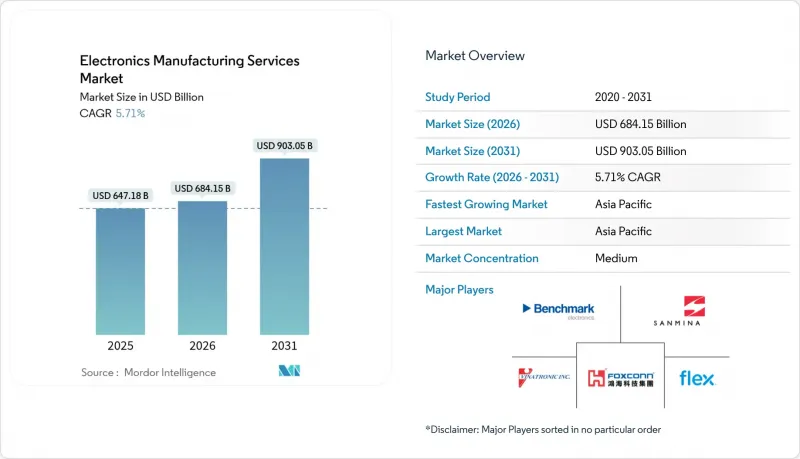

전자기기 제조 서비스 시장은 2025년 6,471억 8,000만 달러에서 2026년에는 6,841억 5,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 5.71%를 기록하며 2031년까지 9,030억 5,000만 달러에 달할 것으로 예측됩니다.

이러한 성장 궤적은 OEM 업체들이 조사개발에 집중하면서 최첨단 조립 기술을 활용하기 위해 지속적으로 외주화를 선택하는 경향을 반영하고 있습니다. AI 인프라 장비에 대한 수요, 자동차의 급속한 전동화, 그리고 중국에서 다양한 지역 거점으로의 공급망 회귀가 가장 두드러진 성장 촉진요인입니다. IEC 60601 및 RoHS III 관련 규제 비용, 반도체 가격 변동, 사이버 보안 요구 사항 증가로 인해 공급업체들은 컴플라이언스 대응 공장에 대한 통합과 투자를 늘리고 있습니다. 한편, 디지털 MES 플랫폼에 대한 스마트 팩토리 투자는 생산성을 향상시키고 다품종 소량 생산 프로그램에서의 차별화를 실현합니다.

다품종 소량 생산 프로그램을 위한 고자본 집약적 금형 설비는 2025년 이전에 더 많은 북미 및 유럽 OEM 제조업체를 EMS 파트너에 의존하게 만들었습니다. 제너럴 모터스(GM)의 MES 4.0 도입 사례는 외부 파트너가 복잡한 조립 공정을 맡으면서도 디지털 통합을 통해 현장의 가시성을 향상시킨 사례를 보여줍니다. 아웃소싱을 통해 브랜드 소유자는 디자인, 소프트웨어, 시장 출시 업무에 지출을 재분배할 수 있습니다. 공급업체는 산업용 컨트롤러 제조에서 단기간에 의료기기 생산으로 전환할 수 있는 유연한 라인을 제공함으로써 재공구화 없이 전환할 수 있는 이점을 얻었습니다. 2024년부터 2025년 사이에 6개월마다 빠른 반복이 필요한 민생 전자기기 분야에서 턴키 프로그램에 대한 수요가 급증했습니다. 제품의 복잡성 증가로 사내 라인이 대응에 쫓기는 가운데, 이 요인으로 인해 2027년까지 높은 수준의 거래량이 유지될 것으로 예상됩니다.

관세 불확실성과 팬데믹 기간의 물류 혼란으로 인해 2024년 PCB 및 박스 빌드 생산능력은 멕시코, 동유럽, 아세안 지역으로 빠르게 이전했습니다. 베트남에 3억 8,300만 달러를 투자한 폭스콘의 기판 공장은 단일 국가 의존도 탈피를 상징하는 사례입니다. 멕시코는 USMCA를 활용해 미국향 자동차 및 서버랙 프로그램을 확보하고, 폴란드와 루마니아는 유럽 EV 플랫폼을 타겟으로 삼았습니다. 현지화를 통해 운송 리드타임을 최대 40% 단축하고 재고 리스크를 줄였습니다. 소량 생산 업체도 비슷한 전략을 채택하여 최종사용자와 가까운 곳에서 맞춤 제작을 유지했습니다. 인플레이션으로 인한 운임 상승과 지정학적 긴장으로 인해 거점 분산에 대한 수요가 지속됨에 따라 이러한 추세는 2025년에도 가장 강력하게 유지될 것으로 보입니다.

