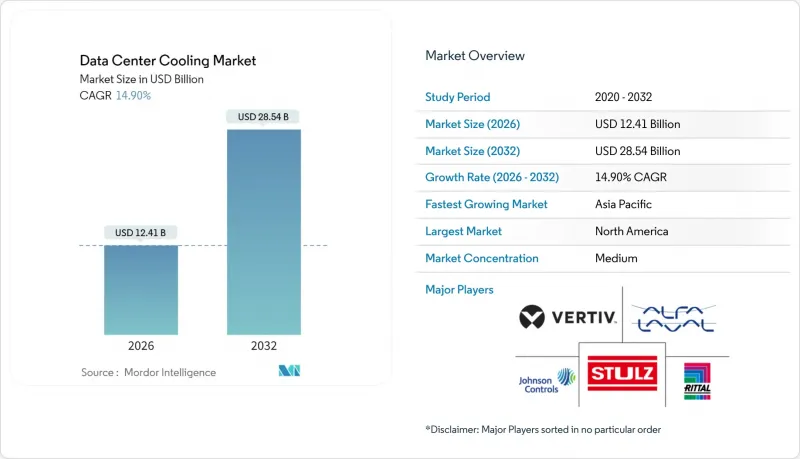

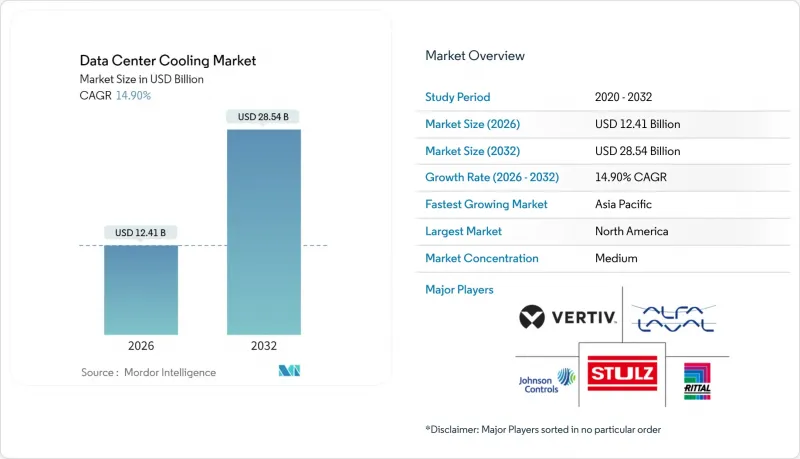

데이터센터 냉각 시장은 2025년에 108억 달러로 평가되며, 2026년 124억 1,000만 달러에서 2032년까지 285억 4,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2032년)에서 CAGR은 14.90%로 전망됩니다.

공랭식에서 액체냉각시스템으로의 지속적인 전환이 이러한 확대를 지원하고 있으며, 하이퍼스케일 시설의 건설, AI 칩의 열부하, 저GWP 냉매 의무화가 단기적으로 구매의욕을 높이고 있습니다. 액체 냉각 솔루션은 이미 데이터센터 냉각 시장의 46%를 차지하고 있으며, 2031년까지 17.50%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, 이는 직접 투 칩 및 액침냉각 아키텍처에 대한 지속적인 선호를 보여줍니다. 하이퍼스케일 사업자가 가장 큰 수요처인 반면, 5G로 인한 지방 네트워크 고도화에 따라 엣지 및 마이크로사이트 구축이 18.00%의 가장 빠른 성장률을 보이고 있습니다. 지역별로는 북미가 지출의 76%를 차지하지만, 아시아태평양의 18.20%의 연평균 복합 성장률(CAGR)은 토지 제약을 고밀도 설계로 보완하는 싱가포르, 중국, 일본에서의 지출 가속화를 강조하고 있습니다. 2024-2025년까지 경쟁 환경은 더욱 치열해졌습니다. 존슨컨트롤즈는 81억 달러 상당의 HVAC 자산을 보쉬에 매각하고 데이터센터 전용 냉각기 사업에 집중합니다. 슈나이더 일렉트릭은 액침냉각 전문 기업 Motivair를 인수하여 액체 냉각 기술로의 전략적 전환을 보여주었습니다.

