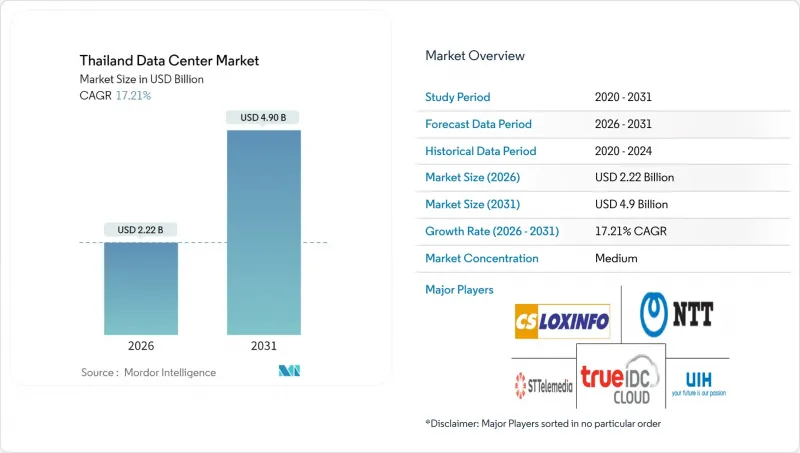

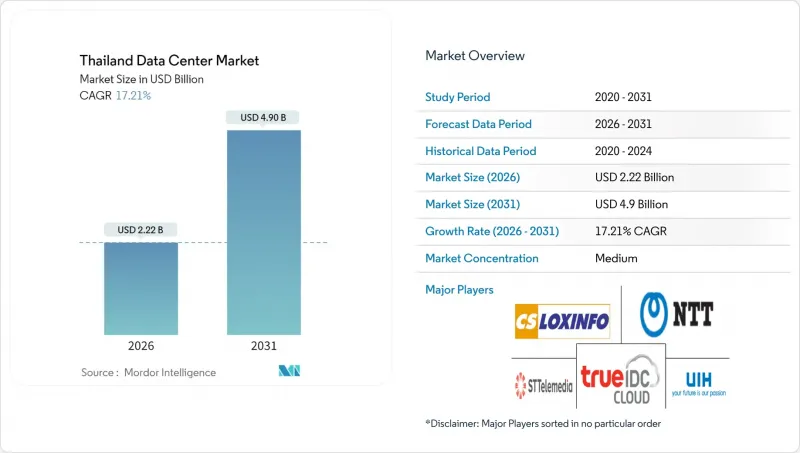

태국의 데이터센터 시장은 2025년에 18억 9,000만 달러로 평가되었고, 2026년 22억 2,000만 달러에서 2031년까지 49억 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 17.21%로 예상됩니다.

시장 규모는 예측 기간(2025-2030년) 동안 CAGR 30.60%로 성장하여 2025년 770MW에서 2030년까지 2,930MW에 달할 것으로 예측됩니다. 시장 세분화 시장 점유율 및 추정치는 메가와트(MW) 단위로 계산되어 보고됩니다. 하이퍼스케일러 기업의 자본 투입, 태국 4.0 정책의 특혜, 적극적인 해저 케이블 설치, 송전망 현대화 및 단계적 재생에너지 구매 규정이 사업자의 신뢰를 유지하고 있습니다. 기업의 클라우드 전환이 AI 도입을 가속화하고, 동부 경제 회랑(EEC)의 엣지 컴퓨팅 구축이 수요를 더욱 강화하고 있습니다. 세계 플랫폼 기업의 진입으로 경쟁이 치열해지면서 랙 밀도, 액체 냉각, 캐리어 중립적 상호 연결에 대한 시설 업그레이드가 촉진되고 있습니다.

