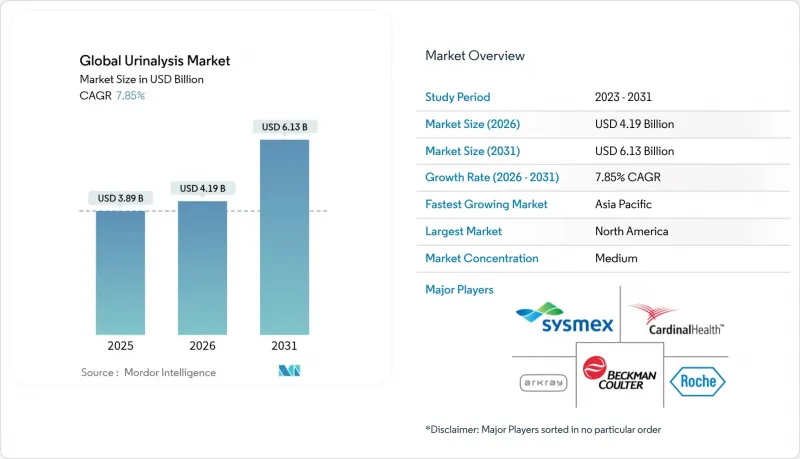

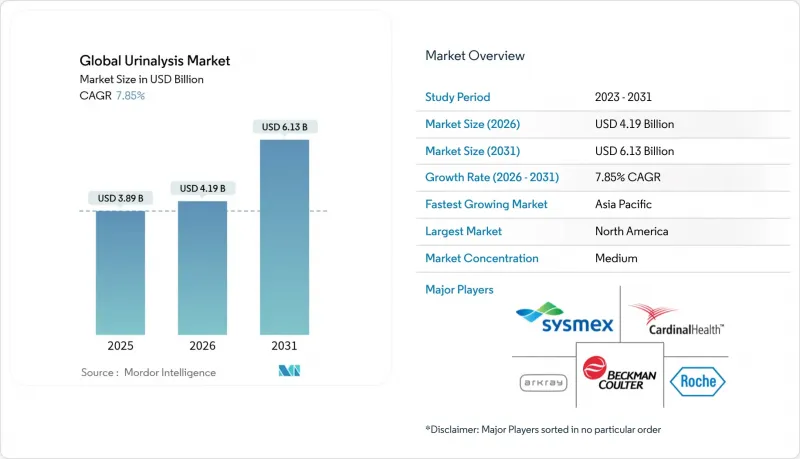

소변검사 시장은 2025년 38억 9,000만 달러에서 2026년에는 41억 9,000만 달러에 이르고, 2026-2031년 CAGR 7.85%로 성장을 지속하여 2031년까지 61억 3,000만 달러에 달할 것으로 예측됩니다.

만성 신장 질환 및 대사성 질환의 유병률 증가, POC(Point-of-Care) 검사 도입, AI를 활용한 자동화 등이 복합적으로 작용하여 수요를 견인하고 있습니다. 공급업체들은 중-고처리량 분석기에 의료용 사물인터넷(IoMT) 연결 기능을 추가하여 검사실과 임상의가 검사 데이터를 통합하고 임상적 판단을 신속하게 내릴 수 있도록 지원하고 있습니다. 재택 원격 진단 키트도 접근성 확대에 기여하고 있으며, 북미에서는 보험 상환의 안정성이 장치 도입의 기반이 되고 있습니다. 한편, 아시아태평양에서는 정부 주도의 진단 역량 확대와 가처분 소득 증가가 그 배경이 되고 있습니다.

만성콩팥병(CKD)과 당뇨병은 정기적인 검사에 대한 지속적인 수요를 주도하고 있으며, 신장 기능 모니터링 용도는 2030년까지 연평균 복합 성장률(CAGR) 10.24%로 증가할 것으로 예측됩니다. 2024년에는 약 5억 3,700만 명의 성인이 당뇨병을 앓고 있을 것으로 추정되며, 조기 신증을 감지하는 미량 알부민-크레아티닌 비율 검사의 필요성이 높아지고 있습니다. 호중구 젤라티나아제 관련 리포카린과 같은 첨단 바이오마커는 소변검사의 임상적 유용성을 확장하고, AI 기반 위험도 계층화 모델은 임상의가 치료를 개별화하고 재입원을 줄이는 데 도움이 됩니다. 미국의 의료 시스템은 CKD 관리에 연간 1,200억 달러 이상을 지출하고 있으며, 예방적 검진 예산을 강화하고 있습니다. 이러한 추세는 소모품의 지속적인 수익과 만성질환 치료 경로에 적합한 POC(Point-of-Care) 기기 도입을 촉진할 것입니다.

