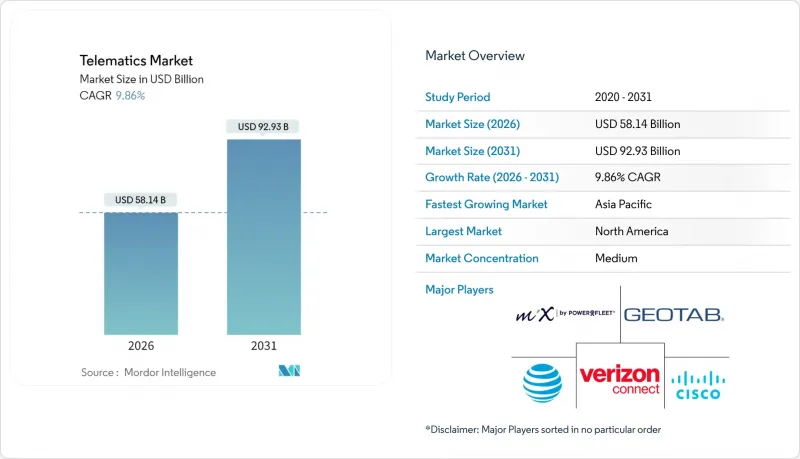

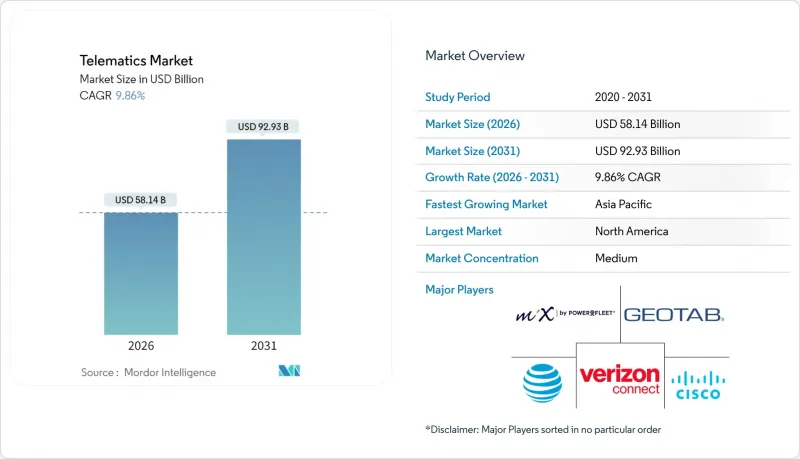

텔레매틱스 시장은 2025년에 529억 3,000만 달러로 평가되며, 2026년 581억 4,000만 달러에서 2031년까지 929억 3,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 9.86%로 예상됩니다.

특히 유럽의 eCall과 인도의 AIS 140과 같은 규제 요건은 자동차 제조업체와 차량 사업자에게 공장 수준의 커넥티비티 구축을 의무화하고 있으며, 이는 OEM 수요를 가속화하고 있습니다. 차량 1대당 반도체 탑재량은 2030년까지 두 배로 증가할 것으로 예상되며, 하드웨어 비용은 증가하지만 고급 분석을 지원하는 풍부한 데이터 스트림을 실현할 수 있습니다. 실시간 주행 데이터를 활용한 사용량 기반 보험 프로그램은 북미와 유럽에서 빠르게 확대되고 있으며, 커넥티드카의 비즈니스 사례를 강화하고 있습니다. 5G와 엣지 컴퓨팅의 급속한 보급으로 텔레매틱스는 단순한 추적에서 예측 유지보수 및 V2X(차량 간 통신)로 변모하고 있습니다. UNECE WP.29 및 ISO/SAE 21434에 따른 사이버 보안 대응 비용의 상승은 중소 벤더들에게 압박을 가하고 있지만, 자금력이 있는 기업에게는 경쟁 우위를 가져다주고 있습니다.

