귀리 플레이크 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Oat Flakes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801840

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

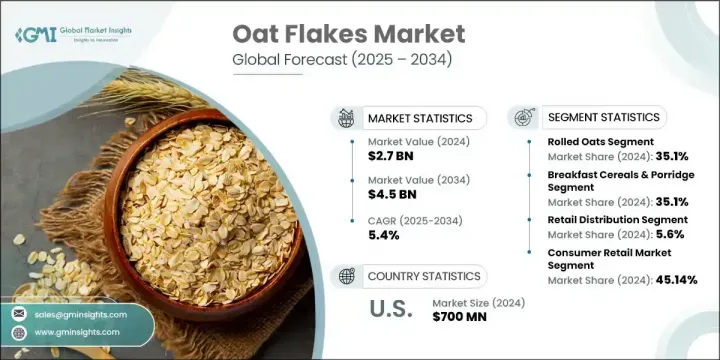

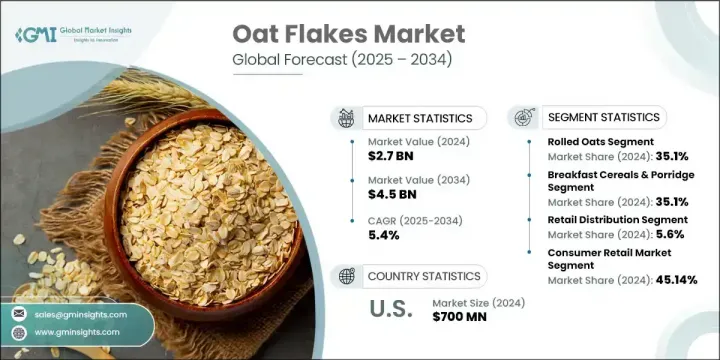

세계의 귀리 플레이크 시장은 2024년에는 27억 달러로 평가되었으며 CAGR 5.4%로 성장할 전망이며 2034년까지는 45억 달러에 이를 것으로 추정됩니다.

귀리 플레이크는 통귀리 알곡을 쪄서 압연하고 편평하게 가공하여 생산됩니다. 이 플레이크는 인기 있는 아침 식사 필수품이자 다양한 포장 및 제빵 식품의 기능성 원료로 자리 잡았습니다. 소비자들 사이에서 건강과 웰빙에 대한 관심이 높아지는 것이 이 시장 성장을 주도하는 상당한 요인이다. 식이섬유, 필수 미네랄, 비타민이 풍부한 것으로 알려진 귀리 플레이크는 건강을 중시하는 사람들이 건강하고 편리한 식사 또는 간식 대안을 찾는 데 매력적이다.

제품 혁신은 산업을 형성하는 데 핵심적인 역할을 하고 있다. 많은 주요 브랜드들은 바쁜 생활 방식과 다양한 식이 요구를 위해 설계된 인스턴트 귀리, 맛을 낸 제품, 영양 강화 제품 등을 포함하도록 제품군을 다양화하고 있다. 뜨거운 아침 식사, 스무디 보울, 베이킹 레시피 등 다양한 용도로 간편하게 활용할 수 있다는 점은 귀리 플레이크를 전 세계 가정의 필수품으로 자리매김하는 데 기여했습니다. 북미는 강력한 소비자 인식, 확립된 아침 식사 문화, 고품질 귀리 기반 제품의 광범위한 접근성 덕분에 전 세계 시장에서 지배적인 점유율을 차지하고 있습니다. 이 지역의 고급 유통망과 탄탄한 국내 귀리 생산량 또한 꾸준한 수요 유지에 기여하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

27억 달러

예측 금액

45억 달러

CAGR

5.4%

롤드 귀리 부문은 2024년 35.1%의 점유율을 기록했으며, 2034년까지 연평균 5.5%의 성장률을 보일 것으로 예측됩니다. 이들의 광범위한 인기는 적당한 조리 시간과 높은 영양가 사이의 균형에서 비롯됩니다. 소비자들은 친숙한 식감과 아침 식사 그릇부터 베이킹 제품에 이르기까지 다양한 레시피에서의 다용도성 때문에 이 귀리을 선호합니다. 상대적으로 낮은 가공 수준은 주요 영양소를 보존하여 건강을 중시하는 구매자들 사이에서 입지를 강화합니다.

