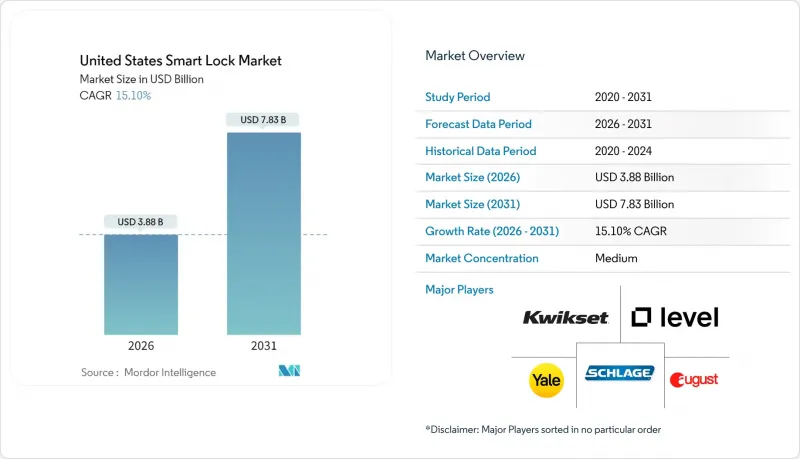

미국의 스마트 락 시장은 2025년 33억 7,000만 달러에서 2026년에는 38억 8,000만 달러에 이르고, 2026-2031년 CAGR 15.1%로 성장을 지속하여 2031년까지 78억 3,000만 달러에 달할 것으로 예측됩니다.

출하량 측면에서 시장 규모는 2025년 1,746만 대에서 2030년까지 3,903만 대로 확대될 것이며, 예측 기간(2025-2030년) 동안 17.45%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이러한 성장의 배경에는 지속적인 택배 도난 사건, 스마트홈 생태계의 성숙, 주류 스마트폰에 초광대역(UWB) 기술의 통합 등이 있습니다. 기존 도어 하드웨어와의 호환성이 주거 분야에서의 보급을 뒷받침하는 한편, 특수 잠금장치는 상업시설의 리노베이션에서 주목받고 있습니다. 임대용 분양주택 개발업체와 보험 인센티브가 수요를 촉진하고, 주요 브랜드 간의 전략적 통합이 온라인과 오프라인 채널 모두에서 경쟁이 심화되고 있습니다.

제조업체들이 Amazon Alexa, Google Home, Apple HomeKit과의 네이티브 호환성을 실현하면서 스마트 락에 대한 수요가 가속화되고 있습니다. Matter over Thread 프로토콜의 등장으로 디바이스 통신이 표준화되어 스마트 락이 에너지 절약형 메시 노드로 기능할 수 있게 되었습니다. Yale Assure Lock 2는 자체 허브 없이 여러 생태계를 넘나들며 작동하며, 이러한 변화를 구현하고 있습니다. 음성으로 잠금해제는 음성 패턴과 상황에 따른 신호로 인증을 다층화하여 보안성과 편의성을 향상시켰습니다. 추가되는 스마트 디바이스가 추가될 때마다 네트워크 전체의 유용성이 높아지고, 사용자가 개별 솔루션에서 통합 액세스 관리로 전환함에 따라 업데이트 주기가 빨라집니다.

2024년에는 2억 6,000만 건 이상의 배송물이 도난당해 2,200억 달러 상당의 상품이 분실됐습니다. 스마트 락은 배달원을 위한 임시 코드 발급을 통해 '라스트 미터 보안'을 해결하고, 실내 또는 현관 홀에 짐을 맡길 수 있도록 합니다. 아마존의 '키(Key)' 프로그램은 감시된 접근과 책임 보상을 통해 주류로 받아들여질 수 있는 가능성을 입증했습니다. 청소부, 의료 보조원 등의 서비스 제공업체에게도 유사한 기능이 확장되어 보험사나 부동산 관리회사를 만족시킬 수 있는 감사 로그를 제공합니다.

