구조용 접착제 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측

Structural Bonding Agents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1773391

리서치사:Global Market Insights Inc.

발행일:2025년 06월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

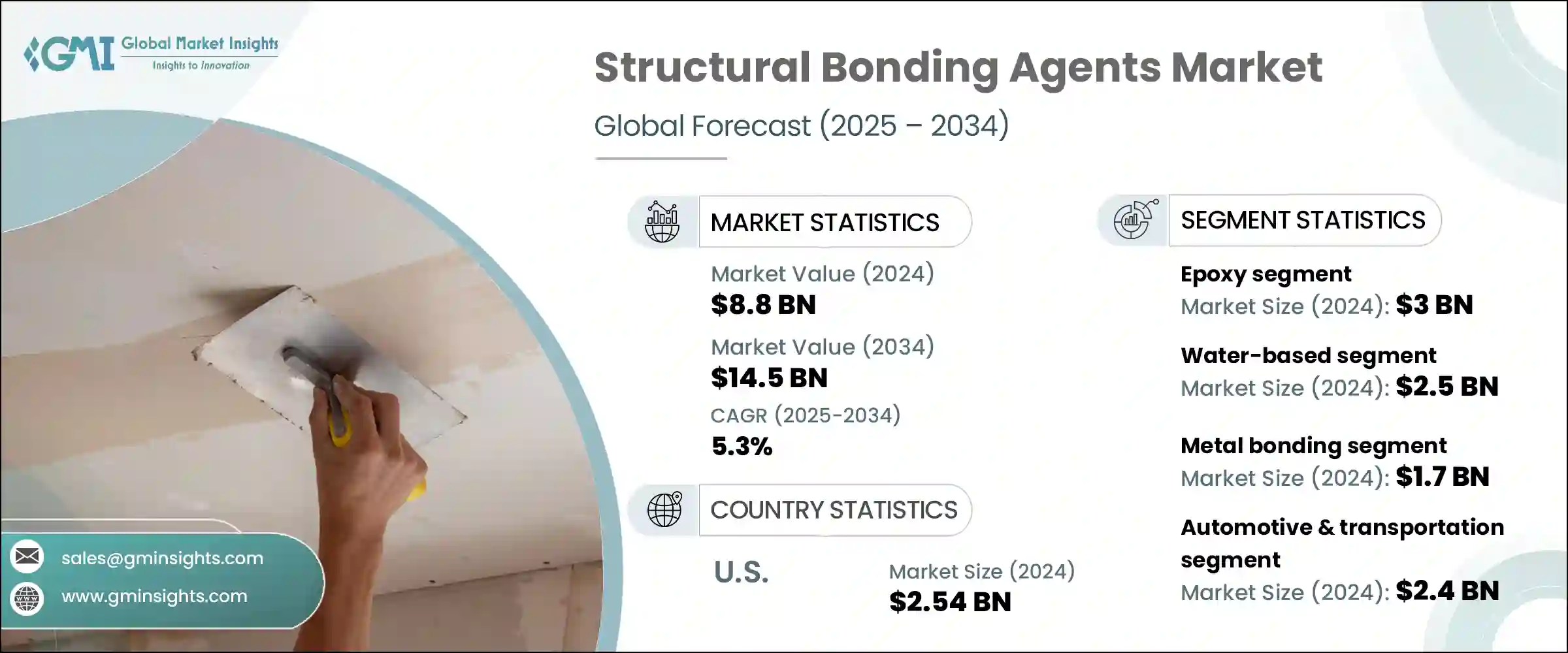

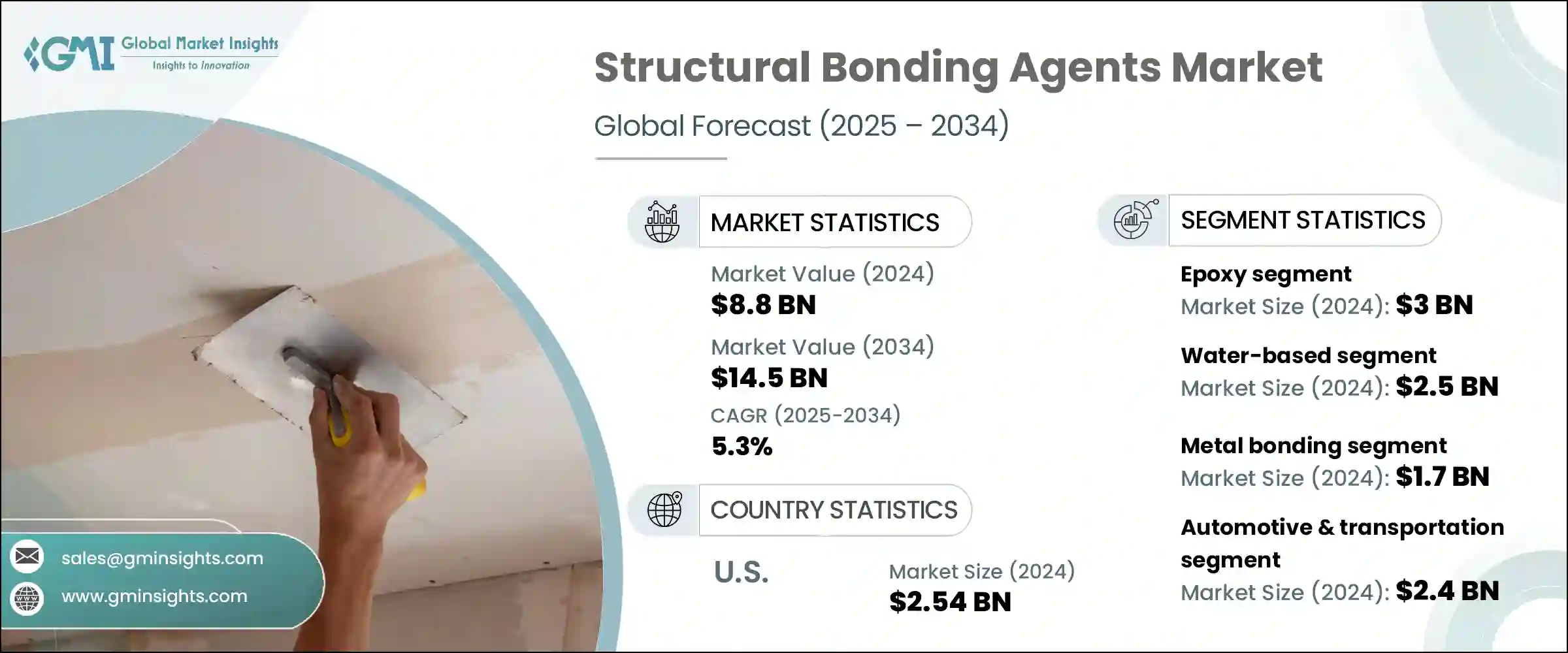

세계의 구조용 접착제 시장 규모는 2024년에 88억 달러를 달성하였고, CAGR 5.3%로 성장하여 2034년에는 145억 달러에 이를 것으로 예측되고 있습니다.

시장 확대의 요인은 여러가지 있지만 그 중에서도 자동차산업과 항공우주산업에 있어서의 경량 재료에 대한 수요 상승을 들 수 있습니다.

뛰어난 강도 대 중량비와 내구성에 의해 다양한 용도로 복합재료의 채용이 확대되고 있는 것도 시장의 성장을 뒷받침하고 있습니다. 또한 현재 진행중인 세계의 건설 프로젝트는 수요에 크게 기여하고 있습니다.

시장 범위

시작연도

2024

예측연도

2025-2034

시작금액

88억 달러

예측금액

145억 달러

CAGR

5.3%

