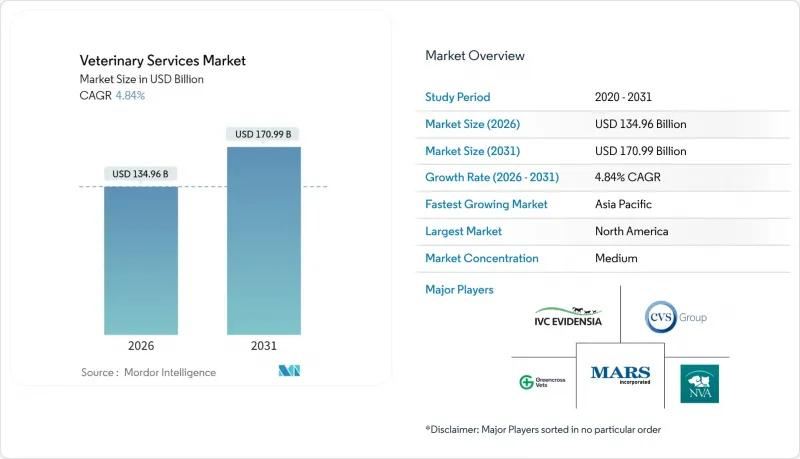

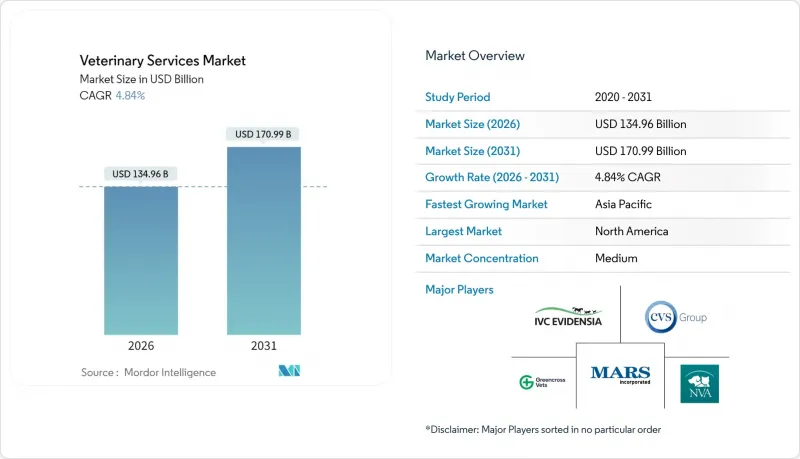

수의 서비스 시장은 2025년에 1,287억 3,000만 달러로 평가되며, 2026년 1,349억 6,000만 달러에서 2031년까지 1,709억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 4.84%로 예상됩니다.

반려동물 소유자의 건전한 지출, 기술의 급속한 보급, 지속적인 기업 인수로 인해 수의학 서비스 시장은 확대 추세를 유지하고 있습니다. 예방 의료는 가정이 일시적인 치료에서 지속적인 치료로 전환함에 따라 수요가 증가하고 있으며, 인공지능은 진단 처리 능력을 향상시켜 바쁜 임상의를 돕고 있습니다. 사모펀드와 전략적 투자자들은 규모의 경제, 데이터 자산, 인재 풀을 확보하기 위해 롤업 활동을 가속화하고 있습니다. 컴패니언 케어 이외의 분야에서도 수요가 확대되고 있습니다. 인수공통전염병 감시, 가축 생산성 향상 의무, 원헬스 정책 프레임워크가 수의사 서비스 시장의 매출 기반을 확대하고 있습니다.

미국내 반려동물 보유 가구 수는 2011년 5,600만 가구에서 2025년 9,400만 가구에 달할 것으로 예상되며, Z세대가 신규 반려동물 소유자 중 가장 빠르게 증가하고 있습니다. 이 세대는 기존에는 인간 의료에 국한되었던 종양학, 심장병학, 행동치료에 대한 기대를 가지고 있습니다. 부유층 고객들은 게놈 검사, 영양 상담, 전문의와의 24시간 365일 원격 접속을 결합한 컨시어지 플랜을 구매하고 있습니다. 이러한 프리미엄화는 수의사 서비스 시장 전체의 현금 흐름에 대한 가시성을 높이는 동시에 장비 업그레이드와 전문의 교육을 정당화할 수 있는 근거가 됩니다.