2024년 메모리 및 전력 디바이스 가격이 두 자릿수 변동률을 보이며, 고객 계약에 따라 분기별 부품 원가가 고정된 EMS 기업들은 큰 영향을 받았습니다. 공급 프레임의 데이터에 따르면, 부품의 75%는 가격이 안정되거나 하락한 부품이며, 고 대역폭 메모리는 심각한 부족에 직면하여 AI 서버 구축에 부담을 주었습니다. 대형 업체들은 칩 제조업체에 대한 선지급과 위탁거래를 통한 헤징을 실시했지만, 중소기업들은 수익률 압박을 흡수할 수밖에 없었습니다. 노후화가 가속화되면서 재고 버퍼의 리스크가 높아졌고, 변동성을 극복하기 위해서는 규모가 중요해졌기 때문에 통합이 진행되었습니다. 2025년 초에는 가격이 안정세를 보였지만, 전략적 조달의 번거로움이 수익의 발목을 잡고 있는 상황은 변하지 않았습니다.

인쇄회로기판 조립 및 박스 빌드 서비스는 전자기기 제조 서비스 시장 매출의 61.85%를 차지했습니다. 폐쇄형 지속가능성에 대한 선호도가 높아지면서 애프터마켓 서비스는 8.05%의 CAGR로 성장하여 전체 전자기기 제조 서비스 시장을 능가하는 성장세를 보였습니다. 각 공급업체들은 주요 대륙에 수리 거점을 확장하여 납기를 단축하고 전자폐기물을 줄이기 위해 노력했습니다. OEM 업체들이 동시 병렬 설계를 통한 비용 절감을 추구하면서 전자기기 설계 및 엔지니어링 업무가 활성화되었습니다. 시제품 및 신제품 도입 라인은 로트 규모를 축소한 것으로, 초기 제품 일정을 몇 주 단축하여 높은 수익률을 실현하였습니다. 시험인증연구소는 새로운 규제 체크리스트에 대응하기 위해 전기 안전 평가와 더불어 사이버 보안 평가를 통합하고 있습니다.

2025년에는 EU의 순환경제 지침에 따라 부품 회수 및 재생사업이 수익원으로 자리 잡았습니다. 주요 EMS 사업자는 디지털 트윈을 도입하여 기판 레벨의 고장 예측 및 예비 부품의 사전 준비를 실현하고 있습니다. 산업 자동화 및 가전제품에서 하드웨어 구독 모델이 확산되고 있는 가운데, 애프터서비스가 계약 갱신의 핵심이 되고 있습니다. 경쟁 우위는 전 세계 창고 네트워크의 밀집도와 데이터 기반 고장 분석에 따라 달라질 것입니다.

계약 제조는 2025년 매출의 70.92%를 차지하며 기반을 유지했지만, 브랜드가 원스톱 솔루션을 찾는 가운데 주문자상표부착생산(ODM)의 성장률을 상회했습니다. ODM 매출은 연평균 8.76% 증가할 것으로 예상되며, 설계, 조달, 이행을 일괄 도급하는 하이브리드형 벤더가 전자기기 제조 서비스 시장을 주도할 것으로 보입니다. AI 서버, 의료기기 등 안전한 공급망이 요구되는 분야에서는 턴키 제조가 주목을 받았습니다. 프라이빗 브랜드 제조는 브랜드 차별화보다 비용 우위가 요구되는 틈새 가전과 스마트 조명 분야에서 수요를 충족시켰습니다.

대만계 제공업체는 세계 시장에 사전 인증된 화이트 박스 플랫폼을 제공함으로써 경계를 모호하게 만들었습니다. Foxconn과 Wistron은 고객이 자체 브랜드화할 수 있는 레퍼런스 디자인을 도입하여 제품 출시 시간을 단축했습니다. 적어도 단순 설계 능력을 개발하지 못하는 위탁생산 기업은 상품화가 진행되는 조립 환경에서 수익률 압축 리스크에 직면하게 됩니다.