새로운 동향은 지속 가능성을 향하고 있으며, 제조업체는 보다 엄격한 규제와 소비자의 취향에 부응하기 위해 환경친화적이고 저VOC 무용제 접착제에 주력하고 있습니다. 그린빌딩의 인증과 배출 기준이 엄격해짐에 따라 기업은 진화하는 세계 벤치마크에 맞춰 접착제를 적극적으로 개량하고 있습니다.

에폭시 부문은 2024년에 30억 달러 시장 가치를 획득하였으며, 2034년까지 5%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이러한 접착제는 뛰어난 기계적 강도, 내약품성, 금속과 경량 복합재료 모두를 접착할 수 있는 능력을 제공하며 고성장 분야에서 필수적인 요소가 되고 있습니다.

수성 구조용 접착제 분야는 2024년에 25억 달러를 차지하였고 2034년까지 연평균 복합 성장률(CAGR) 5.8%를 보일 것으로 예측됩니다.

미국의 2024년 구조용 접착제 시장 규모는 25억 4,000만 달러였으며 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 4.8%를 보일 것으로 예측됩니다. 미국의 성장은 인프라와 건설 프로젝트에 대한 많은 투자와 함께 항공우주 및 자동차 부문의 고성능, 경량 접착 솔루션에 대한 수요가 큰 원동력이 되고 있습니다.

세계의 구조용 접착제 시장의 주요 기업인 Arkema Group, Henkel AG & Co.KGaA, 3M Company, Sika AG, HB Fuller Company 등의 대기업은 여러가지 전략적 차원에서 활발하게 경쟁하고 있습니다. 각사는 연구개발에 많은 투자를 하여 성능을 향상시키면서 환경 규제에 적합한 배합을 개발하고 있습니다.

