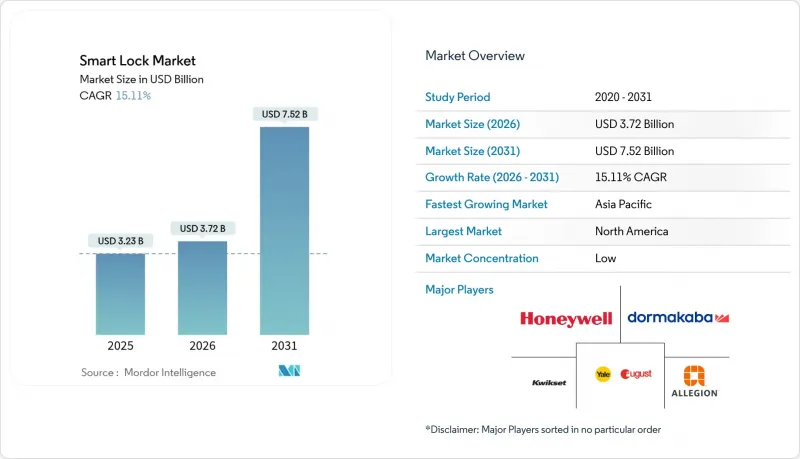

스마트락 시장은 2025년에 32억 3,000만 달러로 평가되었고, 2026년 37억 2,000만 달러에서 2031년까지 75억 2,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 15.11%로 예상됩니다.

이러한 전망은 스마트홈 플랫폼의 성숙, 도시 지역의 보안에 대한 관심 증가, 원격 출입문 접근을 가능하게 하는 IoT 연결성 확대가 결합되어 형성되고 있습니다. Matter 및 Thread 표준을 통한 상호운용성의 발전으로 많은 통합 장벽이 해소되고 있습니다. 한편, 생체 인식 센서의 가격 하락으로 인해 주거용 및 경상업용 모델 모두에서 기능 세트가 확대되고 있습니다. 반도체 부족에 따른 가격 상승은 단기적인 역풍이지만, 보험료 할인과 총소유비용(TCO) 절감 효과로 인해 기계식 잠금장치의 대체가 지속적으로 촉진되고 있습니다. 인수 활동의 활성화는 기존 출입통제 리더 기업들이 규모, 판로, 핵심 기술 확보를 위해 입지를 다지고 있다는 것을 보여줍니다.

통합 기기 제어에 대한 선호도가 높아짐에 따라 스마트 잠금장치의 통합은 커넥티드 홈의 첫 번째 업그레이드 중 하나가 되었습니다. Yale, Schlage, Level의 Matter over Thread 출시로 벤더 종속성을 해소하고 배터리 수명을 12개월 이상 연장했습니다. 음성비서는 이미 미국 가구의 70%에 보급되어 음성 인식 잠금장치의 도입을 가속화하고 있습니다. 2026년까지 예정된 Thread 1.4의 채택으로 추가 허브 없이도 신제품이 기존 네트워크에 연결될 수 있게 되어 생태계의 정착성을 더욱 강화할 수 있습니다.

도시 지역의 범죄 패턴은 주택 소유자의 경각심을 높이고 있으며, 데이터에 따르면 침입자의 83%가 침입 전에 방범 시설을 조사하고 있다고 합니다. 스마트 잠금장치와 영상인증의 통합으로 기존 시스템에서 흔히 발생하는 15초의 경보 대응 지연을 해소할 수 있습니다. Lockly의 얼굴인식 엔진은 현재 1.5초 만에 부정한 얼굴을 감지하고 실시간 경보를 발령하여 기회주의 범죄를 억제합니다. 생체 인식과 PIN의 다단계 조합은 익명성이 침입을 조장하기 쉬운 고밀도 주거용 고층 건물에 다층적인 보호 기능을 추가합니다.

주목받는 침해 사례로 인해 주류 모델에서 생체 인증 우회 및 복제 가능한 NFC 태그의 문제가 드러났습니다. 한 소비자 단체의 테스트에 따르면, 칩 작동식 장치의 85.7%가 적어도 한 가지 이상의 심각한 결함이 있는 것으로 나타났습니다. 벤더들은 현재 엔드투엔드 암호화와 이중 인증을 제공하고 있지만, 단편화된 하드웨어 설계로 인해 보편적인 패치 적용을 유지하기가 어렵습니다. 커넥티비티 표준화 연맹 내 업계 단체들이 기본 요구사항을 수립 중이지만, 구현의 편차가 사이버 리스크의 고착화를 초래하고 있습니다.