2024년 H5N1 인플루엔자 발생으로 미국에서 800마리 이상의 젖소가 감염되었고, 동물과의 접촉으로 인해 확인된 인체 감염 사례는 66건에 달했습니다. 반려동물의 수명이 길어지면서 만성질환이 증가하고 있으며, 2024년에는 반려견의 73%, 반려묘의 64%가 치과 질환으로 진단받을 것으로 예측됩니다. 이러한 이중의 압력은 수의학 서비스 시장의 검사, 영상 진단, 바이오 보안 관련 지출을 지속적으로 지원하고 있습니다.

예측에 따르면 2032년까지 수의사는 70,092명이 부족할 것으로 예상되지만, 졸업생은 52,926명에 불과합니다. 이 부족은 평균 40만 달러에 달하는 학자금 대출 부채로 인해 더욱 심각해지고 있습니다. 번아웃율이 40%를 넘어섰고, 자살 위험도 높아져 수의업계의 진료체계에 압박을 가하고 있습니다. 특히 지방의 영향이 심각해 2025년에는 미국 243개 카운티가 수의사 부족 지역으로 지정되어 있습니다.

예방 및 헬스케어 서비스는 2025년 매출의 31.02%를 차지하며 수의학 서비스 시장의 기반이 될 것입니다. 정기적인 건강관리 플랜과 연례 건강검진은 안정적인 이익률을 창출하고, 약품 자동 보충 서비스는 고객 유지율을 높이고 있습니다. 텔레헬스 분야 시장 규모는 2026년 3억 9,298만 달러에서 2031년 5억 4,000만 달러에 달하고, CAGR 6.45%로 확대될 것으로 예측됩니다. AI 강화형 영상 진단은 처리 능력을 향상시켜 급증시 대응력을 지원합니다. 최소침습수술 기술로 인한 회복기간 단축으로 수술 수요는 안정화되는 추세입니다. 치과 치료는 건당 평균 170-350달러로 수익성이 높으며, 반려견의 73%가 일생 동안 최소 한 번 이상 치료를 받아야 합니다.

진단검사실은 진료소와의 교차판매 효과를 누리고, 전자처방전 플랫폼은 약품 컴플라이언스를 효율화합니다. 응급 및 중환자실은 인력 부족에 직면하고 있으며, 기업 그룹이 원격 ICU 대시보드를 통해 협력하는 24시간 대응 거점을 개설하는 움직임이 가속화되고 있습니다. 반려동물의 고령화에 따라 재활치료, 침술, 수처리법 등이 보급되면서 반려동물 서비스 시장의 평생 지출이 확대되고 있습니다.

2025년에는 반려동물이 매출의 62.68%를 차지할 것으로 예상되며, 2031년까지 연평균 6.63%로 가장 높은 성장률을 보일 것으로 전망됩니다. 개가 가장 큰 하위 부문으로 남아 있으며, 종양학 및 심장병학 서비스는 인간 의료 프로토콜을 반영하고 있습니다. 밀레니얼 세대와 Z세대 사이에서 도시내 고양이 사육이 증가하면서 고양이 전문 클리닉에 대한 수요가 증가하고 있습니다. 말 의료는 틈새 시장이지만, 파행 진단과 스포츠 부상 재활치료에서 높은 평균 거래액을 유지하고 있습니다.