용도별로는 아침 시리얼 및 죽 부문이 2024년 35.1%의 점유율을 기록했으며, 2034년까지 연평균 성장률(CAGR) 5.5%로 성장할 것으로 예상됩니다. 아침 식사로 고섬유질, 심장 건강에 좋은 식사에 대한 선호도가 높아지면서 이 부문에서 귀리 소비가 증가했습니다. 콜레스테롤 관리와 지속적인 에너지 공급에 대한 귀리의 역할이 인정받으면서, 하루를 영양가 있게 시작하려는 소비자들의 최우선 선택이 되고 있습니다. 또한 베이킹 및 포장 식품 산업 내 수요도 증가하고 있는데, 머핀, 쿠키, 빵 등의 제품에서 식감과 영양 성분을 개선하기 위해 귀리 플레이크 사용이 점차 확대되고 있습니다.

미국의 귀리 플레이크 시장은 2024년에 7억 달러를 창출했습니다. 미국 시장의 성장세는 건강 의식 고조, 식물성 및 글루텐 프리 식단에 대한 관심 증가, 강력한 국내 공급망이 복합적으로 뒷받침하고 있습니다. 현지 귀리 재배 기술 향상과 효율적인 제조 운영 역시 주요 기여 요인입니다. 미국 소비자들은 소화 기능 개선 및 심장 건강 증진과 같은 기능성 건강 혜택을 제공하는 제품에 대한 꾸준한 수요를 보이고 있으며, 이는 귀리 플레이크의 영양 프로필과 잘 부합합니다.

세계의 귀리 플레이크 시장을 형성하는 기업은 Richardson International Limited, Great River Organic Milling, McCann's Irish Oatmeal, Blue Lake Milling, Kellogg Company, Grain Millers Inc, Nature's Path Foods, Jordans Dorset Ryvita, Flahavan'sPeps Foods Limited, Arrowhead Mills(Hain Celestial Group), Hodgson Mill, Honeyville Food Products, Avena Foods Limited, Cream Hill Estates, General Mills, Country Choice Organic, Gluten Free Oats LLC, Bob's Red Mill Natural Foods, Hamlyns of Scotland 등 귀리 플레이크 부문에서 활동하는 기업들은 시장 점유율을 확대하기 위해 혁신, 지속가능성, 시장 세분화를 최우선 과제로 삼고 있습니다. 주요 전략 중 하나는 유기농 및 글루텐 프리 제품부터 향이 첨가된 제품, 조리용 귀리 플레이크에 이르기까지 다양한 제품 라인을 출시하여 변화하는 소비자 선호도를 충족시키는 것입니다. 많은 업체들이 영양 성분을 유지하면서 맛과 식감을 개선하는 고급 가공 기술에 투자하고 있습니다. 클린 라벨과 건강 관련 주장을 강조하는 노력을 통해 브랜딩과 포장도 중요한 역할을 합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 리스크 및 제목

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품 유형별

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속가능한 관행

폐기물 감축 전략

생산의 에너지 효율

환경 친화적인 노력

탄소발자국 고려 사항

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

주요 동향

롤드 귀리(옛날 귀리)

통상의 롤드 귀리

유기농 롤드 귀리

맛 첨가 롤드 귀리

퀵 귀리(퀵 쿠킹 귀리)

표준 퀵 귀리

유기농 퀵 귀리

강화 퀵 귀리

인스턴트 귀리

일반 인스턴트 귀리

맛을 낸 인스턴트 귀리

프리미엄 인스턴트 귀리

스틸 컷 귀리(아일랜드 귀리)

