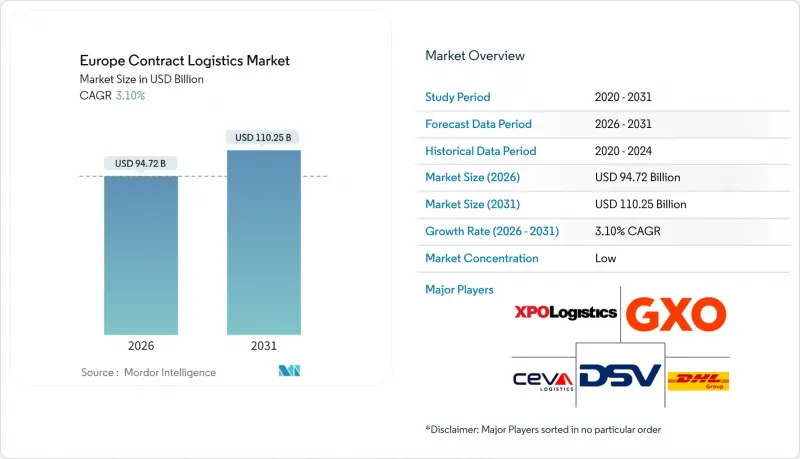

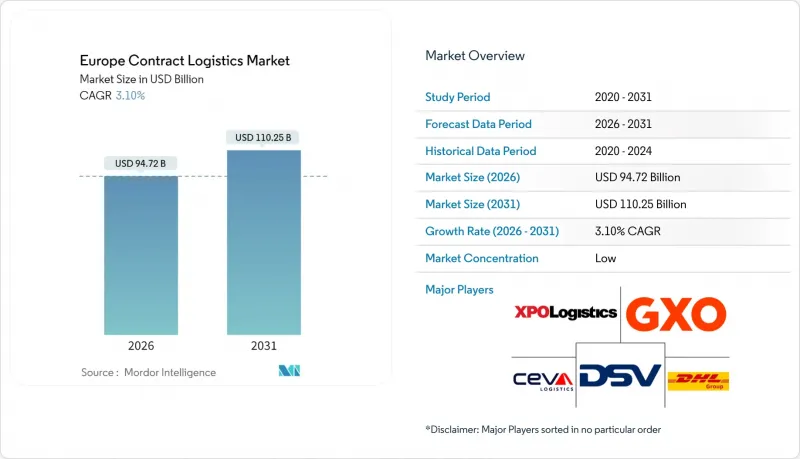

유럽의 계약 물류 시장 규모는 2026년에 947억 2,000만 달러로 추정되며, 2025년 918억 7,000만 달러에서 성장하며, 2031년에는 1,102억 5,000만 달러에 달할 것으로 예측됩니다. 2026-2031년에는 CAGR 3.10%로 성장이 전망됩니다.

성숙한 시장 환경은 EC 풀필먼트, 공급망 탄력성 강화, AI를 활용한 최적화가 기존 운영 모델을 변화시키면서 부가가치 솔루션으로 꾸준히 이동하고 있습니다. 동유럽으로의 니어쇼어링은 무역 통로를 재구성하고 있으며, EU의 'Fit for 55' 패키지에 기반한 지속가능성 목표는 저탄소 운송 자산과 녹색 창고에 대한 투자를 촉진하고 있습니다. DSV의 DB쉥커 대형 인수로 대표되는 통합의 가속화는 노동력 부족, 부동산 가격 상승, 규제 복잡화에 대응하기 위해 사업자들이 규모의 경제를 추구하고 있음을 보여줍니다. 로봇 기술, 엔드-투-엔드 가시성 플랫폼, 유연한 창고 배치를 통합한 사업자는 유럽 계약 물류 시장의 다음 아웃소싱 수요를 포착할 수 있는 최적의 위치에 있습니다.

소매업체들이 고정된 부동산 비용을 유연한 창고 계약으로 대체하는 자산 경량화 모델로 전환하는 가운데, 3자 물류(3PL) 업체들은 증가하는 E-Commerce 수요를 포착하고 있습니다. 초대형 물류센터 수요 증가로 공급이 부족해지면서 유통업체들은 장기 임대를 통해 일상적인 업무를 3PL에 위탁하는 경향이 강해지고 있습니다. 각 공급업체들은 유럽 계약물류 시장 전체에서 당일 배송 목표를 달성하기 위해 옴니채널 분류, 로봇 피킹, 운송업체에 의존하지 않는 라스트마일 네트워크에 대한 투자를 진행하고 있습니다. 패션 및 신발 업계의 높은 반품률은 역물류의 복잡성을 증가시키고 있으며, 통합 반품 처리는 새로운 계약의 표준 기능으로 자리 잡고 있습니다. 풀필먼트와 반품 처리를 하나의 기술 기반으로 통합하는 선구적인 기업은 고객 유지율을 높이고 프리미엄 가격 책정을 실현하고 있습니다.