자동차 제조업체들은 2025년부터 적용되는 EU 데이터법 등 새로운 데이터 공유 규정에 대응하기 위해 텔레매틱스를 차량 전자장치에 직접 통합하고 있습니다. 이 법은 제조업체가 차량 데이터를 제3자 서비스 프로바이더에 공개할 것을 의무화하고 있습니다. 지오탭의 볼보자동차와의 제휴를 통해 지오탭의 OEM 통합은 157개 브랜드 이상으로 확대되어 임베디드 커넥티비티가 빠르게 확산되고 있음을 증명하고 있습니다. 애널리스트들의 추정에 따르면 커넥티드 서비스는 차량 1대당 1,600달러의 매출을 창출할 수 있으며, 이는 자동차 제조업체들이 데이터를 수입원으로 인식하는 동기를 부여하고 있습니다. WirelessCar와 같은 전문 벤더들은 현재 OEM이 데이터법을 운영할 수 있는 지원 툴키트을 제공하고 있으며, 도입 일정을 앞당기고 있습니다. 규제가 강화되는 가운데 공장 출고시 장착 유닛이 표준화되어 대응 가능한 애프터마켓이 축소되고, 텔레매틱스 시장의 재편이 진행되고 있습니다.

보험사들은 실시간 운전 데이터를 활용하여 인구 통계에 기반한 가격 책정에서 행동 기반 가격 책정으로 전환하고 있습니다. 인튜이트는 젠드라이브의 분석 기능을 크레딧 카르마(Credit Karma) 앱에 통합하고, 2025년까지 6백만 명의 회원에게 4백만 건의 보험 계약 제안서를 발송하여 주류 규모로 확장할 수 있음을 보여주었습니다. 기아차와 LexisNexis는 EU 27개국에서 운전자 평가 점수 공유 서비스를 시작했으며, GDPR(EU 개인정보보호규정)을 준수하면서 고객 등록을 간소화했습니다. 안전운전자들은 최대 30%의 보험료 할인을 받을 수 있으며, 소비자 수요를 유발하는 동시에 보험사의 손해율 개선에 기여하고 있습니다. 캠브리지 모바일 텔레매틱스는 연료 소비량 평가를 추가하여 보험사가 안전 운전뿐만 아니라 친환경 운전도 평가하게 된 것을 입증했습니다. 이러한 발전은 데이터 중심의 인수 업무를 강화하고 텔레매틱스 시장의 성장을 가속화하고 있습니다.

유엔 유럽경제위원회 WP.29는 자동차 제조업체가 차량 수명주기 전반에 걸쳐 인증된 사이버 보안 관리 시스템을 운영할 것을 의무화하고 있습니다. 컴플라이언스를 준수하기 위해서는 지속적인 모니터링, 사고 보고, 안전한 업데이트 채널이 필요하며, 이로 인해 엔지니어링 비용이 증가하고 개발 주기가 길어지고 있습니다. ISO/SAE 21434는 수명주기 리스크 관리 절차를 추가하고, 미국에서는 현재 특정 국가로부터의 커넥티드카 부품 조달을 금지하고 있으며, 공급망 감사를 의무화하고 있습니다. 하만과 같은 벤더들은 OEM 업체들이 인증 획득을 위한 컨설팅 업무를 전개하고 있으며, 이는 컴플라이언스가 엔지니어링 업무에서 비용 항목으로 변모하고 있음을 보여줍니다. 중소 공급업체들은 이러한 비용 부담으로 인해 어려움을 겪을 수 있으며, 텔레매틱스 시장으로의 신규 진입이 둔화될 수 있습니다.

2025년 기준 애프터마켓 솔루션은 텔레매틱스 시장 점유율의 56.30%를 차지할 것으로 예상되며, 이는 개조 차량과 혼합 차량에서 애프터마켓 솔루션의 역사적 역할을 반영하고 있습니다. OEM 시스템은 2031년까지 연평균 복합 성장률(CAGR) 11.62%로 빠르게 성장하고 있으며, 보다 깨끗한 데이터 스트림과 원활한 보증 통합을 위한 공장 연결 기능으로 전환하고 있습니다. 텔레매틱스 시장은 이 두 가지 채널 구조의 혜택을 누리고 있습니다. 왜냐하면 구형 차량은 여전히 개조 장치가 필요한 반면, 신차는 생산 라인에서 커넥티드 상태로 출고되기 때문입니다.

애프터마켓용 eCall의 규제 표준화로 인해 제3자 프로바이더의 존재 의미는 유지되지만, EU 데이터법 등 OEM 데이터 공유 규정은 임베디드 채널을 우대합니다. 자동차 제조업체가 커넥티드카 구독을 상용화함에 따라 다운스트림 가치의 획득이 진행됨에 따라 애프터마켓의 이익 여지가 축소될 것입니다. 이에 따라 텔레매틱스 시장에서의 지위 유지를 위해 분석 기능과 멀티 플릿 대응력을 강화하고 있습니다.

