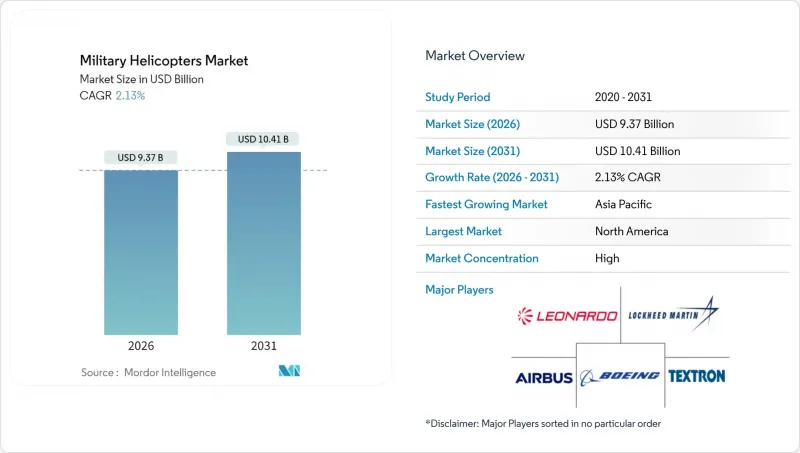

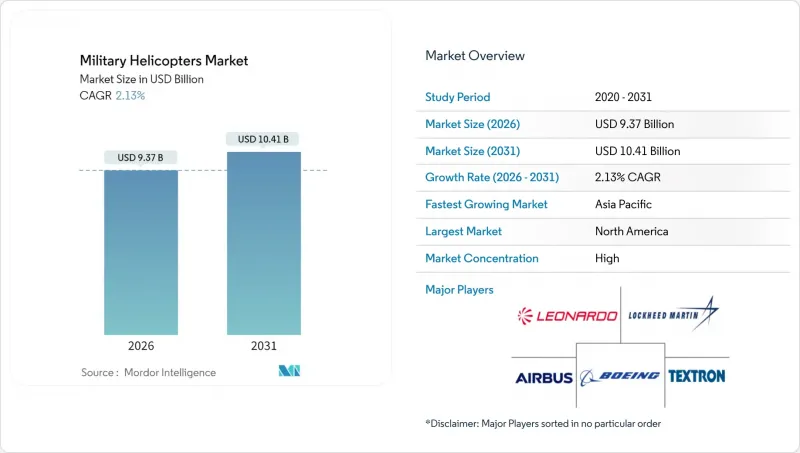

군용 헬리콥터 시장은 2025년에 91억 7,000만 달러로 평가되었으며, 2026년 93억 7,000만 달러에서 2031년까지 104억 1,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 2.13%로 예상됩니다.

수요는 북미에 집중되어 있으며, 함대 현대화 계약과 수명 연장 프로그램이 조달 모멘텀을 유지하고 있습니다. 한편, 아시아태평양에서는 지역 강대국들이 새로운 국산 플랫폼을 도입하고 출격 가능한 항공기 수를 늘리면서 가장 가파른 상승세를 보이고 있습니다. 차세대 프로젝트인 미래형 수직이착륙기(FVL), 틸트 로터, 유인/무인항공기 연계 개념 등은 기술적 장벽이 높으며, 주요 계약자는 지적재산권 관리와 성능 기반 물류를 통해 수익률을 보호할 수 있습니다. 그러나 라이프사이클 비용 상승, 접근거부/영역거부(A2/AD) 위협 증가, 무장무인항공기(UAV) 능력 향상 등의 역풍이 대규모 조달을 억제하는 요인으로 작용하고 있습니다. 이러한 배경에서 군용 헬리콥터 시장에서는 전체 함대 수를 줄이고 유지 관리를 간소화하는 다목적, 다임무 설계가 계속 강조되고 있습니다.