팬데믹으로 인해 회복탄력성은 비용 중심에서 이사회 차원의 우선순위로 재정의되었고, 유럽 전역에서 이중 소싱, 지역적 완충, 공급업체 다변화를 촉진했습니다. 해상, 육상, 철도, 항공의 운송 이벤트를 단일 대시보드에 통합하는 멀티모달 시각화 시스템은 유럽 계약 물류 시장에서 계약 입찰시 핵심적인 선정 기준이 되고 있습니다. 고객은 여러 재고 거점을 조정하고 혼란시 화물의 경로를 동적으로 변경할 수 있는 3PL을 선호합니다. 2024-2025년까지 컨트롤타워 아키텍처에 투자한 공급업체들은 운송업체들이 비상 대응 매뉴얼을 입증할 수 있는 데이터가 풍부한 파트너를 찾고 있는 가운데, 수주율 증가를 보고하고 있습니다. 가시성의 중요성은 ESG 보고에도 적용되며, 실시간 탄소 추적이 서비스 수준 계약에 명시되는 경우가 증가하고 있습니다.

유럽에서는 전문 트럭 운전사 부족이 심각해지고 있으며, 국제도로운송연맹(IRU)은 2026년까지 200만 명 이상의 부족이 발생할 수 있다고 경고하고 있습니다. 창고 노동자의 이직률은 고령 노동자의 퇴직이 신규 채용보다 빠른 속도로 가속화되고 있습니다. 사업자들은 입사금, 유연근무제, 사내 교육 아카데미 등에 대응하고 있지만, 임금 상승이 유럽 계약물류 시장의 이익률을 압박하고 있습니다. 자동화를 통해 일부 압력은 완화되지만, 선행 투자 및 변경 관리 주기로 인해 회수 기간은 길어질 수 있습니다. 인력 전략을 현대화하지 않는 한, 서비스 중단이나 용량 조정으로 인해 고객 만족도가 떨어질 위험이 있습니다.

2025년 유럽 계약 물류 시장 점유율의 60.35%를 운송 서비스가 차지했습니다. 이는 도로, 철도, 항공, 해상 운송이 대륙간 무역을 지원하고 있기 때문입니다. 그러나 화주들이 순수한 운송 속도보다 재고 배치를 우선시하는 경향으로 인해 창고 및 유통 부문은 2031년까지 연평균 복합 성장률(CAGR) 3.92%로 가장 빠르게 성장할 것으로 예측됩니다. 유럽 계약 물류 시장에서 운송 부문의 규모는 여전히 견고하지만, 가치는 화물 운송, 보관, 경제조 업무를 통합한 패키지 서비스로 이동하고 있습니다. 철도화물 운송은 2024년 0.7% 감소, EU가 점유율을 두 배로 늘리려는 가운데 운송수단의 제약이 부각되고 있습니다. 도어 투 도어 운송은 여전히 도로 운송이 주류를 이루고 있지만, 운송 회사 네트워크에는 동적 경로 설정을 위한 디지털 화물 플랫폼이 내장되어 있습니다. 항공화물 운송은 고가품 및 시간 엄수품에 특화된 틈새 시장을 유지하고, 단거리 해상운송은 지중해와 발트해의 관문을 다중 모드 운송망로 연결하고 있습니다.

창고 및 유통 분야에서도 비슷한 추세를 볼 수 있습니다. 인구 밀집 지역 인근의 초대형 허브 수요는 토지 부족 및 엄격한 구역 규제와 충돌하여 우량 부동산의 임대료를 상승시키고 있습니다. 사업자는 고층 자동화, 메자닌형 로봇 도입, 다크스토어 구성으로 비용을 절감하고 평당 처리 능력을 3배로 높였습니다. 콜드체인의 확장은 의약품과 신선식품을 지원하며 진입의 기술적 장벽을 더욱 높이고 있습니다. 그 결과, 계약서에는 팔레트 이동량을 넘어 피킹 정확도, 역물류 사이클, 마이크로 풀필먼트 처리 속도 등 다양한 성과지표가 명시되어 있습니다. 유럽의 계약 물류 시장은 부동산에 대한 지식과 첨단 프로세스 엔지니어링을 융합할 수 있는 기업에게 보상을 주는 구조로 되어 있습니다.

