Clinical Trials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034

상품코드:1699405

리서치사:Global Market Insights Inc.

발행일:2025년 02월

페이지 정보:영문 183 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

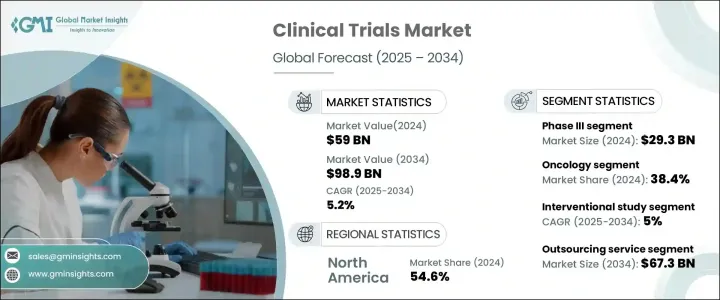

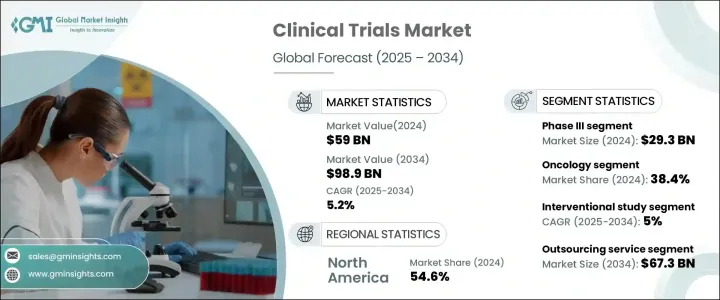

세계 임상시험 시장은 2024년 590억 달러로 평가되었고, 2025-2034년 연평균 5.2%의 성장률을 보일 것으로 예측됩니다.

첨단 치료 옵션에 대한 수요 증가와 의약품 개발에 대한 투자 증가가 시장 확대의 원동력이 되고 있습니다. 암, 당뇨병, 심혈관 질환과 같은 만성 질환이 확산됨에 따라 제약 및 생명공학 기업들은 혁신적인 치료법을 도입하기 위한 노력을 강화하고 있습니다. 임상 연구 활동의 급증은 정밀의료와 표적 치료로의 광범위한 전환을 반영하고 있으며, 임상시험 부문의 성장을 더욱 촉진하고 있습니다. 또한 인공지능(AI), 빅데이터 분석, 분산형 임상시험과 같은 기술 발전은 임상연구를 혁신하고 임상시험의 효율성과 비용 효율성을 높이고 있습니다. 의약품의 조기 승인을 위한 규제 당국의 지원과 연구 기관과 의료 서비스 제공업체 간의 협력 관계 강화도 시장 확대에 기여하고 있습니다. 환자 중심의 접근 방식과 적응형 시험 설계에 대한 관심이 높아지면서 임상시험 시장은 향후 몇 년 동안 큰 진화를 이룰 것으로 예상됩니다.

임상시험 시장은 I, II, III, III, IV 단계로 구분됩니다. 이 중 임상 III상은 2024년 293억 달러로 이 분야를 지배하고 있습니다. 이러한 대규모 임상시험은 의약품의 안전성과 유효성을 검증하는 데 필수적입니다. 복잡하고 다양한 환자 집단의 필요성으로 인해 임상 3상 시험은 종합적인 임상 데이터를 얻기 위해 여러 곳에서 실시됩니다. 기업들이 신약 제제 및 바이오시밀러를 개발함에 따라 대규모 임상 3상 시험에 대한 수요는 지속적으로 증가하고 있으며, 이 분야는 시장에서 주요한 위치를 차지하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

590억 달러

예상 금액

989억 달러

CAGR

5.2%

임상시험은 시험 설계에 따라 중재 시험, 관찰 시험, 확대 접근 시험으로 분류됩니다. 중재 시험 부문은 2024년 시장을 주도할 것으로 예상되며, 2025-2034년 연평균 5%의 성장률을 보일 것으로 예측됩니다. 이러한 연구는 통제된 치료 프로토콜에 참가자를 적극적으로 참여시킴으로써 새로운 의료 개입의 효과를 결정하는 데 매우 중요한 역할을 합니다. 중재연구는 회상 편향을 배제하고 치료 결과에 대한 구조화된 평가를 제공함으로써 최고 수준의 임상적 증거를 제공합니다. 그 결과, 제약회사와 규제기관은 의약품 승인 속도를 높이고 치료 기준을 개선하기 위해 이러한 시험에 대한 의존도를 높이고 있습니다.