H5N1형 조류 인플루엔자(H5N1)의 젖소 집단 발병으로 공중보건 리스크가 부각되면서 생산동물에 대한 서비스 통합에 대한 수요가 증가하고 있습니다. 축산 경영자는 실시간 모니터링과 백신 준수 감사를 도입하고, 양돈 및 양계업자는 종합적인 바이오 보안 패키지를 확대합니다. 양식업자들은 전문적인 헬스케어 계획을 요구하고 있으며, 모두 수의사 서비스 시장의 폭을 넓히고 있습니다. 소비자의 단백질 공급원이 다양해지면서 소형 반추동물에 대한 관심이 높아져 고객층이 더욱 확대되고 있습니다.

북미는 2025년 기준 전 세계 매출의 42.01%를 차지했습니다. 성숙한 보험 보급률, 탄탄한 E-Commerce 약국 채널, 원헬스 정책 통합이 보험료 가격의 탄력성을 지원하고 있습니다. 다국적 체인은 미국 도시권에 집중되어 있으며, 캐나다 사업자들도 비슷한 통합 경향을 보이고 있으며, 공중보건 지침에 맞추어 서비스를 제공합니다. 멕시코에서는 중산층 확대가 반려동물 사료의 두 자릿수 성장을 촉진하고 있으며, 다운스트림 서비스 기회의 조짐을 보이고 있습니다.

유럽에서는 꾸준한 보급이 이루어지고 있습니다. 영국 왕립수의사회는 인증제도를 효율화하여 국경을 초월한 임상의의 이동을 촉진하고 있습니다. 독일과 프랑스는 동물과 인간의 역학 데이터를 연계하는 모니터링 플랫폼에 투자하고 있습니다. EQT의 VetPartners 인수는 회원국 전체에서 진료소 플랫폼 확장을 위한 자본 유입을 시사하고 있습니다. 원격의료와 처방 데이터 상호운용성에 대한 규제 조화는 수의학 서비스 시장 전체에서 진료 그룹이 업무상 시너지를 창출할 수 있도록 돕고 있습니다.

아시아태평양은 5.57%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. 중국의 반려동물 의료비는 2024년 1조 6,200억 위안에 달할 것으로 예상되며, 시장 분산에도 불구하고 계속 증가할 것으로 전망됨. 인도 반려동물 사료 시장은 15.37%의 연평균 복합 성장률(CAGR)로 성장하며 영양 상담, 피부과 진료 등 부수적인 서비스를 견인. 일본의 고령화가 진행 중인 반려견은 노년기 의료 수요를 불러일으키고, 한국은 소동물 영상 진단용 AI 알고리즘 개발을 주도하고 있습니다. 호주의 진료소 통합은 규제 준수도가 높은 시장에 진출하고자 하는 유럽 바이어들을 끌어들이고 있습니다. 이러한 추세와 맞물려 이 지역의 수의학 서비스 시장 규모가 확대되고 있습니다.

The veterinary services market was valued at USD 128.73 billion in 2025 and estimated to grow from USD 134.96 billion in 2026 to reach USD 170.99 billion by 2031, at a CAGR of 4.84% during the forecast period (2026-2031).

Healthy pet-owner spending, rapid technology adoption, and sustained corporate buy-outs keep the veterinary services market on an expansion path. Preventive medicine captures demand as households shift from episodic to continuous care, while artificial intelligence raises diagnostic throughput and supports busy clinicians. Private-equity and strategic buyers accelerate roll-up activity to secure scale economies, data assets, and talent pools. Demand also grows outside companion care: zoonotic-disease surveillance, livestock productivity mandates, and One-Health policy frameworks widen the revenue base of the veterinary services market.

Pet ownership reached 94 million U.S. households in 2025, up from 56 million in 2011, and Generation Z now represents the fastest-growing cohort of new owners. This demographic expects oncology, cardiology, and behavioural therapies once reserved for human medicine. High-net-worth clients also purchase concierge plans that bundle genomic screening, nutrition counselling, and 24/7 tele-access to specialists. Such premiumisation strengthens cash-flow visibility across the veterinary services market while justifying equipment upgrades and specialist training.