목차

제1장 조사방법

시장의 범위와 정의

조사 디자인

조사 접근

데이터 수집방법

데이터 마이닝 소스

세계

지역/국가

기본 추정과 계산

기준연도 계산

시장 예측의 주요 동향

1차 조사와 검증

1차 정보

예측모델

조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 위험 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품별

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속 가능성과 환경 측면

지속 가능한 관행

폐기물 감축 전략

생산에서의 에너지 효율

환경친화적인 노력

탄소발자국의 고려

제4장 경쟁구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

주요 동향

에폭시

1성분 에폭시

2성분 에폭시

개질 에폭시

폴리우레탄

1성분 폴리우레탄

2성분 폴리우레탄

아크릴

시아노아크릴레이트

개질 아크릴

메틸메타크릴레이트(MMA)

실리콘

기타

제6장 시장 추계 및 예측 : 기술별(2021-2034년)

주요 동향

수성

용제 베이스

핫멜트

반응성

기타

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

금속 접합

강철

알루미늄

기타 금속

복합 접합

탄소섬유 복합재

유리섬유 복합재

기타 복합재료

플라스틱 접합

열가소성 플라스틱

열경화성 수지

목재 접착

유리 접착

콘크리트와 돌의 접착

다재료 접합

기타

제8장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

주요 동향

자동차 및 운송

승용차

상용차

전기자동차

철도

기타

항공우주

상용기

군용기

일반항공

우주용도

건축 및 건설

주택

상업

산업

인프라

풍력에너지

육상풍력

해상풍력

해양

조선

보트 건조

해양구조물

일렉트로닉스

소비자 일렉트로닉스

산업용 전자기기

의료

공업용 조립

기타

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

Henkel AG &Co. KGaA

3M Company

Sika AG

HB Fuller Company

Huntsman Corporation

Arkema Group

Lord Corporation(Parker Hannifin Corporation)

Ashland Global Holdings Inc.

Illinois Tool Works Inc.

Dow Inc.

Mapei SpA

RPM International Inc.

Permabond LLC

Master Bond Inc.

Dymax Corporation

Jowat SE

Delo Industrial Adhesives

Pidilite Industries Ltd.

Parson Adhesives, Inc.

Hernon Manufacturing, Inc.

CSM

영문 목차

영문목차

The Global Structural Bonding Agents Market was valued at USD 8.8 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 14.5 billion by 2034. The market expansion is driven by several factors, most notably the rising demand for lightweight materials in the automotive and aerospace industries. These sectors are increasingly incorporating bonding agents to support lighter composite materials, which help boost fuel efficiency and reduce emissions without sacrificing structural strength.

The growing adoption of composite materials across various applications also fuels market growth, thanks to their superior strength-to-weight ratio and durability. Structural bonding agents play a crucial role by enhancing the performance and acceptance of these materials in challenging environments. Additionally, ongoing global construction projects contribute significantly to demand, as bonding agents offer advantages over traditional mechanical fasteners in terms of load distribution, aesthetics, and resistance to environmental stressors.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$8.8 Billion

Forecast Value

$14.5 Billion

CAGR

5.3%

Emerging trends also point toward sustainability, with manufacturers focusing on eco-friendly, low-VOC, and solvent-free adhesives to meet stricter regulations and consumer preferences. This shift is not only driven by environmental compliance but also by the increasing demand for healthier indoor air quality and reduced ecological impact. As green building certifications and emissions standards become more stringent, companies are proactively reformulating their bonding agents to align with evolving global benchmarks. The market is witnessing a growing preference for water-based and bio-based structural adhesives, particularly in sectors like construction, packaging, and transportation, where sustainability has become a core design consideration.

The epoxy segment held a market value of USD 3 billion in 2024 and is expected to grow at a 5% CAGR through 2034. Epoxy adhesives lead the market due to their wide-ranging applications in industries like aerospace, automotive, construction, and electronics. These adhesives provide excellent mechanical strength, chemical resistance, and the ability to bond both metals and lightweight composites, making them indispensable in high-growth sectors. Their ability to distribute loads effectively and deliver visually appealing finishes adds to their demand.

The water-based structural bonding agents segment accounted for USD 2.5 billion in 2024 and is anticipated to grow at a CAGR of 5.8% through 2034. Driven by stringent environmental regulations and a shift toward low-VOC formulations, water-borne adhesives are gaining traction, especially in the construction and packaging industries. These adhesives provide a safer, more environmentally friendly alternative without compromising bond strength or performance.

U.S. Structural Bonding Agents Market was valued at USD 2.54 billion in 2024 and is forecasted to grow at a CAGR of 4.8% from 2025 to 2034. Growth in the U.S. is largely fueled by the demand for high-performance, lightweight bonding solutions in the aerospace and automotive sectors, alongside substantial investments in infrastructure and construction projects. Innovation in adhesive technology and favorable government policies continue to bolster market expansion.

Leading players in the Global Structural Bonding Agents Market, such as Arkema Group, Henkel AG & Co. KGaA, 3M Company, Sika AG, and H.B. Fuller Company, are actively competing across several strategic dimensions. Companies in the structural bonding agents market strengthen their position by focusing on innovation and expanding product portfolios tailored to emerging industry needs, particularly lightweight and eco-friendly adhesives. They invest heavily in R&D to develop formulations that comply with environmental regulations while enhancing performance. Strategic collaborations and partnerships with key players in the automotive, aerospace, and construction sectors help expand market reach and credibility. Additionally, geographic expansion into fast-growing regions supports revenue growth.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product Type

2.2.3 Technology

2.2.4 Application

2.2.5 End Use Industry

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and Innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By product

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)