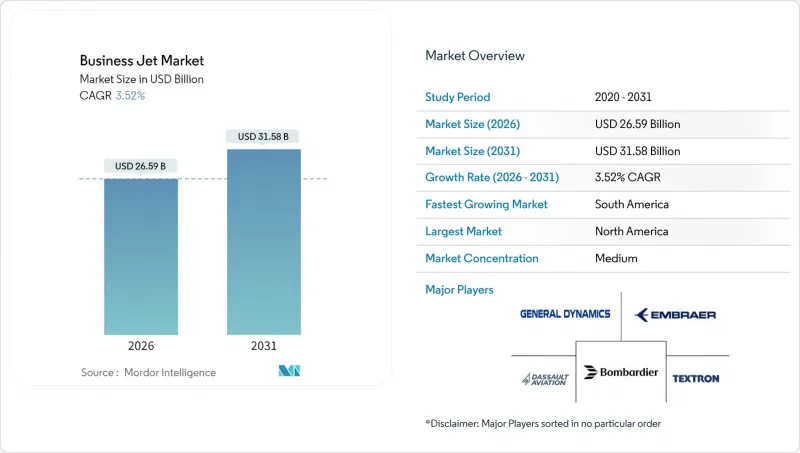

2026년 비즈니스 제트 시장 규모는 265억 9,000만 달러로 추정되며, 2025년 256억 9,000만 달러에서 성장이 전망됩니다.

2031년 예측치는 315억 8,000만 달러로 2026년부터 2031년까지 CAGR 3.52%로 확대될 것으로 예상됩니다.

주요 성장요인은 기체 교체 수요, 분양소유권 보급, 초장거리 노선 개척입니다. 한편, 높은 구매 비용과 강화되는 탄소 규제는 전체 시장 확대를 완만하게 만들고 있습니다. 대형 캐빈기가 수요를 견인하고, 암호화폐로 창출된 부로 고객층이 확대되고 있습니다. 수소전기기술의 연구개발이 진행되면서 구매자의 기대치가 변화하고 있습니다. 지역적으로는 북미가 여전히 중심이지만, 남미에서는 농업 관련 산업을 통한 부의 창출이 지역 성장을 가속화하고 있습니다. 공급망의 병목현상으로 인해 리드타임이 길어지고, 구매 희망자들이 전세, 회원제, 분양형 솔루션으로 전환하는 가운데 OEM 업체들은 가격 결정권을 갖게 되었습니다.

미국 내 비즈니스 제트기의 평균 기령은 2024년 18.5년으로, 연료비와 정비비용이 급등하는 가운데 운항사들은 노후 항공기를 조기에 교체해야 하는 상황에 직면해 있습니다. 신형 항공기는 최대 30%의 연료 절감과 40% 더 긴 정비 주기를 실현하여, 겉으로 보이는 가격에도 불구하고 총소유비용의 매력도를 높였습니다. 보험사들은 구형 기종에 대해 더 높은 보험료를 부과하고 있으며, 경제성을 더욱 갱신 방향으로 기울이고 있습니다. 하니웰은 금세기 중 2,800억 달러 규모의 갱신 수요를 예상하고 있으며, 대형 캐빈 항공기가 그 대부분을 차지할 것으로 예상하고 있습니다. 하이테크 조종석은 조종사 훈련 의무화와 맞물려 업데이트의 물결을 더욱 가속화하고 있습니다.

걸프스트림의 G700은 2024년 65개 이상의 도시 간 직항 기록을 세우며 7,750해리 무착륙 비행이 가능한 항공기에 대한 수요를 뒷받침했습니다. 2025년 취항 예정인 Bombardier World 8000은 8,000마일의 항속거리로 뉴욕-두바이, 런던-싱가포르 간 무급유 비행을 실현할 예정입니다. 아시아태평양의 오너들은 허브공항 인프라가 부족한 지역에서 시차를 효율적으로 활용할 수 있는 직항편을 높이 평가하고 있습니다. 운항사들은 이러한 항공기의 가동률이 30-40% 향상되어 수익성 향상으로 이어지고 있다고 보고하고 있습니다. 이러한 초장거리 임무의 추구로 연구개발비는 대형 연료 탱크와 경량 복합재 구조물 개발에 집중되고 있습니다.

신 기종의 정가는 연간 8-12% 상승하여 2024년 제트 연료 A는 갤런당 6.07달러에 달했습니다. 부품 가격의 급등과 기술자 부족으로 비용 압박이 심화되고 있으며, 정비 인건비는 현재 시간당 평균 138-161달러에 달합니다. 보험료가 고공행진을 하고 있으며, 특히 국제선 구간 전쟁 위험 보상은 고액입니다. 이러한 지출로 인해 신규 진입을 고려하는 계층은 완전 소유가 아닌 전세편이나 회원제 프로그램을 선택하는 경향이 있습니다. 신흥시장 구매자들은 통화 약세와 제한된 자금 조달 수단으로 인해 가장 심각한 압박을 받고 있습니다.

