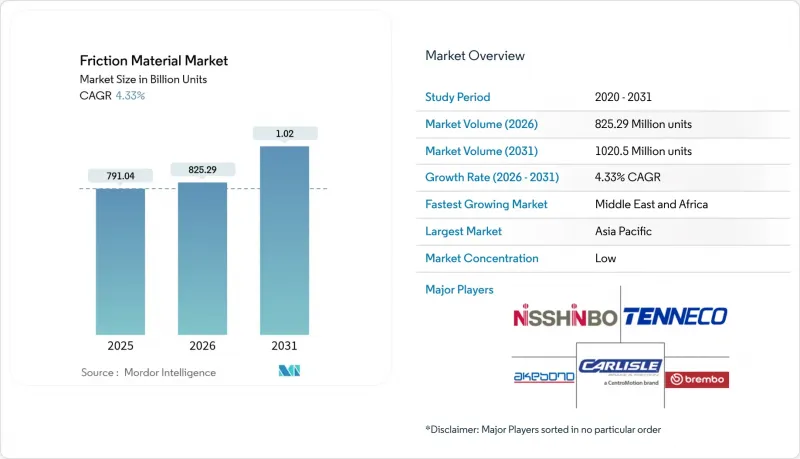

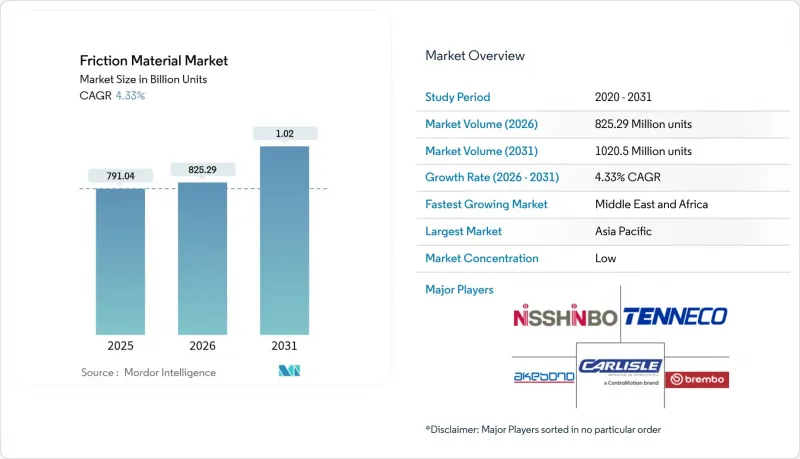

2026년 마찰 재료 시장 규모는 8억 2,529만 유닛이라고 추정되어 2025년 7억 9,104만 유닛으로부터 성장이 전망됩니다.

2031년 예측치는 10억 2,050만대로 2026-2031년 연평균 복합 성장률(CAGR) 4.33%로 성장할 전망입니다.

유로7 미립자 규제와 같은 규제적 이슈, 저분진 디스크 및 패드에 대한 활발한 수요, 자동차 보유대수 증가는 마찰재 시장을 꾸준한 성장 궤도에 올려놓았습니다. 각 제조업체들은 구리 프리를 유지하기 위해 패드의 화학 성분을 재설계하는 한편, 센서 탑재형 '스마트 패드'를 채택하여 서비스형 유지보수 수익 모델 확대에 기여하고 있습니다. 아시아태평양의 자동차 생산 능력과 깊은 애프터마켓 생태계가 지역 최대 점유율을 뒷받침하는 한편, 비용 최적화된 동유럽 공장은 구리, 아라미드, 세라믹 섬유의 가격 변동으로 인한 마진 압력을 전 세계 공급업체들이 균형을 맞추는 데 기여하고 있습니다. 경쟁의 치열함은 소프트웨어, 예측 분석, 재생 원료를 차세대 제품에 통합하는 경쟁을 벌이는 중견 지역 전문 기업과 대규모 다국적 기업들에 의해 형성되고 있습니다.

광업, 건설, 농업용 중장비는 극한의 열과 오염에 견디는 마찰 부품을 소비하기 때문에 승용차보다 더 많은 수량을 소비합니다. 자율 주행 광산 트럭에는 센서가 장착된 디스크 패드 세트가 장착되어 마모 데이터를 실시간으로 차량 관리 시스템에 전송하여 예기치 못한 다운타임을 줄입니다. 현지 지원이 제한적인 신흥 시장에서는 OEM 제조업체가 고밀도 라이닝을 채택하여 서비스 수명을 연장하고 있습니다. 통합 구동계 공급업체는 브레이크, 클러치, 리타더 시스템을 번들로 묶어 교차 판매 가능성을 높이고 있습니다. 특히 동남아시아에서는 대형 디스크의 리드타임 단축을 위해 현지에 재고가 있는 공급업체를 선정하는 경향이 증가하고 있습니다. 정부의 인프라 확충을 위한 자금 투입과 고톤급 상품 운송이 지속되는 가운데, 중기적으로 운전자 수요는 견조한 흐름을 보일 것으로 예측됩니다.