응급실과 응급 진료소에서는 환자 분류에 즉각적인 딥스틱 검사 및 카트리지 검사 결과를 점점 더 많이 활용하고 있으며, 대기 시간을 단축하고 처리 능력을 향상시키고 있습니다. 코로나19는 원격 의료를 촉진하고, 제조업체들은 전자 건강 기록에 안전한 데이터를 전송하는 휴대용 분석기로 대응했습니다. 지멘스 헬스인어스는 MULTISTIX 스트립에 광학 식별 밴드를 추가하여 품질 검사 자동화 및 수동 오류를 줄였습니다. 분산형 플랫폼이 중앙 검사실이 멀리 떨어져 있는 경우의 공백을 메워주기 때문에 지방의 의료 서비스 제공업체들이 가장 큰 혜택을 누리고 있습니다. 가치 기반 보상 체계는 의료 서비스 제공업체가 일상적인 선별 검사를 검사실 중심에서 병상 워크플로우로 전환하도록 동기를 부여하여 소변검사 시장을 두 자릿수 POC 성장으로 이끌고 있습니다.

2024년 FDA 실험실 개발 검사 규정은 단계적 시판 전 심사 및 품질 시스템 준수를 의무화하여 진단 기기 제조업체에 누적 35억 6,000만 달러의 추가 비용을 발생시킬 것으로 예측됩니다. 중국의 개정된 의료기기 규정과 인도의 판매법도 마찬가지로 모니터링을 강화하고 있으며, 기업들은 여러 관할권에 대한 신청과 감사에 예산을 책정해야 합니다. 2026년까지 ISO 13485와의 조화는 세계 정합성을 높이는 한편, 단기적으로 운영비용을 증가시킬 것입니다. 중소기업은 제품 출시가 늦어질 수 있고, 경쟁의 격렬함은 완화될 것이며, 소변검사 시장의 혁신 속도도 둔화될 것입니다.

2025년 기준 소모품은 소변검사 시장의 65.62%를 차지할 것으로 예상되며, 높은 판매량의 시약 스트립은 공급업체에 연금과 같은 수익을 가져다 줄 것입니다. 장비 카테고리는 규모는 작지만, 인력 부족 대책과 엄격해지는 품질 기준에 대응하기 위한 검사실 자동화로 인해 2031년까지 연평균 복합 성장률(CAGR) 8.76%를 나타낼 것으로 예측됩니다. 예를 들어 로슈의 cobas u 601은 시간당 240개의 검체를 처리할 수 있는데, 고객을 전용 스트립 기술에 묶어두어 소모품 수요를 분석기 도입에 연동시키는 '면도칼과 칼날'의 비즈니스 모델을 구현하고 있습니다. 초기 비용을 염려하는 많은 중규모 병원들은 완전한 설비투자 없이도 수작업에 의한 오류를 줄일 수 있는 반자동 장비를 선호하고 있습니다.

소모품은 각 환자 검체마다 새로운 스트립 컨트롤 컵이 필요하기 때문에 반복 주문이 발생하여 주기적인 장비 수요를 완화하고 공급업체의 수익 기반을 지속적으로 지원합니다. 소변검사 소모품 시장 규모는 당뇨병 선별검사와 요로감염증(UTI) 유병률 증가에 따라 확대될 것으로 예측됩니다. 반면, 장비 매출은 소규모 기준선에서 더 빠른 성장세를 보이고 있습니다. 분석기 성능을 원격으로 모니터링하는 IoMT(사물인터넷)를 포함한 종합적인 서비스 계약은 벤더와 고객 간의 관계를 강화하고 시장에서의 입지를 유지합니다.

생화학 검사는 2025년 전체 매출의 45.10%를 차지할 것으로 예상되며, 2031년까지 연평균 9.21%의 성장이 예상됩니다. 대사 및 신장 기능 평가에서 혈당, 단백질, 케톤 측정에 필수적이며, 검사마다 스트립을 재사용할 수 있습니다. 질량분석법에 기반한 단백질체학 확장 기술은 현재 수천 종의 소변 단백질을 검출할 수 있어 질병의 조기 징후 파악 및 개인별 맞춤 치료 모니터링이 가능합니다.

유세포 분석은 현재 소변검사 시장 규모에서 작은 분야이지만, 세포 계수 및 형태학적 분류의 자동화가 가능하기 때문에 가장 빠르게 성장하고 있는 방법입니다. 현미경 검사 병목현상에 직면한 검사실에서는 처리 능력 향상과 보고 표준화를 위해 플로우 시스템을 선택하고 있습니다. 또한, 스마트폰 기반의 비색 측정 리더는 생화학 검사의 편의성과 디지털 분석을 결합하여 자원이 제한된 환경에서의 접근성 확대를 실현하고 있습니다. 첨단 검사 플랫폼과 소비자 리더의 이중 추진으로 검사량이 증가하고 데이터 정밀도가 향상되고 있습니다.

