자율주행 열차 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Autonomous Train Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1833651

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 230 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

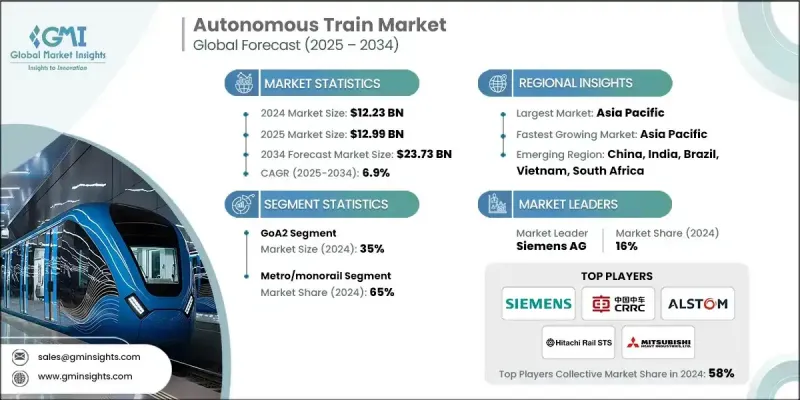

세계의 자율주행 열차 시장 규모는 2024년에 122억 3,000만 달러로 평가되었고, CAGR 6.9%로 성장할 전망이며, 2034년에는 237억 3,000만 달러에 달할 것으로 예측되고 있습니다.

철도 사업자는 운행 효율을 향상시키고 인적 실수를 줄이며, 정확한 스케줄링을 가능하게 하기 위해 자율주행 기술의 채용을 늘리고 있습니다. 이러한 수요가 증가함에 따라 센서, 제어 시스템, 차량 진단 등 중요한 구성요소의 필요성이 가속화되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

122억 3,000만 달러

예측 금액

237억 3,000만 달러

CAGR

6.9%

메트로 채용 증가

도시 교통망의 급속한 확대와 혼잡한 도시에서의 드라이버리스 모빌리티의 추진에 의해 2024년에는 지하철 부문이 지속적인 점유율을 유지했습니다. 지하철은 고정된 선로와 다이아몬드로 주행하기 때문에 완전 자동화에 이상적인 후보이며, 자동 열차 운전(ATO), 자동차 센서, 실시간 제어 유닛 등의 고급 시스템이 필요합니다. 이 기회를 살리기 위해 각 회사는 신설 차량과 기존 차량에 대한 후퇴가 가능한 컴팩트하고 에너지 효율적인 컴포넌트의 개발에 주력하고 있습니다. 지하철 당국 및 턴키 프로젝트 제공업체와의 전략적 파트너십도 제조업체가 시장에서 발판을 강화하는 데 도움이 됩니다.

LIDAR 모듈의 견인력

LIDAR 모듈은 안전하고 효율적인 네비게이션에 필수적인 고해상도 3D 매핑과 물체 감지 기능을 제공합니다. 이 센서는 실시간 장애물 인식, 거리 계산 및 속도 규제를 가능하게 합니다. 특히 혼합 사용 환경이나 터널과 오픈 트랙을 오가는 경우에 유효합니다. 시장의 성장을 뒷받침하는 것은 안전에 대한 의무화 증가 및 자율 주행 시스템 중복성의 필요성입니다. 주요 기업은 가벼운 철도에 최적화된 LIDAR 기술에 투자하고 있습니다.

아시아태평양이 견인 역할로 상승

아시아태평양의 자율주행 열차 컴포넌트 시장은 대규모 인프라 투자, 급속한 도시화, 스마트 철도 운송에 대한 정부의 강력한 추진이 원동력이 되어 2024년에는 적정한 수익에 이른 것으로 평가되었습니다. 중국, 일본, 한국, 인도 등 국가들은 운전자가 없는 지하철 시스템이나 고속철도 프로젝트에 많은 투자를 하고 있으며 센서, 제어 유닛, 통신 모듈 등의 자동화 컴포넌트에 대한 왕성한 수요를 창출하고 있습니다. 이 지역에서 사업을 전개하는 기업은 현지화 전략을 채용하고, 지역의 연구 개발 및 제조 허브를 설치해, 제공하는 제품을 각국의 기술 표준에 맞추고 있습니다.

자율주행 열차 컴포넌트 시장의 주요 기업은 Qualcomm Technologies, Inc., Hitachi Ltd., Siemens AG, Wabtec Corporation, Rockwell Automation Inc., Mitsubishi Electric, Thales Group, Schneider Electric, Alstom SA 및 CRRC Corporation Limited입니다.

