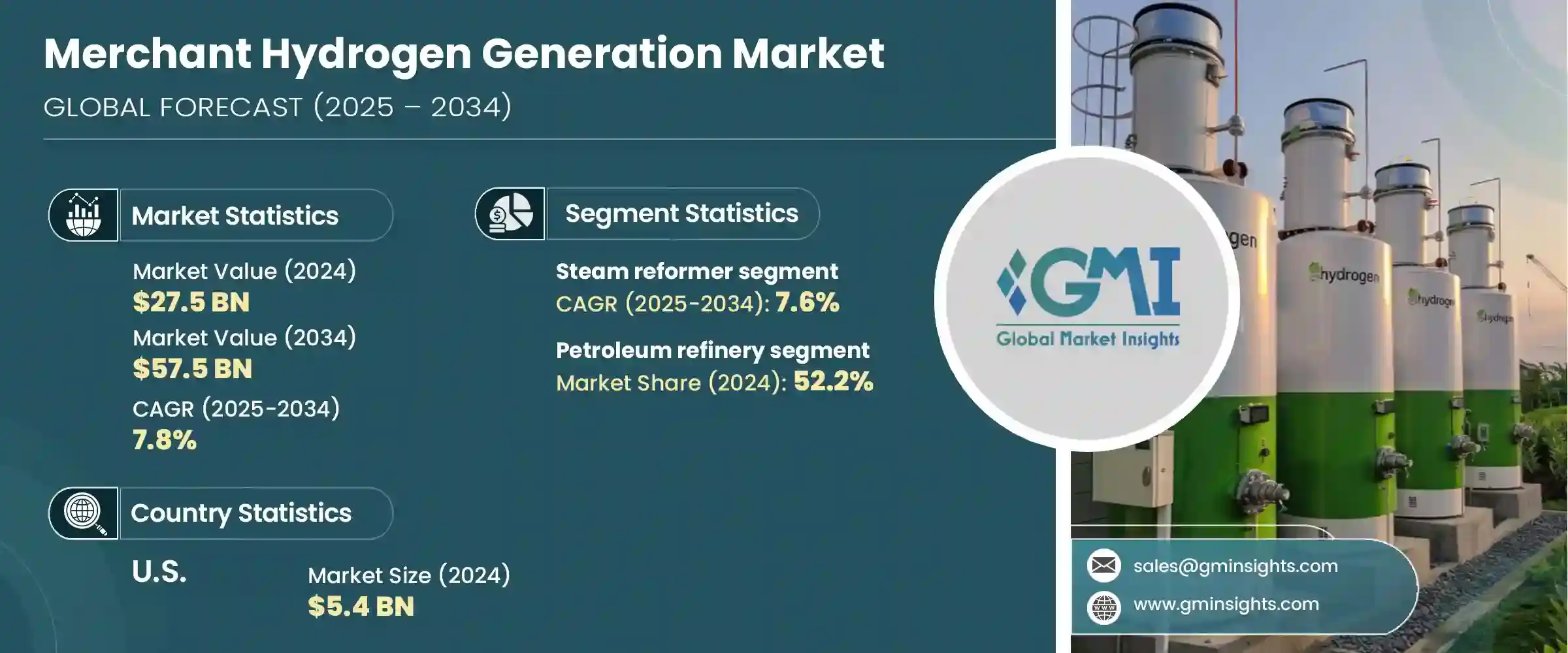

세계의 상용 수소 생성 시장은 2024년에는 275억 달러로 평가되었고, CAGR 7.8%로 성장하여 2034년에는 575억 달러에 이를 것으로 예측됩니다.

세계 정부와 산업계가 이산화탄소 배출량 감축에 중점을 두면서 시장은 꾸준한 모멘텀을 보이고 있습니다. 이러한 변화는 수소를 포함한 청정 에너지원에 대한 수요를 촉진하고 있으며, 수소는 세계 탈탄소화 아젠다의 주요 기업으로 부상하고 있습니다. 넷제로 목표 달성을 위한 정책과 부문 간 기후 변화에 대한 인식이 높아지면서 상업용 수소 생산 확대에 유리한 조건이 조성되고 있습니다.

