유전자 치료 시장 : 치료 분야별, 벡터 유형별, 치료 유형별, 유전자 전달 방법별, 투여 경로별, 지역별, 주요 기업, 매출 예측 : 산업 동향 및 세계 예측(-2035년)

Gene Therapy Market by Therapeutic Area, Type of Vector, Type of Therapy, Type of Gene Delivery Method, Route of Administration, Geographical Regions, Leading Players and Sales Forecast: Industry Trends and Global Forecasts, Till 2035

상품코드:1616873

리서치사:Roots Analysis

발행일:2024년 12월

페이지 정보:영문 972 Pages

라이선스 & 가격 (부가세 별도)

한글목차

세계 유전자 치료 시장 규모는 2035년까지 예측 기간 동안 19.25%의 CAGR로 확대되어 현재 24억 달러에서 2035년까지 165억 달러로 성장할 것으로 예상됩니다.

선천성 기형이나 유전성 유전자 변이는 암 질환, 유전성 질환, 자가면역질환, 신경질환 등 다양한 질환을 포괄합니다. 세계보건기구(WHO)에 따르면, 유전성 질환은 1,000명당 10명이 앓고 있으며, 그 결과 전 세계적으로 7,000만 명 이상이 이러한 질환을 안고 살아가고 있습니다. 특히, 전 세계 영아 사망률의 40% 이상이 다양한 유전적 질환과 관련이 있습니다. 현재 개별 환자의(돌연변이된, 질병을 유발하는) 유전자를 선택적으로 교정하는 안전하고 효과적인 방법을 개발하기 위한 여러 연구 개발이 진행 중입니다. 그 중 유전자 치료가 유망한 대안으로 떠오르고 있습니다. 이러한 치료법은 돌연변이된 유전자의 건강한 버전을 도입하거나 체내에서 질병을 유발하는 유전자의 기능을 비활성화하여 질병의 근본적인 유전적 원인을 표적으로 삼도록 고안되었습니다. 지난 몇 년 동안 1,100건 이상의 유전자 치료 관련 임상시험이 등록되었다는 점은 주목할 만합니다. 또한 미국 FDA에 따르면 2025년까지 매년 10-20개의 치료법이 시장에 진입할 것으로 예상됩니다. 유전자 치료 기업들의 공동 노력과 효과적인 단회 투여 치료에 대한 선호도가 높아짐에 따라 유전자 치료 시장은 예측 기간 동안 큰 성장을 이룰 것으로 예상됩니다.

이 보고서는 세계 유전자 치료 시장을 조사하여 시장 개요와 함께 치료 분야별, 벡터 유형별, 치료 유형별, 유전자 전달 방법별, 투여 경로별, 지역별 동향, 시장 진입 기업 프로파일 등을 제공합니다.

목차

제1장 서문

제2장 조사 방법

제3장 시장 역학

제4장 경제적 고려

제5장 주요 요약

제6장 소개

분석 개요

유전자 치료의 진화

유전자 치료 분류

투여 경로

유전자 치료 작용기서

유전자 치료의 장단점

유전자 치료에 따른 과제

유전체 편집 소개

결론

제7장 유전자 전달 벡터

분석 개요

유전자 도입 방법

유전자 재조합 치료를 위한 바이러스 벡터

유전자 재조합 치료를 위한 비바이러스 벡터

제8장 규제 상황과 상환 시나리오

분석 개요

북미의 규제 가이드라인

유럽의 규제 가이드라인

아시아태평양의 규제 가이드라인

상환 시나리오

결론과 향후 전망

제9장 시장 상황

제10장 개발자 상황

분석 개요

유전자 치료 : 경쟁 구도

제11장 기업 개요

제12장 출시된 유전자 치료

제13장 주요 상업화 전략

제14장 후기 유전자 치료

분석 개요

LUMEVOQ (GS010)

OTL-103

PTC-AADC

BMN 270

rAd-IFN/Syn3

beti-cel

eli-cel

lovo-cel

SRP-9001

EB-101

ProstAtak

D-Fi

CG0070

Vigil-EWS

Engensis

VGX-3100

INVOSSA (TG-C)