The 2024 H5N1 influenza episode affected more than 800 U.S. dairy herds, with 66 confirmed human infections traced to animal exposure. Companion pets live longer, which increases chronic conditions: 73% of dogs and 64% of cats were diagnosed with dental disease in 2024. These dual pressures support sustained laboratory, imaging, and bio-security spending within the veterinary services market.

Forecasts show a deficit of 70,092 veterinarians by 2032 versus only 52,926 graduates, a shortfall aggravated by student debt that averages USD 400,000. Burnout exceeds 40%, and suicide risk remains elevated, pressuring clinic rosters in the veterinary services industry. Rural zones suffer most, with 243 U.S. counties classified as shortage areas in 2025.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Preventive and wellness care captured 31.02% of 2025 revenue, anchoring the veterinary services market. Subscription wellness plans and annual health screens generate predictable margins, while pharmacy auto-refills deepen client stickiness. The veterinary services market size for tele-health is set to climb from USD 392.98 million in 2026 to USD 0.54 billion by 2031, a 6.45% CAGR. AI-enhanced imaging lifts throughput and supports surge capacity. Surgical demand stabilises as minimally-invasive techniques cut recovery time. Dental procedures remain lucrative, averaging USD 170-350 per case, and 73% of dogs need at least one intervention during their lifetime.

Diagnostic laboratories enjoy cross-selling with clinics, and e-prescribing platforms streamline drug compliance. Emergency and critical-care centres face labour constraints, prompting corporate groups to open 24-hour hubs linked by tele-ICU dashboards. Rehabilitation, acupuncture, and hydro-therapy gain traction as pets age, extending lifetime spending in the veterinary services market.

Companion animals constituted 62.68% of revenue in 2025 and will post the fastest 6.63% CAGR through 2031. Dogs continue as the largest sub-segment, with oncology and cardiology services mirroring human care protocols. Urban cat ownership rises among millennials and Generation Z, pushing demand for feline-only clinics. Equine medicine remains niche but commands high average transaction values for lameness diagnostics and sports-injury rehabilitation.

Production animals demand service integration after the H5N1 dairy-herd outbreak highlighted public-health risks. Cattle operators now purchase real-time monitoring and vaccine-compliance audits. Swine and poultry producers expand comprehensive bio-security packages, and aquaculture ventures request specialised health plans, both adding breadth to the veterinary services market. Small ruminants gain attention as consumers diversify protein sources, further widening the client base.

The Veterinary Services Market Report is Segmented by Service (Surgery, Diagnostic Imaging & Laboratory, and More), Animal Type (Companion Animals and Production/Farm Animals), Provider Ownership Structure (Independent Practices, and More), Delivery Mode (Mobile / On-Farm, and More), Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 42.01% of global revenue in 2025. Mature insurance penetration, robust e-commerce pharmacy channels, and One-Health policy integration sustain premium-price elasticity. Multinational chains cluster around U.S. urban centres, and Canadian operators observe similar consolidation but tailor offerings to public-health mandates. Mexico's rising middle class fuels double-digit pet-food growth, a signal of downstream service opportunity.

Europe shows steady uptake. The United Kingdom's Royal College of Veterinary Surgeons streamlines accreditation, facilitating cross-border clinician mobility. Germany and France invest in surveillance platforms that link animal and human epidemiological data. EQT's acquisition of VetPartners indicates capital inflows aiming at clinic platform scaling across member states. Regulatory harmonisation for tele-medicine and prescription data interoperability aids clinic groups in capturing operational synergies across the veterinary services market.

Asia-Pacific is the fastest-expanding zone at 5.57% CAGR. China's pet-medical spend hit 1,062 billion yuan in 2024 and keeps rising despite fragmentation. India's pet-food market is growing at 15.37% CAGR and pulls ancillary services such as dietetic consults and dermatology. Japan's super-aging dogs spur demand for geriatric care, while South Korea pioneers AI algorithms for small-animal imaging. Australia's clinic roll-ups attract European buyers hunting for exposure to a high-compliance market. Collectively, these dynamics enlarge the veterinary services market size for the region.