2025년 기준 텔레매틱스 시장 규모의 47.80%를 차지하는 임베디드 유닛은 12.94%의 연평균 복합 성장률(CAGR)로 가장 높은 성장률을 보일 것으로 예측됩니다. 이러한 전환은 예측 유지보수, 전기자동차 배터리 관리, 규제에 따른 데이터 공유 의무 등 차량에 대한 심층적인 통합이 필요한 요소들에 의해 추진되고 있습니다. 비용 중심의 차량에서는 스마트폰 기반 솔루션도 효과적이지만, 성능과 데이터 정확도에서는 임베디드 아키텍처에 비해 떨어집니다.

차량 운영자들은 전기 차량에서 에너지 비용을 55% 절감하는 스마트 충전 알고리즘과 같은 미션 크리티컬한 분석을 위해 임베디드 하드웨어를 선호합니다. 5G 모듈이 표준화됨에 따라 V2X 및 고정밀 위치추적과 같은 고급 용도에서 임베디드 솔루션이 주류가 되어 텔레매틱스 시장에서 전략적 중요성을 더욱 확고히할 것입니다.

유럽은 2025년 31.95%의 점유율로 텔레매틱스 시장을 이끌었습니다. 이는 의무화된 eCall, GDPR(EU 개인정보보호규정)에 의한 보호, 2028년까지 2,760만 대에 달할 것으로 예상되는 차량 관리 장치 설치 기반에 의해 지원되고 있습니다. 2025년 시행되는 EU 데이터법은 데이터 공유를 의무화하고, 프라이버시 보호를 유지하면서 제3자 서비스의 새로운 물결을 촉진할 것으로 예측됩니다. 공급업체들은 보다 엄격한 통합 및 컴플라이언스 요구사항을 충족시키기 위해 콘티넨탈의 'Aumovio'와 같은 커넥티비티 스위트를 브랜드화하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 2031년까지 연평균 복합 성장률(CAGR) 12.26%를 나타낼 것으로 예측됩니다. 인도의 AIS 140 의무화와 정부의 100 루피(1,200만 달러) 규모의 지형공간 투자가 기반이 되는 지도 인프라를 확충할 것입니다. 중국의 새로운 운전 지원 안전 규정도 OEM의 커넥티비티 기준을 높이고 있습니다. 급속한 도시화와 대규모 상용차량 증가는 수요를 창출하고, 세계 벤더들을 현지 파트너십으로 이끌며 지역 전체 텔레매틱스 시장 규모를 확대시키고 있습니다.

북미는 성숙한 시장임에도 불구하고 지속적으로 성장하고 있으며, ELD 의무화, 미국 연방조달청의 Geotab사와의 40만대 규모의 정부 차량 도입 계약 등 정부 차량의 대규모 도입에 힘입어 성장세를 이어가고 있습니다. 아메리카 지역의 차량 관리 유닛은 2028년까지 4,300만 대에 달할 것으로 예측됩니다. 특정 외국산 부품을 제한하는 공급망 보안 규정으로 인해 하드웨어 비용이 상승할 수 있지만, 동시에 국내 반도체 투자를 촉진하고 텔레매틱스 시장에 대한 장기적인 공급 안정화로 이어질 수 있습니다.

The telematics market was valued at USD 52.93 billion in 2025 and estimated to grow from USD 58.14 billion in 2026 to reach USD 92.93 billion by 2031, at a CAGR of 9.86% during the forecast period (2026-2031).

Regulatory mandates, especially eCall in Europe and AIS 140 in India, are compelling automakers and fleets to embed connectivity at the factory level, which accelerates OEM demand. Semiconductor content per vehicle is set to double by 2030, raising hardware costs yet enabling richer data streams that underpin advanced analytics. Usage-based insurance programs, powered by real-time driving data, are expanding quickly across North America and Europe, reinforcing the business case for connected cars. Rapid adoption of 5G and edge computing is transforming telematics from simple tracking to predictive maintenance and vehicle-to-everything communication. Rising cybersecurity compliance costs under UNECE WP.29 and ISO/SAE 21434 are pressuring smaller vendors but giving well-capitalized players a competitive edge.

Automakers are integrating telematics directly into vehicle electronics to meet new data-sharing rules such as the EU Data Act, which applies from 2025 and obliges manufacturers to open vehicle data to third-party service providers. Geotab's collaboration with Volvo Cars lifts its OEM integrations to more than 157 brands, proving that embedded connectivity is scaling quickly. Analysts estimate connected services could yield USD 1,600 revenue per car, incentivizing automakers to treat data as a profit center. Specialized vendors like WirelessCar now offer compliance toolkits that help OEMs operationalize the Data Act, accelerating rollout timelines. As regulations tighten, factory-fitted units are becoming standard, shrinking the addressable aftermarket and reshaping the telematics market.