인도, 인도네시아, 베트남의 경우 평균 차령이 9년을 넘어선 가운데 자동차 보유대수 증가율이 신차 판매량을 상회하고 있어 애프터마켓용 패드 수요가 지속되고 있습니다. 도심의 밀집된 교통 환경에서는 스톱 앤 고 주행이 패드의 마모를 가속화하기 때문에 교체 주기가 단축되어 전동화로 인한 수량 감소를 상쇄하고 있습니다. 구독 서비스나 라이드 셰어링용 차량군에서는 예방정비 스케줄이 도입되고 있으며, 높은 가격에도 불구하고 마모 예측이 용이한 세라믹 패드가 채택되기 쉬워지고 있습니다. OEM 연계 서비스 네트워크에서는 여러 플랫폼에 대응하는 패드 라인의 재고를 보유하여 모델 세대를 넘어선 재고 관리를 효율화하고 있습니다. 프리미엄 패드 브랜드는 적합도 데이터를 활용한 온라인 채널을 활용하여 DIY 소비자를 타겟으로 하고 있습니다. 장기적으로 이 요인은 세계 CAGR에 가장 큰 긍정적 기여를 할 것으로 예측됩니다.

도심 사용 환경에서의 전기 승용차는 패드 수명이 10만 마일(약 16만km)을 초과하는 경우가 많아 내연기관 모델에 비해 교체 빈도가 크게 감소하고 있습니다. 차량 계산에서 저분진 패드의 가격과 유지 보수 빈도 감소를 비교 검토하기 위해 애프터마켓 채널에 이익률 압박이 발생했습니다. 적극적인 회생 에너지 회수를 하는 하이브리드 SUV는 비상 정지 시 강력한 패드 마찰력이 여전히 필요하기 때문에 고비용의 듀얼 컴파운드 솔루션이 요구됩니다. 지방 버스 사업자들은 회생 브레이크가 회수 단계에 도달하면 전체 브레이크 시스템의 총 소유 비용이 감소하고 패드 교체 시기가 지연된다고 보고하고 있습니다. 공급업체들은 수익의 초점을 수량에서 고부가가치 코팅 및 분석 기술로 전환하고 있지만, 이러한 억제요인은 마찰 재료 시장의 CAGR을 계속 억제하고 있습니다.

2025년 기준, 브레이크 패드는 마찰재 시장 점유율의 40.85%를 차지하며 세계 교체 부품 사업의 근간을 이루고 있습니다. 패드 관련 마찰재 시장 규모는 높은 마모율과 표준화된 설계 템플릿을 통한 플랫폼 간 공급의 단순화를 반영하고 있습니다. 반면, 디스크는 통합형 전자식 브레이크 시스템이 정밀한 금속 가공이 적용된 대형 로터를 요구하고 평균 판매 가격을 끌어올리면서 5.59%의 가장 빠른 CAGR을 보이고 있습니다.

패드의 개선은 계수 안정성을 유지하면서 먼지를 억제하는 구리 프리 유기농 블렌드를 중심으로 진행되고 있습니다. 로터 수요는 스프링 하중을 줄이는 벤틸레이션 디스크와 카본 세라믹 디스크를 지정하는 고급 SUV의 보급에 힘입어 호황을 누리고 있습니다. 블록과 라이닝 수요량은 철도 및 중공업 분야에서 안정적이지만, 자동화로 인해 블록 교체 간격은 연장되는 추세입니다. 클러치 페이싱과 같은 틈새 부품은 로봇 공학 및 산업 자동화의 성장을 주도하고 있습니다. 전반적인 추세는 패드가 여전히 주류를 이루고 있지만, 디스크는 매출 증가 속도가 빠르기 때문에 전 세계 공급업체의 전략적 초점이 확대되고 있습니다.

2025년 기준 마찰재 시장 규모의 37.95%를 차지할 것으로 예상되는 세미메탈릭 배합은 검증된 가성비 특성으로 인해 지지받고 있습니다. 강철 또는 구리 섬유와 유기 바인더를 결합한 이 배합은 퇴색 저항과 소음 제어의 균형을 이룹니다. 세라믹 배합은 후발주자이지만, 유로7 먼지 캡 규제와 고성능 전기차 수요에 힘입어 CAGR 5.98%로 성장하고 있습니다.