소변검사 시장은 제품 유형별(기기(자동 분석기 등), 소모품(시약-키트 등)), 검사 유형별(생화학 검사, 침전물 검사 등, 기타), 용도별(질병 스크리닝, 신장 질환 모니터링, 기타), 최종 사용자별(병원, 임상 실험실, 기타), 기술별(딥스틱, 현미경, 기타), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류됩니다. 딥스틱, 현미경 검사, 기타), 지역(북미, 유럽, 아시아태평양, 기타)으로 분류됩니다.

북미는 2025년 매출의 38.85%를 차지하며, 종합적인 보험 적용(Medicare 2025 스케줄에 따른 검체 채취 비용 8.57달러 포함)의 혜택을 받고 있습니다. 병원에서는 응급실 혼잡 완화를 위해 POC 유닛을 도입하고 있으며, 캐나다의 단일 지불자 제도는 소모품 소비가 적고 비용 효율적인 분석기를 선호합니다. 멕시코에서는 중산층 증가와 공공 부문의 진단검사 지출이 기초검사 수요를 증가시키고 있으며, 특히 도시 주변 지역의 진료소에서 기초검사 수요가 증가하고 있습니다. HIPAA, 2024년 사이버 보안 현대화법 등 데이터 프라이버시 법안은 분석 장비의 안전한 연결성을 강조하고 있으며, 강력한 암호화 기능을 갖춘 주요 브랜드에 대한 조달을 촉진하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 2031년까지 연평균 복합 성장률(CAGR) 10.72%를 나타낼 것으로 예측됩니다. 중국은 현립병원의 업그레이드부터 20위안의 수수료로 소변을 현지에서 분석하는 스마트 공중화장실과 같은 혁신적인 개념에 이르기까지 대규모 진단 현대화에 자금을 투입하고 모니터링 범위를 확장하고 있습니다. 일본에서는 노인들이 만성질환 관리를 위해 재택검진에 의존하고, 인도에서는 '메이크 인 인디아' 정책으로 현지 조립을 촉진하여 소유비용을 낮추었습니다. 동남아시아는 아세안 조화에 따른 승인 효율화를 배경으로 다국적 공급업체들이 지역 서비스 거점을 설치.

유럽에서는 고령화에 따른 만성질환 검진 수요 증가로 꾸준한 시장 확대가 지속되고 있습니다. CE 마킹의 통일과 EUDAMED 데이터베이스의 구축으로 신규 분석기기 시장 진입이 용이해졌습니다. 독일과 영국에서는 공립병원에서 AI 지원 침전물 영상진단을 시범 운영하기 시작했고, 프랑스에서는 원격진료 규정에 따라 재택 검사 키트에 대한 보험 적용이 이루어지고 있습니다. 중동에서는 석유 수입을 투자하여 고처리량 장비를 갖춘 3차 의료 센터를 정비하고 있습니다. 남아공은 규제 측면의 투명성으로 인해 사하라 이남 지역의 유통 거점 역할을 하고 있습니다. 남미에서는 브라질이 주도하는 민관협력 진단 파트너십이 도시 외 지역으로의 소변검사 접근성 확대를 추진하면서 완만한 성장이 예상됩니다.

The urinalysis market is expected to grow from USD 3.89 billion in 2025 to USD 4.19 billion in 2026 and is forecast to reach USD 6.13 billion by 2031 at 7.85% CAGR over 2026-2031.

Rising chronic kidney and metabolic disease prevalence, point-of-care (POC) adoption, and AI-enabled automation collectively propel demand. Suppliers are layering Internet-of-Medical-Things (IoMT) connectivity onto mid- and high-throughput analyzers, allowing laboratories and clinicians to consolidate test data and speed clinical decisions. Home-based tele-diagnostic kits are also broadening access, while North American reimbursement stability underpins steady instrument placements. Asia-Pacific, meanwhile, benefits from government-funded diagnostic capacity expansion and growing disposable incomes.

Chronic kidney disease (CKD) and diabetes drive sustained demand for routine testing, with kidney monitoring applications rising at a 10.24% CAGR to 2030. An estimated 537 million adults lived with diabetes in 2024, heightening the need for microalbumin and creatinine ratio checks that detect early nephropathy.Advanced biomarkers such as neutrophil gelatinase-associated lipocalin broaden the clinical utility of urinalysis, while AI-based risk-stratification models help clinicians tailor therapy and reduce hospital readmissions. Health systems spend more than USD 120 billion annually on CKD management in the United States, reinforcing preventive screening budgets. These patterns strengthen both recurrent consumable revenue and adoption of POC devices that fit chronic-care pathways.

