자나 연구기관과의 제휴를 통해 이들 기업은 임상 요구에 맞는 맞춤형 솔루션을 공동 개발하고 있습니다. 기술력을 강화하고 지리적 범위를 넓히기 위해 합병과 인수가 진행되고 있습니다. 또한 각 회사는 임상적 타당성과 시장 접근을 보장하기 위해 규제 당국의 승인과 규정 준수에 중점을 두고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

업계에 미치는 영향요인

성장 촉진요인

연구개발 투자 증가

암의 유병률 증가

정밀의료 접근의 채용 증가

부작용 부담 증가

업계의 잠재적 위험 및 과제

비용 및 상환의 과제

유전자 데이터의 복잡성 및 해석

시장 기회

미생물 기반 및 호르몬 표적 치료의 혁신

멀티진 패널 및 동반진단약의 개발

성장 가능성 분석

규제 상황

향후 시장 동향

기술적 상황

현재의 기술

신흥 기술

특허 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

세계

북미

유럽

아시아태평양

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 협력

신제품 발표

확장 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

주요 동향

제품 정보

키트 및 시약

시퀀싱 키트 및 시약

PCR 키트 및 시약

마이크로어레이 키트 및 시약

기타 키트 및 시약

기기 및 소모품

서비스

제6장 시장 추계 및 예측 : 기술별(2021-2034년)

주요 동향

시퀀싱

PCR

마이크로어레이

기타 기술

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

맞춤형 의료

임상 연구

창약 및 전임상 개발

기타 용도

제8장 시장 추계 및 예측 : 질환 영역별(2021-2034년)

주요 동향

암 영역

심혈관 질환

신경질환

감염증

정신 건강

기타 질환 영역

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

주요 동향

병원 및 진료소

학술기관 및 연구기관

제약 및 바이오테크놀러지 기업

연구 수탁 기관(CRO)

기타 최종 사용

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

23andMe

Admera Health

Agilent Technologies

Becton, Dickinson and Company

Bio-Rad Laboratories

Charles River Laboratories

Danaher

Eurofins Scientific

F. Hoffmann-La Roche

Genelex

Genomind

Illumina

Laboratory Corporation of America Holdings

Novogene

OneOme

Qiagen

Revvity

Takara Bio

Thermo Fisher Scientific

AJY

영문 목차

영문목차

The Global Pharmacogenomics Market was valued at USD 6.6 billion in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 17.7 billion by 2034.

The steady growth is fueled by increasing demand for targeted therapies and the ongoing development of genomic technologies. As healthcare systems worldwide push for more personalized treatment approaches, pharmacogenomic testing is seeing wider adoption across clinical and research settings. The expanding role of genomics in decision-making is further propelled by the burden of chronic diseases such as cancer, cardiovascular diseases, and infectious conditions. Pharmacogenomics focuses on understanding how a person's genetic code influences their drug response, allowing clinicians to fine-tune dosages and treatment options for improved safety and efficacy. The ongoing shift toward digital health solutions, combined with the integration of AI-powered clinical decision tools and real-world data analytics, continues to advance the field. The market's progress is directly tied to the broader move toward personalized medicine and the need to reduce adverse drug reactions while enhancing therapeutic outcomes.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$6.6 Billion

Forecast Value

$17.7 Billion

CAGR

10.4%

In 2024, the products segment held a 67.1% share, driven by rising demand for tools supporting personalized care. This category includes instruments, consumables, and a wide range of genetic testing kits and reagents, which are essential for clinical and research use. Subsegments such as sequencing kits, PCR-based reagents, microarrays, and other diagnostic tools are widely used across various specialties, including cardiology, oncology, psychiatry, and infectious diseases. The increasing need for precision-driven solutions in therapeutic decision-making continues to boost demand for pharmacogenomic product offerings.

The personalized medicine segment generated USD 2.6 billion in 2024. Its rapid growth is attributed to the expansion of access to advanced genomic tools, improved diagnostics, and the integration of data analytics into routine care. Programs focused on national genomics initiatives are encouraging the inclusion of pharmacogenomic data into everyday clinical practice. Regulatory bodies are supporting this transition by approving relevant biomarkers that enable safer drug use and individualized therapy. Growing use of companion diagnostics and AI-powered technologies has made personalized medicine more scalable and widely accepted.

North America Pharmacogenomics Market held a 48.6% share in 2024. Market expansion in the U.S. and Canada is supported by a strong focus on genomic innovation, high healthcare expenditure, and advanced digital infrastructure. The increased adoption of genomic testing and personalized treatments across hospitals and clinics has been backed by favorable reimbursement policies, contributing to the widespread implementation of pharmacogenomic panels into clinical practice. Ongoing advancements in sequencing tools and AI-enabled diagnostics are enhancing clinical outcomes and driving regional market penetration.

Leading players in the Pharmacogenomics Market are expanding their market presence through strategic R&D investments, partnerships, and product diversification. Companies such as Thermo Fisher Scientific, Agilent Technologies, Illumina, and Qiagen are focused on developing comprehensive kits, reagents, and sequencing platforms that enable faster and more accurate genetic profiling. Collaborations with healthcare providers and research institutions help these firms co-develop custom solutions tailored to clinical needs. Mergers and acquisitions are being pursued to strengthen technological capabilities and widen geographic reach. Additionally, players are emphasizing regulatory approvals and compliance to ensure clinical relevance and market access.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumption and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Offering trends

2.2.3 Technology trends

2.2.4 Application trends

2.2.5 Disease area trends

2.2.6 End use trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Value addition at each stage

3.1.3 Factor affecting the value chain

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing research and development investments

3.2.1.2 Increasing prevalence of cancer

3.2.1.3 Increasing adoption of precision medicine approaches

3.2.1.4 Rising burden of adverse drug reactions

3.2.2 Industry pitfalls and challenges

3.2.2.1 Cost and reimbursement challenges

3.2.2.2 Complexity and interpretation of genetic data

3.2.3 Market opportunities

3.2.3.1 Innovation in microbiome-based and hormone-targeted therapies

3.2.3.2 Development of multi-gene panels and companion diagnostics

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East and Africa

3.5 Future market trends

3.6 Technological landscape

3.6.1 Current technologies

3.6.2 Emerging technologies

3.7 Patent analysis

3.8 Porter's analysis

3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 Global

4.2.2 North America

4.2.3 Europe

4.2.4 Asia Pacific

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Merger and acquisition

4.6.2 Partnership and collaboration

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Offerings, 2021 - 2034 ($ Mn)

5.1 Key trends

5.2 Products

5.2.1 Kits and reagents

5.2.1.1 Sequencing kits and reagents

5.2.1.2 PCR kits and reagents

5.2.1.3 Microarray kits and reagents

5.2.1.4 Other kits and reagents

5.2.2 Instrument and consumables

5.3 Services

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

6.1 Key trends

6.2 Sequencing

6.3 PCR

6.4 Microarray

6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

7.1 Key trends

7.2 Personalized medicine

7.3 Clinical research

7.4 Drug discovery and preclinical development

7.5 Other applications

Chapter 8 Market Estimates and Forecast, By Disease Area, 2021 - 2034 ($ Mn)

8.1 Key trends

8.2 Oncology

8.3 Cardiovascular diseases

8.4 Neurological diseases

8.5 Infectious diseases

8.6 Mental health

8.7 Other disease areas

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

9.1 Key trends

9.2 Hospitals and clinics

9.3 Academic and research institutions

9.4 Pharmaceutical and biotechnology companies

9.5 Contract research organization (CROs)

9.6 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)