브렘보의 그린톨 레이저 증착 로터 코팅은 PM10을 줄이고 규제 준수 경제성을 변화시킬 수 있는 세라믹의 잠재력을 보여주고 있습니다. 소결금속은 철도 및 항공기 분야에서 필수적이지만, 시장 점유율은 작습니다. 아라미드 섬유가 풍부한 패드는 경량과 고강도의 특성으로 인해 항공우주 및 고성능 오토바이 시장에서 틈새 시장을 점유하고 있습니다. 단계적인 연구개발은 바이오 바인더에 초점을 맞추고 있으며, 내구성을 유지하면서 탄소 발자국을 줄이는 것을 목표로 하고 있습니다.

아시아태평양은 탄탄한 공급망, 비용 경쟁력 있는 노동력, 중국, 인도, 아세안 국가들의 자동차 보유량 급증으로 인해 2025년 마찰재 시장에서 45.90%의 압도적인 점유율을 차지할 것으로 예측됩니다. 중국의 로터 제조업체들은 주조공장과 가공공장을 동일 산업단지에 집적화하여 물류비용을 절감하고, 세계 수출 경쟁력을 뒷받침하고 있습니다. 인도에서는 이륜차 판매 회복과 애프터마켓 네트워크 확대로 2024년 상반기 매출 성장을 보고했습니다. 일본은 고성능 차량 프로그램 관련 프리미엄 디스크 기술 수출에 기여하고 있으며, 전기 이륜차 브레이크 키트 분야에서 선도적인 위치를 유지하고 있습니다.

북미와 유럽은 환경적 리더십으로 성숙한 시장 기반을 형성하고 있습니다. 유로 7과 캘리포니아의 구리 규제로 인해 이들 시장은 저분진 디스크와 센서 패드의 시험장 역할을 하고 있으며, 그 결과는 아시아태평양으로 확대되고 있습니다. 생산은 비용의 균형을 유지하면서 루마니아, 폴란드, 멕시코로 동쪽으로 이동하고 있지만, 설계 및 검증 센터는 독일, 이탈리아, 미국에 남아있습니다.

중동 및 아프리카는 건설 붐, 광물 채굴, 기후 변화에 강한 패드를 필요로 하는 수입 승용차 수요에 힘입어 4.66%의 가장 높은 지역 CAGR을 기록했습니다. 걸프협력회의는 수도권 네트워크와 경전철에 자본을 투입하여 블록과 라이닝에 대한 수요를 자극하고 있습니다. 사하라 사막 이남의 광산용 차량은 대형 습식 디스크 브레이크를 채택하고 있으며, 이는 특히 중량물 운반 트럭을 위해 설계되었습니다. 남미에서는 브라질의 자동차 생산이 점진적으로 회복되고 있음에도 불구하고 통화 변동이 애프터마켓 지출을 억제하고 있기 때문에 전망은 완만합니다.

Friction Material Market size in 2026 is estimated at 825.29 million units, growing from 2025 value of 791.04 million units with 2031 projections showing 1020.5 million units, growing at 4.33% CAGR over 2026-2031.

Regulatory milestones such as the Euro 7 particulate limits, brisk demand for low-dust discs and pads, and rising vehicle parc volumes keep the friction material market on a steady growth path. Manufacturers are re-engineering pad chemistry to remain copper-free, while adoption of sensor-enabled "smart pads" is broadening maintenance-as-a-service revenue models. The Asia-Pacific's vehicle production strength and deep aftermarket ecosystem anchor the largest regional volume share, whereas cost-optimized Eastern European plants help global suppliers balance margin pressure from volatile prices of copper, aramid, and ceramic fiber. Competitive intensity is shaped by mid-sized regional specialists and large multinational players racing to embed software, predictive analytics, and recycled inputs into next-generation products.

Heavy mining, construction, and agricultural equipment consume friction components that tolerate extreme heat and contamination, lifting unit volumes well above those of passenger vehicles. Autonomous mining trucks now feature sensor-fed disc and pad sets that transmit wear data in real-time to fleet dashboards, reducing unscheduled downtime. Original-equipment manufacturers adopt higher-density linings to extend service life in emerging markets where on-site support is scarce. Integrated drivetrain suppliers bundle brake, clutch, and retarder systems, boosting cross-selling potential. Industrial procurement teams increasingly select suppliers with localized stock points to reduce lead times on oversized discs, particularly in Southeast Asia. The driver's mid-term impact remains firm as governments fund infrastructure expansion and commodities continue to move at high tonnage.