미국, 유럽 및 주요 아시아태평양 동맹국의 헬리콥터 함대는 빠르게 노후화되고 있으며, 각국 국방부는 구조 개조, 항공전자 혁신, 동력장치 업그레이드를 위한 자금 배분을 서두르고 있습니다. 미 육군의 700억 달러 규모의 '차세대 장거리 공격기(FLRAA)' 계획은 재원 조달이 단기적인 재정적 제약을 넘어서는 것을 보여줍니다. 유럽의 163억 6,000만 달러 규모의 차세대 회전익 기능력 계획(NGRC)도 이와 유사한 긴급성을 반영하여 파트너 국가들이 조사개발 위험을 공유하고 물류 체인을 통합할 수 있도록 하고 있습니다. 이러한 다년간의 프레임워크는 예측 가능한 조달량을 지원하고, 산업의 고용을 보호하며, 전문적인 공급 네트워크를 유지합니다. 이를 통해 군용 헬리콥터 시장은 연간 예산이 변동하더라도 확정된 수주 잔고의 혜택을 계속 누릴 수 있습니다. NATO 표준화 협정에 포함된 상호운용성 조항은 요구사항의 추가 조정을 촉진하고, 부품의 공통화를 가속화하며, 인증 주기를 단축할 수 있습니다.

국방부는 특수 용도 기체에서 플러그 앤 플레이 방식의 임무 키트를 장착할 수 있는 다목적 플랫폼으로 전환을 추진하고 있습니다. 레오나르도의 AW249는 이러한 개념을 구현하고 있으며, 지상 정비반이 몇 시간 내에 센서와 무기 시스템을 교체할 수 있기 때문에 단일 편대가 추가 항공기 없이 정찰 임무에서 부상자 구조 임무로 즉시 전환할 수 있습니다. 미 해병대가 운용하는 AH-1Z와 UH-1Y는 부품 공통률이 84%에 달해 훈련 부하 감소, 예비 부품 재고 감소, 수명주기 비용 절감을 실현했습니다. 이는 유지비를 감시하는 입법부의 관심과도 부합하는 성과입니다. 전술 교리가 기동적인 부대 편성을 중시하는 가운데, 모듈식 설계는 연합 작전을 단순화합니다. 동맹국이 기체 전체가 아닌 키트를 빌릴 수 있기 때문에 군용 헬리콥터 시장은 분쟁 영공에서 무인항공기(UAV)의 진출에 맞서 자신의 존재 의미를 지키는 데 일조할 수 있습니다.

대형 수송헬기 1대의 구입 및 30년 유지비용은 최대 8,000만 달러에 달하기 때문에 재무부가 비용절감을 할 때 헬리콥터는 주요 감축 대상입니다. 미 해군의 CH-53K 가격 급등으로 인해 조달 감축을 강요당하고, 독일은 NATO의 지출 상한선을 준수하기 위해 H145M 발주를 연기했습니다. 이에 반해 군은 제조업체가 소유권을 보유하고 가동률을 보장하는 '시간당 계약'을 시범적으로 도입하고 있습니다. 이러한 변화는 매출의 회계처리 패턴을 변화시키지만, 군용 헬리콥터 시장의 미래 현금흐름을 예측할 수 있게 해줍니다.

2025년 기준 다목적 헬리콥터는 군용 헬리콥터 시장 규모의 51.05%를 차지했으며, 이는 국방 계획 담당자들이 여러 임무에 대응할 수 있는 단일 기체를 선호하는 경향을 뒷받침합니다. 수요의 배경에는 후방 지원의 단순화, 훈련 부하 감소, 부품 공통성 감소 등의 이점이 있습니다. UH-60M의 광범위한 채택은 이러한 논리를 구현하고 있으며, 엔진을 변경하지 않고도 의료 수송, 특수 작전, 병력 수송을 커버하는 변형이 존재합니다. 2026년부터 2031년까지 수출 고객이 항공전자 및 무기 통합을 NATO 표준으로 업그레이드함에 따라 이 부문은 점차 확대될 것으로 예상됩니다. 반면, 전용 전자전 헬기나 수색구조(SAR) 헬기는 고수익률을 보장하는 임무 특화형 센서 페이로드에 의해 안정적이면서도 틈새 규모를 유지합니다.