2024년 학술 시험에서 주류 스마트 락에서 14건의 제로데이 취약점이 확인되었습니다. 문제점으로는 정적 블루투스 GATT 값, 433MHz 리플레이 벡터, RFID 클론 공격 등이 있습니다. 일부 구형 하드웨어는 무선 업데이트 기능이 없어 사용자를 위험에 빠뜨릴 수 있습니다. 새로운 모델이 암호화 스토리지와 강력한 암호화 기술을 추가하는 한편, 주목받는 실증 실험이 신뢰를 떨어뜨리고 있습니다. 규제 당국은 위협의 진전을 따라잡지 못하고 있으며, 소비자는 자주 결함을 지적하는 제3자 감사에 의존할 수 밖에 없습니다.

데드볼트식 잠금장치는 미국에서 생산되는 대부분의 문이 이 형식에 대응하는 구멍이 뚫려 있기 때문에 2025년 미국 스마트 락 시장 점유율의 61.12%를 차지하였습니다. 기존 도어에 쉽게 장착할 수 있어 DIY 도입을 촉진하고, 주요 브랜드의 플랫폼 지원은 데드볼트의 강점을 강화합니다. 이 부문은 빈번한 보험 할인과 비디오 초인종 및 센서를 포함한 풍부한 액세서리 생태계의 혜택을 누리고 있습니다. 상업시설 개보수에서 건축에 특화된 하드웨어가 요구됨에 따라, 인레이 잠금장치 및 레버 잠금장치와 같은 특수 카테고리는 17.43%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 이 제품들은 생체 인식 패드와 같은 고급 인증 기능을 통합하여 평균 판매 가격과 수익률을 높이고 있습니다.

특수 분야의 성장은 상업용 건물의 리노베이션, 접객 산업의 리트로핏, 디자인 일관성을 중시하는 고급 주거용으로 인한 것입니다. 미국 스마트 락 시장에서의 인그레이빙 잠금 솔루션의 규모는 시스템 통합사업자들이 출입통제 시스템을 빌딩 자동화 플랫폼과 번들로 제공하면서 꾸준히 확대될 것으로 예측됩니다. 견고한 자물쇠는 내후성이 중요한 야외 보관 및 건설 현장의 요구를 충족시킵니다. 틈새 시장이긴 하지만, 자물쇠 분야는 현관문을 넘어 스마트 액세스 기능을 가지고 있어 벤더의 수익 기회를 확대하고 있습니다.

2025년에는 단독주택의 방대한 설치 기반과 DIY 문화의 확대로 인해 주택 구매자가 수익의 88.90%를 차지했습니다. 음성비서와의 상호운용성과 보험료 할인이 가정용 수요를 뒷받침하고 있습니다. 배터리 수명 개선으로 교체 주기는 연장되지만, UWB 및 Matter 기능을 통한 차세대 제품으로의 교체 의향은 여전히 높으며, 업그레이드 의향은 견고합니다. 반면, 상업시설에서의 도입은 18.28%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 부동산 관리 회사는 기계식 키 관리에 따른 인건비를 절감하는 중앙집중식 인증 관리를 높이 평가했습니다.

클라우드 대시보드를 통해 시설 관리자는 수백 개의 출입문에 대한 접근 권한을 몇 초 만에 부여 및 취소할 수 있습니다. 미국의 스마트 락 시장 규모는 감사 컴플라이언스가 기술 도입을 촉진하는 공동주택, 의료시설 등 상업용에서 급성장할 것으로 예측됩니다. 기업의 ESG 목표가 높아짐에 따라 에너지 관리 시스템 및 점유율 분석과 통합 가능한 스마트 잠금 장치도 증가합니다.

미국 스마트 락 시장 보고서는 제품 유형(데드볼트, 패드락, 기타), 최종 사용자(주거용, 상업용), 설치 유형(리노베이션, 신축 통합), 유통 채널(온라인, 오프라인)로 분류됩니다. 시장 예측은 금액(USD)과 수량(출하량)으로 제공됩니다.