전자기기 제조 서비스(EMS) 시장은 서비스 유형(전자기기 설계 및 엔지니어링, 프로토타입 및 신제품 도입 서비스, 인쇄회로기판 조립 등), 비즈니스 모델(위탁 제조, 턴키 제조 등), 제조 공정(표면 실장 기술, 스루홀 기술, 혼합 기술 등), 최종 이용 산업(모바일 기기, 민수용 전자기기 등), 지역별로 구분됩니다. 모바일 기기, 민생용 전자기기 등), 및 지역별로 구분됩니다.

아시아태평양은 2025년 매출의 47.05%를 차지하며 12.52%의 CAGR을 기록해 지역 중 가장 높은 성장률을 기록할 것으로 예상됩니다. 이는 기업이 중국에서의 규모 생산을 유지하면서 베트남, 인도, 태국으로 다변화했기 때문입니다. 인도 정부의 PLI 제도의 특혜는 휴대폰 및 웨어러블 기기 프로그램을 유치하고, 베트남은 미국을 위한 고층 PCB의 우선적인 입지가 되었습니다. 북미에서는 멕시코 산업회랑에 대한 투자가 활발합니다. 많은 전기자동차 제조업체들이 2026년까지 현지 생산능력을 확보할 것을 요구하고 있습니다. 국방 전자제품의 국내 조달 규정에 따라 애리조나주와 텍사스에 신공장이 건설되었습니다. 유럽은 높은 인건비에도 불구하고 OEM 설계 센터와의 근접성을 활용하여 규제가 엄격한 의료 및 산업 프로그램을 우선시합니다.

남미의 점유율은 여전히 미미하지만, 브라질과 멕시코가 자동차 최종 조립 관련 전자기기 클러스터를 추진하면서 성장했습니다. 대만의 PCB 생태계는 2025년까지 연평균 5.8%로 성장할 것으로 예상되며, 전 세계 AI 서버 제조업체에 첨단 기판을 공급하고 있습니다. 중동 및 아프리카에서는 스마트 미터 및 재생에너지 제어장치에 대한 초기 투자가 교육 이니셔티브와 함께 이뤄지는 경우가 늘고 있습니다. 탈탄소화 프로젝트가 현지 조달 전자부품을 요구함에 따라 신흥 지역의 전자기기 제조 서비스 시장 규모는 확대될 것입니다.

The electronic manufacturing services market is expected to grow from USD 647.18 billion in 2025 to USD 684.15 billion in 2026 and is forecast to reach USD 903.05 billion by 2031 at 5.71% CAGR over 2026-2031.

The growth trajectory reflects OEMs' ongoing preference for outsourcing to focus on R&D while accessing cutting-edge assembly capabilities. Demand for AI infrastructure equipment, the rapid electrification of vehicles, and a wave of supply-chain reshoring from China to diversified regional hubs are the most visible accelerants. Regulatory costs tied to IEC 60601 and RoHS III, volatile semiconductor pricing, and mounting cybersecurity requirements have pushed providers to consolidate and invest in compliance-ready plants. Meanwhile, smart-factory investments in digital MES platforms sharpen productivity and offer differentiation in high-mix, low-volume programs.

Capital-intensive tooling for high-mix, low-volume programs pushed many North American and European OEMs to rely on EMS partners prior to 2025. General Motors' MES 4.0 roll-out illustrated how digital integration improved shop-floor visibility while external partners handled complex assemblies. Outsourcing lets brand owners redirect spending toward design, software, and go-to-market work. Providers benefited by offering flexible lines that could switch from an industrial controller build to a short-run medical device without retooling. Over 2024-2025, demand for turnkey programs rose sharply in consumer electronics, where six-month refresh cycles require rapid iteration. This driver is poised to keep transaction volumes high through 2027 as product complexity grows and in-house lines struggle to keep pace.