GPU 고밀도 서버는 현재 랙당 200kW가 넘는 방열량을 보이고 있으며, 기존 10kW의 한계를 훨씬 뛰어넘어 기존 CRAC 유닛으로는 더 이상 대응할 수 없게 되었습니다. 이 때문에 직접 투 칩 콜드 플레이트와 완전 침지형 냉각조는 특히 메타(Meta)와 마이크로소프트(Microsoft)의 AI 클러스터에서 시험 운영에서 생산 현장으로 전환되고 있습니다. 칩 제조업체들은 차세대 패키지에 액체 인터페이스 채널을 통합하여 컴퓨팅 실리콘과 시설 인프라의 경계를 모호하게 만들고 있습니다. 동시에 규제기관은 PUE를 1.3 이하로 낮추도록 추진하고 있으며, 액체 냉각 기술에 유리한 이중 압력 환경이 조성되고 있습니다.

사업자들은 피닉스, 콜럼버스, 오사카 등에서 저렴한 토지 비용과 깨끗한 전력을 원하고 있지만, 이들 지역에는 성숙한 유틸리티 인프라가 부족한 경우가 많습니다. 그 결과, 이 프로젝트에는 모듈식 냉각기와 리어 도어형 열교환기를 채택하여 시운전 주기를 단축하고 환경 온도 변동에 대한 내성을 크게 향상시켰습니다. 또한 지방 도시의 기후는 더 많은 자연 환기 가능 시간을 가져와 기판 수준의 설비 투자 승인을 좌우하는 수명주기 비용 지표를 낮추는 데 기여하고 있습니다.

침지탱크는 기존 핫아일 봉쇄 방식보다 60% 더 비싸고, 특수 유전체 유체는 리터당 5-7달러로 2MW 미만의 사이트에서는 투자회수율에 대한 문제가 있습니다. 그러나 전기요금이 높은 지역에서는 30-40%의 에너지 절감 효과로 투자회수 기간이 3년 이내로 단축됩니다.

액체 냉각 방식의 데이터센터 냉각 시장 규모는 2026년 59억 달러에 달할 것으로 예상되며, 2032년까지 연평균 17.25%의 성장률을 기록하며 153억 3,000만 달러를 넘어설 것으로 예측됩니다. 직접 투 칩 파이프라인은 새로운 AI 랙을 지배하고, 이중 침지 탱크는 암호화 해시 클러스터와 같은 틈새 워크로드를 차지합니다. 랙 밀도가 15kW 미만인 기업 환경에서는 공랭식 냉각기와 CRAC 어레이가 여전히 일반적이지만, 규제에 의한 PUE 목표가 엄격해짐에 따라 그 점유율은 해마다 감소하고 있습니다. 각 업체들은 글리콜루프와 단열패드를 결합한 하이브리드 쿨러로 대응하고 있으며, 프리쿨링 적용 기간을 연장하고 있습니다.

후면 도어형 열교환기는 홀 전체 랙 재배치를 원하지 않는 사업자를 위한 솔루션이 될 수 있습니다. 단일 교환기를 통해 바닥 용접 공사 없이 랙 용량을 12kW에서 30kW까지 끌어올릴 수 있습니다. 한편, 마이크로 대류식 콜드 플레이트의 특허 기술은 350W/cm2의 열 플럭스 제거를 약속하며, 액체 냉각이 x86 서버의 주류로 진입할 조짐을 보이고 있습니다. 엣지 인클로저는 공장 밀폐형 냉각 모듈을 도입하여 현장 작업을 줄였습니다. 무인 운영 요건과 일치하도록 노력하고 있습니다.

컴퓨터실용 공조 장비는 여전히 지출의 30.60%를 차지하지만, CAGR 3.75%로 전체 데이터센터 냉각 시장을 밑돌고 있습니다. 한편, 냉각장치 및 열교환 유닛은 액체냉각 보급에 따른 배관 수요 증가로 15.70%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 펌프, 밸브, 이중화 매니폴드는 직접-투-칩 루프의 보급에 힘입어 2026년 19억 5,000만 달러 규모의 서브마켓을 형성할 것으로 예측됩니다. AI 기반 모니터링 소프트웨어는 가장 빠른 성장세를 보이고 있으며, 구글과 알리바바의 캠퍼스에서는 팬의 회전수(RPM)와 압축기 스테이징을 조정하여 15-25%의 에너지 절감을 실현하고 있습니다. 하드웨어, 텔레메트리, 머신러닝 제어를 통합한 제품군은 높은 가격대임에도 불구하고 정량화할 수 있는 운영 비용 절감을 실현하고, 단독 콘솔보다 더 빠르게 CFO를 설득할 수 있습니다.