The United States Smart Lock Market is expected to grow from USD 3.37 billion in 2025 to USD 3.88 billion in 2026 and is forecast to reach USD 7.83 billion by 2031 at 15.1% CAGR over 2026-2031.

In terms of shipment volume, the market is expected to grow from 17.46 million units in 2025 to 39.03 million units by 2030, at a CAGR of 17.45% during the forecast period (2025-2030). Momentum stems from persistent package-theft incidents, broader smart-home ecosystem maturity, and ultra-wideband (UWB) integration in mainstream smartphones. Deadbolt compatibility with existing door hardware underpins widespread residential adoption, while specialty locks gain traction in commercial retrofits. Build-to-rent developers and insurance incentives accelerate demand, and strategic consolidation among leading brands reinforces competitive intensity across both online and offline channels.

Smart lock demand accelerates as manufacturers achieve native compatibility with Amazon Alexa, Google Home, and Apple HomeKit. The arrival of the Matter over Thread protocol standardizes device communication and allows smart locks to function as energy-efficient mesh nodes. Yale Assure Lock 2 operates across multiple ecosystems without proprietary hubs, illustrating this shift. Voice-activated unlocking now layers authentication through voice patterns and contextual cues, improving security and convenience. Each additional smart device increases overall network utility, prompting replacement cycles as users transition from point solutions to unified access management.

More than 260 million deliveries faced theft in 2024, representing USD 20 billion in lost goods. Smart locks solve last-meter security by issuing temporary codes for delivery personnel, enabling in-home or vestibule drops. Amazon's Key program demonstrated mainstream acceptance when monitored access and liability coverage are present . The same capability extends to service providers such as cleaners and healthcare aides, offering audit logs that satisfy insurers and property managers.

Academic testing in 2024 revealed 14 zero-day flaws in mainstream smart locks. Issues include static Bluetooth GATT values, 433 MHz replay vectors, and RFID cloning. Some older hardware lacks over-the-air update capability, leaving users exposed. High-profile demonstrations erode trust, even as new models add encrypted storage and stronger cryptography. Regulators lag behind the threat curve, so consumers rely on third-party audits that frequently uncover gaps.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Deadbolt locks accounted for 61.12% of the US Smart Lock Market share in 2025 because most US doors are pre-bored for this format. Retrofit convenience encourages DIY adoption, and platform support from dominant brands reinforces deadbolt strength. The segment benefits from frequent insurance discounts and a rich accessory ecosystem that includes video doorbells and sensors. Specialty categories such as mortise and lever locks grow at a 17.43% CAGR as commercial renovations demand architecture-specific hardware. These products integrate advanced credentials such as biometric pads, which lift the average selling price and margin.

Specialty growth stems from commercial building upgrades, hospitality retrofits, and high-end residential applications that favor design continuity. The US Smart Lock Market size for mortise solutions is forecast to expand steadily as system integrators bundle access control with building automation platforms. Rugged padlocks address outdoor storage and construction needs where weather sealing is critical. Although niche, the padlock segment proves smart access utility beyond the front door, broadening vendor addressable revenue.

Residential buyers represented 88.90% of revenue in 2025 due to the enormous installed base of single-family homes and growing DIY culture. Voice-assistant interoperability and discounted insurance premiums sustain household demand. Battery life improvements lengthen replacement cycles, but upgrade intent remains high because UWB and Matter features motivate second-generation purchases. Commercial deployments, however, record an 18.28% CAGR. Property managers value centralized credential management that trims labor costs tied to mechanical key turnover.

Cloud dashboards let facilities revoke or grant access across hundreds of doors within seconds. The US Smart Lock Market size for commercial applications is forecast to rise sharply in multi-family and healthcare properties, where audit compliance drives technology adoption. Rising corporate ESG goals also favor smart locks that integrate with energy management systems and occupancy analytics.

The United States Smart Lock Market Report is Segmented by Product Type (Deadbolt, Padlock, Other Product Types), End-User (Residential, Commercial), Installation Type (Retrofit, New-Construction Integrated), and Distribution Channel (Online, Offline). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Shipments).