VYJUVEKT

PF-06939926

PF06838435

PF-07055480

SPK-8011

AMT-061

VB-111

Generx

ADXS-HPV

AGTC 501

LYS-SAF302

NFS-01

AG0302-COVID19

RGX-314

Hologene 5

제15장 특허 분석

제16장 인수합병

제17장 자금 조달과 투자

제18장 임상시험 분석

제19장 원가분석

제20장 스타트업 평가

제21장 대형 제약회사의 대처

제22장 수요 분석

제23장 시장 영향 분석 : 촉진요인, 제약요인, 기회, 과제

제24장 세계의 유전자 치료 시장

제25장 유전자 치료 시장, 치료 분야별

제26장 유전자 치료 시장, 벡터 유형별

제27장 유전자 치료 시장, 치료 유형별

제28장 유전자 치료 시장, 유전자 전달 방법별

제29장 유전자 치료 시장, 투여 경로별

제30장 유전자 치료 시장, 지역별

제31장 유전자 치료 시장, 주요 기업별

제32장 유전자 치료 시장, 치료제 매출 예측

제33장 유전자 치료 시장 : 신기술

제34장 유전자 치료용 벡터 제조

제35장 사례 연구 : 유전자 치료 공급망

제36장 이그제큐티브 인사이트

제37장 결론

제38장 부록 I : 표형식 데이터

제39장 부록 II : 기업 및 단체 리스트

ksm

영문 목차

영문목차

GENE THERAPY MARKET: OVERVIEW

As per Roots Analysis, the global gene therapy market is estimated to grow from USD 2.4 billion in the current year to USD 16.5 billion by 2035, at a CAGR of 19.25% during the forecast period, till 2035.

The market sizing and opportunity analysis has been segmented across the following parameters:

Therapeutic Area

Cardiovascular Disorders

Dermatological Disorders

Genetic Disorders

Hematological Disorders

Metabolic Disorders

Muscle Disorders

Oncological Disorders

Ophthalmic Disorders

Other Disorders

Type of Vector

Adeno-associated Virus Vectors

Adenovirus Vectors

Herpes Simplex Virus Vectors

Lentivirus Vectors

Non-viral Vectors

Retrovirus Vectors

Other Viral Vectors

Type of Therapy

Gene Augmentation

Gene Editing

Gene Regulation

Oncolytic Immunotherapies

Other Therapies

Type of Gene Delivery Method

Ex vivo Gene Delivery

In vivo Gene Delivery

Route of Administration

Intramuscular Route

Intratumoral Route

Intravenous Route

Subretinal Route

Other Routes of Administration

Key Geographical Regions

North America

Europe

Asia-Pacific

Latin America

Rest of the World

GENE THERAPY MARKET: GROWTH AND TRENDS

Congenital abnormalities and inherited genetic mutations encompass a diverse range of disorders, including oncological disorders, genetic disorders, autoimmune disorders and neurological disorders. According to the World Health Organization (WHO), genetic disorders affect 10 out of every 1,000 individuals, resulting in over 70 million people living with these conditions globally. Notably, more than 40% of infant mortality worldwide is linked to various genetic disorders. At present, several research initiatives are underway to develop safe and effective methods to selectively correct (the mutated, disease-causing) genes of individual patients. Of these, gene therapies have emerged as a promising option. These therapies are designed to target the underlying genetic cause of a disease, either by introducing a healthy version of the mutated gene or by disabling the functions of genes that cause the disease within the body. It is worth highlighting that over 1,100 clinical trials related to gene therapies have been registered in the past few years, indicating substantial research activity. Additionally, as per the USFDA, 10 to 20 therapies are expected to gain market access, each year, till 2025. Driven by the collaborative efforts of gene therapy companies and an increasing preference for effective single-dose treatments, the gene therapy market is set to experience significant growth during the forecast period.