데이터센터 냉각 시장은 냉각 기술(공랭식, 액체 냉각), 냉각 부품(컴퓨터실용 에어 핸들러(CRAH/CRAC), 냉각기 및 열교환기 등), 데이터센터 유형(하이퍼스케일, 기업, 코로케이션), 최종사용자(IT, 통신, 소매, 소비재 등), 지역별로 분류됩니다. 산업(IT 및 통신, 소매 및 소비재 등), 지역별로 분류됩니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

북미는 2026년 93억 5,000만 달러의 데이터센터 냉각 시장 규모를 기록했습니다. 이는 피닉스, 애틀랜타, 콜럼버스의 하이퍼스케일 캠퍼스가 재생 폐수를 응축기 루프에 활용할 수 있는 액체 냉각기를 우선순위에 두었기 때문입니다. 여름철 장기 폭염으로 자연환기 가능 시간이 단축됨에 따라 사업자들은 내재해성 향상을 위해 단열형 트림쿨러를 추가 도입하고 있습니다.

아시아태평양은 2026년 17억 3,000만 달러 규모였으나, 2032년까지 연평균 17.85% 성장하여 46억 4,000만 달러 이상에 달할 것으로 예측됩니다. 싱가포르에서는 PUE 1.3 미만 목표 달성을 조건으로 신축 허가를 재개하고 해수냉방과 액체침지냉방 입찰을 촉진하고 있습니다. 도쿄의 밀집화 전략은 각 층에 직접 팽창 코일을 설치한 다층 홀을 쌓아 올리는 방식이며, 뭄바이의 해안 지역의 높은 습도로 인해 물 부족을 완화하기 위해 하이브리드 유체 냉각기를 채택하는 프로젝트가 증가하고 있습니다.

유럽에서는 2026년 11억 4,000만 달러의 시장 규모를 기록할 것으로 예상되며, 북유럽 국가에서는 데이터센터 폐열을 지역난방용 열원으로 250MW를 회수하고 있습니다. 프랑크푸르트와 암스테르담은 폐열 재사용 할당 기준을 도입하여 고품질 물 순환 시스템으로의 조달을 촉진하고 있습니다. 중동 및 아프리카에서는 50℃에 달하는 외기 온도에 대응하기 위해 액체 냉각을 채택하고 있습니다. 두바이의 경우, 태양광발전소와 축열 탱크를 통해 냉각장치의 전력 소비를 17% 절감했습니다. 라틴아메리카에서는 케레타로와 산티아고에 신규 건설이 진행 중이며, 밤에는 서늘한 기후를 활용하여 간접 증발 냉각 모듈을 도입했습니다. 낮의 높은 온도에도 불구하고 1.2의 PUE를 달성했습니다.

The data center cooling market was valued at USD 10.80 billion in 2025 and estimated to grow from USD 12.41 billion in 2026 to reach USD 28.54 billion by 2032, at a CAGR of 14.90% during the forecast period (2026-2032).

Ongoing migration from air-based to liquid-based thermal systems underpins this expansion, while hyperscale build-outs, AI chip heat loads and low-GWP refrigerant mandates reinforce near-term purchasing momentum. Liquid solutions already claim a 46% data center cooling market share, and their 17.50% CAGR through 2031 signals lasting preference for direct-to-chip and immersion architectures. Hyperscale operators represent the single largest demand node, yet edge and micro-site deployments now post the fastest growth at 18.00% as 5G densifies rural networks. Geographically, North America contributes 76% of spending, but Asia-Pacific's 18.20% CAGR highlights accelerating spend in Singapore, China and Japan, where high-density designs offset land constraints. Competitive dynamics intensified in 2024-2025: Johnson Controls divested USD 8.1 billion of HVAC assets to Bosch to double down on data center-specific chillers, and Schneider Electric added immersion specialist Motivair to its portfolio, signaling a strategic pivot toward liquid engineering.

