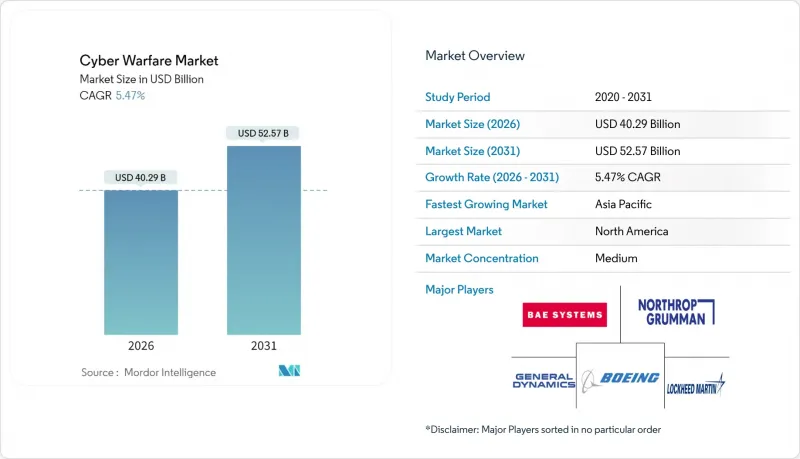

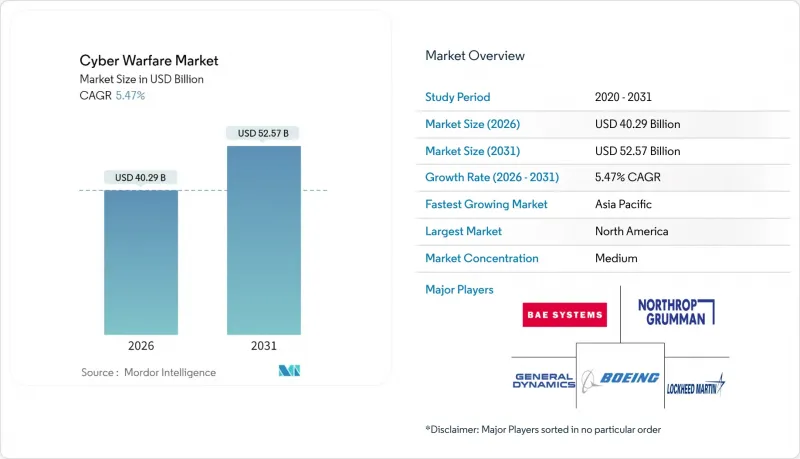

사이버 전쟁 시장은 2025년에 382억 달러로 평가되었으며, 2026년 402억 9,000만 달러에서 2031년까지 525억 7,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 5.47%로 예상됩니다.

국가 주체의 공격 강화, 군 C4ISR 네트워크의 급속한 디지털화, 자율적 도구의 보급으로 사이버 공간의 전략적 가치는 지속적으로 증가하고 있으며, 각국 국방부는 이 영역의 보호와 전력투입을 추진하고 있습니다. 북미는 기술적 우위를 유지하는 한편, 핵심 인프라에 대한 공격이 강화되고 있으며, 아시아태평양은 지역적 긴장이 고조되면서 조달 주기가 빨라져 가장 빠르게 성장하는 시장으로 부상하고 있습니다. 과거 주변 영역이었던 의료 분야에서는 병원 그룹이 군사적 수준의 방어책을 채택할 수밖에 없는 고도화된 랜섬웨어가 위협이 되고 있습니다. 한편, 방산 대기업과 사이버 보안 전문 기업 간의 인수 주도형 통합은 인공지능과 자율 대응 엔진을 융합한 통합 공방 솔루션으로의 전환을 시사하고 있습니다.

사이버 작전은 간헐적인 첩보 활동에서 지속적인 '지속적 관여'로 전환하고 있으며, 군대는 공격적인 사냥팀과 강력한 방어 태세에 투자해야 합니다. 미국 사이버사령부의 2024년 선제공격 작전은 억지력이 적대자 네트워크 내 사전 배치에 의존하게 되었음을 분명히 했습니다. 중국의 전략지원부대도 비슷한 접근 방식을 채택하고 있으며, 이에 대응하는 역내 국가들은 악성코드 개발, 제로데이 공격 비축, 속임수 도구의 예산 확대를 추진하고 있습니다. 공격의 귀속이 불분명하기 때문에 부정 가능한 공격이 가능하고, 에스컬레이션의 위험이 높아져 사이버 전쟁 시장 전체에 대한 수요가 지속되고 있습니다. 위협 인텔리전스와 자동 대응 기능을 패키지로 제공하는 벤더들이 인기를 끌고 있습니다. 이는 정부가 기밀성을 유지하면서 의사결정 주기를 단축해야 한다는 압력에 직면해 있기 때문입니다.