GENE THERAPY MARKET: KEY INSIGHTS

The report delves into the current state of the gene therapy market and identifies potential growth opportunities within the industry. Some key findings from the report include:

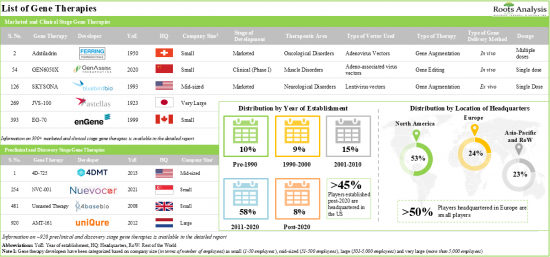

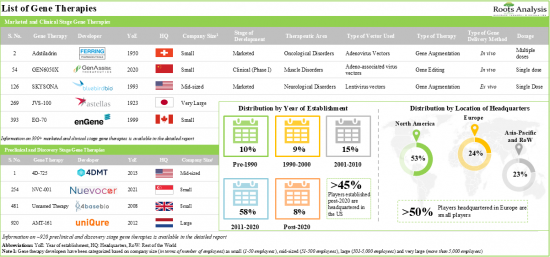

1. Presently, 345 developers, worldwide, are engaged in the development of gene therapies targeting various disorders; of these, more than 50% of the stakeholders are headquartered in the US, alone.

2. 70% of the gene therapies being evaluated in phase III clinical trials are gene augmentation therapies; it is worth noting that more than 35% of the candidates have received fast track designation.

3. Close to 95% of the preclinical stage gene therapies are in vivo therapies; more than 20% of the gene therapy candidates are being developed for the treatment of neurological disorders.

4. Over the years, the intellectual capital related to gene therapies has grown at a commendable pace; several patents have been filed by both industry stakeholders and academic players.

5. Over 500 patents focused on gene editing have been filed in the past five years; till date, 6% of such patents have been granted.

6. Rising interest of the stakeholders in this domain is reflected by the number of mergers and acquisitions reported over the last few years; 26% of these initiatives were focused on gaining access to novel platforms.

7. Foreseeing lucrative opportunities, many public and private investors have made investments worth USD 36.4 billion, across more than 560 funding instances.

8. In the recent past, more than 18,000 patients have been enrolled in clinical trials focused on gene therapies; close to 45% trials are evaluating gene therapies for the treatment of oncological disorders.

9. Start-ups are spearheading the innovation in the gene therapy domain; the valuation of a start-up is not solely dependent on profits, instead, it depends on experience and amount previously invested by industry stakeholders.

10. In order to tap into the lucrative opportunity associated with gene therapies, big pharma players have adopted various approaches, from proprietary product development to strategic investments, to advance their portfolios.

11. Given the growing incidence of inherited disorders, the demand for gene therapies (in terms of number of patients) has risen; by 2035, it is anticipated to grow at an annualized rate of 11.67%, across various geographies.

12. Owing to the growing interest towards personalized medicines and high specificity, the market for gene therapies is expected to rise steadily in the foreseeable future.

13. The gene therapy market is anticipated to grow at an annualized rate (CAGR) of 19.25%, till 2035; North America is expected to capture the majority share (close to 65%) of the market by 2035.

GENE THERAPY MARKET: KEY SEGMENTS

Currently, Muscle Disorders Segment Occupies the Largest Share of the Gene Therapy Market

Based on the therapeutic area, the market is segmented into cardiovascular disorders, dermatological disorders, genetic disorders, hematological disorders, metabolic disorders, muscle disorders, oncological diseases, ophthalmic disorders and other disorders. At present, muscle disorders segment holds the maximum share of the gene therapy market. This can be attributed to the growing prevalence of muscle disorders and proven efficacy of gene therapies in treating such conditions.

Adeno-Associated Virus (AAV) Vector-Based Gene Therapies is Likely to Dominate the Gene Therapies Market During the Forecast Period

Based on the type of vector, the market is segmented into adeno-associated virus vectors, adenovirus vectors, herpes simplex virus vectors, lentivirus vectors, non-viral vectors, retrovirus vectors and other viral vectors. At present, AAV vector-based gene therapies holds the maximum share within the gene therapies market. It is worth highlighting that, owing to the numerous advantages of AAV vector, such as high target specificity, greater efficacy and infectivity, AAV vector-based gene therapies are likely to capture larger share in the coming decade.