수송용 헬리콥터는 규모가 작지만 5.64%의 가장 빠른 CAGR을 기록할 것으로 예상됩니다. 이는 신속한 부대 전개와 재난 구호에 중점을 둔 교훈이 반영된 결과입니다. 태풍 시즌과 지진 발생 후 아시아태평양의 재난 대응 자금 유입은 신규 조달을 직접적으로 촉진합니다. 다목적 플랫폼이 사양을 계속 지배하는 한편, 새로운 운송 프로그램은 종종 광범위한 수륙 양용 및 항공 물류 개념에 통합되어 후속 예비 부품 및 정비소 수준의 업그레이드를 통해 전체 군용 헬리콥터 시장을 강화하고 있습니다.

육군 항공 부대는 2025년까지 수익의 42.35%를 차지했으며, 지상군이 기동 및 화력 지원을 위해 회전익 항공기에 의존하고 있음을 뒷받침합니다. 폴란드, 호주, 인도의 대대급 조달 계획은 각국이 1970년대 기체를 디지털 조종석과 네트워크 중심 임무 시스템으로 교체하면서 수요를 지속하고 있습니다. 공군의 수주 규모는 작지만, 인명구조, 특수작전, 핵안보 임무가 고정익기에서 회전익기로 전환되고, 호버링 능력과 수직이착륙의 우위를 확보하면서 2031년까지 CAGR 4.18%로 가장 높은 성장세를 보일 것으로 예상됩니다.

해군 및 해병대 사용자는 접이식 블레이드, 부식 방지 대책, 함정용 항공 전자공학을 갖춘 해상 최적화 기체를 계속 주문할 것입니다. 한편, 준군사조직과 해안경비대 기관은 국내 안보 위협과 관련된 예산 증가를 배경으로 제조업체가 군용 항공기를 고가의 재설계 없이 저사양의 공공질서 유지 사양으로 재포장할 수 있도록 허용합니다. 이러한 추세와 함께 다양한 교리상의 필요에 따라 다양한 변형을 제공하는 주요 제조업체가 획득할 수 있는 전체 군용 헬리콥터 시장 점유율이 확대될 것입니다.

북미는 2025년 지출의 44.80%를 차지하며, 미국 육군, 해군, 해병대에서 진행 중인 CH-53K, UH-60M, CH-47F의 수십억 달러 규모의 수주가 기반이 되고 있습니다. 탄탄한 산업 기반은 신속한 개조 캠페인을 지원하고, 항공전자, 무기, 사이버 보안 분야에서 세계 표준을 선도하는 애프터마켓의 우위를 강화하고 있습니다. 캐나다에서는 CH-148 사이클론 해상부대가 수요를 보완하고, 멕시코의 국경경비용 경수송기 조달로 국경을 넘는 MRO 협력이 확대되고 있습니다.