동맹군은 센서, 사격장치, 의사결정 노드를 상호연결하는 통합 전 영역 지휘 프레임워크로 전환하고 있습니다. 디지털화는 작전상 민첩성을 가져오는 한편, 적대자가 제로데이 액세스를 노리는 공격 대상 영역을 확대합니다. AI 지원 계획 도구는 현재 미션 크리티컬한 네트워크에 존재하며, 분석적 이점과 함께 새로운 취약점을 만들어내고 있습니다. 그 결과, 조달 프로그램은 엔드포인트 탐지, 제로 트러스트 아키텍처, 크로스 도메인 게이트웨이를 통합하여 데이터 흐름을 보호하고 있습니다. 강화된 통신 시스템에 대한 지속적인 자금 투입은 다국적 임무 부대 간의 상호 운용성을 인증할 수 있는 사이버 전쟁 시장 벤더에게 장기적인 성장을 약속합니다.

최고 기밀 취급 승인을 받은 오퍼레이터 직책의 공석이 2024년에 급증하여 심사 대기 기간이 18개월까지 늘어났습니다. 지휘관은 인력 확보에 프로그램 예산을 할당하기 때문에 신규 도구 조달 예산이 압박을 받고 있습니다. 사이버 학습과 AI 기반 교육을 통해 실무를 통한 학습을 가속화하고 기술 격차를 부분적으로 해소할 수 있게 되었습니다. 그러나 기밀취급허가 심사 지연으로 인해 전력 생산 과정이 지연되고 있습니다. 이러한 제약으로 인해 각 기관이 새로운 공격 플랫폼을 운영할 수 있는 속도가 제한되어 사이버 전쟁 시장의 장기적인 성장이 억제될 것으로 예상됩니다.

국방 및 항공우주 분야는 2025년 기준 사이버 전쟁 시장 점유율의 32.08%를 차지할 것으로 예상되며, 공격적 익스플로잇과 다층 방어가 결합된 기밀 예산이 주도하고 있습니다. 의료 분야는 절대 금액은 작지만, 랜섬웨어 조직이 의료의 긴급성을 악용하여 지불을 강요하기 때문에 6.83%의 가장 빠른 CAGR을 기록했습니다. BFSI(은행, 금융, 보험) 분야의 사이버 전쟁 시장 규모는 안정적입니다. 규제 당국이 다층적인 보안 조치를 의무화하는 한편, 국가 차원의 위협 행위자가 공급망 침입으로 전환하는 가운데 기업 부문은 군사적 수준의 솔루션으로 전환하고 있기 때문입니다. 유틸리티 및 에너지 사업자는 조달을 산업안전 규제와 연계하고, IT와 OT의 보안을 통합 플랫폼을 중심으로 융합하고 있습니다. 국방을 제외한 정부 민간 기관은 유권자 데이터와 공공 서비스 포털을 보호하기 위해 위협 사냥 계약을 추진하고 있습니다. 항만 폐쇄와 같은 주목할 만한 사건으로 인해 운송 기업들도 조달 목록에 이름을 올렸고, 엔드포인트 격리 및 암호화 텔레메트리에 대한 수요가 증가하고 있습니다. 산업 간 융합이 진행됨에 따라 벤더들은 제품군의 모듈화를 추진하고 있으며, 기업 IT에서 미션 크리티컬 시스템까지 코드 기반의 분기 없이도 원활하게 확장 가능한 툴을 구현하고 있습니다. 이러한 범용성으로 인해 기존에는 민간용 사이버 보안 툴을 구매하던 고객층에서도 사이버 전쟁 시장의 확대를 촉진하고 있습니다.

성장의 역동성은 산업별 규제와 보험 조항에 의해 영향을 받고 있으며, 군사 사이버 전략을 참조하는 경향이 강해지고 있습니다. 주요 방산업체들은 수년간의 관계를 활용하여 분석 기능의 확장을 민간 산업으로 업셀링하여 수익원을 확장하고 있습니다. 의료 컨소시엄은 정보 공유 동맹을 형성하고, 위협 인텔리전스를 국방 연구소에 피드백하여 패치 적용 주기를 단축하고 있습니다. 은행은 국가 전략을 탐지하는 국방 유래 텔레메트리 피드를 구독하여 상황 인식 능력을 향상시키고 있습니다. 이러한 크로스오버는 한 분야의 데이터가 다른 분야의 보안 성과를 강화하는 사이버 전쟁 산업 생태계를 강화하고, 여러 부문의 확장을 지속시키는 긍정적인 네트워크 효과를 창출하고 있습니다.