Currently, Gene Augmentation Segment Occupies the Largest Share of the Gene Therapies Market

Based on the type of therapy, the market is segmented into gene augmentation, gene editing, gene regulation, oncolytic immunotherapies and other therapies. Owing to their ability to deliver therapeutic genes to the patient's genome, fewer side effects and precisely correcting the genomic mutations, the gene therapy market is currently dominated by gene augmentation therapies. This trend is likely to remain the same in the mid-to-long term.

In Vivo Gene Delivery Method is Likely to Dominate the Gene Therapies Market During the Forecast Period

Based on the type of gene delivery method, the market is segmented into ex vivo and in vivo gene delivery methods. It is worth highlighting that, at present, in vivo gene delivery method holds a larger share of the gene therapy market. This trend is likely to remain the same in the coming decade.

Intravenous Route of Administration is Likely to Dominate the Gene Therapy Market During the Forecast Period

Based on the route of administration, the market is segmented into intramuscular, intratumoral, intravenous, subretinal and other routes of administration. It is worth highlighting that majority of the current gene therapy market is captured by the intravenous route of administration and this trend is unlikely to change in mid-long term. This can be attributed to the fact that gene therapies allow widespread distribution of the gene-carrying therapeutic vector to multiple target organs. In addition, intravenous administration is easier to administer and minimally invasive compared to other methods like intralesional or intratumoral injection.

North America Accounts for the Largest Share of the Market

Based on the key geographical regions, the market is segmented into North America, Europe, Asia-Pacific, Latin America and Rest of the World. Majority share is expected to be captured by drug developers based in North America. It is worth highlighting that, over the years, the market for Europe is expected to grow at a higher CAGR.

Example Players in the Gene Therapy Market

Amgen

Artgen Biotech

BioMarin Pharmaceutical

bluebird bio

CRISPR Therapeutics

CSL Behring

Ferring Pharmaceuticals

Kolon TissueGene

Krystal Biotech

Novartis

Orchard Therapeutics

Pfizer

PTC Therapeutics

Sarepta Therapeutics

Shanghai Sunway Biotech

Sibiono GeneTech

Spark Therapeutics

Primary Research Overview

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders. The research report features detailed transcripts of interviews held with the following industry stakeholders:

Former Corporate Communications Manager, Orchard Therapeutics

Co-Founder and Chief Executive Officer, Vivet Therapeutics

Chief Executive Officer, Chairman and President, Kubota Pharmaceutical

Former Chief Executive Officer and President, Eyevensys

Former Chief Executive Officer and President, AGTC

Former Chief Business Officer, LogicBio Therapeutics

Founder and Chief Executive Officer, AAVogen

Chief Executive Officer, Hemera Biosciences

Ex Co-Founder, Chief Executive Officer and President, Myonexus Therapeutics

Former Chief Executive Officer, Arthrogen

Project Manager and Tatjana Buchholz, Former Marketing Manager, PlasmidFactory

Former Executive and Scientific Director, Delphi Genetics

Former Chief Commercial Officer, Vigene Biosciences

Chief Executive Officer and Chairman, Gene Biotherapeutics

Chief Executive Officer, Milo Biotechnology

GENE THERAPY MARKET: RESEARCH COVERAGE

Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the gene therapy market, focusing on key market segments, including [A] therapeutic area, [B] type of vector, [C] type of therapy, [D] type of gene delivery method, [E] route of administration, [F] geographical regions and [H] leading players.

Market Landscape (Gene Therapies): A comprehensive evaluation of marketed and clinical stage gene therapies, considering various parameters, such as [A] stage of development, [B] drug designations, [C] therapeutic area, [D] target gene, [E] type of vector used, [F] type of therapy, [G] type of gene delivery method, [H] route of administration and [I] dosing frequency. The chapter also provides a detailed analysis of the current landscape of discovery and preclinical stage gene therapies based on parameters, such as [J] stage of development, [K] therapeutic area, [L] target gene, [M] type of vector used, [N] type of therapy and [O] type of gene delivery method.