북미 임상시험 시장은 2024년 54.6%의 점유율을 차지할 것으로 예상되며, 제약 및 생명공학 기업들이 집중되어 있어 우위를 점하고 있습니다. 의약품 개발, 특히 정밀의학 및 생물학적 제제 개발이 복잡해짐에 따라, 이 지역 기업들은 차세대 치료제를 시장에 출시하기 위해 임상시험에 많은 투자를 하고 있습니다. 강력한 규제 프레임워크, 잘 구축된 연구 인프라, 임상시험에 대한 자금 지원 증가는 북미의 리더십을 더욱 뒷받침하고 있습니다. 혁신적인 치료법에 대한 수요가 증가함에 따라 이 지역은 지속적으로 성장하고 있으며, 전 세계 임상연구에서 매우 중요한 역할을 하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

성장 가능성 분석

임상시험 건수 분석

임상시험 건수 분석, 지역별, 2021년-2024년

임상시험 건수 분석 : 개발 단계별, 2021년-2024년

임상시험 건수 분석, 적응증별, 2021년-2024년

규제 상황

미국

유럽

아시아태평양

싱가포르

말레이시아

인도네시아

태국

한국

필리핀

임상시험 - 아시아태평양의 우위성

Porter의 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업 매트릭스 분석

인수합병(M&A) 상황

주요 시장 기업 - 경쟁 분석

경쟁 포지셔닝 매트릭스

전략 대시보드

제5장 시장 추산 및 예측 : Phase별, 2021년-2034년

주요 동향

Phase I

Phase II

Phase III

Phase IV

제6장 시장 추산 및 예측 : 임상시험 디자인별, 2021년-2034년

주요 동향

개입 조사

관찰 조사

확장 액세스 조사

제7장 시장 예측 : 서비스 유형별 시장 추산·예측 : 서비스 유형별, 2021년-2034년

주요 동향

아웃소싱 서비스

내부 서비스

제8장 시장 추산 및 예측 : 치료 영역별, 2021년-2034년

주요 동향

자가면역 질환

종양

순환기 영역

감염증

피부과

안과

신경

혈액 내과

기타 치료 영역

제9장 시장 추산 및 예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

폴란드

네덜란드

스위스

아시아태평양

중국

일본

인도

호주

한국

싱가포르

말레이시아

인도네시아

태국

필리핀

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트(UAE)

제10장 기업 개요

Charles River Laboratories

Clinipace

Eli Lilly and Company

ICON

IQVIA

Laboratory Corporation of America Holdings(Covance Inc)

Medpace

Merck &Co

Parexel International Corporation

Pfizer

SGS SA

Syneos Health

The Emmes Company

Thermo Fisher Scientific(PPD)

Veeda Clinical Research

Worldwide Clinical Trials

WuXi AppTech

LSH

영문 목차

영문목차

The Global Clinical Trials Market was valued at USD 59 billion in 2024 and is projected to grow at a CAGR of 5.2% between 2025 and 2034. The rising demand for advanced treatment options, coupled with increasing investments in drug development, is driving market expansion. As chronic diseases such as cancer, diabetes, and cardiovascular conditions become more prevalent, pharmaceutical and biotechnology companies are ramping up their efforts to introduce innovative therapies. The surge in clinical research activity reflects a broader shift toward precision medicine and targeted treatments, further fueling growth in the clinical trials sector. Additionally, technological advancements such as artificial intelligence (AI), big data analytics, and decentralized trials are transforming clinical research, making trials more efficient and cost-effective. Regulatory support for fast-track drug approvals and increased collaboration between research institutions and healthcare providers are also contributing to market expansion. With an increasing focus on patient-centric approaches and adaptive trial designs, the clinical trials market is set to witness significant evolution in the coming years.

The clinical trials market is segmented by phase into Phase I, II, III, and IV. Among these, Phase III dominates the sector, accounting for USD 29.3 billion in 2024. These large-scale trials are critical for validating a drug's safety and efficacy before regulatory approval. Given their complexity and the need for diverse patient populations, Phase III studies are conducted across multiple locations to generate comprehensive clinical data. As companies push forward with novel drug formulations and biosimilars, the demand for extensive Phase III trials continues to rise, reinforcing this segment's leading position in the market.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$59 Billion

Forecast Value

$98.9 Billion

CAGR

5.2%

Based on study design, clinical trials are categorized into interventional, observational, and expanded access studies. The interventional study segment led the market in 2024 and is anticipated to grow at a CAGR of 5% from 2025 to 2034. These studies play a pivotal role in determining the efficacy of new medical interventions by actively involving participants in controlled treatment protocols. By eliminating recall bias and offering a structured evaluation of treatment outcomes, interventional trials provide the highest level of clinical evidence. As a result, pharmaceutical companies and regulatory bodies increasingly rely on these studies to accelerate drug approvals and enhance treatment standards.