경쟁력을 유지하고 시장 경쟁력을 확대하기 위해 주요 기업은 기술 혁신, 전략적 파트너십 및 지역 확대를 선호합니다. 특히 성능 및 안전성을 모두 높이는 LIDAR 모듈, 실시간 제어 시스템, 예지보전 플랫폼 등 AI 대응 센서 통합 솔루션 개발에 중점을 둡니다. 기업은 또한 철도 사업자, 운송 기관, 도시 교통 당국과 협력하여 특히 지하철 및 고속 철도 프로젝트에서 장기 계약을 확보하고 있습니다. 이러한 전략은 기업이 진화하는 규제와 운행상의 요구에 부응할 뿐만 아니라 경쟁 구도가 격화되는 가운데 엔드 투 엔드 솔루션 제공업체로서의 지위를 확립하는 데 도움이 됩니다. 현지화는 여전히 중요한 전술이며, 많은 기업들이 비용 절감과 지역 규격 준수를 목적으로 아시아태평양 등 고성장 지역에 제조 및 연구개발 거점을 설립하고 있습니다.

목차

제1장 조사 방법

시장의 범위 및 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역 및 국가

기본 추정 및 계산

기준 연도 계산

시장 예측의 주요 동향

1차 조사 및 검증

1차 정보

예측 모델

조사의 전제 및 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

도시의 대중교통기관 수요 증가

신호 및 통신 기술의 진보

지속가능성을 향한 세계의 대처

스마트 인프라 투자 확대

승객의 안전성 및 서비스 신뢰성 향상

장기 운용에 있어서 비용 효율

업계의 잠재적 위험 및 과제

고액의 설비 투자의 필요성

레거시 시스템과의 통합의 과제

시장 기회

스마트 화물 회랑의 출현

반자율형 지역 열차의 개발

정부 주도의 대규모 인프라 프로젝트

AI 및 디지털 트윈의 도입

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기술과 혁신의 상황

기존 기술 동향

향후 기술

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품별

가격 모델 및 총소유비용(TCO) 분석

생산 통계

생산 거점

소비 거점

수출과 수입

비용 내역 분석

특허 분석

투자 및 자금 조달 동향 분석

사이버 보안 위협 상황

5G 및 6G가 철도 자동화에 미치는 영향

비즈니스 케이스 분석

ROI 계산 모델 및 회수 기간 분석

리스크 평가 및 경감 전략

성능 메트릭

변경 관리 및 조직 준비

구현 전략

실장 타임라인의 벤치마크

단계적인 전개 전략

리스크 평가 및 경감의 프레임워크

벤더 선정 및 조달 가이드 라인

품질 보증 및 테스트 프로토콜

인재에 대한 영향 및 변화 관리

직종 카테고리의 영향 분석

재훈련 및 재스킬 습득 요건

지속가능성 및 환경 측면

지속가능한 관행

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경 친화적인 노력

탄소발자국의 고려

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

시장 개척 전략

고객만족도 벤치마크

주요 발전

합병 및 인수

파트너십 및 협업

신제품 발매

확장 계획 및 자금 조달

제5장 시장 추계 및 예측 : 레벨별(2021-2034년)

주요 동향

고A1

고A2

고A3

고A4

제6장 시장 추계 및 예측 : 전철로별(2021-2034년)

주요 동향

지하철 및 모노레일

라이트 레일

고속철도 및 신칸센

제7장 시장 추계 및 예측 : 기술별(2021-2034년)

주요 동향

CBTC

ERTMS

PTC

항공관제국

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

승객

화물

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

러시아

아시아태평양

중국

인도

일본

호주

인도네시아

필리핀

태국

한국

싱가포르

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

제10장 기업 프로파일

세계 기업

Siemens Mobility

Alstom

Hitachi Rail

CRRC Corporation

Thales

Wabtec

Kawasaki Heavy Industries

CAF

지역 기업

Stadler Rail

Progress Rail

Mitsubishi Electric

Ansaldo

Knorr-Bremse

Huawei Technologies

Bombardier

Toshiba

신흥 기업 및 교란 기업

ADLINK Technology

Cylus

OTIV

Parallel Systems

Cisco Systems

AJY

영문 목차

영문목차

The Global Autonomous Train Market was valued at USD 12.23 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 23.73 billion by 2034.