Market Landscape (Gene Therapy Developers): A comprehensive evaluation of gene therapy developers, considering various parameters, such as [A] year of establishment, [B] company size (in terms of number of employees), [C] location of headquarters and [D] most active players (in terms of the number of gene therapies developed).

Company Profiles: In-depth profiles of key industry players engaged in the development of gene therapies, focusing on [A] company overviews, [B] financial information (if available), [C] gene therapy portfolio, [D] recent developments and [E] an informed future outlook.

Drug Profiles: In-depth profiles of marketed and late stage (phase II / III and above) gene therapies, along with information on the [A] development timeline of the therapy, [B] mechanism of action, [C] type of vector used, [D] dosage and manufacturing details, [E] target indication, as well as [F] details related to the developer company.

Commercialization Strategy: An elaborate discussion on the various commercialization strategies that have been adopted by drug developers engaged in the gene therapy domain across different stages of therapy development, including prior to drug launch, at / during drug launch and post-marketing stage.

Patent Analysis: Detailed analysis of various patents filed / granted related to gene therapies and gene editing therapies based on [A] type of patent, [B] publication year, [C] regional applicability, [D] CPC symbols, [E] emerging focus areas, [F] leading industry players (in terms of the number of patents filed / granted), and [G] patent valuation. It also includes a [H] patent benchmarking analysis and [I] a detailed valuation analysis.

Merger and Acquisitions: A comprehensive examination of the various mergers and acquisitions, focusing on multiple relevant parameters, including [A] year of agreement, [B] type of deal, [C] geographical location of the companies involved, [D] key value drivers, [E] highest phase of development of the acquired company' product, [F] target therapeutic area and [G] deal multiples.

Funding and Investment Analysis: A detailed evaluation of the investments made in the gene therapy domain, encompassing seed financing, venture capital financing, IPOs, secondary offerings, debt financing, grants and other equity offerings.

Clinical Trial Analysis: Examination of completed, ongoing, and planned clinical studies of various gene therapies, based on parameters, such as [A] trial registration year, [B] trial status, [C] trial phase, [D] target therapeutic area, [E] geography, [F] type of sponsor, [G] prominent treatment sites and [H] enrolled patient population.

Pricing Analysis: An analysis of the various factors that are likely to influence the pricing of gene therapies, featuring different models / approaches that may be adopted by developers / manufacturers to decide the prices of these therapies.

Start-up Valuation Analysis: An analysis of the startup companies engaged in this domain (since 2017) based on year of experience.

Big Pharma Analysis: A comprehensive examination of various gene therapy-based initiatives undertaken by major pharmaceutical companies, based on several relevant parameters, such as [A] therapeutic area, [B] type of vector used, [C] type of therapy and [D] type of gene delivery method used. In addition, it includes a detailed benchmarking analysis across key parameters, such as [E] number of gene therapies under development, [F] funding information, [G] partnership activity and [H] patent portfolio strength.

Demand Analysis: Informed estimates of the annual commercial and clinical demand for gene therapies based on several relevant parameters, such as [A] target patient population, [B] dosing frequency and [C] dose strength.

Additional Insight 1: A review of the various emerging technologies and therapy development platforms that are being used to manufacture gene therapies, featuring detailed profiles of technologies that are being used for the development of gene therapies.

Additional Insight 2: A case study examining the current and emerging trends in vector manufacturing, along with details on companies that provide contract services for producing viral vectors utilized in gene therapy products. The analysis also includes an in-depth discussion of the manufacturing processes associated with different types of vectors.

Additional Insight 3: Assessment of the supply chain model adopted by gene therapy developers highlighting the stakeholders involved, factors affecting the supply of therapeutic products and challenges encountered by developers across the different stages of the gene therapy supply chain.

Market Impact Analysis: The report analyzes various factors such as drivers, restraints, opportunities, and challenges affecting the market growth.

KEY QUESTIONS ANSWERED IN THIS REPORT

How many companies are currently engaged in this market?

