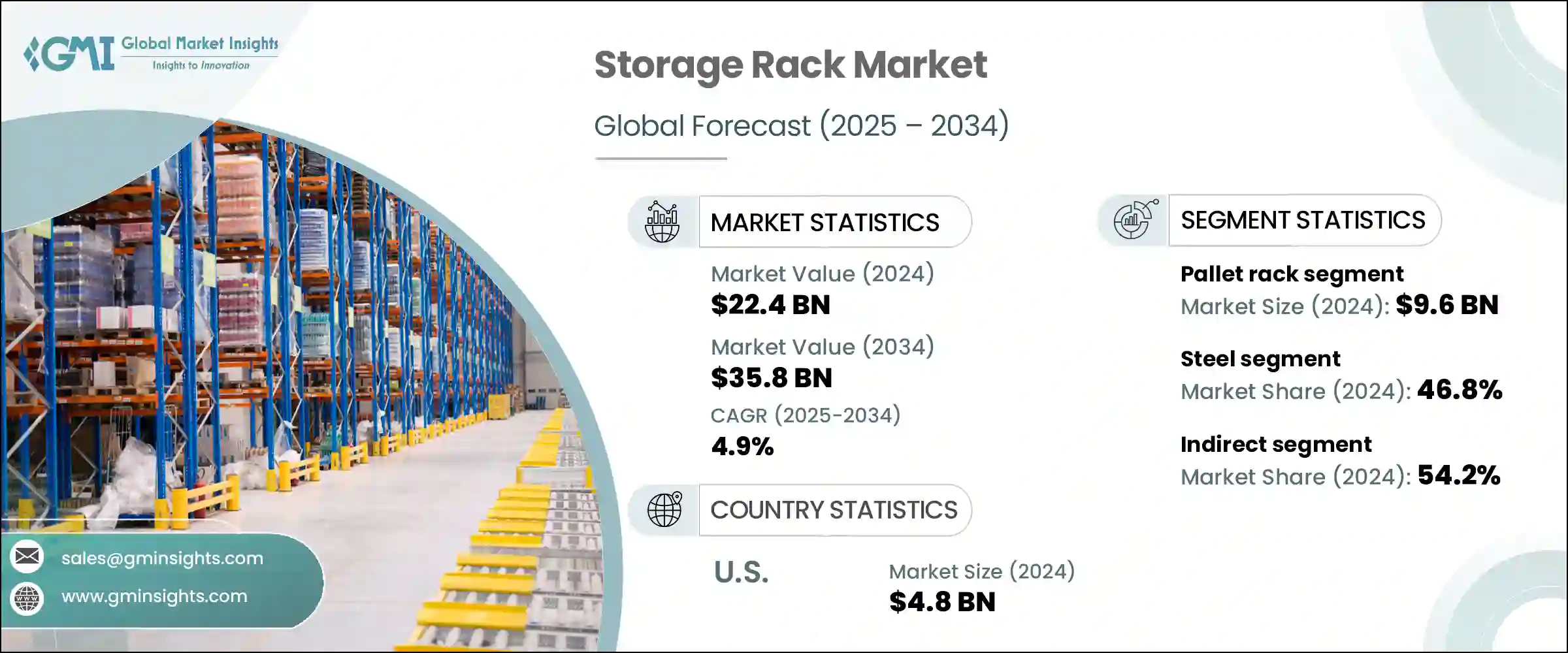

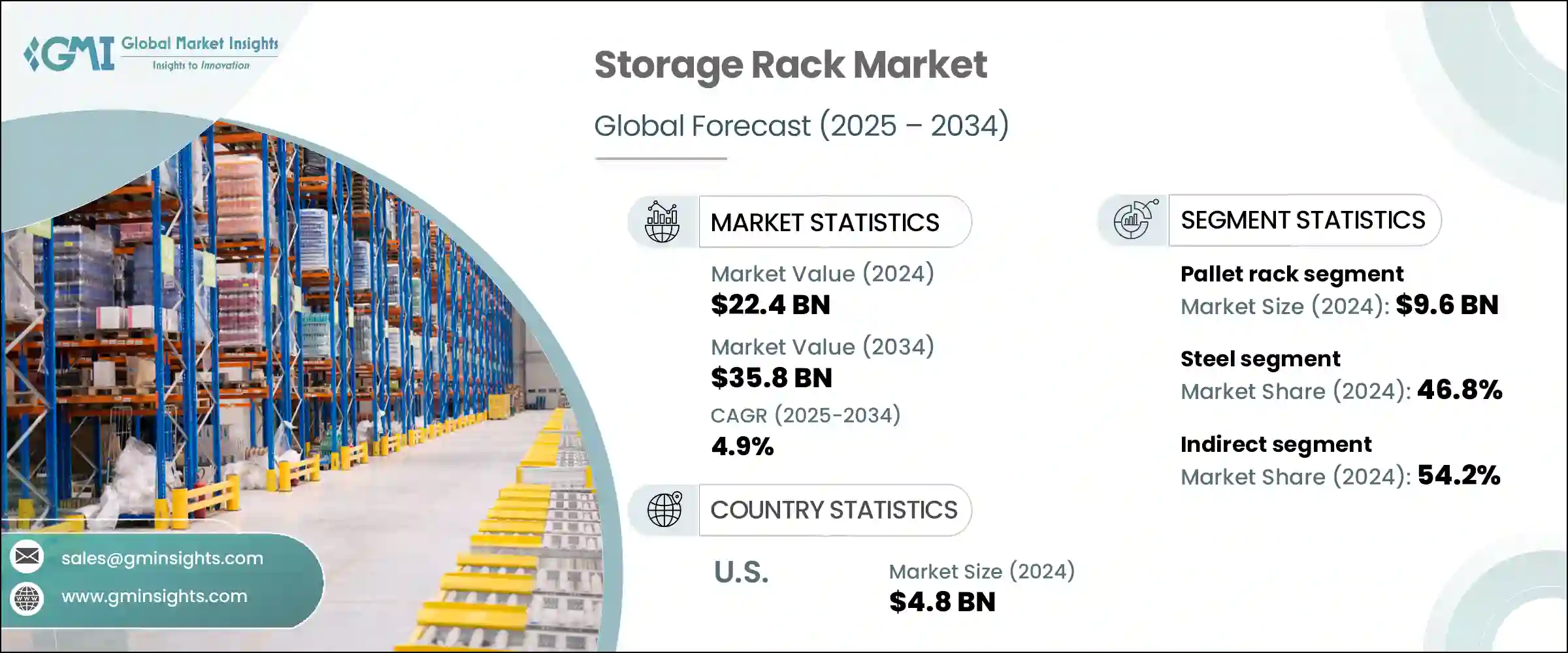

세계의 스토리지 랙 시장 규모는 2024년에 224억 달러에 달하였고, CAGR 4.9%로 성장하여 2034년에는 358억 달러에 이를 것으로 예측됩니다.

도시의 풀필먼트 허브에서 효율적이고 공간절약적인 솔루션에 대한 수요가 증가함에 따라 이러한 성장에 박차를 가하고 있습니다. 전자상거래 가운데 특히 퀵커머스의 확대에 의해 신속한 오더 피킹과 재고 회전의 필요성이 증가하고 있습니다. 이를 서포트하기 위해, 창고는 로봇 피킹이나 자동 보관 및 검색 시스템 등의 자동화 시스템과 심리스하게 연동하는 랙을 채용하고 있습니다.

스토리지 인프라는 물류 워크플로우와 운송 스케줄의 변화에 따라 급속히 진화하고 있으며, 기업은 업무 속도와 유연성을 높이는 랙 시스템을 우선시하고 있습니다. 기업은 재고 수요의 변화에 맞추어 진화할 수 있는 조정 및 확장 가능한 스토리지 솔루션을 선호하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 224억 달러 |