대형 캐빈 플랫폼은 2025년 납품 항공기의 81.62%를 차지하여 대륙간 노선에서 급유 중단을 피할 수 있는 항공기에 대한 구매자의 선호를 반영합니다. 이 부문은 최대 19명의 승객을 편안하게 태울 수 있는 신규 진입 기종에 힘입어 2031년까지 CAGR 3.74%로 확대될 것으로 예상됩니다. 와이드 캐빈 설계는 더 많은 수하물, 대형 갤리, 전용 승무원 휴게실을 허용하여 야간 이동의 임무 능력을 강화합니다. 중형 제트기는 직접 운영비 절감을 원하는 기업 셔틀 사업자로부터 일정한 수요를 유지하고 있으며, 소형 제트기는 단거리 및 조종사 소유의 임무에 대응하고 있습니다.

구매자는 대형기종 선택에 있어 비즈니스 제트기 시장의 효율성 향상, 정비 주기 연장, 보험 조건 우대 등을 이유로 꼽았습니다. 이에 대해 OEM 업체들은 탄소섬유 소재의 얇은 날개, 고추력 엔진, 15시간 비행 시 피로를 줄이는 객실 고도 감소 기술 등으로 대응하고 있습니다. 기체 노후화가 진행됨에 따라 운항사들은 경제성에 대한 획기적인 변화를 인식하고 있습니다. 2005년형 항공기를 갱신함으로써 연간 450시간의 표준 운항 주기로 연간 250만 달러의 운영비용을 절감할 수 있습니다. 그 결과, 대형 제트기 카테고리는 예측 기간을 크게 넘어서도 비즈니스 제트기 시장의 근간을 이룰 것으로 예상됩니다.

북미는 2025년 기준 66.25%의 점유율을 유지했습니다. 이는 5,000개 이상의 제트기 전용 공항, 성숙한 분양 프로그램, 세계 최대 규모의 초부유층 인구가 뒷받침한 결과입니다. 미국 기업들은 직항편을 통한 생산성 향상을 중시하고, 갱신 주기가 수주 활동의 주류를 차지합니다. 캐나다와 멕시코는 자원개발과 니어쇼어링 공급망으로 인한 안정적인 수요가 더해집니다.

남미는 브라질의 농업 비즈니스 확대와 부유층 증가에 힘입어 2031년까지 CAGR 8.72%로 가장 빠르게 성장하는 지역입니다. 이미 약 3,000여대의 비즈니스 항공기가 운영되고 있으며, 엠브라에르의 현지 지원 체제의 혜택을 누리고 있습니다. 아르헨티나, 칠레, 콜롬비아는 광업 및 금융 서비스 클러스터가 성장을 주도하고 있습니다. 국경을 넘는 비행 계획 규칙의 개선으로 플로리다에서 재배치하는 대신 지역 내 항공기 배치가 증가하는 추세입니다.

유럽에서는 수요가 성숙기에 접어들었고, 지속가능성으로의 전환이 진행되고 있습니다. 지속가능한 항공 연료(SAF) 의무화 및 미래 수소 연료 허브 구상 등이 구매 기준을 형성하고 있습니다. 아시아태평양에서는 중국, 인도, 동남아시아를 중심으로 연간 2.02%의 항공기 수 증가율(세계 평균 1.36%)을 보이고 있으며, 신규 공항의 도입과 슬롯 규제 완화로 인해 도시 간 노선이 증가하고 있습니다. 중동 및 아프리카는 틈새시장이자 전략적인 지역이며, UAE와 사우디아라비아는 유럽-아시아-아프리카를 잇는 초장거리 노선의 중계 거점 역할을 하고 있습니다. 이러한 추세는 서방 국가들의 갱신 수요 중심의 성숙한 시장과 남방 국가들의 초기 성장 시장이 균형을 이루는 다각화된 비즈니스 제트기 시장을 형성하고 있습니다.

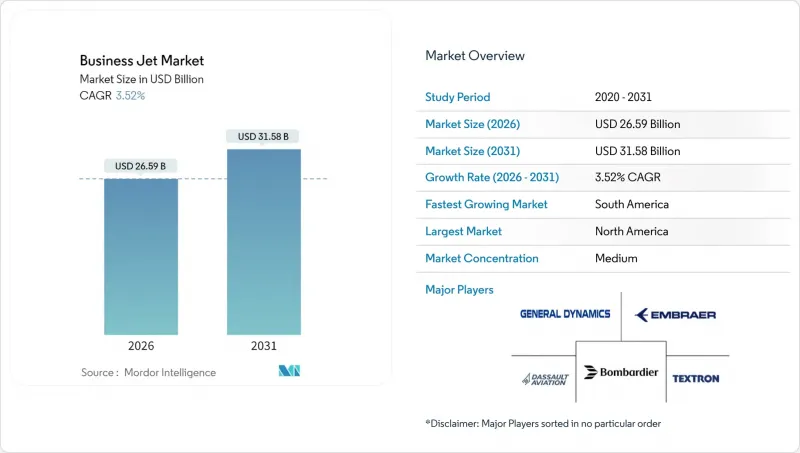

The business jet market size in 2026 is estimated at USD 26.59 billion, growing from 2025 value of USD 25.69 billion with 2031 projections showing USD 31.58 billion, growing at 3.52% CAGR over 2026-2031.