North America Clinical Trials Market held a 54.6% share in 2024, maintaining its dominance due to a high concentration of pharmaceutical and biotechnology companies. With the growing complexity of drug development, particularly in precision medicine and biologics, companies across the region are investing heavily in clinical trials to bring next-generation treatments to market. Strong regulatory frameworks, well-established research infrastructure, and increased funding for clinical studies further support North America's leadership in the sector. As demand for innovative therapies escalates, the region is poised for continued growth, reinforcing its pivotal role in global clinical research.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Base estimates and calculations

1.3.1 Base year calculation

1.3.2 Key trends for market estimation

1.4 Forecast model

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing prevalence of chronic diseases across the globe

3.2.1.2 Growing demand for outsourcing clinical trials to CROs

3.2.1.3 Rise in government and non-government funding for clinical trials

3.2.1.4 Growing opportunities for conducting clinical trials in countries of Asia Pacific

3.2.2 Industry pitfalls and challenges

3.2.2.1 Lack of skilled workforce in clinical research

3.2.2.2 Infrastructural barriers in developing countries

3.2.2.3 Challenges faced in North America and Europe for conducting clinical trials

3.3 Growth potential analysis

3.4 Clinical trials volume analysis

3.4.1 Clinical trials volume analysis, by region, 2021 - 2024

3.4.2 Clinical trials volume analysis, by phase of development, 2021 - 2024

3.4.3 Clinical trials volume analysis, by indication, 2021 - 2024

3.5 Regulatory landscape

3.5.1 U.S.

3.5.2 Europe

3.5.3 Asia Pacific

3.5.3.1 Singapore

3.5.3.2 Malaysia

3.5.3.3 Indonesia

3.5.3.4 Thailand

3.5.3.5 South Korea

3.5.3.6 Philippines

3.6 Clinical trials - Asia Pacific advantage

3.7 Porters analysis

3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company matrix analysis

4.3 Merger and acquisition landscape

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Phase, 2021 – 2034 ($ Mn)

5.1 Key trends

5.2 Phase I

5.3 Phase II

5.4 Phase III

5.5 Phase IV

Chapter 6 Market Estimates and Forecast, By Study Design, 2021 – 2034 ($ Mn)

6.1 Key trends

6.2 Interventional study

6.3 Observational study

6.4 Expanded access study

Chapter 7 Market Estimates and Forecast, By Service Type, 2021 – 2034 ($ Mn)

7.1 Key trends

7.2 Outsourcing service

7.3 In-house service

Chapter 8 Market Estimates and Forecast, By Therapeutic Area, 2021 – 2034 ($ Mn)

8.1 Key trends

8.2 Autoimmune disease

8.3 Oncology

8.4 Cardiology

8.5 Infectious disease

8.6 Dermatology

8.7 Ophthalmology

8.8 Neurology

8.9 Hematology

8.10 Other therapeutic areas

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

9.1 Key trends

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.3 Europe

9.3.1 Germany

9.3.2 UK

9.3.3 France

9.3.4 Spain

9.3.5 Italy

9.3.6 Poland

9.3.7 Netherlands

9.3.8 Switzerland

9.4 Asia Pacific

9.4.1 China

9.4.2 Japan

9.4.3 India

9.4.4 Australia

9.4.5 South Korea

9.4.6 Singapore

9.4.7 Malaysia

9.4.8 Indonesia

9.4.9 Thailand

9.4.10 Philippines

9.5 Latin America

9.5.1 Brazil

9.5.2 Mexico

9.5.3 Argentina

9.6 Middle East and Africa

9.6.1 Saudi Arabia

9.6.2 South Africa

9.6.3 UAE

Chapter 10 Company Profiles

10.1 Charles River Laboratories

10.2 Clinipace

10.3 Eli Lilly and Company

10.4 ICON

10.5 IQVIA

10.6 Laboratory Corporation of America Holdings (Covance Inc)