| 예측금액 | 358억 달러 |

| CAGR | 4.9% |

2024년 팔레트 랙 시장 규모는 96억 달러에 이르렀으며, 2034년까지 연평균 복합 성장률(CAGR)은 5.3%로 예측됩니다. 팔레트 랙 시스템은 수직 방향으로 복수단에 걸쳐 쌓아 올리도록 설계되어 있어 창고의 효율을 높이고 재고의 중량이나 수량 변동에 대응합니다.

강철 부문은 2024년에 46.8%의 점유율을 차지하였으며, 스토리지 랙의 주요 재료로서 최고의 인기를 유지하고 있으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.4%를 보일 것으로 예측됩니다. 강철의 높은 강도 대 중량비, 긴 수명, 비용 효율성은 대규모 창고 및 산업 용도에 이상적입니다. 제조업, 소매업, 전자상거래 등의 분야에서는 대량의 재료를 취급하고 운영을 합리화하여 구조적인 타협 없이 중량 설비를 견딜 수 있는 강철 랙에 의지하고 있습니다.

미국 스토리지 랙 시장은 2024년 48억 달러로 평가되었으며 2034년까지 연평균 복합 성장률(CAGR) 5.5%를 보일 것으로 예측되고 있습니다. 콜드체인 인프라의 개발이 시장 확대에 기여하고 있습니다.