The primary growth levers are replacing demand, fractional-ownership uptake, and pursuing ultra-long-range city pairs. At the same time, high acquisition costs and tightening carbon rules keep overall expansion moderate. Large-cabin jets dominate demand, crypto-generated wealth is expanding the customer pool, and hydrogen-electric R&D is beginning to reshape buyer expectations. Geography remains skewed toward North America, yet South America's agribusiness-linked wealth is accelerating regional growth. Supply-chain bottlenecks lengthen lead times, giving OEMs pricing power even as would-be buyers pivot to charter, membership, and fractional solutions.

The average age of US business jets reached 18.5 years in 2024, prompting operators to replace older aircraft sooner as fuel costs and maintenance bills rise steeply. New models deliver up to 30% fuel savings and 40% longer maintenance intervals, making the total cost of ownership attractive despite headline prices. Insurance carriers now impose higher premiums on legacy airframes, further tipping economics toward replacement. Honeywell projects a USD 280 billion replacement opportunity this decade, with large-cabin jets capturing the lion's share. Higher-tech cockpits also align with pilot-training mandates, reinforcing the wave of replacements.

Gulfstream's G700 set more than 65 city-pair records in 2024, underscoring demand for aircraft that fly 7,750 nautical miles nonstop. Bombardier's Global 8000 enters service in 2025 with an 8,000-mile envelope, allowing flights to New York-Dubai and London-Singapore without refueling. Asia-Pacific owners value the time-zone efficiency of nonstop links across sparse hub infrastructure. Operators report 30-40% higher utilization on such aircraft, which translates to stronger revenue yields. Pursuing these ultra-long-range missions shifts R&D dollars toward larger fuel tanks and lighter composite structures.

New-aircraft sticker prices rise 8-12% annually, while Jet-A hit USD 6.07 per gallon in 2024. Parts inflation and technician shortages compound cost pressures; maintenance labor now averages USD 138-161 per hour. Insurance premiums remain elevated, especially for war-risk coverage on international legs. These outlays encourage entry-level prospects to opt for charter and membership programs rather than outright ownership. Buyers in emerging markets feel the squeeze most acutely due to weaker currencies and limited financing options.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Large-cabin platforms commanded 81.62% of 2025 deliveries, reflecting buyers' preference for aircraft that skip fuel stops on intercontinental routes. The segment is expected to expand at a 3.74% CAGR to 2031, driven by new entrants that carry up to 19 passengers in lie-flat comfort. Wide-cabin footprints support more baggage, larger galleys, and dedicated crew rest, reinforcing mission capability for overnight trips. Mid-size jets retain pockets of appeal among corporate shuttle operators seeking lower direct-operating costs, while light jets cater to short-haul, pilot-owned missions.

Buyers cite enhanced business jet market efficiency, lower maintenance intervals, and more favorable insurance terms when selecting larger models. OEMs respond with thinner carbon-fiber wings, high-thrust engines, and cabin-altitude reductions that lessen fatigue on 15-hour flights. As fleet age rises, operators see a step-change in economics: upgrading from a 2005-vintage aircraft can save USD 2.5 million in annual operating expenses over a typical 450-hour cycle. Consequently, the large-jet category should continue to anchor the business jet market well past the forecast window.

The Business Jet Market Report is Segmented by Body Type (Large Jet, Mid-Size Jet, and Light/Very-Light Jet), End User (Individual Owners, Businesses and Corporate Entities, Charter/Air-Taxi Operators, and More), Ownership Model (New Aircraft Purchase, Pre-Owned Purchase, Fractional Ownership, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained a 66.25% share in 2025, thanks to 5,000+ jet-capable airports, mature fractional programs, and the world's largest ultra-high-net-worth population. United States corporations value productivity gains from point-to-point travel, and replacement cycles dominate order activity. Canada and Mexico add steady demand from resources and near-shoring supply chains.

South America is the fastest-growing region, with a 8.72% CAGR through 2031, driven by Brazil's agribusiness expansion and rising elite wealth. The country already fields around 3,000 business aircraft and benefits from Embraer's local support footprint. Argentina, Chile, and Colombia contribute incremental growth to mining and financial services clusters. Improved cross-border flight-planning rules encourage operators to base aircraft regionally instead of repositioning from Florida.

Europe faces mature demand but pivots to sustainability: SAF mandates and future hydrogen hubs frame purchase criteria. The Asia-Pacific region posts a 2.02% annual fleet expansion, compared to 1.36% worldwide, led by China, India, and Southeast Asia, where the introduction of new airports and easing of slot controls increases the number of city pairs. The Middle East and Africa remain niche but strategic, with the UAE and Saudi Arabia acting as stopover hubs for ultra-long-range legs linking Europe, Asia, and Africa. Collectively, these dynamics shape a diversified business jet market that balances replacement-driven maturity in the Western countries with initial growth in the Southern ones.