데드볼트는 2025년 매출의 45.12%를 차지할 것으로 예상되며, 이는 물리적 견고성에 대한 주택 소유자들의 폭넓은 신뢰를 반영합니다. 이 점유율은 하드웨어 형태의 스마트 잠금장치 시장 규모에서 가장 큰 비중을 차지합니다. 레버 핸들 시스템은 호텔과 사무실의 ADA(미국 장애인법) 준수 필요성 때문에 15.18%의 최고 수준의 CAGR을 달성하여, 조작의 용이성이 교통량이 많은 환경에서 얼마나 매력적인지 보여주고 있습니다.

눈에 띄지 않는 업그레이드를 원하는 소비자들은 기존 하우징 안에 전자 부품을 숨기는 레트로핏 실린더에 대한 관심이 높아지고 있으며, 레벨의 보이지 않는 메커니즘이 그 대표적인 예입니다. 자물쇠 스타일의 스마트 기기는 실외 산업 이용 사례에 적합하지만, 내후성 비용으로 인해 틈새 시장으로 분류됩니다. 지속적인 소형화로 인해 카테고리 경계가 모호해질 것으로 예상되지만, 데드볼트는 2031년까지 스마트 잠금장치 시장에서 압도적인 존재감을 유지할 것으로 예측됩니다.

2025년 기준 블루투스는 61.68%의 점유율을 차지하며 연결 방식 중 스마트 잠금장치 시장 점유율 1위를 유지했습니다. 스마트폰과 잠금장치의 페어링 편의성은 라우터 연결이 불안정한 임대주택에 적합합니다. 그러나 통신 범위와 메시 네트워크의 제약으로 인해 공동주택에는 적합하지 않습니다.

Zigbee-Thread 스택은 Matter 인증과 Silicon Labs의 초저전력 SoC에 힘입어 16.74%의 연평균 복합 성장률(CAGR)이 예상됩니다. Wi-Fi는 배터리 소모를 수반하는 것, 직접적인 원격 조작을 우선시하는 클라우드 우선 배포에서 계속 채택되고 있습니다. 신기술인 초광대역(UWB)은 핸즈프리로 고정밀 조작이 가능하지만, 출하량이 확대되기 전까지는 '기타' 카테고리로 분류됩니다. 프로토콜 전반에 걸쳐 표준화가 진행되면서 분절화가 줄어들고 있으며, 이러한 추세는 스마트 잠금장치 시장 전체의 보급 곡선을 끌어올릴 것입니다.

스마트 잠금장치 시장은 잠금장치 유형(데드볼트, 레버 핸들 등), 통신 기술(블루투스, Wi-Fi 등), 인증 방식(PIN 코드/키패드, 생체 인증(지문, 얼굴 등), 최종 사용자(주거용, 상업용 사무실 등), 그리고 지역별로 세분화됩니다. 세분화됩니다. 시장 예측은 금액(USD)으로 제공됩니다.

북미는 스마트홈의 조기 도입, 유리한 건축 기준, 커넥티드 보안에 대한 최대 10%의 보험 할인으로 인해 2025년 매출의 37.05%를 차지할 것으로 예측됩니다. 미국에서는 개발업체들이 스마트 잠금장치를 표준 설비 패키지로 간주하고 있어 리노베이션 수요가 주도하고 있습니다. 캐나다는 비슷한 건축 기준과 브로드밴드 보급률을 활용하여 이를 따라가고 있습니다.

아시아태평양은 15.42%의 가장 높은 CAGR을 나타낼 것으로 예상되며, 이는 급속한 도시로의 인구 이동과 중산층의 가처분 소득 증가를 반영하고 있습니다. 중국은 스마트홈 출하량에서 선두를 달리고 있으며, 인도 주택 자동화 시장은 39.79%의 성장 전망을 보이고 있으며, 스마트 잠금장치는 소비자의 업그레이드 목록에서 높은 순위를 차지하고 있습니다. 일본에서는 고령화가 진행되는 인구 구성을 배경으로 고령자의 자립을 지원하는 비접촉식 도어 솔루션이 주목받고 있습니다.

유럽에서는 에너지 절약 지침과 강력한 프라이버시 감시를 기반으로 꾸준한 진전을 보이고 있습니다. 고도의 암호화 요구사항은 개발 비용을 증가시키지만, GDPR(EU 개인정보보호규정)을 준수하는 차별화된 제품 제공을 촉진하고 있습니다. 중동 및 아프리카은 현재 규모가 작지만, 신규 개발 부동산 프로젝트에 포함된 스마트시티 투자의 수혜를 받아 스마트 잠금장치 시장 전망 기반을 강화하는 비약적인 도입 경로를 실현하고 있습니다.