정부 주도의 디지털 정책이 지속적으로 추진되고 있는 가운데, 기업은 규제 대상 워크로드를 국내에서 호스팅해야 하는 의무가 있습니다. 투자위원회(BOI)는 현지 컴퓨팅 역량을 확충하는 7억 5,000만 바트(2,170만 달러) 이상의 프로젝트에 대해 최대 13년간 소득세 면제를 허용하고 있어 실질적인 총소유비용(TCO) 절감에 기여하고 있습니다. Midea와 같은 제조업체들은 동부 경제 회랑(EEC) 지역에서 5G를 지원하는 스마트 공장을 운영하고 있으며, 실시간 품질 관리를 위해 인근 엣지 노드에 의존하고 있습니다. 고정 브로드밴드 분야의 합병(특히 AIS와 3BB의 합병)으로 인해 접속 속도가 향상되고 기업의 클라우드 도입이 가속화되고 있습니다. 따라서 높은 가격대에서도 고밀도의 온램프가 장착된 캐리어 중립 사이트는 장기 계약을 체결하고 있습니다.

새로운 아시아 횡단 시스템을 통해 싱가포르, 홍콩, 도쿄로의 왕복 지연이 10밀리초 미만으로 단축되어 컨텐츠, 핀테크, SaaS 기업들이 방콕에 지역 워크로드를 집중할 수 있게 되었습니다. 하이퍼스케일러 업체들은 대역폭 확대를 소버린 클라우드 리전 개설의 전제조건으로 삼고 있으며, 이로 인해 도매 코로케이션 시설에 대한 수요가 연쇄적으로 발생하고 있습니다. 삼중 경로 섬유와 다크 파이버의 다양성이 요구되고 있습니다. 처리량 증가로 태국 통신사업자들은 국내 허브에서 인근 메콩 시장으로 서비스를 제공할 수 있게 되어 도매 수익원이 개척되고 있습니다.

방콕의 캐리어 호텔과 CBD 회랑 내 우량 부지는 기록적인 프리미엄 가격이 형성되어 확장 예산을 가진 멀티 테넌트 사업자를 압박하고 있습니다. 하이퍼스케일러는 보다 두터운 재무기반을 활용하여 산업단지 전체를 선점하기 위해 코로케이션 사업자는 수직적 확장 개보수 및 지방으로 용량을 이전할 수밖에 없는 상황입니다. 그 결과, 부지 물색에 수개월이 소요되는 프로젝트 리드타임이 길어지고, 평방미터당 수익을 높이기 위해 높은 랙 밀도 전략을 채택해야 하는 상황에 처해 있습니다.

태국의 데이터센터 시장 규모에서 중규모 시설이 차지하는 비중이 두드러지며, 기업 및 통신 사업자가 사용자에 가까운 저지연 구역을 선호하는 추세에 따라 CAGR 17.95%로 성장하고 있습니다. 대규모 캠퍼스는 규모의 경제를 가지고 있으며, 2025년 태국의 데이터센터 시장 점유율의 26.35%를 차지했지만, 도심의 토지 제약으로 인해 추가 확장이 제한되고 있습니다.

사업자는 지방 산업단지에 표준화된 6-12MW의 설계도를 복제하고, 제조 클러스터 인근에 프라이빗 네트워크 코어를 배치하는 Advanced Info Service의 5G 엣지 컴퓨팅 구축과 연계하고 있습니다. 이 패턴은 공장 자동화의 전송 지연을 줄이고, 방콕 외 지역의 다양한 수요를 견인하고 있습니다.

2025년 기준 태국의 데이터센터 시장 점유율 85.62%를 차지한 Tier 3 사양은 Tier 4보다 더 현실적인 가격대로 99.982%의 가동률을 실현하여 기업 수요를 충족시키고 있습니다. 고밀도 AI 랙 지원 업그레이드로 인해 2026년부터 2031년까지 18.88%의 연평균 복합 성장률(CAGR)로 Tier 3 시설 건설이 확대될 것으로 예측됩니다.

코로케이션 제공업체들은 완전한 티어4로의 전환보다는 모듈형 전원공급장치와 핫스왑이 가능한 냉각장치를 통한 이중화 강화로 설비투자에 대한 규율을 유지하고 있습니다. STT GDC의 Frost & Sullivan 어워드(Frost and Sullivan Award)는 액체 침지 냉각 수요에 최적화된 Tier 3 시설 내 운영의 우수성을 인정하는 상입니다.