기존 스틸 컷

퀵 쿠킹 스틸 컷

유기농 스틸 컷 귀리

특성 프리미엄 귀리 플레이크

고대 곡물 블렌드

글루텐 프리 인증 귀리

기존 품종

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

아침 시리얼과 죽

따뜻한 아침 시리얼

차가운 아침 식사 응용

오버나이트 귀리과 조리된 귀리

베이킹 및 식품 제조

가정용 베이킹

상업용 식품 제조

식품 가공 산업

음료 및 스무디

스무디 및 셰이크 용도

식물성 우유 대체품

기능성 음료

스낵 식품과 바

그래놀라와 에너지 바

스낵 믹스와 트레일 믹스

크래커와 칩스

베이비 푸드와 유아의 영양

유아용 시리얼 제품

유아와 어린이 영양

제7장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

주요 동향

소매 유통

슈퍼마켓 및 대형 슈퍼마켓

건강식품 및 전문점

편의점

온라인과 전자상거래

주요 전자상거래 플랫폼

소비자 직접 판매 채널

모바일 상거래

푸드서비스 유통

레스토랑과 카페

시설 내 푸드 서비스

접객 및 관광

도매 및 B2B 유통

식품 도매업체

산업 및 상업 판매

제8장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

주요 동향

소비자 소매 시장

가계 소비

건강 지향 소비자

가족과 어린이를 위한 시장

고령자

식품 제조업

아침 시리얼 제조업체

구운 과자 제조업체

스낵 식품 회사

베이비 푸드 제조업체

외식 산업

레스토랑 및 카페 운영자

시설 내 푸드 서비스

케이터링과 이벤트 서비스

헬스 케어 푸드서비스

산업용도

원료 공급업계

영양 보조 식품 제조

동물사료 산업

수출과 국제무역

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

PepsiCo Inc.(Quaker Oats)

Kellogg Company

General Mills Inc.

Bob's Red Mill Natural Foods

Nature's Path Foods

Arrowhead Mills(Hain Celestial Group)

Country Choice Organic

Grain Millers Inc.

Richardson International Limited

Avena Foods Limited

Blue Lake Milling

Gluten Free Oats LLC

Morning Foods Limited

Mornflake

Hamlyns of Scotland

Jordans Dorset Ryvita

Flahavan's

Honeyville Food Products

Great River Organic Milling

Hodgson Mill

McCann's Irish Oatmeal

Cream Hill Estates

HBR

영문 목차

영문목차

The Global Oat Flakes Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 4.5 billion by 2034. Oat flakes are produced by steaming, rolling, and flattening whole oat groats. These flakes have become a popular breakfast staple and functional ingredient in various packaged and baked food products. The rising emphasis on health and wellness among consumers is a significant factor fueling the growth of this market. Known for being rich in fiber, essential minerals, and vitamins, oat flakes appeal to health-conscious individuals seeking wholesome and convenient meal or snack alternatives.

Product innovation is playing a key role in shaping industry. Many top brands are diversifying their offerings to include instant oats, flavored options, and nutrient-enriched formulations designed for busy lifestyles and varied dietary needs. Their ease of use-whether in a hot breakfast, smoothie bowl, or a baking recipe-has helped establish oat flakes as a go-to product across global households. North America holds the dominant share in the global market, supported by strong consumer awareness, a well-established breakfast culture, and widespread access to high-quality oat-based products. The region's advanced retail networks and robust domestic oat production also contribute to consistent demand.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2.7 Billion

Forecast Value

$4.5 Billion

CAGR

5.4%

The rolled oats segment held 35.1% share in 2024 and is forecasted to grow at a CAGR of 5.5% by 2034. Their widespread appeal stems from a balance between moderate cook times and strong nutritional value. Consumers gravitate toward these oats for their familiar texture and versatility across recipes ranging from breakfast bowls to baked goods. Their relatively lower processing level ensures they retain key nutrients, which strengthens their position among health-minded buyers.

In terms of application, the breakfast cereals and porridge segment held 35.1% share in 2024, and is expected to grow at a CAGR of 5.5% through 2034. The growing preference for high-fiber, heart-healthy meals in the morning has increased the consumption of oats in this category. Their recognized role in managing cholesterol and providing long-lasting energy makes them a top choice for consumers prioritizing nutritious starts to the day. Additionally, demand is growing within the baking and packaged food industry, where oat flakes are increasingly used to improve texture and nutritional content in items such as muffins, cookies, and breads.

United States Oat Flakes Market generated USD 700 million in 2024. The market's growth trajectory in the US is supported by a mix of rising health awareness, growing interest in plant-based and gluten-free diets, and strong domestic supply. Improvements in local oat cultivation and efficient manufacturing operations are also key contributors. Consumers in the US are showing consistent demand for products that offer functional health benefits like improved digestion and heart health, which aligns well with oat flakes' nutritional profile.