아시아태평양은 5.57%의 CAGR로 가장 빠르게 성장하고 있으며, 중국의 Z-20, 인도의 IMRH, 한국의 수리온 시리즈와 같은 국산 헬리콥터 개발이 가속화되고 있습니다. 동중국해와 남중국해의 지역적 긴장이 고조되는 가운데 각국 공군은 높은 대응태세를 유지해야 하는 상황에서 현지 조달 의무를 포함한 수명연장 및 블록 업그레이드가 추진되고 있습니다. 호주의 MRH-90 후속기 도입과 일본의 UH-2 라이선스 생산은 동맹국들이 오프셋 계약에 기반한 공동생산으로 공급망 리스크를 분산하는 방식을 보여주고 있으며, 이를 통해 군용헬기 시장과 연계된 지역경제 파급효과가 확대되고 있습니다. 유럽은 안정적이면서도 예산 제약이 있는 구매자로, 상호운용성을 극대화하고 연구개발 비용을 분산하기 위해 NH90과 타이거와 같은 공동 개발 플랫폼에 집중하고 있습니다. 140억 유로(162억 7,000만 달러) 규모의 NGRC 로드맵에 따라 파트너 국가들은 첨단 추진 시스템, 재료 과학, 디지털 조종석에 대한 공동 연구를 지속할 예정이지만, 실제 기체 발주 수는 의회 예산 승인 상황에 따라 지연될 수 있습니다. 중동 및 아프리카에서는 석유 수입과 외부의 안보 지원금에 의한 기회주의적 구매가 지속되고 있으며, 빠른 능력 향상을 실현하는 기성품인 미국산 및 유럽산 모델을 일반적으로 선호하고 있습니다. 남미의 수요는 마약 단속 및 수색 및 구조(SAR) 수요에 힘입어 견고한 다목적 기체에 대한 의존도가 높으며, 가능한 한 현지 최종 조립 라인에서 생산되고 있습니다.

The Military Helicopters Market was valued at USD 9.17 billion in 2025 and estimated to grow from USD 9.37 billion in 2026 to reach USD 10.41 billion by 2031, at a CAGR of 2.13% during the forecast period (2026-2031).

Demand is concentrated in North America, where fleet-modernization contracts and service-life extension programs sustain procurement momentum. At the same time, Asia-Pacific registers the steepest ascent as regional powers field new indigenous platforms and boost sortie availability. Next-generation projects such as Future Vertical Lift (FVL), tiltrotors, and manned-unmanned teaming concepts keep technological barriers high, allowing prime contractors to protect margins through intellectual-property control and performance-based logistics. However, elevated life-cycle costs, rising anti-access/area-denial (A2/AD) threats, and the growing competence of armed unmanned aerial vehicles (UAVs) introduce headwinds that temper large-scale acquisitions. Against this backdrop, the military helicopter market continues to favor versatile multi-mission designs that lower overall fleet counts and simplify sustainment.

Helicopter fleets across the US, Europe, and key Asia-Pacific allies are aging fast, prompting ministries to allocate funds toward structural refurbishments, avionics refresh, and power-plant upgrades. The US Army's USD 70 billion Future Long-Range Assault Aircraft initiative underscores how recapitalization overrides short-term fiscal limitations. European collaboration via the USD 16.36 billion Next Generation Rotorcraft Capability mirrors that urgency, allowing partners to share R&D risk and align logistics chains. These multi-year frameworks underpin predictable procurement volumes that safeguard industrial employment and sustain specialized supply networks, ensuring the military helicopters market benefits from firm order backlogs even when annual budgets fluctuate. Interoperability clauses embedded in NATO standardization agreements further harmonize requirements, accelerating component commonality and compressing certification cycles.

Defense departments are pivoting from niche airframes to configurable workhorses that accept plug-and-play mission kits. Leonardo's AW249 illustrates this mindset; field crews can swap sensor or weapon suites within hours, enabling a single squadron to pivot from reconnaissance to CASEVAC without additional hulls. The US Marine Corps experience with the AH-1Z and UH-1Y, which share 84% parts commonality, validates lower training loads, leaner spares inventories, and reduced lifecycle cost outcomes that resonate with lawmakers monitoring sustainment bills. As doctrines emphasize agile force packages, modularity simplifies coalition operations because allied forces can borrow kits instead of entire aircraft, helping the military helicopters market defend relevance against UAV encroachment in contested airspace.

