동물 표준 실험실 시장 : 서비스별, 용도별, 동물 유형별, 최종 사용자별, 지역별, 예측(-2030년)

Veterinary Reference Laboratory Market by Service (Microbiology, Immunodiagnostics, Molecular Diagnostics, PCR, ELISA, Hematology, Urinalysis), Animal (Companion, Livestock), Application (Clinical Pathology, Toxicology), Region - Global Forecast to 2030

상품코드:1881286

리서치사:MarketsandMarkets

발행일:2025년 11월

페이지 정보:영문 606 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

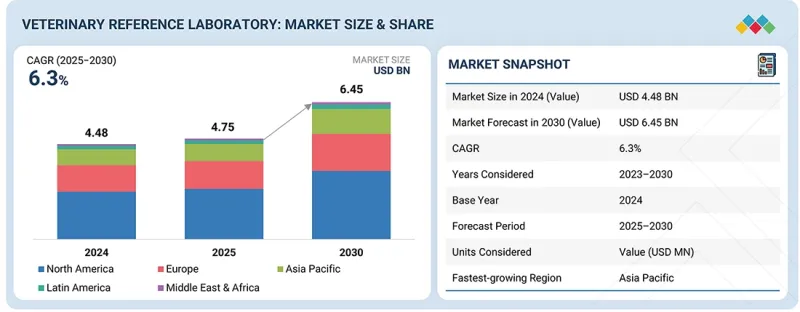

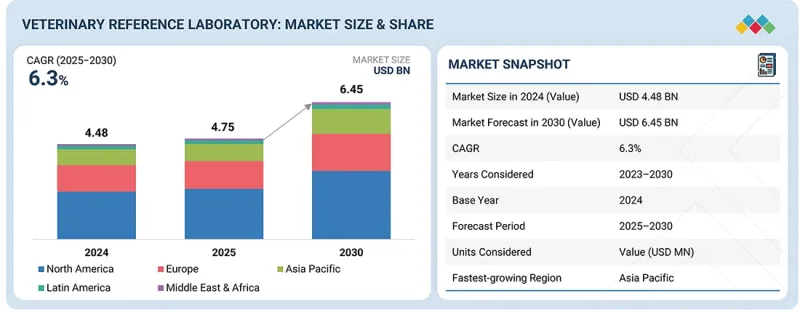

동물 표준 실험실 시장 규모는 2025년 475만 달러, 2030년까지 646만 달러에 이르고, CAGR은 6.3%를 보일 것으로 예측됩니다.

인수 공통 감염과 만성 동물 질환 증가, 동반 동물의 사육률의 상승, 예방 의료에 대한 중시 증가가 주로 시장 확대를 견인하고 있습니다.

조사 범위

조사 기간

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

대상 단위

금액(10억 달러)

부문

서비스별, 용도별, 동물 유형별, 최종 사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

분자진단, 면역진단, 임상화학검사 등 고도의 진단검사에 대한 수요가 높아짐에 따라 선진국 및 신흥지역 모두에서 높은 처리량 기준검사기관의 설립이 가속화되고 있습니다. 또한 자동화, AI 기반 영상 분석, 분자 검사의 기술적 진보로 검사 결과의 신속한 제공과 진단 정밀도의 향상이 가능해짐에 따라 수의사와 반려동물 소유자 간의 신뢰 관계가 더욱 깊어지고 있습니다.

동시에 진단 서비스와 디지털 플랫폼과 실험실 정보 관리 시스템(LIMS)의 통합이 진행됨에 따라 워크플로우의 효율화, 시료의 추적성 향상, 검사 결과에 대한 원격 액세스가 가능해지고 있습니다. 질병의 조기 발견과 동반 동물의 건강 관리 프로그램에 대한 관심 증가가 검사 도입을 더욱 뒷받침하는 한편, 수의학의 기업화나 진료소와 기준 검사 기관과의 제휴 확대가, 안정된 검체 유입을 촉진하고 있습니다. 그러나 시장은 높은 운영 비용과 검사 비용, 숙련된 검사 기사 부족, 수의 진단을 규제하는 엄격한 기준 등 과제에 직면하고 있습니다. 게다가 다양한 지역에서의 품질보증 유지, 바이오 보안 대책 및 시료 운송의 과제에 대한 대응은 정확성, 신뢰성, 성장의 지속을 목표로 하는 검사기관에 있어서 중요한 우선사항이 되고 있습니다.