The smart lock market was valued at USD 3.23 billion in 2025 and estimated to grow from USD 3.72 billion in 2026 to reach USD 7.52 billion by 2031, at a CAGR of 15.11% during the forecast period (2026-2031).

The outlook highlights the convergence of maturing smart-home platforms, rising urban security concerns, and expanding IoT connectivity that favors remote door access. Interoperability progress through the Matter and Thread standards now removes many integration barriers, while declining biometric sensor prices are broadening feature sets across both residential and light-commercial models. Price increases linked to semiconductor shortages are a near-term headwind, yet insurance premium discounts and total-cost-of-ownership savings continue to encourage replacement of mechanical locks. Intensifying acquisition activity shows established access-control leaders positioning to secure scale, channel reach, and core technology.

Growing preference for unified device control makes smart lock integration one of the first upgrades in connected homes. Matter-over-Thread launches by Yale, Schlage, and Level are removing vendor lock-in and extending battery life to more than 12 months. Voice assistants already reside in 70% of United States households, which accelerates voice-enabled locking. Scheduled Thread 1.4 adoption by 2026 will let new products join existing networks without additional hubs, further tightening ecosystem stickiness.

Urban crime patterns have raised homeowner vigilance, and data show 83% of burglars survey security setups before entry. Integrating a smart lock with video verification closes the 15-second alarm response gap common in legacy systems. Lockly's facial recognition engine now flags unauthorized faces in 1.5 seconds, sending real-time alerts that deter opportunistic crime. Multi-factor combinations of biometrics and PINs add layered protection for dense residential high-rises where anonymity often aids break-ins.

High-profile breaches have exposed biometric bypasses and cloneable NFC tags in mainstream models. Tests by one consumer association found 85.7% of chip-activated units exhibited at least one critical flaw. Vendors now ship end-to-end encryption and two-factor log-ins, yet fragmented hardware designs make universal patching hard to maintain. Industry groups within the Connectivity Standards Alliance are drafting baseline requirements, but wide variation in implementation keeps cyber-risk elevated.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Deadbolts retained 45.12% of 2025 revenue, reflecting widespread homeowner confidence in their physical robustness. This share equates to the largest slice of the smart lock market size for hardware formats. Lever handle systems achieved the leading 15.18% CAGR due to ADA compliance needs in hotels and offices, demonstrating how ease-of-operation appeals to high-traffic settings.

Consumers seeking discreet upgrades have driven interest in retrofit cylinders that hide electronics inside existing housings, exemplified by Level's invisible mechanism. Padlock-style smart devices service out-door industrial use cases but remain niche because of weather-proofing costs. Continuous miniaturization will likely blur category boundaries, though deadbolts are expected to keep a commanding presence through 2031 in the smart lock market.

Bluetooth held 61.68% share in 2025, translating into the top position within the smart lock market share for connectivity. Its phone-to-lock pairing simplicity favors rental properties where router access is uncertain. Range and mesh limitations, however, make it less suited to multi-unit dwellings.

The Zigbee-Thread stack is projected for a 16.74% CAGR, propelled by Matter certification and Silicon Labs' ultra-low-power SoCs. Wi-Fi continues in cloud-first deployments that prioritize direct remote control despite battery drain. Emerging ultra-wideband adds hands-free precision but sits within the "Others" bucket until shipping volumes scale. Across protocols, standardization is shrinking fragmentation, a trend that will raise the overall smart lock market adoption curve.

Smart Lock Market is Segmented by Lock Type (Deadbolt, Lever Handle, and More), Communication Technology (Bluetooth, Wi-Fi, and More), Authentication Method (Pin-Code / Keypad, Biometric (Fingerprint, Face), and More), End User (Residential, Commercial Offices, and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America secured 37.05% of 2025 revenue due to early smart-home adoption, favorable codes, and insurance discounts of up to 10% for connected security. The United States drives renovation demand as developers view smart locks as standard amenity packages. Canada follows, leveraging similar building norms and broadband penetration.

Asia-Pacific is set for the highest 15.42% CAGR, reflecting rapid urban migration and growing middle-class disposable income. China leads smart-home shipments, while India's residential automation pipeline shows a 39.79% expansion outlook that positions smart locks near the top of consumer upgrade lists. Japan's aging demographic attracts contactless door solutions supporting senior independence.

Europe posts steady progression anchored by energy-efficiency directives and strong privacy oversight. Advanced encryption requirements raise development costs yet promote differentiated offerings that comply with GDPR. The Middle East and Africa, though smaller today, benefit from smart-city investments baked into greenfield real-estate projects, enabling leapfrog adoption paths that raise the future baseline of the smart lock market.