A single heavy-lift platform can cost as much as USD 80 million to buy and sustain over 30 years, making helicopters prime targets when finance ministries hunt for savings. The US Navy's CH-53K price tag forced procurement cuts, while Germany postponed H145M orders to comply with NATO spending ceilings. In response, services experiment with power-by-the-hour contracts where manufacturers retain ownership and guarantee availability. This shift alters top-line booking patterns but ensures predictable out-years cash flows for the military helicopters market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Multi-mission helicopters generated 51.05% of the military helicopters market size in 2025, validating defense planners' preference for a single adaptable airframe across multiple roles. Demand stems from logistics simplification, reduced training load, and lower spares commonality. The UH-60M's widespread adoption exemplifies this logic; variants cover medevac, special operations, and troop lift without changing power-plants. From 2026 to 2031, the segment is set to expand gradually as export customers upgrade avionics and weapon integration to NATO standards. Conversely, dedicated electronic-warfare and SAR helicopters keep stable but niche volumes, protected by mission-specific sensor payloads commanding premium margins.

Although transport helicopters have a smaller base, they are forecasted to post the fastest 5.64% CAGR, reflecting the lessons-learned emphasis on rapid troop deployment and disaster relief. The influx of disaster-response funding in the Asia-Pacific after typhoon seasons and earthquake events directly supports incremental procurements. While multi-mission platforms continue to dominate specifications, new transport programs often plug into broader amphibious and airborne logistics concepts, reinforcing the overall military helicopters market through follow-on spares and depot-level upgrades.

Army aviation contributed 42.35% to 2025 revenue, confirming ground forces' reliance on rotorcraft for maneuver and fire support. Battalion-level acquisition plans in Poland, Australia, and India sustain volume as each nation replaces 1970s-era fleets with digital cockpits and network-centric mission suites. Air force orders, though smaller, register the strongest 4.18% CAGR through 2031 as personnel recovery, special operations, and nuclear security missions migrate from fixed-wing to rotary assets to gain hover and vertical-lift advantages.

Naval and marine corps users continue ordering maritime-optimized airframes featuring folding blades, corrosion protection, and shipboard avionics. Meanwhile, paramilitary and coast-guard agencies capture rising budgets tied to domestic security threats, allowing manufacturers to repackage military airframes into lower-spec public-order configurations without costly redesign. Together, these dynamics widen the total military helicopters market share obtainable by primes that tailor variants to diverse doctrinal needs.

The Military Helicopters Market Report is Segmented by Helicopter Type (Multi-Mission Helicopter, Transport Helicopter, and Other Helicopter), End-User Service (Air Force, Army Aviation, Naval/Marine Corps Aviation, and More), Engine Type (Single Engine and Twin Engine), Application (Combat and Close Air Support, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America captured 44.80% of 2025 spending, anchored by multibillion-dollar CH-53K, UH-60M, and CH-47F orders underway at the US Army, Navy, and Marine Corps. Robust industrial depth supports quick retrofit campaigns, reinforcing aftermarket dominance that shapes global standard-setting across avionics, armament, and cybersecurity. Canada supplements demand with CH-148 Cyclone maritime units, while Mexico's procurement of light utility models for border patrol increases cross-border MRO cooperation.

Asia-Pacific, the fastest-growing geography at 5.57% CAGR, accelerates on indigenous efforts such as China's Z-20, India's IMRH, and South Korea's Surion line. Regional tensions in the East and South China Seas push air forces to maintain high readiness, prompting service-life extensions and block upgrades that embed local content mandates. Australia's MRH-90 replacement and Japan's UH-2 license-build illustrate how allied nations hedge supply-chain risk by co-producing under offset agreements, thereby enlarging regional economic multipliers tied to the military helicopters market. Europe remains a stable yet budget-constrained buyer focused on collaborative platforms like NH90 and Tiger to maximize interoperability and spread R&D outlays. The EUR 14 billion (USD 16.27 billion) NGRC roadmap ensures that partner states sustain joint research into advanced propulsion, material science, and digital cockpits, though actual unit orders may lag parliamentary appropriations. The Middle East and Africa continue opportunistic purchases funded by hydrocarbon revenues or external security grants, typically favoring off-the-shelf US or European models that deliver quick capability boosts. South American demand stays moderate, driven by counter-narcotics and SAR needs that lean on rugged, multi-mission airframes assembled through local final-assembly lines when possible.