The Europe Contract Logistics Market size in 2026 is estimated at USD 94.72 billion, growing from 2025 value of USD 91.87 billion with 2031 projections showing USD 110.25 billion, growing at 3.10% CAGR over 2026-2031.

The mature landscape is steadily pivoting toward value-added solutions as e-commerce fulfillment, supply-chain resilience, and AI-enabled optimization transform traditional operating models. Nearshoring into Eastern Europe is redrawing trade corridors, while sustainability targets under the EU Fit for 55 package amplify investment in low-carbon transport assets and green warehousing. Intensifying consolidation-exemplified by DSV's recent mega-acquisition of DB Schenker-shows providers chasing economies of scale to blunt labor shortages, real-estate inflation, and regulatory complexity. Providers that embed robotics, end-to-end visibility platforms, and flexible warehousing footprints are best placed to capture the next wave of outsourced demand across the Europe contract logistics market.

Third-party logistics (3PL) operators are capturing rising e-commerce volumes as retailers shift toward asset-light models that trade fixed real-estate costs for flexible warehousing contracts. Demand for XXL distribution centers has tightened availability, prompting retailers to secure long leases while outsourcing day-to-day operations to 3PLs. Providers are investing in omnichannel sortation, robotic picking, and carrier-agnostic last-mile networks to achieve same-day delivery targets across the Europe contract logistics market. High return rates in fashion and footwear elevate reverse-logistics complexity, making integrated returns processing a standard feature of new contracts. Early movers that bundle fulfillment and returns under one technology stack enhance customer stickiness and unlock premium pricing.

The pandemic reframed resilience from a cost center to a board-level priority, driving dual-sourcing, regional buffers, and supplier diversification across Europe. Multimodal visibility systems that consolidate ocean, road, rail, and air events into a single dashboard are now core selection criteria when tendering for Europe contract logistics market contracts. Customers prioritize 3PLs capable of orchestrating parallel inventory locations and dynamically rerouting freight during disruption. Providers that invested in control-tower architectures in 2024-2025 report win-rate uplifts as shippers seek data-rich partners able to evidence contingency playbooks. The visibility imperative extends to ESG reporting, with real-time carbon tracking increasingly written into service-level agreements.

Europe faces a looming shortfall of professional truck drivers, with the International Road Transport Union warning that vacancies could top 2 million by 2026. Warehouse attrition has accelerated as aging workforces retire faster than recruits enter the sector. Operators respond through signing bonuses, flexible schedules, and in-house training academies, but wage inflation squeezes margins in the Europe contract logistics market. Automation offsets some pressure, yet up-front capex and change-management cycles lengthen payback periods. Service disruptions and capacity rationing risk eroding customer satisfaction unless workforce strategies are modernized.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Transportation services captured 60.35% of the Europe contract logistics market share in 2025 as road, rail, air, and sea movements underpin continental trade. Yet Warehousing & Distribution is growing fastest at 3.92% CAGR to 2031 as shippers prioritize inventory positioning over pure transit speed. The Europe contract logistics market size allocated to Transportation remains healthy, but value is shifting toward integrated bundles that combine freight, storage, and light manufacturing tasks. Rail freight slipped 0.7% in 2024, underscoring modal constraints despite EU ambitions to double its share. Road continues to dominate door-to-door flows, although carrier networks now embed digital freight platforms for dynamic routing. Air freight retains a niche, serving high-value or time-critical goods, while short-sea lanes link Mediterranean and Baltic gateways into wider multimodal offerings.

A parallel narrative unfolds in Warehousing & Distribution. Demand for XXL hubs near population centers collides with scarce land and stricter zoning, inflating prime rents. Operators mitigate costs by adopting high-bay automation, mezzanine robotics, and dark-store configurations that triple throughput per square meter. Cold-chain extensions support pharmaceuticals and fresh food, deepening technical barriers to entry. Consequently, contracts now stipulate performance metrics beyond pallet moves, tracking pick accuracy, reverse-logistics cycles, and micro-fulfillment turnaround. The Europe contract logistics market thus rewards firms able to marry real-estate acumen with advanced process engineering.

The Europe Contract Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Distribution, and Value-Added Services), Contract Duration (1-3 Years and Above 3 Years), End-User Industry (Manufacturing & Automotive, Retail & E-Commerce, Healthcare & Pharmaceuticals, and More), Country (Germany, United Kingdom, France, Italy, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).