GPU-dense servers now dissipate beyond 200 kW per rack, dwarfing legacy 10 kW envelopes and rendering conventional CRAC units ineffective. Direct-to-chip cold plates and full-immersion baths have therefore moved from pilots to production floors, particularly inside Meta and Microsoft AI clusters. Chipmakers embed liquid interface channels in next-generation packages, eroding the barrier between compute silicon and facility infrastructure Regulatory bodies simultaneously push PUE below 1.3, creating a dual-pressure environment that favors liquid technologies.

Operators chase lower land costs and cleaner power in Phoenix, Columbus and Osaka, but those locations often lack mature utility infrastructure. As a result, projects specify modular chillers and rear-door heat exchangers that shorten commissioning cycles and tolerate wide ambient swings. Secondary-city climates also grant more free-air hours, lowering lifecycle cost metrics that drive board-level cap-ex approvals.

Immersion tanks cost 60% more than traditional hot-aisle containment, and specialized dielectric fluids range USD 5-7 per liter, challenging ROI in sites below 2 MW. Nevertheless, energy savings of 30-40% compress payback to under three years in high-electricity-tariff regions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The data center cooling market size for liquid methods reached USD 5.90 billion in 2026 and will eclipse USD 15.33 billion by 2032, advancing at 17.25% CAGR. Direct-to-chip pipelines dominate new AI racks, while dual-phase immersion tubs claim niche workloads such as crypto hashing clusters. Air-based chiller and CRAC arrays remain common in enterprise environments where rack densities linger below 15 kW, yet their share declines annually as regulations squeeze PUE targets. Vendors counter with hybrid coolers marrying glycol loops and adiabatic pads to extend free-cooling seasons.

Rear-door heat exchangers bridge the gap for operators unwilling to re-rack entire halls; a single exchanger lifts rack capacity from 12 kW to 30 kW without floor welding. Meanwhile, patents on microconvective cold plates promise 350 W/cm2 heat flux removal, foreshadowing liquid's march into mainstream x86 servers. Edge enclosures import factory-sealed coolant modules to slash on-site labor, aligning with unmanned operation mandates.

Computer-room air handlers still account for 30.60% of spend, but their 3.75% CAGR lags the overall data center cooling market. Conversely, chillers and heat-exchanger units will log 15.70% CAGR as liquid adoption expands pipework demand. Pumps, valves and redundancy manifolds form a USD 1.95 billion submarket in 2026, benefitting from direct-to-chip loop proliferation. AI-driven supervisory software posts the fastest growth, trimming fan RPM and compressor staging to save 15-25% energy at Google and Alibaba campuses. Integrated suites that blend hardware, telemetry and machine-learning controls command premium pricing yet deliver quantifiable OPEX reduction, convincing CFOs faster than standalone consoles.

Data Center Cooling Market is Segmented by Cooling Technology (Air-Based Cooling, Liquid-Based Cooling), Cooling Component (Computer-Room Air Handlers (CRAH/CRAC), Chillers and Heat-Exchanger Units, and More), Data Center Type (Hyperscale, Enterprise, Colocation), End-User Industry (IT and Telecom, Retail and Consumer Goods, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America recorded USD 9.35 billion of data center cooling market size in 2026, driven by hyperscale campuses in Phoenix, Atlanta and Columbus that favor liquid chillers able to exploit reclaimed wastewater for condenser loops. Extended summer heat waves shorten free-air windows, prompting operators to add adiabatic trim coolers for resilience.

Asia-Pacific contributed USD 1.73 billion in 2026 but will surpass USD 4.64 billion by 2032 on an 17.85% CAGR. Singapore reinstated new-build permits contingent on sub-1.3 PUE targets, steering bids toward seawater and liquid immersions. Tokyo's densification strategy stacks multi-story halls using direct-expansion coils for each floor, while Mumbai's coastal humidity inclines projects toward hybrid fluid coolers that mitigate water scarcity.

Europe generated USD 1.14 billion in 2026, with Nordic states extracting 250 MW of district-heating value from data center exhaust water. Frankfurt and Amsterdam now impose waste-heat-reuse quotas, nudging procurements toward high-grade water loops. Middle East and Africa adopt liquid cooling to battle 50 °C ambient peaks; Dubai's collocated solar farm plus thermal-storage tank trims chiller electricity by 17%. Latin America saw emergent builds in Queretaro and Santiago, where cooler night air favors indirect evaporative modules that achieve 1.2 PUE despite high daytime highs.