Which are the leading companies in this market?

What is the annual demand for gene therapies?

What factors are likely to influence the evolution of this market?

What is the current and future market size?

What is the CAGR of this market?

How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

Complimentary PPT Insights Packs

Complimentary Excel Data Packs for all Analytical Modules in the Report

10% Free Content Customization

Detailed Report Walkthrough Session with Research Team

Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

1.1. Introduction

1.2. Market Share Insights

1.3. Key Market Insights

1.4. Report Coverage

1.5. Key Questions Answered

1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

2.1. Chapter Overview

2.2. Research Assumptions

2.2.1. Market Landscape and Market Trends

2.2.2. Market Forecast and Opportunity Analysis

2.2.3. Comparative Analysis

2.3. Database Building

2.3.1. Data Collection

2.3.2. Data Validation

2.3.3. Data Analysis

2.4. Project Methodology

2.4.1. Secondary Research

2.4.1.1. Annual Reports

2.4.1.2. Academic Research Papers

2.4.1.3. Company Websites

2.4.1.4. Investor Presentations

2.4.1.5. Regulatory Filings

2.4.1.6. White Papers

2.4.1.7. Industry Publications

2.4.1.8. Conferences and Seminars

2.4.1.9. Government Portals

2.4.1.10. Media and Press Releases

2.4.1.11. Newsletters

2.4.1.12. Industry Databases

2.4.1.13. Roots Proprietary Databases

2.4.1.14. Paid Databases and Sources

2.4.1.15. Social Media Portals

2.4.1.16. Other Secondary Sources

2.4.2. Primary Research

2.4.2.1. Types of Primary Research

2.4.2.1.1. Qualitative Research

2.4.2.1.2. Quantitative Research

2.4.2.1.3. Hybrid Approach

2.4.2.2. Advantages of Primary Research

2.4.2.3. Techniques for Primary Research

2.4.2.3.1. Interviews

2.4.2.3.2. Surveys

2.4.2.3.3. Focus Groups

2.4.2.3.4. Observational Research

2.4.2.3.5. Social Media Interactions

2.4.2.4. Key Opinion Leaders Considered in Primary Research

2.4.2.4.1. Company Executives (CXOs)

2.4.2.4.2. Board of Directors

2.4.2.4.3. Company Presidents and Vice Presidents

2.4.2.4.4. Research and Development Heads

2.4.2.4.5. Technical Experts

2.4.2.4.6. Subject Matter Experts

2.4.2.4.7. Scientists

2.4.2.4.8. Doctors and Other Healthcare Providers

2.4.2.5. Ethics and Integrity

2.4.2.5.1. Research Ethics

2.4.2.5.2. Data Integrity

2.4.3. Analytical Tools and Databases

3. MARKET DYNAMICS

3.1. Chapter Overview

3.2. Forecast Methodology

3.2.1. Top-down Approach

3.2.2. Bottom-up Approach

3.2.3. Hybrid Approach

3.3. Market Assessment Framework

3.3.1. Total Addressable Market (TAM)

3.3.2. Serviceable Addressable Market (SAM)

3.3.3. Serviceable Obtainable Market (SOM)

3.3.4. Currently Acquired Market (CAM)

3.4. Forecasting Tools and Techniques

3.4.1. Qualitative Forecasting

3.4.2. Correlation

3.4.3. Regression

3.4.4. Extrapolation

3.4.5. Convergence

3.4.6. Sensitivity Analysis

3.4.7. Scenario Planning

3.4.8. Data Visualization

3.4.9. Time Series Analysis

3.4.10. Forecast Error Analysis

3.5. Key Considerations

3.5.1. Demographics

3.5.2. Government Regulations

3.5.3. Reimbursement Scenarios

3.5.4. Market Access

3.5.5. Supply Chain

3.5.6. Industry Consolidation

3.5.7. Pandemic / Unforeseen Disruptions Impact