Vehicle fleets in India, Indonesia, and Vietnam are growing faster than new-car sales, as the average car age climbs past nine years, sustaining aftermarket pad demand. Replacement intervals shorten in dense urban traffic because stop-and-go conditions accelerate pad wear, offsetting electrification-driven volume losses. Subscription and ride-hailing fleets impose proactive maintenance schedules that favor predictable-wear ceramic pads despite higher ticket prices. OEM-aligned service networks stock multi-platform pad lines to streamline inventory across model generations. Premium pad brands utilize online channels, leveraging fitment data, to target do-it-yourself consumers. Over the long term, this driver adds the largest positive swing to the global CAGR.

Electric passenger cars in urban duty show pad life stretching past 100,000 miles, slashing replacement events relative to internal-combustion models. Fleet calculations weigh the pricing of low-dust pads against fewer interventions, placing margin pressure on aftermarket channels. Hybrid SUVs with aggressive regen reclaim still demand robust pad friction for emergency stops, forcing costly dual-compound solutions. Municipal bus operators report a drop in total brake system cost of ownership once regenerative braking reaches recovery, delaying pad changeouts. Suppliers shift their revenue focus from volume to value-added coatings and analytics, but the restraint remains a noticeable drag on the CAGR of the friction material market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Brake pads captured 40.85% of the friction material market share in 2025 and continue to form the backbone of the global replacement business. The friction material market size tied to pads reflects high wear rates and standardized design templates that simplify cross-platform supply. Discs, however, post the quickest 5.59% CAGR as integrated electronic braking systems demand larger rotors with precise metallurgy, nudging average selling prices upward.

Pad upgrades center on copper-free organic blends that limit dust without compromising coefficient stability. Rotor demand gains a tailwind from premium SUVs specifying ventilated or carbon-ceramic discs, which reduce unsprung mass. Block and lining volumes remain steady in rail and heavy industry, although automation is extending block change intervals. Other niche components, such as clutch facings, leverage growth in robotics and industrial automation. Aggregate dynamics keep pads dominant, although discs accrue incremental revenue faster, thereby widening the strategic focus for global suppliers.

Semi-metallic recipes accounted for 37.95% of the friction material market size in 2025, thanks to proven cost-performance trade-offs. These blends combine steel or copper fibers with organic binders, providing a balance between fade resistance and noise control. Ceramic formulations trail but expand at 5.98% CAGR, propelled by Euro 7 dust caps and high-performance electric vehicle demand.

Brembo's Greentell laser-deposited rotor coating reduces PM10 and demonstrates the ceramic's potential to shift the economics of regulatory compliance. Sintered metals remain essential for rail and aircraft, but they account for a smaller slice. Aramid-rich pads capture a niche share in the aerospace and performance motorcycle markets due to their lightweight strength. Incremental research and development efforts focus on bio-based binders, aiming to reduce the carbon footprint without compromising durability.

The Global Friction Material Market Report is Segmented by Product Type (Discs, Pads, Blocks, Linings, and Other Types), Material (Ceramic, Asbestos, Semi-Metallic, and More), Application (Clutch and Brake Systems, Gear Tooth Systems, and Other Applications), End-User Industry (Automotive, Railway, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Units).

The Asia-Pacific region held a commanding 45.90% market share of the friction material market in 2025, thanks to its entrenched supply chains, cost-competitive labor, and soaring vehicle ownership across China, India, and ASEAN. Chinese rotor producers integrate foundries and machining shops within a single industrial park, slashing logistics costs and supporting global export competitiveness. India reported a revenue growth in H1 2024, as two-wheeler sales rebounded and aftermarket networks expanded. Japan contributed premium disc technology exports tied to performance vehicle programs and maintained leadership in electric-motorcycle braking kits.

North America and Europe together form a mature volume base governed by environmental leadership. Euro 7 and California's copper restrictions position these markets as test beds for low-dust discs and sensorized pads, knowledge that subsequently scales to the Asia-Pacific region. Production shifts eastward to Romania, Poland, and Mexico, keeping cost parity, while design and validation centers stay in Germany, Italy, and the United States.

The Middle East and Africa represent the fastest-growing regional CAGR at 4.66%, driven by construction booms, mineral extraction, and the demand for imported passenger vehicles, which require climate-resilient pads. Gulf Cooperation Council projects funnel capital into metro networks and light-rail, spurring block and lining demand. Sub-Saharan mining fleets utilize oversized wet-disc brakes, specifically designed for heavy-haul trucks. South America exhibits a tempered outlook as currency volatility restrains aftermarket spending, despite a gradual recovery in Brazilian auto output.