용도별로 볼 때 동물 표준 실험실 시장은 임상 병리학, 세균학, 바이러스학, 기생충학 및 기타 용도로 분류됩니다. 2024년에는 임상병리학이 시장에서 가장 큰 점유율을 차지했습니다. 이 이점은 혈액학, 세포학 및 임상 화학 검사를 통해 상세한 진단 지식을 제공하는 동일한 부문의 중요한 역할에 기인합니다. 이러한 분석을 통해 수의사는 전신 질환의 정확한 진단, 치료 경과 추적, 복잡한 병리학의 효과적인 관리가 가능합니다. 반려동물 증가와 수의사 진료의 빈도 상승이 일상적인 병리 검사 서비스 수요를 뒷받침하고 있습니다. 또한, 자동 분석기와 디지털 병리 시스템의 기술 진보로 진단 정확도, 효율성, 결과 보고까지의 시간이 크게 개선되어 이 분야 시장 성장을 더욱 촉진하고 있습니다.

최종 사용자별로, 동물 표준 실험실 시장은 동물 병원 및 진료소, 연구 기관·대학, 포인트 오브 케어/원내 검사실, 기타 최종 사용자로 분류됩니다. 2024년 기준에서 수의사 클리닉 병원 부문은 세계 시장에서 가장 큰 점유율을 차지했습니다. 이 우위성은 주로 진단 정밀도와 효율 향상을 위해 분자진단, 면역 진단, 임상 화학 검사 등의 고도이고 전문적인 검사를 외부 위탁하는 클리닉이 증가하고, 집중형 검사 기관과의 제휴에 의한 진단 검사량이 증가하고 있는 것에 기인합니다.

반려동물 증가, 반려동물 의료비의 확대, 소규모·대규모 동물 병원 네트워크의 확충도, 진료소·병원으로부터의 검체 유입 증가에 기여하고 있습니다. 이러한 시설에서는 원내에서는 효율적으로 실시할 수 없는 확정 진단이나 복잡한 검사를 참고 검사 기관에 의존하는 것으로, 치료 성과와 업무 흐름의 개선을 도모하고 있습니다. 또한, 진료소와 참고검사기관 간의 디지털 검체 관리 시스템과 자동 결과 보고 시스템의 통합으로 검사 결과의 반환 시간이 단축되어 근거 기반의 수의학이 지원됩니다.

동물 표준 실험실 시장은 북미, 유럽, 아시아태평양, 중동 및 아프리카로 구분됩니다. 2024년 현재 북미는 세계 시장에서 가장 큰 점유율을 차지했습니다. 이러한 이점은 반려동물 사육률의 높이, 예방수의료에 대한 강한 의식, 지역 전체에서 반려동물을 위한 의료비 지출의 많음 등 몇 가지 주요 요인에 기인하고 있습니다. IDEXX Laboratories, Zoetis Services LLC, Mars, Incorporated와 같은 주요 기업의 존재 외에도 확립 된 동물 병원 및 진단센터 네트워크가이 지역의 주도적 지위를 더욱 강화하고 있습니다. 북미 내에서 미국은 가장 큰 시장 점유율을 차지합니다. 이는 일본의 첨단 수의학 인프라, 전문 및 분자진단 검사에 대한 수요 증가, 자동화 및 디지털 병리 솔루션의 급속한 도입을 지원합니다. 또한 미국 시장은 반려동물 보험의 보급률이 높고 수의학 서비스 제공업체의 견고한 생태계, 반려동물 및 가축 진단 기술 혁신을위한 연구 개발에 적극적인 투자 등의 이점을 누리고 있습니다.

본 보고서에서는 세계의 동물 표준 실험실 시장에 대해 조사했으며, 서비스별, 용도별, 동물 유형별, 최종 사용자별, 지역별 동향, 시장 진출기업프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

시장 역학

업계 동향

기술 분석

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

규제 분석

특허 분석

가격 분석

상환 분석

반려동물 보호자 행동

2025년-2026년의 주된 회의와 이벤트

최종 사용자의 시점과 충족되지 않은 요구

AI/GEN AI가 동물 표준 실험실 시장에 미치는 영향

에코시스템 맵

생태계에서의 역할

밸류체인 분석

투자 및 자금조달 시나리오

사례 연구 분석

고객의 비즈니스에 영향을 미치는 동향/혼란

2025년 미국 관세가 동물 표준 실험실 시장에 미치는 영향

제6장 동물 표준 실험실 시장(서비스별)

소개

임상 화학

면역진단

분자진단

혈액학

소변 검사

조직병리학 및 세포학

미생물학

기타

제7장 동물 표준 실험실 시장(용도별)

소개

임상병리학

세균학

바이러스학

기생충학

생산성 테스트

임신 검사

독성시험

기타

제8장 동물 표준 실험실 시장(동물 유형별)