Insurance carriers are shifting from demographic to behaviour-based pricing, fuelled by real-time driving data. Intuit embedded Zendrive analytics into the Credit Karma app, sending 4 million policy offers to its 6 million members in 2025, which demonstrates mainstream scale. Kia and LexisNexis rolled out driver-score sharing in 27 EU countries, simplifying customer enrolment while preserving GDPR compliance. Safe drivers can secure premium cuts of up to 30%, boosting consumer demand and improving loss ratios for insurers. Cambridge Mobile Telematics added fuel consumption scoring, proving that insurers now value eco-efficient driving as well as safety. These advances reinforce data-centric underwriting and amplify the telematics market's growth.

UNECE WP.29 obliges automakers to operate certified Cyber Security Management Systems across the vehicle lifecycle. Compliance demands continuous monitoring, incident reporting and secure update channels, which raises engineering costs and lengthens development cycles. ISO/SAE 21434 adds lifecycle risk-management steps, while the U.S. now blocks connected-vehicle components sourced from certain countries, forcing supply-chain audits. Vendors like HARMAN have built consulting practices to help OEMs navigate certification, showing that compliance is transforming from an engineering task to a line-item expense. Smaller suppliers may struggle to shoulder these costs, slowing new-entrant momentum within the telematics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Aftermarket solutions held 56.30% of the telematics market share in 2025, reflecting their historical role in retrofits and mixed fleets. OEM systems are scaling faster at an 11.62% CAGR to 2031, signalling a pivot toward factory-installed connectivity that delivers cleaner data streams and seamless warranty integration. The telematics market benefits from this dual-channel structure because older vehicles still need retrofit devices, while new cars roll off the line connected.

Regulatory standardization of aftermarket eCall ensures that third-party providers remain relevant, yet OEM data-sharing rules like the EU Data Act favour embedded channels. As automakers commercialize connected-car subscriptions, they capture more downstream value, narrowing the aftermarket's margin pool. Providers are thus emphasizing analytics and cross-fleet compatibility to preserve their position in the telematics market.

Embedded units accounted for 47.80% of the telematics market size in 2025 and exhibit the highest growth at a 12.94% CAGR. The shift is propelled by predictive maintenance, battery management in EVs, and regulatory data-sharing obligations that all require deep vehicle integration. Smartphone-based offerings remain viable in cost-sensitive fleets, but performance and data fidelity lag behind embedded architectures.

Fleet operators prefer embedded hardware for mission-critical analytics such as smart charging algorithms that cut energy expenses by 55% in electric fleets. As 5G modules become standard, embedded solutions will dominate advanced applications like V2X and high-accuracy positioning, cementing their strategic weight in the telematics market.

The Telematics Market Report is Segmented by Channel (OEM, and Aftermarket), Solution (Embedded, Smartphone-Based, Portable/Plug-in), Offering Type (Hardware, Services - Entry-Level, Services - Mid-Tier, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Application (Fleet Management, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe led the telematics market with a 31.95% share in 2025, underpinned by mandatory eCall, GDPR protections, and an installed base of 27.6 million fleet management units projected by 2028. The EU Data Act, effective in 2025, compels data sharing and is expected to stimulate a new wave of third-party services while maintaining privacy safeguards. Suppliers are branding connectivity suites, such as Continental's Aumovio, to meet tighter integration and compliance demands.

Asia-Pacific is the fastest-growing region, forecast at a 12.26% CAGR through 2031. India's AIS 140 mandate and the government's geospatial investment of INR 100 crore (USD 12 million) will broaden foundational mapping infrastructure. China's new driver-assistance safety rules also raise the bar for OEM connectivity. Rapid urbanization and large commercial fleets create volume, pulling global vendors into local partnerships and expanding the telematics market size across the region.

North America maintains a mature but still growing base, helped by ELD mandates and sizeable government-fleet deployments such as the US General Services Administration's 400,000-vehicle contract with Geotab. Fleet management units in the Americas are projected to reach 43 million by 2028. Supply-chain security rules limiting certain foreign components could elevate hardware costs yet may also spur domestic chip investments that stabilize long-term supply for the telematics market.