Rail operators are increasingly adopting autonomous technologies to improve operational efficiency, reduce human error, and enable precise scheduling. This rising demand is accelerating the need for critical components such as sensors, control systems, and onboard diagnostics.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$12.23 Billion

Forecast Value

$23.73 Billion

CAGR

6.9%

Increasing Adoption in Metro

The metro segment held a sustainable share in 2024, driven by the rapid expansion of urban transit networks and the push for driverless mobility in congested cities. With metros running on fixed tracks and schedules, they are ideal candidates for full automation, requiring advanced systems like automatic train operation (ATO), onboard sensors, and real-time control units. To capitalize on this opportunity, companies are focusing on developing compact, energy-efficient components that can be integrated into new builds as well as retrofitted onto existing fleets. Strategic partnerships with metro rail authorities and turnkey project providers are also helping manufacturers solidify their market foothold.

LIDAR Module to Gain Traction

The LIDAR modules segment held a robust share in 2024, offering high-resolution 3D mapping and object detection capabilities essential for safe and efficient navigation. These sensors enable real-time obstacle recognition, distance calculation, and speed regulation-especially in mixed-use environments or when transitioning between tunnels and open tracks. Market growth is supported by increasing safety mandates and the need for redundancy in autonomous systems. Key players are investing in lightweight, rail-optimized LIDAR technologies that can withstand harsh environments while delivering high precision.

Asia Pacific to Emerge as a Propelling Region

Asia Pacific autonomous train components market is expected to reach decent revenues in 2024, driven by major infrastructure investments, rapid urbanization, and a strong government push for smart rail transport. Countries like China, Japan, South Korea, and India are heavily investing in driverless metro systems and high-speed rail projects, creating robust demand for automation components such as sensors, control units, and communication modules. Companies operating in this region are adopting localization strategies, setting up regional R&D and manufacturing hubs, and aligning their offerings with national technology standards.

Key players in the autonomous train components market are Qualcomm Technologies, Inc., Hitachi Ltd., Siemens AG, Wabtec Corporation, Rockwell Automation Inc., Mitsubishi Electric, Thales Group, Schneider Electric, Alstom SA, and CRRC Corporation Limited.

To stay competitive and expand their footprint in the autonomous train components market, leading companies are prioritizing technology innovation, strategic partnerships, and regional expansion. A major focus is on developing AI-enabled, sensor-integrated solutions such as LIDAR modules, real-time control systems, and predictive maintenance platforms that enhance both performance and safety. Companies are also collaborating with rail operators, transit agencies, and urban transport authorities to secure long-term contracts, especially in metro and high-speed rail projects. These strategies are helping companies not only meet evolving regulatory and operational demands but also establish themselves as end-to-end solution providers in an increasingly competitive landscape. Localization remains a key tactic, with many players establishing manufacturing and R&D hubs in high-growth regions like Asia Pacific to reduce costs and comply with regional standards.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Level

2.2.3 Train

2.2.4 Technology

2.2.5 Application

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future-outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising Demand for Urban Mass Transit

3.2.1.2 Advancements in Signaling & Communication Technologies

3.2.1.3 Global Push Toward Sustainability

3.2.1.4 Growing Investments in Smart Infrastructure

3.2.1.5 Enhanced Passenger Safety & Service Reliability

3.2.1.6 Cost Efficiency in Long-Term Operations

3.2.2 Industry pitfalls and challenges

3.2.2.1 High Capital Expenditure Requirements

3.2.2.2 Integration Challenges with Legacy Systems

3.2.3 Market opportunities

3.2.3.1 Emergence of Smart Freight Corridors

3.2.3.2 Development of Semi-Autonomous Regional Trains

3.2.3.3 Government-Led Infrastructure Mega Projects

3.2.3.4 Adoption of AI and Digital Twins

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 LATAM

3.4.5 MEA

3.5 Technology and innovation landscape

3.5.1 Existing Technological trends

3.5.2 Upcoming Technologies

3.6 Porter's analysis

3.7 PESTEL analysis

3.8 Price trends

3.8.1 By region

3.8.2 By product

3.8.3 Pricing models & total cost of ownership (TCO) analysis

3.9 Production statistics

3.9.1 Production hubs

3.9.2 Consumption hubs

3.9.3 Export and import

3.10 Cost breakdown analysis

3.11 Patent analysis

3.12 Investment & funding trends analysis

3.13 Cybersecurity Threat Landscape

3.14 5G/6G Impact on Rail Automation

3.15 Business case analysis

3.15.1 ROI calculation models & payback period analysis