소개

반려동물

가축

제9장 동물 표준 실험실 시장(최종사용자별)

소개

동물병원 및 클리닉

포인트 오브 케어/사내 검사

수의학 조사 기관 및 대학

기타

제10장 동물 표준 실험실 시장(지역별)

소개

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시 경제 전망

독일

영국

프랑스

이탈리아

스페인

네덜란드

기타

아시아태평양

아시아태평양의 거시 경제 전망

중국

일본

인도

호주

한국

태국

뉴질랜드

기타

라틴아메리카

라틴아메리카의 거시 경제 전망

브라질

멕시코

아르헨티나

기타

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

GCC 국가

기타

제11장 경쟁 구도

소개

주요 진입기업의 전략/강점

수익 분석, 2020년-2024년

시장 점유율 분석, 2024년

기업평가 매트릭스: 주요 진입기업, 2024년

기업평가 매트릭스: 스타트업/중소기업, 2024년

브랜드/제품 비교

주요 기업의 연구 개발비

기업평가와 재무지표

경쟁 시나리오

제12장 기업 프로파일

주요 진출기업

IDEXX LABORATORIES, INC.

MARS, INCORPORATED

ZOETIS SERVICES LLC

GD(ROYAL GD ANIMAL HEALTH)

LABOKLIN GMBH & CO. KG

CVS(UK) LIMITED

NATIONAL VETERINARY SERVICES LABORATORY USDA-APHIS

ANIMAL AND PLANT HEALTH AGENCY

ICAR-NIVEDI(NATIONAL INSTITUTE OF VETERINARY EPIDEMIOLOGY AND DISEASE INFORMATICS)

NATIONAL VETERINARY SERVICES

TEXAS A&M VETERINARY MEDICAL DIAGNOSTIC LABORATORY(TVMDL)

ANIMAL HEALTH DIAGNOSTIC CENTER, CORNELL UNIVERSITY

COLORADO STATE UNIVERSITY(VETERINARY DIAGNOSTIC LABORATORY)

BIOBEST LABORATORIES LTD.

PRIVATE VETERINARY CLINIC SAN MARCO SRL UNIPERSONALE

기타 기업

ROYAL VETERINARY COLLEGE, UNIVERSITY OF LONDON

UNIVERSITY OF GUELPH, ANIMAL HEALTH LABORATORY

VAXXINOVA

MIRA VISTA LABS

ELLIE DIAGNOSTICS

PROTATEK INTERNATIONAL, INC.

THE PIRBRIGHT INSTITUTE

CVR LABORATORY(CVRL)

VETERINARY PATHOLOGY GROUP

FRIEDRICH-LOEFFLER-INSTITUT(FLI)

제13장 부록

SHW

영문 목차

영문목차

The veterinary reference laboratory market is forecasted to grow from USD 4.75 million in 2025 to USD 6.46 million by 2030, recording a CAGR of 6.3%. The increasing prevalence of zoonotic and chronic animal diseases, rising companion animal ownership, and the growing emphasis on preventive healthcare primarily drive market expansion.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

By Service, Application, Animal type, End User, Region

Regions covered

North America, Europe, APAC, RoW

The rising demand for advanced diagnostic testing, including molecular diagnostics, immunodiagnostics, and clinical chemistry, has accelerated the establishment of high-throughput reference laboratories in both developed and emerging regions. Moreover, technological advancements in automation, AI-based image analysis, and molecular testing are enabling faster turnaround times and improved diagnostic accuracy, fostering greater trust among veterinarians and pet owners.

At the same time, the increasing integration of diagnostic services with digital platforms and laboratory information management systems (LIMS) is streamlining workflows, enhancing sample traceability, and enabling remote access to test results. The rising focus on early disease detection and companion animal wellness programs further supports test adoption, while expanding veterinary corporatization and partnerships between clinics and reference labs are driving consistent sample inflows. However, the market faces challenges such as high operational and testing costs, a shortage of skilled laboratory professionals, and stringent regulatory standards governing veterinary diagnostics. Additionally, maintaining quality assurance across diverse geographies and addressing biosecurity and sample transport challenges remain key priorities for laboratories aiming to sustain accuracy, reliability, and growth momentum.

The clinical pathology segment accounted for the largest share of the market, by application, in 2024.