성장을 가능하게 하는 주요 요인 중 하나는 재생에너지의 도입 규모 확대이며, 잉여 전력의 활용을 통해 수소 제조와의 시너지 효과를 창출하고 있습니다. 에너지 시스템의 다양화 및 분산화가 진행됨에 따라 수소는 에너지 저장 및 그리드 밸런싱을 위한 중요한 도구가 되고 있습니다. 이러한 상황에서 양성자 교환막 및 고체 산화물 전해질과 같은 차세대 전해질 기술이 인기를 끌고 있습니다. 이러한 기술 혁신은 높은 효율성과 비용 우위를 제공하여 상업적 규모의 수소 생성을 보다 현실적으로 만들고 있습니다. 산업계는 특히 철강, 제련, 화학 등 에너지 소비가 많은 부문에서 지속가능성 목표에 부합하는 사업 운영을 적극적으로 추진하고 있습니다. 이러한 전환은 생산성을 유지하면서 배출량을 줄일 수 있는 수소 기반 공정으로의 점진적인 전환을 촉진하고 있습니다. 이러한 추세에 따라 상업용 수소 생산 시장은 향후 10년간 구조적인 변화를 겪게 될 것입니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 275억 달러 |

| 예측 금액 | 575억 달러 |

| CAGR | 7.8% |

공정 유형에 따라 증기 개질기 카테고리는 2034년까지 연평균 7.6%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 증기 개질기의 지속적인 관련성은 비용 효율성과 기존 천연가스 인프라와의 호환성에 있습니다. 새로운 방법들이 각광을 받고 있지만, 수증기 개질은 산업용 수소 수요에 대한 확장성과 신뢰성으로 인해 여전히 널리 채택되고 있습니다. 파이프라인 네트워크와의 원활한 통합을 통해 다양한 응용 분야에서 상업용 수소의 유통을 지원하는 역할을 더욱 강화할 수 있습니다.

용도별로 시장은 석유 정제, 화학, 금속 및 기타 부문으로 분류됩니다. 정유 부문은 2024년 시장의 52.2%를 차지하며 가장 큰 수익 점유율을 차지할 것으로 예측됩니다. 정유소는 강화된 배출 규제에 대응하고 다운스트림 사업의 환경 발자국을 줄이기 위해 수소의 채택이 증가하고 있습니다. 친환경 원료와 청정 연료에 대한 수요가 증가함에 따라 정유사들은 공정을 업그레이드하고 탈황 장치와 수소화 분해 장치에 수소를 통합해야 합니다. 이러한 정유 산업의 지속적인 변화는 신뢰할 수 있는 온디맨드 상용 수소 서비스를 제공하는 수소 공급업체에게 큰 비즈니스 기회를 제공합니다.

지역별로는 북미 상업용 수소 생산 시장이 2024년 세계 매출의 24.3%를 차지할 것으로 예측됩니다. 이 지역에서 미국은 지속적인 성장세를 보이고 있으며, 시장 규모는 2022년 49억 달러에서 2024년 54억 달러로 증가할 것입니다. 강력한 정책 프레임워크와 연방 정부 기관과 민간 기업 간의 협력 관계가 확대되면서 미국 전역의 수소 생태계가 활성화되고 있습니다. 정부 지원 자금 지원 프로그램과 청정 에너지 인센티브는 특히 수소 허브와 연료 보급 통로 주변의 인프라 구축을 촉진하고 있습니다. 운송 및 물류 능력의 확대는 수소 상거래 솔루션의 산업 규모 채택을 가속화하는 데 중요한 역할을 하고 있습니다.

시장 리더들은 저탄소 인증 기준을 준수하면서 프로젝트의 경제성을 최적화하고 생산량을 확대하기 위해 많은 투자를 하고 있습니다. 산업 클러스터나 모빌리티 존과 같이 수요가 많은 중심지 근처에 상업용 수소 허브를 배치하여 배송 비용을 최소화하고 공급 대응력을 높이는 데 전략적 초점을 맞추었습니다. 또한, 이들 기업은 디지털 기술을 통해 운영을 간소화하고, 배송 일정을 개선하며, 수소 공급망 전반에 대한 실시간 가시성을 확보하기 위해 디지털 기술을 모색하고 있습니다. 현장 발전, 네트워크화된 인프라, 스마트 배송 관리 시스템을 결합한 통합 비즈니스 모델은 주요 기업들 사이에서 표준 관행이 되고 있습니다.