스토리지 랙 업계의 주요 기업으로는 Interlake Mecalux, Dematic, Kardex Group, Toyota Industries, Constructor Group, Gonvarri Material Handling, AK Material Handling Systems, SSI Schaefer, Ridg-U-Rak, Mecalux, Daifuku, Arpac, North American Steel Equipment, AR Racking, Jungheinrich 등이 있습니다. 스토리지 랙 시장의 선두 기업은 경쟁력을 강화하기 위해 디지털 통합, 제품 혁신 및 비즈니스 효율성에 중점을 둡니다.

대부분은 로봇공학, AS/RS, 고급 창고 소프트웨어 플랫폼을 지원하는 자동화 지원 랙 시스템 개발에 투자하고 있습니다. 제조업체 각사는 다양한 공간의 제약이나 보관 요건에 맞춘 모듈러 설계를 제공하고 있어 커스터마이즈도 주요 요소가 되고 있습니다. 물류 회사 및 공급망 운영자와의 전략적 파트너십은 고객 네트워크를 확장하고 유통을 간소화하는 데 도움이 됩니다. 게다가 납기를 단축하고 변화하는 시장 수요에 신속하게 대응하기 위해 기업은 보다 강력한 지역 공급망과 지역 제조 허브를 구축하고 있습니다.

The Global Storage Rack Market was valued at USD 22.4 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 35.8 billion by 2034. Increasing demand for efficient, space-saving solutions in urban fulfillment hubs is fueling this growth. As urban centers face rising operational costs and space limitations, businesses are turning to high-density racking, modular shelving, and mezzanine-based structures to optimize storage. The expansion of e-commerce, especially in the quick commerce segment, has accelerated the need for rapid order picking and inventory turnover. To support this, warehouses are adopting racks that work seamlessly with automation systems like robotic picking and automated storage and retrieval systems.

Storage infrastructure is evolving rapidly alongside changes in logistics workflows and delivery timelines, with businesses prioritizing racking systems that boost operational speed and flexibility. Urban distribution centers are adopting narrow aisle racks, mobile shelving, and vertical layouts. The trend toward modularity is also strong, with businesses favoring adjustable and expandable storage solutions that can evolve with changing inventory demands. The market's transformation is being powered by a mix of adoption of automation, smart warehousing trends, and cost-efficient design solutions suited for fast-paced distribution environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.4 Billion |

| Forecast Value | $35.8 Billion |

| CAGR | 4.9% |

In 2024, the pallet racks segment contributed USD 9.6 billion and is projected to grow at a CAGR of 5.3% through 2034. These racks remain the most widely used in the market due to their adaptability, economic value, and compatibility across a range of sectors. Designed to store palletized inventory horizontally with multiple vertical tiers, pallet racks enhance warehouse efficiency and accommodate variable inventory weights and volumes. Their relevance spans key industries, including logistics, food and beverage, retail, pharma, and automotive, making them a staple in both traditional and modern warehouse formats.

The steel segment accounted for 46.8% share in 2024, maintaining its lead as the primary material of choice for storage racks, and is expected to grow at a CAGR of 5.4% from 2025 to 2034. Its high strength-to-weight ratio, longevity, and cost-efficiency make it ideal for large-scale warehousing and industrial applications. Steel racks are widely implemented in heavy-duty storage environments where they support large and dense inventory loads. Sectors like manufacturing, retail, and e-commerce rely on steel-based racks for their ability to handle bulk materials, streamline operations, and endure heavy equipment use without structural compromise.

U.S. Storage Rack Market was valued at USD 4.8 billion in 2024 and is anticipated to grow at a CAGR of 5.5% through 2034. This growth stems from the country's rapid e-commerce expansion, rising adoption of warehouse robotics, and widespread implementation of automation systems. Demand is driven by industrial sectors, logistics providers, and large-scale retailers. In addition, the development of cold chain infrastructure in pharma and food supply chains is contributing to market expansion. High labor costs in the region further incentivize investment in high-density storage to enhance productivity and reduce manual handling. The U.S. remains the dominant market in the region, followed by Mexico and Canada.

Leading players in the Storage Rack Industry include Interlake Mecalux, Dematic, Kardex Group, Toyota Industries, Constructor Group, Gonvarri Material Handling, AK Material Handling Systems, SSI Schaefer, Ridg-U-Rak, Mecalux, Daifuku, Arpac, North American Steel Equipment, AR Racking, and Jungheinrich. Top companies in the storage rack market are focusing on digital integration, product innovation, and operational efficiency to strengthen their competitive edge.

Many are investing in the development of automation-compatible racking systems to support robotics, AS/RS, and advanced warehouse software platforms. Customization is also key, with manufacturers offering modular designs tailored to different space constraints and storage requirements. Strategic partnerships with logistics firms and supply chain operators help expand client networks and streamline distribution. In addition, companies are building stronger local supply chains and regional manufacturing hubs to reduce delivery times and adapt quickly to shifting market demands.