Based on application, the veterinary reference laboratory market is segmented into clinical pathology, bacteriology, virology, parasitology, and other applications. In 2024, clinical pathology accounted for the largest share of the market. This dominance is attributed to the segment's critical role in delivering detailed diagnostic insights through hematology, cytology, and clinical chemistry testing. These analyses enable veterinarians to accurately diagnose systemic disorders, track therapeutic progress, and effectively manage complex disease conditions. The rising companion animal population and increasing frequency of veterinary consultations have fueled the demand for routine pathology services. Moreover, technological advancements in automated analyzers and digital pathology systems have significantly improved diagnostic precision, efficiency, and turnaround time, further driving market growth in this segment.

The veterinary clinics & hospitals segment is expected to dominate the market, by end user, during the forecast period.

Based on end user, the veterinary reference laboratory market is segmented into veterinary clinics and hospitals, research institutes and universities, point-of-care/in-house labs, and other end users. In 2024, veterinary clinics and hospitals accounted for the largest share of the global market. This dominance is primarily driven by the rising volume of diagnostic testing conducted through referral partnerships with centralized laboratories, as clinics increasingly outsource advanced and specialized tests such as molecular diagnostics, immunodiagnostics, and clinical chemistry to improve diagnostic accuracy and efficiency.

The growing companion animal population, higher pet healthcare expenditure, and expanding network of small and large veterinary practices have further contributed to the rising sample inflow from clinics and hospitals. These facilities rely on reference laboratories for confirmatory and complex testing that cannot be efficiently performed in-house, thereby enhancing treatment outcomes and operational workflows. Additionally, the integration of digital sample management systems and automated result reporting between clinics and reference labs is improving turnaround times and supporting evidence-based veterinary care.

In 2024, North America dominated the veterinary reference laboratory market.

The veterinary reference laboratory market is segmented into North America, Europe, Asia Pacific, and the Middle East & Africa. In 2024, North America accounted for the largest share of the global market. This dominance can be attributed to several key factors, including the high prevalence of companion animal ownership, strong awareness of preventive veterinary care, and significant healthcare expenditure on pets across the region. The presence of leading industry players such as IDEXX Laboratories, Zoetis Services LLC, and Mars, Incorporated, coupled with a well-established network of veterinary hospitals and diagnostic centers, has further reinforced the region's leadership. Within North America, the United States held the largest market share, supported by the country's advanced veterinary infrastructure, growing demand for specialized and molecular diagnostic testing, and rapid adoption of automation and digital pathology solutions. Additionally, the U.S. market benefits from favorable pet insurance penetration, a robust ecosystem of veterinary service providers, and strong investment in R&D for companion and livestock diagnostic innovations.

Breakdown of supply-side primary interviews:

By Company Type: Tier 1 (45%), Tier 2 (20%), and Tier 3 (35%)

By Designation: C-level Executives (35%), Directors (25%), and Other Designations (40%)

By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

By Company Type: Veterinary Clinics & Hospitals (70%), POC/In-house labs (15%), Research Institutions and Universities (10%), and Other End Users (5%)

By Designation: Veterinary Healthcare Professionals (35%), Department Heads (27%), Procurement Heads (22%), and Other Designations (16%)

By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and Middle East & Africa (5%)

Research Coverage

This report studies the veterinary reference laboratory market based on service, application, animal type, end user, and region. It also studies factors affecting market growth (drivers, restraints, opportunities, and challenges). It analyzes the market's opportunities and challenges and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micromarkets with respect to their individual growth trends and forecasts the revenue of the market segments with respect to six main regions and respective countries.

Reasons to Buy the Report

The report can help established companies and new or smaller firms understand market trends, which will help them capture a larger market share. Firms that purchase the report can utilize one or more of the five strategies mentioned below.

This report provides insights into the following points:

Analysis of key drivers, opportunities, restraints, and challenges influencing the growth of the veterinary reference laboratory market.

Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and service launches in the veterinary reference laboratory market

Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of veterinary reference laboratory services across regions.

Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the veterinary reference laboratory market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the veterinary reference laboratory market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION

1.3.2 REGIONAL SCOPE

1.3.3 INCLUSIONS & EXCLUSIONS

1.3.4 YEARS CONSIDERED

1.4 MARKET STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.2 RESEARCH METHODOLOGY DESIGN

2.2.1 SECONDARY DATA

2.2.1.1 Key sources of secondary research

2.2.1.2 Key objectives of secondary research

2.2.1.3 Key data from secondary sources

2.2.2 PRIMARY DATA

2.2.2.1 Key primary sources

2.2.2.2 Key objectives of primary research

2.2.2.3 Key data from primary sources

2.2.2.4 Key industry insights

2.3 MARKET SIZE ESTIMATION

2.3.1 REVENUE SHARE ANALYSIS

2.3.2 COMPANY PRESENTATIONS AND PRIMARY INTERVIEWS