2025년 기준 북미는 사이버 전쟁 시장의 31.18%를 차지하며 미국이 주도하고 있습니다. 이 나라의 국방비 지출은 공격적 침투 부대와 대규모 사이버 훈련장 모두를 재정적으로 뒷받침하고 있습니다. 파이브아이즈 정보 네트워크는 캐나다, 영국, 호주, 뉴질랜드가 상호 운용 가능한 솔루션을 조달하고 원격 측정 데이터를 실시간으로 공유하면서 플랫폼에 대한 수요가 증가하고 있기 때문입니다. 미국의 선제공격 전략은 엔드포인트 텔레메트리, 기만 그리드, 지속적 관여 사이클을 지원하는 미션 특화형 익스플로잇 체인에 대한 지출을 정착시키고 있습니다. 캐나다는 중요 광물 공급망 보호를 위해 조달을 확대하고, 멕시코는 국경을 넘는 무역 통로를 보호하기 위해 선택적으로 투자하고 있습니다.

아시아태평양은 2031년까지 CAGR 6.98%로 성장할 것으로 예상되며, 남중국해의 전략적 갈등과 대만 주변에서 강화되는 사이버 정찰 활동을 반영합니다. 중국 전략지원부대가 지역 투자를 촉진합니다. 일본, 사이버 부대 인원 두 배로 증원, 한국, AI 대응 방어망에 자금 투입, 호주, 미 인도태평양군과의 합동 레드팀 훈련 조정. 인도는 '디지털 바랏 샤크티(Digital Bharat Shakti)' 정책에 따라 국산 플랫폼을 육성하여 수입 의존도를 낮추고 지역 벤더 생태계를 육성하고 있습니다. 싱가포르, 베트남 등 동남아시아 국가들은 디지털 무역 확대에 따른 위협 환경 변화에 따라 SOC(보안운영센터) 현대화를 우선 과제로 삼고 있습니다.

유럽에서는 NATO의 교리가 조달을 통일하고, EU 사이버 연대법이 공동 방위 프로젝트의 자금 조달을 효율화하면서 꾸준히 확대되고 있습니다. 독일과 프랑스는 자율 공격 플랫폼에 신규 자금을 할당하고, 북유럽의 전력회사들은 전력망 교란 대책으로 내한성 방어 시스템을 조달하고 있습니다. 러시아의 하이브리드 전술을 경계하는 동유럽 국가들은 국경 방어 계획에 기동형 사고 대응 부대를 통합하고 있습니다. 중동 국가들은 에너지 수입을 사이버 무기고에 투입하여 지역 분쟁에서 비대칭적 우위를 점하고 있습니다. 아프리카와 남미 군대는 해저 케이블과 위성 노드를 보호하는 시범 프로젝트를 시작하고 있으며, 세계 사이버 전쟁 시장 규모를 확대할 수 있는 새로운 기회를 창출하고 있습니다.

The cyber warfare market was valued at USD 38.2 billion in 2025 and estimated to grow from USD 40.29 billion in 2026 to reach USD 52.57 billion by 2031, at a CAGR of 5.47% during the forecast period (2026-2031).

Escalating nation-state offensives, the rapid digitalization of military C4ISR networks, and the diffusion of autonomous tools continue to raise the strategic value of cyberspace, prompting defense ministries to protect and project power in this domain. North America retains technological primacy, yet faces intensified attacks on critical infrastructure, while the Asia-Pacific becomes the fastest-growing arena as regional tensions accelerate procurement cycles. Healthcare, once peripheral, now attracts high-grade ransomware that compels hospital groups to adopt military-grade defenses. Meanwhile, acquisition-driven consolidation among defense primes and cybersecurity specialists signals a shift toward integrated offensive-defensive suites that fuse artificial intelligence with autonomous response engines

Cyber operations have shifted from episodic espionage to continuous "persistent engagement," forcing militaries to invest in offensive hunt teams and resilient defensive postures. The U.S. Cyber Command's 2024 forward-hunt missions clarified that deterrence now hinges on pre-positioning inside adversary networks. China's Strategic Support Force mirrors this approach, prompting regional counter-moves that expand budget lines for malware engineering, zero-day stockpiles, and deception tooling. Attribution ambiguity enables deniable aggression, heightens the risk of escalation, and sustains demand across the cyber warfare market. Vendors that package threat intelligence with automated response gain favor because governments are under pressure to shorten decision cycles without compromising secrecy.