Tariff uncertainty and pandemic-era logistics disruptions triggered a fast relocation of PCB and box-build capacity toward Mexico, Eastern Europe, and ASEAN in 2024. Foxconn's USD 383 million board plant in Vietnam typified the movement away from single-country dependence. Mexico leveraged USMCA to secure automotive and server rack programs for the United States, while Poland and Romania targeted European EV platforms. Localization reduced freight lead times by up to 40% and lowered inventory risk. Small-batch manufacturers adopted the same strategy to keep custom builds closer to end customers. The trend remains strongest in 2025 as inflationary freight rates and geopolitical tensions sustain the need for diversified footprints.

Memory and power devices swung in price by double-digit percentages during 2024, leaving EMS firms exposed when customer contracts locked BOM prices for quarters in advance. Supplyframe data showed that 75% of components either stabilized or declined, yet high-bandwidth memory faced acute shortages, straining AI server builds. Large providers prepaid chipmakers or hedged with consignment deals, but small firms absorbed margin pressure. Higher obsolescence made inventory buffers riskier, prompting consolidation as scale became critical to weather volatility. Although prices moderated in early-2025, strategic sourcing complexity remains a drag on earnings.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

PCB assembly and box-build services contributed 61.85% of the electronic manufacturing services market revenue. Growing preference for closed-loop sustainability drove after-market services toward an 8.05% CAGR, outpacing the broader electronic manufacturing services market. Providers expanded repair hubs on every major continent to cut turnaround times and lower e-waste. Electronics design and engineering engagements intensified as OEMs sought concurrent-engineering savings. Prototype and NPI lines handled shorter lots but yielded high margins by helping brands cut weeks from first-article schedules. Testing and certification labs are integrating cybersecurity assessments alongside electrical safety to meet new regulatory checklists.

In 2025, circular-economy directives in the EU made component harvest and refurbishment viable revenue streams. Leading EMS operators embedded digital twins to predict board-level failures and pre-stage spares. As hardware subscription models spread in industrial automation and consumer devices, post-sale services will become central to contract renewals. Competitive differentiation will hinge on global depot density and data-driven failure analytics.

Contract manufacturing remained the bedrock, representing 70.92% of 2025 revenue, yet original design manufacturing grew faster as brands chased one-stop solutions. ODM revenue is set to climb 8.76% annually, pulling the electronic manufacturing services market toward hybrid engagements where design, sourcing, and fulfillment reside in one vendor. Turnkey manufacturing gained traction for AI servers and medical devices that demand secure supply chains. Private-label builds filled niche appliance and smart-lighting slots requiring cost leadership over brand differentiation.

Taiwan-based providers blurred lines by offering white-box platforms pre-certified for global markets. Foxconn and Wistron introduced reference designs that customers could brand, accelerating launch timelines. Contract manufacturers that fail to develop at least light design capabilities risk margin compression in a commoditizing assembly landscape.

Electronic Manufacturing Services (EMS) Market is Segmented by Service Type (Electronics Design and Engineering, Prototype and NPI Services, PCB Assembly, and More), Business Model (Contract Manufacturing, Turnkey Manufacturing, and More), Manufacturing Process (Surface-Mount Technology, Through-Hole and Mixed Technology, and More), and End-Use Industry (Mobile Devices, Consumer Electronics, and More), and Geography.

Asia-Pacific held 47.05% of 2025 revenue and posted a 12.52% CAGR, the highest among regions, as companies diversified into Vietnam, India, and Thailand while retaining China for scale production. Government incentives in India's PLI scheme drew handset and wearables programs, and Vietnam became a preferred site for high-layer PCBs targeting US buyers. North America enjoyed strong inflows into Mexican industrial corridors, with many EV OEMs demanding localized printed-circuit capacity by 2026. Domestic content rules in defense electronics secured new plant builds in Arizona and Texas. Europe prioritized compliance-heavy medical and industrial programs, leveraging proximity to OEM design centers despite higher labor costs.

South America's share remained modest yet grew as Brazil and Mexico advanced electronics clusters linked to automotive final assembly. Taiwan's PCB ecosystem, projected to grow 5.8% yearly through 2025, supplied advanced substrates to global AI server builders. Middle East and Africa saw initial investments in smart metering and renewable energy controllers, often bundled with training initiatives. The electronic manufacturing services market size in emerging regions will broaden as decarbonization projects demand localized electronics content.