Companies shaping the Global Oat Flakes Market include Richardson International Limited, Great River Organic Milling, McCann's Irish Oatmeal, Blue Lake Milling, Kellogg Company, Grain Millers Inc., Nature's Path Foods, Jordans Dorset Ryvita, Flahavan's, PepsiCo Inc. (Quaker Oats), Mornflake, Morning Foods Limited, Arrowhead Mills (Hain Celestial Group), Hodgson Mill, Honeyville Food Products, Avena Foods Limited, Cream Hill Estates, General Mills Inc., Country Choice Organic, Gluten Free Oats LLC, Bob's Red Mill Natural Foods, and Hamlyns of Scotland. Companies operating in the oat flakes sector are prioritizing innovation, sustainability, and market segmentation to expand their presence. One of the primary strategies is the launch of diverse product lines-ranging from organic and gluten-free variants to flavored and ready-to-cook oat flakes-to cater to evolving consumer preferences. Many players are investing in advanced processing techniques that retain nutritional content while improving taste and texture. Branding and packaging also play a critical role, with efforts aimed at highlighting clean labels and health claims.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Product type

2.2.2 Application

2.2.3 Distribution channel

2.2.4 End use industry

2.2.5 Regional

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By product type

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million & Tons)

5.1 Key trends

5.2 Rolled oats (old-fashioned oats)

5.2.1 Regular rolled oats

5.2.2 Organic rolled oats

5.2.3 Flavored rolled oats

5.3 Quick oats (quick-cooking oats)

5.3.1 Standard quick oats

5.3.2 Organic quick oats

5.3.3 Fortified quick oats

5.4 Instant oats

5.4.1 Plain instant oats

5.4.2 Flavored instant oats

5.4.3 Premium instant oats

5.5 Steel-cut oats (irish oats)

5.5.1 Traditional steel-cut

5.5.2 Quick-cooking steel-cut

5.5.3 Organic steel-cut oats

5.6 Specialty and premium oat flakes

5.6.1 Ancient grain blends

5.6.2 Gluten-free certified oats

5.6.3 Heritage and heirloom varieties

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Tons)

6.1 Key trends

6.2 Breakfast cereals & porridge

6.2.1 Hot breakfast cereals

6.2.2 Cold breakfast applications

6.2.3 Overnight and prepared oats

6.3 Baking and food manufacturing

6.3.1 Home baking applications

6.3.2 Commercial food manufacturing

6.3.3 Industrial food processing

6.4 Beverages and smoothies

6.4.1 Smoothie and shake applications

6.4.2 Plant-based milk alternatives

6.4.3 Functional beverages

6.5 Snack foods and bars

6.5.1 Granola and energy bars

6.5.2 Snack mixes and trail mixes

6.5.3 Crackers and chips

6.6 Baby food and infant nutrition

6.6.1 Infant cereal products

6.6.2 Toddler and child nutrition

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Million & Tons)

7.1 Key trends

7.2 Retail distribution

7.2.1 Supermarkets and hypermarkets

7.2.2 Health food and specialty stores

7.2.3 Convenience stores

7.3 Online and e-commerce

7.3.1 Major e-commerce platforms

7.3.2 Direct-to-consumer channels

7.3.3 Mobile commerce

7.4 Food service distribution

7.4.1 Restaurant and cafe sales

7.4.2 Institutional food service

7.4.3 Hospitality and tourism

7.5 Wholesale and b2b distribution

7.5.1 Food distributors

7.5.2 Industrial and commercial sales

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million & Tons)

8.1 Key trends

8.2 Consumer retail market

8.2.1 Household consumption

8.2.2 Health-conscious consumers

8.2.3 Family and children's market

8.2.4 Senior and elderly consumers

8.3 Food manufacturing industry

8.3.1 Breakfast cereal manufacturers

8.3.2 Baked goods producers

8.3.3 Snack food companies

8.3.4 Baby food manufacturers

8.4 Food service industry

8.4.1 Restaurant and cafe operators

8.4.2 Institutional food service

8.4.3 Catering and event services

8.4.4 Healthcare food service

8.5 Industrial applications

8.5.1 Ingredient supply industry

8.5.2 Nutritional supplement manufacturing

8.5.3 Animal feed industry

8.5.4 Export and international trade

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Tons)