Emergency departments and urgent-care clinics increasingly rely on immediate dipstick or cartridge results to triage patients, shortening wait times and improving throughput. COVID-19 catalyzed telemedicine, and manufacturers responded with portable analyzers that transmit secure data to electronic health records. Siemens Healthineers added optical identification bands to its MULTISTIX strips, automating quality checks and reducing manual errors. Rural providers benefit most, as decentralized platforms fill gaps where central labs are distant. Value-based reimbursement further motivates providers to convert routine screens from laboratory-centric to bedside workflows, lifting the urinalysis market toward double-digit POC growth.

The 2024 FDA Laboratory Developed Tests rule mandates staged pre-market review and quality-system compliance, adding up to USD 3.56 billion in cumulative costs for diagnostics producers.China's updated Medical Device Regulation and India's marketing code similarly tighten oversight, compelling companies to budget for multi-jurisdiction submissions and audits. Harmonization with ISO 13485 by 2026 will improve global alignment yet raises near-term operating expense. Smaller firms may delay launches, trimming competitive intensity but also slowing innovation cadence within the urinalysis market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Consumables held 65.62% of the urinalysis market in 2025, anchored by high-volume reagent strip sales that create annuity-like revenue for suppliers. The instruments category, although smaller, is set for a 8.76% CAGR to 2031 as laboratories automate to counter workforce shortages and to align with stricter quality mandates. Roche's cobas u 601, for instance, processes 240 samples an hour while locking customers into proprietary strip technology, illustrating the razor-and-blade dynamic that tethers consumable pull-through to analyzer placements. Several mid-tier hospitals, deterred by upfront costs, favor semi-automated units that still reduce manual error without full capital investment.

Consumables continue to underpin supplier profitability because each patient sample requires new strips, controls, and cups, generating repeat orders that buffer cyclical instrument demand. The urinalysis market size for consumables is forecast to expand in line with rising diabetes screens and UTI prevalence, whereas instrument revenue grows faster from a smaller baseline. Bundled service agreements, including remote IoMT monitoring of analyzer performance, cement vendor-client relationships and sustain market visibility.

Biochemical assays accounted for 45.10% of total revenue in 2025 and are projected to climb 9.21% annually through 2031. They remain indispensable for glucose, protein, and ketone measurement in metabolic and renal assessments, ensuring recurrent strip usage per encounter. Mass-spectrometry-based proteomic extensions now detect thousands of urinary proteins, promising earlier disease signatures and personalized therapeutic monitoring.

Flow cytometry, although representing a smaller slice of the urinalysis market size today, is the fastest-growing modality due to its ability to automate cell counting and morphological classification. Laboratories facing microscopy bottlenecks choose flow systems to raise throughput and standardize reporting. Moreover, smartphone-based colorimetric readers fuse biochemical simplicity with digital analytics, broadening access in resource-constrained settings. The dual push from advanced lab platforms and consumer-grade readers multiplies test volumes and enriches data granularity.

The Urinalysis Market is Segmented by Product Type (Instruments [Automated Analyzer, and More], Consumables [Reagents & Kits, and More]), by Test Type (Biochemical, Sediment, and More), by Application (Disease Screening, Kidney Disease Monitoring, and More), by End User (Hospitals, Clinical Laboratories, and More), by Technology (Dipstick, Microscopy, and More), by Geography (North America, Europe, Asia-Pacific, and More).

North America held 38.85% of 2025 revenue and benefits from comprehensive insurance coverage, including a USD 8.57 specimen collection fee under Medicare's 2025 schedule. Hospitals deploy POC units in emergency departments to alleviate crowding, while Canada's single-payer framework favors cost-effective analyzers with low consumable burn rates. Mexico's middle-income growth and public-sector spending on diagnostics lift baseline test demand, particularly in peri-urban clinics. Data-privacy legislation such as HIPAA and the 2024 Cybersecurity Modernization Act emphasize secure analyzer connectivity, influencing procurement toward major brands with robust encryption.

Asia-Pacific is the fastest-growing region, posting an 10.72% CAGR to 2031. China funds large-scale diagnostic modernization, from county hospital upgrades to innovative concepts such as smart public toilets that analyze urine on site for a 20-yuan fee, expanding surveillance reach. Japan's senior population relies on home testing to manage chronic illnesses, while India's Make-in-India program stimulates local analyzer assembly that lowers cost of ownership. Southeast Asia leverages ASEAN harmonization to streamline approvals, prompting multinational suppliers to set up regional service hubs.

Europe maintains steady expansion as aging demographics raise chronic disease screening volumes. CE-marking alignment and EUDAMED database rollout simplify market entry for new analyzers. Germany and the United Kingdom pilot AI-assisted sediment imaging in public hospitals, while France reimburses home test kits under tele-consult rules. The Middle East invests oil revenues in tertiary-care centers stocked with high-throughput instruments, and South Africa anchors sub-Saharan distribution due to its relative regulatory clarity. South America offers moderate growth, led by Brazil's public-private diagnostic partnerships that extend urinalysis access beyond urban cores.