Allied forces are migrating to joint all-domain command frameworks that interlink sensors, shooters, and decision nodes. While digitization delivers operational agility, it also enlarges the attack surface that adversaries probe for zero-day access. AI-assisted planning tools now reside within mission-critical networks, creating new vulnerabilities alongside analytics advantages. Consequently, acquisition programs bundle endpoint detection, zero-trust architecture, and cross-domain gateways to secure data flows. Continued funding for hardened communications promises long-tail growth for cyber warfare market vendors that can certify interoperability across multinational task forces.

Vacancies for top-secret cleared operators surged in 2024, and vetting wait times stretched to 18 months. Commanders allocate program budgets to talent retention, squeezing procurement for new tools. Cyber ranges and AI-based tutoring partially offset the skills gap by accelerating on-the-job learning, but clearance backlogs slow the force-generation pipeline. This restraint caps how fast agencies can operationalize new offensive platforms, tempering the cyber warfare market's longer-term growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Defense and aerospace contributed 32.08% of the cyber warfare market share in 2025, driven by classified budgets that combine offensive exploits with layered defenses. Healthcare, though smaller in absolute spend, records the fastest 6.83% CAGR as ransomware syndicates exploit medical urgency to force payments.The cyber warfare market size captured by BFSI remains steady because regulators compel multilayered safeguards, while corporate sectors move toward military-grade solutions as nation-state threat actors pivot to supply-chain infiltration. Utilities and energy operators tie procurement to industrial safety mandates, blending IT and OT security in ways that favor integrated platforms. Government civilian agencies outside defense pursue threat-hunting contracts to secure voter data and public-service portals. Transportation firms now rank in procurement queues after headline-grabbing port shutdowns, driving demand for endpoint isolation and encrypted telemetry. Cross-industry convergence prompts vendors to modularize their offerings, enabling tools to extend seamlessly from enterprise IT to mission-critical systems without requiring codebase forks. This versatility helps expand the cyber warfare market within customer segments that historically purchased consumer-grade cybersecurity tools.

Growth dynamics are influenced by sector-specific regulations and insurance clauses that increasingly reference military cyber doctrines. Defense primes leverage long-standing relationships to upsell analytics extensions into civilian industries, thereby compounding revenue streams. Healthcare consortia form information-sharing alliances that funnel threat intelligence back to defense labs, accelerating patch cycles. Banks valorize situational awareness by subscribing to defense-derived telemetry feeds that flag nation-state strategies. Such a crossover reinforces the cyber warfare industry's ecosystem, where data from one vertical enriches security outcomes in another, creating positive network effects that sustain multi-segment expansion.

The Cyber Warfare Market Report is Segmented by End-User Industry (Defense and Aerospace, BFSI, Corporate, Power and Utilities, Government, Healthcare, and More), Deployment Mode (On-Premises, Cloud-Based, and More), Solution Type (Offensive Platforms and Exploits, Defensive Platforms, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America controlled 31.18% of the cyber warfare market in 2025, led by the United States' defense outlays that fund both offensive penetration units and large-scale cyber ranges. The Five Eyes intelligence network amplifies platform demand because Canada, the United Kingdom, Australia, and New Zealand procure interoperable solutions that share telemetry in real time. U.S. forward-hunt doctrines entrench spending on endpoint telemetry, deception grids, and mission-specific exploit chains that feed continuous engagement cycles. Canada increases procurement to safeguard critical mineral supply chains, while Mexico invests selectively to shield cross-border trade corridors.

Asia-Pacific is projected to grow at a 6.98% CAGR through 2031, reflecting strategic rivalry in the South China Sea and escalating cyber probes surrounding Taiwan. China's Strategic Support Force catalyzes regional investments; Japan doubles the headcount of its cyber unit, South Korea funds AI-enabled defensive lattices, and Australia coordinates joint red-team exercises with the U.S. Indo-Pacific Command. India's indigenous platforms gain traction under "Digital Bharat Shakti," reducing import dependency and fostering regional vendor ecosystems. Southeast Asian states, including Singapore and Vietnam, prioritize SOC modernization as digital trade expands their threat landscape.

Europe shows steady expansion as NATO doctrine synchronizes procurement, and the EU Cyber Solidarity Act streamlines funding for joint defensive projects.Germany and France allocate new funds for autonomous hunt platforms, while Nordic utilities procure winter-resilient defenses against grid sabotage. Eastern European states, wary of Russian hybrid tactics, are integrating mobile incident-response units into their border defense plans. Middle Eastern countries channel energy revenues into cyber arsenals that deliver asymmetric leverage in regional conflicts. African and South American militaries are beginning pilot projects to guard undersea cables and satellite nodes, creating nascent opportunities that will expand the global cyber warfare market size.