태국의 데이터센터 시장 보고서는 데이터센터 규모(대규모, 초대형, 중대형, 중형, 메가, 소형), 계층 유형(Tier 1, 2, Tier 3, Tier 4), 데이터센터 유형(하이퍼스케일/자체 구축, 기업/에지, 코로케이션), 최종 사용자(은행, 금융서비스 및 보험(BFSI), IT, ITES, 정부, 제조, 미디어, 엔터테인먼트, 통신 등), 핫스팟별로 구분하여 분석하였습니다. ITES, E-커머스, 정부, 제조, 미디어-엔터테인먼트, 통신 등), 핫스팟별로 분류되어 있습니다. 시장 예측은 IT 부하 용량(MW) 단위로 제공됩니다. 최종 사용자(은행, 금융서비스 및 보험(BFSI), IT 및 ITES, 전자상거래, 정부, 제조, 미디어/엔터테인먼트, 통신 등), 핫스팟별로 분류되어 있습니다. 시장 예측은 IT 부하 용량(MW) 단위로 제공됩니다.

The Thailand Data Center Market was valued at USD 1.89 billion in 2025 and estimated to grow from USD 2.22 billion in 2026 to reach USD 4.9 billion by 2031, at a CAGR of 17.21% during the forecast period (2026-2031).

In terms of market size, the market is expected to grow from 0.77 thousand megawatt in 2025 to 2.93 thousand megawatt by 2030, at a CAGR of 30.60% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. Hyperscaler capital commitments, Thailand 4.0 policy incentives, and aggressive submarine-cable builds underpin the expansion, while grid modernization and progressive renewable-energy purchase rules sustain operator confidence. Enterprise cloud migration accelerated AI adoption, and edge buildouts in the Eastern Economic Corridor (EEC) further strengthen demand. Competition intensifies as global platforms enter, spurring facility upgrades in rack density, liquid cooling, and carrier-neutral interconnection.

Continuous state-backed digital policies now oblige corporations to host regulated workloads in-country. The Board of Investment grants up to 13-year income-tax holidays on projects above THB 750 million (USD 21.7 million) that add local compute, lowering the effective total cost of ownership. Manufacturers such as Midea run 5G-enabled smart factories in the EEC that depend on proximate edge nodes for real-time quality control. Mergers in fixed broadband, notably AIS-3BB, lift access speeds and hasten enterprise cloud adoption. Carrier-neutral sites with dense on-ramps therefore secure long-term contracts despite premium pricing.

New trans-Asian systems shorten round-trip latency to Singapore, Hong Kong, and Tokyo below 10 milliseconds, enabling content, fintech, and SaaS firms to anchor regional workloads inside Bangkok. Hyperscalers cite bandwidth gains as the precondition for launching sovereign cloud regions, which cascade demand into wholesale colocation halls requiring triple-path fiber and dark-fiber diversity. Better throughput also lets Thai operators serve neighbouring Mekong markets from domestic hubs, opening wholesale revenue streams.

Prime plots inside Bangkok's carrier hotels and CBD corridors command record premiums that squeeze multi-tenant operators on expansion budgets. Hyperscalers leverage deeper balance sheets to pre-empt entire industrial parks, leaving colocators to retrofit vertical extensions or migrate capacity to outer provinces. Resultant site hunts add months to project lead-times and compel higher rack-density strategies to lift revenue per square meter.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Medium facilities accounted for a notable slice of the Thailand data center market size, growing at 17.95% CAGR as enterprises and telecom carriers prioritize low-latency zones closer to users. Large campuses hold economies of scale and captured 26.35% of Thailand data center market share in 2025, but their downtown land constraints limit additional expansion.

Operators replicate standardized 6-12 MW blueprints in provincial industrial estates, aligning with 5G edge computing rollouts by Advanced Info Service that anchor private network cores near manufacturing clusters. The pattern lowers transport latency for factory automation and drives diverse demand beyond Bangkok.

Tier 3 specifications represented 85.62% of Thailand data center market share in 2025, demonstrating enterprise comfort with 99.982% uptime at more practical price points than Tier 4. Upgrades to support high-density AI racks fuel a 18.88% CAGR for Tier 3 builds over 2026-2031.

Colocation providers enhance redundancy via modular power trains and hot-swap chillers rather than shifting to full Tier 4, preserving capex discipline. STT GDC's Frost and Sullivan award spotlights operational excellence inside Tier 3 footprints optimized for liquid immersion cooling demand.

The Thailand Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and More), and Hotspot. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).