3.6. Key Market Segmentation

3.7. Robust Quality Control

3.8. Limitations

4. ECONOMIC CONSIDERATONS

4.1. Chapter Overview

4.2. Market Dynamics

4.2.1. Time Period

4.2.1.1. Historical Trends

4.2.1.2. Current and Forecasted Estimates

4.2.2. Currency Coverage

4.2.2.1. Overview of Major Currencies Affecting the Market

4.2.2.2. Impact of Currency Fluctuations on the Industry

4.2.3. Foreign Exchange Impact

4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

4.2.4. Recession

4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

4.2.5. Inflation

4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

4.2.5.2. Potential Impact of Inflation on the Market Evolution

5. EXECUTIVE SUMMARY

6. INTRODUCTION

6.1. Chapter Overview

6.2. Evolution of Gene Therapies

6.3. Classification of Gene Therapies

6.3.1. Based on Source of Origin

6.3.2. Based on Method of Delivery

6.3.2.1. Ex vivo Gene Therapies

6.3.2.2. In vivo Gene Therapies

6.4. Routes of Administration

6.5. Mechanism of Action of Gene Therapies

6.6. Advantages and Disadvantages of Gene Therapies

6.7. Challenges associated with Gene Therapies

6.7.1. Ethical and Social Challenges

6.7.2. Therapy Development Challenges

6.7.3. Manufacturing Challenges

6.7.4. Commercial Viability Challenges

6.8. Introduction to Genome Editing

6.8.1. Evolution of Genome Editing

6.8.2. Applications of Genome Editing

6.8.3. Types of Genome Editing Techniques

6.9. Concluding Remarks

7. GENE DELIVERY VECTORS

7.1. Chapter Overview

7.2. Methods of Gene Transfer

7.3. Viral Vectors for Genetically Modified Therapies

7.3.1. Types of Viral Vectors

7.3.1.1. Adeno-associated Viral Vectors

7.3.1.2. Adenoviral Vectors

7.3.1.3. Lentiviral Vectors

7.3.1.4. Retroviral Vectors

7.3.1.5. Other Viral Vectors

7.4. Non-Viral Vectors for Genetically Modified Therapies

7.4.1. Types of Non-Viral Vectors

7.4.1.1. Plasmid DNA

7.4.1.2. Liposomes, Lipoplexes and Polyplexes

7.4.1.3. Oligonucleotides

7.4.1.4. Nanoparticles

7.4.1.5. Hybrid System Vectors

7.4.1.6. Other Non-Viral Vectors

7.4.2. Gene Delivery using Non-Viral Vectors

7.4.2.1. Biolistic Methods

7.4.2.2. Electroporation

7.4.2.3. Receptor Mediated Gene Delivery

7.4.2.4. Gene Activated matrix (GAM)

8. REGULATORY LANDSCAPE AND REIMBURSEMENT SCENARIOS

8.1. Chapter Overview

8.2. Regulatory Guidelines in North America

8.2.1. The US Scenario

8.2.2. Canadian Scenario

8.3. Regulatory Guidelines in Europe

8.3.1. Quality Documentation for Gene Therapy Products

8.3.2. Non-Clinical Development

8.3.3. Clinical Development

8.4. Regulatory Guidelines in Asia-Pacific

8.4.1. Chinese Scenario

8.4.1.1. Construction of DNA Expression Cassette and Gene Delivery Systems

8.4.1.2. Generation and Characterization of Cell Banks and Engineered Bacteria Banks

8.4.1.2.1. Cell Bank

8.4.1.2.2. Bacterial Cell Bank

8.4.1.3. Manufacturing of Gene Therapy Products

8.4.1.4. Quality Control

8.4.1.5. Evaluation of Efficacy of Gene Therapy Products

8.4.1.6. Evaluation of Safety of Gene Therapy Products

8.4.1.7. Clinical Trial of Gene Therapy Products

8.4.1.8. Ethics Study

8.4.2. Japanese Scenario

8.4.3. South Korean Scenario

8.4.4. Australian Scenario

8.4.5. Hong Kong Scenario

8.5. Reimbursement Scenario

