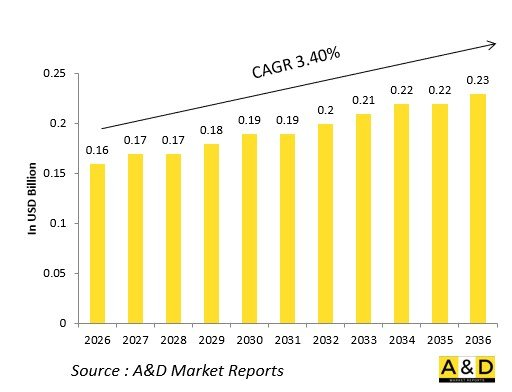

세계의 방위용 점화 익사이터 시장 규모는 2026년에 1억 6,000만 달러로 추정되며, 2036년까지 2억 3,000만 달러에 달할 것으로 예측되며, 2026-2036년의 예측 기간 중 CAGR 3.40%의 성장이 전망되고 있습니다.

세계의 방위형 점화 익사이터 시장은 점화 플러그에 정밀한 용량 방전을 발생시켜 터빈 코어의 시동, 재점화 또는 애프터 버너 전환 시 연소를 시작합니다. 이중 리던던트 채널은 고전압 커패시터에 에너지를 저장하고 변압기 절연기를 통한 FADEC 명령으로 작동합니다.

스크램블 준비 태세에 대한 지정학적 수요가 개발을 추진하고 있으며, 전자기 펄스나 합성 연료에 내성이 있는 시스템이 중시되고 있습니다. 오픈 아키텍처는 엔진 패밀리 간의 통합을 지원합니다. 공급망은 내방사성 반도체와 세라믹 절연체에 주력하고 있습니다. 경쟁에서 Honeywell, Collins Aerospace 및 TransDigm은 레이저 기반 변종 개발을 주도하고 있습니다.

방위형 점화 익사이터의 기술 영향

고체 커패시터 방전은 폭발하는 브리지 와이어를 대체하여 소모품의 열화 없이 안정적인 kV 펄스를 제공합니다. 탄화 규소 정류기는 지속적인 애프터 버너의 재점화에 대응하고, 기존 셀레늄 스택에 비해 서비스 간격을 2배로 연장합니다.

FADEC 통합 상태 모니터링은 방전 파형을 분석하고 아크 통과 전에 절연체의 추적을 감지합니다. 레이저 플라즈마 점화 익사이터는 광섬유를 통해 kW급 빔을 집중시켜 여러 개의 플러그 팁을 동시에 점화하여 균일한 화염 핵을 형성합니다. 임베디드 변류기는 마이크로초 단위로 아크의 형성을 검증합니다.

고도의 연료 분사 패턴에 대해 디지털 트윈 기술은 펄스 타이밍을 최적화합니다. 방사선 저항성 갈륨 질화물 스위치는 핵 환경에서도 작동을 계속합니다. 듀얼 주파수 익사이터는 선택 가능한 파형으로 드라이 터빈 시동과 습식 애프터 버너 점화를 지원합니다.

예측 알고리즘은 전압 상승의 특성으로부터 점화 익사이터의 교체 시기를 알려줍니다. 콤팩트 익사이터는 팬 케이스에 직접 통합되어 하네스 배선을 필요로 하지 않습니다. 가변 에너지 회로는 수소화 합성 연료에 대응하여 스파크 강도를 조정합니다. 이러한 혁신은 완전 정지 상태에서 점화를 보장합니다.

방위형 점화 익사이터의 주요 촉진요인

적응 사이클 엔진에는 가변 바이패스 이행시 연속 재점화가 요구됩니다. 무인 플랫폼에서는 지상 카트가 필요없는 자율 점화가 필수적입니다.

유지관리에서는 예지보전 엑사이터의 채용에 의해 정기적인 분해점검이 불필요합니다. 수출 프로그램은 연합군 전체에서의 전자기 펄스 내성 강화가 요구됩니다. 극한 환경 하에서의 신뢰성 확보에는 빙점 하에서의 점화 성공이 필수입니다.

예산면에서는 군용 규격 인정을 취득한 상용 파생품의 채용이 유리합니다. 공급 탄력성은 국내 팹에 의한 반도체 부족 대책을 실현합니다. 상호 운용성은 각 엔진 패밀리의 인터페이스의 공통화를 가능하게 합니다.