경쟁력을 강화하기 위해 각 업체들은 전략적 파트너십을 통해 지역적 입지를 강화하고, 규제 로드맵에 따라 대규모 배포를 위한 재정적 지원을 확보하고 있습니다. 이러한 노력을 통해 업계 참여자들은 다양한 최종 사용 부문에서 저탄소 수소에 대한 수요 증가에 대응하고 세계 에너지 전환의 미래를 만들어 나갈 수 있습니다.

The Global Merchant Hydrogen Generation Market was valued at USD 27.5 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 57.5 billion by 2034. The market is experiencing steady momentum as governments and industries worldwide place greater emphasis on reducing carbon emissions. This shift is driving demand for clean energy sources, including hydrogen, which has emerged as a key player in the global decarbonization agenda. Policies aimed at achieving net-zero goals, along with rising climate awareness across sectors, are creating favorable conditions for the expansion of merchant hydrogen generation.

One of the major growth enablers is the increasing scale of renewable energy deployment, which creates synergies with hydrogen production through surplus power utilization. As energy systems become more diversified and decentralized, hydrogen is becoming an important tool for energy storage and grid balancing. In this landscape, new-generation electrolysis technologies, such as proton exchange membrane and solid oxide electrolysis, are gaining traction. These innovations offer high efficiency and cost advantages, making hydrogen generation more viable at commercial scales. Industries are actively aligning their operations with sustainability targets, particularly in energy-intensive sectors like steel, refining, and chemicals. This transition is encouraging a gradual shift toward hydrogen-based processes that can lower emissions without compromising productivity. As these trends converge, the merchant hydrogen generation market is positioned for structural transformation over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27.5 Billion |

| Forecast Value | $57.5 Billion |

| CAGR | 7.8% |

Based on process type, the steam reformer category is projected to expand at a CAGR of 7.6% through 2034. Its continued relevance lies in its cost efficiency and compatibility with existing natural gas infrastructure. While newer methods are gaining prominence, steam reforming remains widely adopted due to its scalability and reliability for industrial hydrogen needs. Its seamless integration with pipeline networks further strengthens its role in supporting merchant hydrogen distribution across various application zones.

On the basis of application, the market is categorized into petroleum refinery, chemical, metal, and other segments. The petroleum refinery segment accounted for the largest revenue share in 2024, holding 52.2% of the market. Refineries are increasingly adopting hydrogen to meet tightening emission regulations and reduce the environmental footprint of downstream operations. The rising push for green feedstocks and cleaner fuel outputs is prompting refiners to upgrade processes and integrate hydrogen into desulfurization and hydrocracking units. This ongoing transformation within the refining landscape is creating substantial opportunities for hydrogen suppliers offering reliable, on-demand merchant hydrogen services.

Regionally, the North American merchant hydrogen generation market accounted for 24.3% of global revenue in 2024. Within this region, the United States has shown consistent growth, with market values rising from USD 4.9 billion in 2022 to USD 5.4 billion in 2024. A strong policy framework, combined with growing collaboration between federal agencies and private enterprises, is catalyzing the hydrogen ecosystem across the country. Government-backed funding programs and clean energy incentives are encouraging infrastructure buildout, particularly around hydrogen hubs and refueling corridors. The expansion of transportation and logistics capabilities is playing a key role in accelerating industrial-scale adoption of merchant hydrogen solutions.

Market leaders are investing heavily in optimizing project economics and scaling production volumes while complying with low-carbon certification standards. There is a strategic focus on placing merchant hydrogen hubs near high-demand centers like industrial clusters and mobility zones to minimize delivery costs and enhance supply responsiveness. These firms are also exploring digital technologies to streamline operations, improve delivery timelines, and maintain real-time visibility across hydrogen supply chains. Integrated business models that combine on-site generation, networked infrastructure, and smart delivery management systems are becoming standard practice among major players.

To gain a competitive edge, companies are strengthening their regional presence through strategic partnerships, aligning with regulatory roadmaps, and securing funding support for large-scale deployment. By leveraging these efforts, industry participants are well-positioned to meet the growing demand for low-carbon hydrogen across a broad spectrum of end-use sectors, thereby shaping the future of the global energy transition.