8.5.1. Challenges Related to Reimbursement

8.6. Concluding Remarks and Future Outlook

9. MARKET LANDSCAPE

9.1. Chapter Overview

9.2. Marketed and Clinical Stage Gene Therapies: Market Landscape

9.2.1. Analysis by Stage of Development

9.2.2. Analysis by Drug Designation

9.2.3. Analysis by Therapeutic Area

9.2.4. Analysis by Target Gene

9.2.5. Analysis by Type of Vector Used

9.2.6. Analysis by Type of Therapy

9.2.7. Analysis by Type of Gene Delivery Method

9.2.8. Analysis by Route of Administration

9.2.9. Analysis by Dosing Frequency

9.3. Preclinical and Discovery Stage Gene Therapies: Market Landscape

9.3.1. Analysis by Stage of Development

9.3.2. Analysis by Therapeutic Area

9.3.3. Analysis by Target Gene

9.3.4. Analysis by Type of Vector Used

9.3.5. Analysis by Type of Therapy

9.3.6. Analysis by Type of Gene Delivery Method

10. DEVELOPER LANDSCAPE

10.1. Chapter Overview

10.2. Gene Therapy: Competitive Landscape

10.2.1. Analysis by Year of Establishment

10.2.2. Analysis by Company Size

10.2.3. Analysis by Location of Headquarters

10.2.4. Most Active Players: Analysis by Number of Gene Therapies Developed

11. COMPANY PROFILES

11.1. Chapter Overview

11.2. Gene Therapy Developers in North America

11.2.1. Amgen

11.2.1.1. Company Overview

11.2.1.2. Gene Therapy Portfolio

11.2.1.3. Recent Developments and Future Outlook

11.2.2. BioMarin Pharmaceutical

11.2.2.1. Company Overview

11.2.2.2. Gene Therapy Portfolio

11.2.2.3. Recent Developments and Future Outlook

11.2.3. bluebird bio

11.2.3.1. Company Overview

11.2.3.2. Gene Therapy Portfolio

11.2.3.3. Recent Developments and Future Outlook

11.2.4. CRISPR Therapeutics

11.2.4.1. Company Overview

11.2.4.2. Gene Therapy Portfolio

11.2.4.3. Recent Developments and Future Outlook

11.2.5. Kolon TissueGene

11.2.5.1. Company Overview

11.2.5.2. Gene Therapy Portfolio

11.2.5.3. Recent Developments and Future Outlook

11.2.6. Krystal Biotech

11.2.6.1. Company Overview

11.2.6.2. Gene Therapy Portfolio

11.2.6.3. Recent Developments and Future Outlook

11.2.7. Pfizer

11.2.7.1. Company Overview

11.2.7.2. Gene Therapy Portfolio

11.2.7.3. Recent Developments and Future Outlook

11.2.8. PTC Therapeutics

11.2.8.1. Company Overview

11.2.8.2. Gene Therapy Portfolio

11.2.8.3. Recent Developments and Future Outlook

11.2.9. Sarepta Therapeutics

11.2.9.1. Company Overview

11.2.9.2. Gene Therapy Portfolio

11.2.9.3. Recent Developments and Future Outlook

11.2.10. Spark Therapeutics

11.2.10.1. Company Overview

11.2.10.2. Gene Therapy Portfolio

11.2.10.3. Recent Developments and Future Outlook

11.3. Gene Therapy Developers in Europe

11.3.1. Artgen Biotech

11.3.1.1. Company Overview

11.3.1.2. Gene Therapy Portfolio

11.3.1.3. Recent Developments and Future Outlook

11.3.2. Ferring Pharmaceuticals

11.3.2.1. Company Overview

11.3.2.2. Gene Therapy Portfolio

11.3.2.3. Recent Developments and Future Outlook

11.3.3. Novartis

11.3.3.1. Company Overview

11.3.3.2. Gene Therapy Portfolio

11.3.3.3. Recent Developments and Future Outlook

11.3.4. Orchard Therapeutics

11.3.4.1. Company Overview

11.3.4.2. Gene Therapy Portfolio

11.3.4.3. Recent Developments and Future Outlook

11.4. Gene Therapy Developers in Asia-Pacific and Rest of the World