지향성 에너지의 전력 추출에는 높은 신뢰성의 점화 시퀀싱이 요구됩니다. 이로 인해 엑사이터는 연소의 인에이블러가 되었습니다.

본 보고서에서는 세계의 방위용 이그니션 익사이터 시장에 대해 조사 분석하여 시장에 영향을 미치는 기술, 향후 10년간의 예측, 각 지역의 동향 등의 정보를 제공합니다.

플랫폼별

에너지 출력별

점화 유형별

북미

촉진요인, 억제요인, 과제

PEST

주요 기업

공급자의 Tier 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

미국

방위 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The Global Defense Ignition Exciters Market is estimated at USD 0.16 billion in 2026, projected to grow to USD 0.23 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.40% over the forecast period 2026-2036.

The global Defense Ignition Exciters market generates precise capacitive discharges to arc igniter plugs, initiating combustion in turbine cores during startup, relight, or afterburner transitions. Dual-redundant channels store energy in high-voltage capacitors, triggered by FADEC commands through transformer-isolators.

Geopolitical demands for scramble readiness drive development, prioritizing systems tolerant of electromagnetic pulses and synthetic fuels. Open architectures support integration across engine families. Supply chains focus on radiation-hardened semiconductors and ceramic insulators. Competition features Honeywell, Collins Aerospace, and TransDigm pioneering laser-based variants.

Technology Impact in Defense Ignition Exciters

Solid-state capacitor discharge replaces exploding bridge wires, delivering consistent kV pulses without consumables degradation. Silicon carbide rectifiers handle sustained afterburner relights, doubling service intervals versus legacy selenium stacks.

FADEC-integrated health monitoring analyzes discharge waveforms, detecting insulator tracking before arc-through. Laser plasma igniters focus kilowatt beams through fiber optics, striking multiple plug tips simultaneously for uniform flame kernels. Embedded current transformers validate arc formation within microseconds.

Digital twins optimize pulse timing against fuel spray patterns at altitude. Radiation-hardened gallium nitride switches survive nuclear environments. Dual-frequency exciters support dry turbine starts and wet afterburner lighting through selectable waveforms.

Predictive algorithms cue igniter swaps from voltage-rise signatures. Compact exciters integrate directly into fan cases, eliminating harness runs. Variable energy circuits adjust spark strength for hydrogenated synthetics. These innovations ensure light-off from cold-and-dark states.

Key Drivers in Defense Ignition Exciters

Adaptive cycle engines demand continuous relight during variable bypass transitions. Unmanned platforms require autonomous ignition without ground carts.

Sustainment prioritizes prognostic exciters eliminating scheduled removals. Export programs need electromagnetic pulse hardening across coalitions. Arctic cold soaks mandate sub-zero light-off reliability.

Budget favors commercial derivatives with mil-spec qualification. Supply resilience counters semiconductor shortages via domestic fabs. Interoperability enables common interfaces across engine families.

Directed-energy power extraction requires high-reliability ignition sequencing. These position exciters as combustion enablers.

Regional Trends in Defense Ignition Exciters

North America dominates F-35 sustainment, pioneering laser plasma for STOVL relights.

Europe upgrades Rafale/Typhoon exciters for dispersed basing with synthetic fuels.

Asia-Pacific surges with indigenous programs-India's Kaveri, China's WS-15-prioritizing high-altitude starts.

Middle East adapts circuits for desert overtemps.

Russia hardens systems for Su-57 nuclear missions.

South Korea integrates KF-21 with radiation-tolerant designs.

Trends favor solid-state; Asia-Pacific captures growth.

Key Defense Ignition Exciters Programs

F135 exciters power STOVL transitions and afterburner relights across variants.

NGAD laser plasma enables variable cycle combustion stability.

EJ200 upgrades deliver supercruise dry starts via optimized capacitors.

Kaveri equips Tejas with indigenous silicon avalanche circuits.

F119 systems sustain stealth missions with EMP-hardened stacks.

Rafale M88 integrates carrier catapult ignition surges.

Su-57 AL-41F1 supports 3D thrust vectoring light-offs.

T-50 FADEC-controlled dual-frequency prevents flameout cascades.

By Platform

By Energy Output

By Ignition Type

The 10-year Defense Ignition Exciters market analysis would give a detailed overview of Defense Ignition Exciters market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year Defense Ignition Exciters market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.